The Pomp Letter

520 episodes — Page 7 of 11

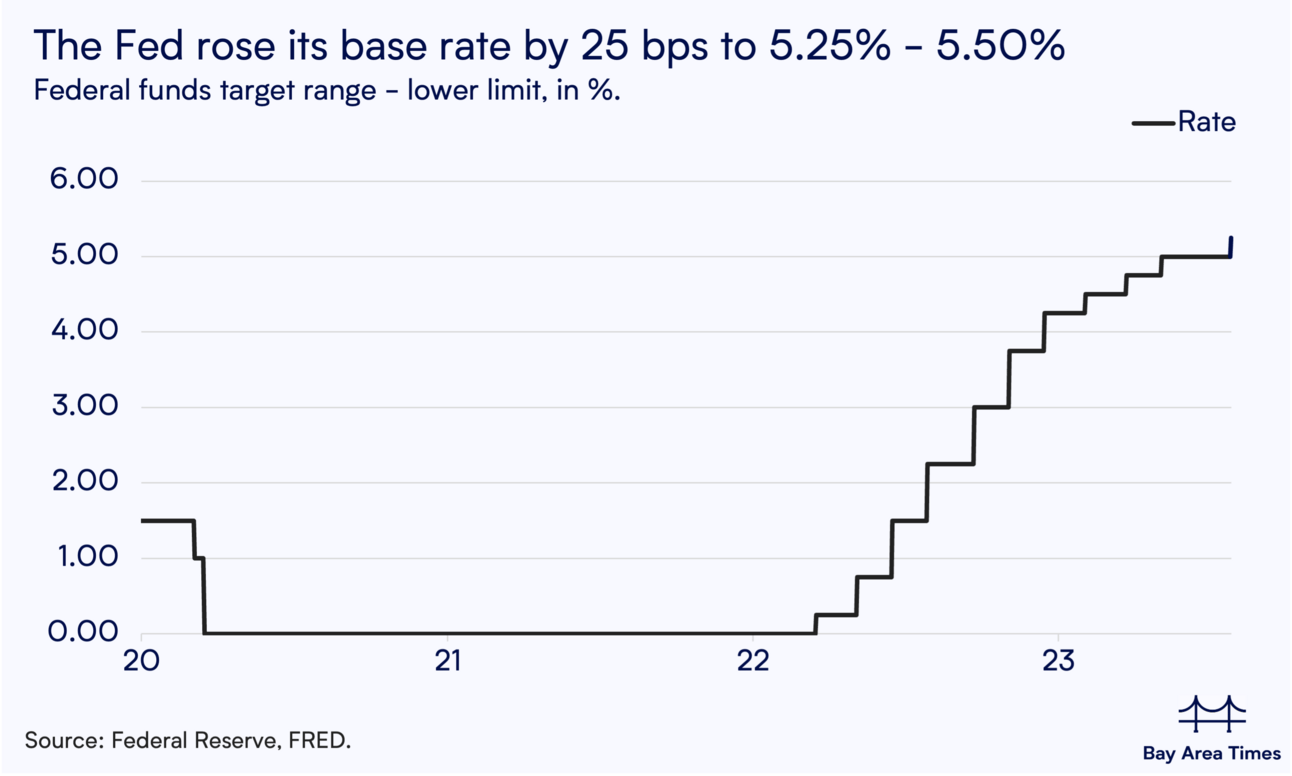

Entrepreneurs Have To Build Since Government Is Spending Like Drunken Sailors

Today’s letter is brought to you by Sidebar!Ready to accelerate your career? As we all know, navigating a big career transition is hard to do. It’s one thing to set a lofty goal, and it’s another thing to have the support system for yourself to follow through.Sidebar is a private, highly vetted leadership program for those who want to do more, do it better, and do it faster. Sidebar’s approach to helping members level up their careers is focused around small peer groups, a tech-enabled platform, and an expert-led curriculum. Members say it’s like having their own Personal Board of Directors. 93% of members say that Sidebar has made a significant difference in their career trajectory."Providing and receiving support from others who play a similar role to you is one of the best ways to grow your capabilities and succeed." - Vice President, Roku“The facilitation has been great. I love the timer bar, the way the conversation is structured, the commitment and accountability.” - Vice President, Clip“I've been impressed by Sidebar’s technology platform. The real time agenda tracker at the top of our weekly meetings really helps the group stay on track.” - Senior Director, MicrosoftNothing will get you further in your career than learning from your peers - it’s a true competitive advantage. Join the growing waitlist of top senior leaders, and apply to become a founding member.To investors,Stanley Druckenmiller is an investing legend. He never had a down year in the three decades that he ran Duquesne Capital Management, while simultaneously achieving investment returns of about 30% annually during the same time period.To say he understands macro economics and financial markets would be an understatement.This is why it is so important to pay attention when Druckenmiller calls our attention to an issue. Lately, the famed investor has been on a roadshow of speeches and interviews to warn about the dire financial situation that the United States finds itself in at the moment. There are three big categories that I would put Druckenmiller’s comments in:* The United States has too much debt and should avoid worsening the situation* The United States has a serious spending problem and should cut expenses* The United States should have refinanced the national debt at low interest ratesThis is not the first time that Druckenmiller has raised these concerns, but given the recent explosion in spending (and the increase of $500+ billion in the national debt) he seems to have a renewed interest in surfacing the warning yet again.Rather than spend our time debating the nuances of Druckenmiller’s comments, including controversial analysis related to whether the Treasury could have found a bid in the market for extremely long duration bonds, I want to call out my biggest takeaway—the solution is not going to come from the government. The national debt is over $33.5 trillion according to government measurements. The actual debt, including future entitlements that have been promised, is actually over $100 trillion already. In order to get spending under control, politicians would have to make incredibly difficult decisions that would be unpopular with voters. This would include cutting entitlements (which Druckenmiller has been saying for years) and refraining from sending hundreds of billions of dollars abroad in support of proxy wars.Some of you will read that last sentence and say to yourself, “that is impossible” which highlights the lack of popularity in both decisions. Essentially, politicians would have to do the hard thing that would guarantee that said politician would lose their job at the next election. It would be a personal sacrifice for the future of our country.There are some great Americans who serve in positions of leadership, but the majority of politicians appear to be more interested in gaining and keeping power, rather than sacrificing themselves for the collective long-term good. So I would not hold your breath waiting for decreases in spending, regardless of which political party is in office. Instead, the American people will have a choice. We can either brace ourselves for the economic pain that comes from crippling national debt, a tailwind for higher inflation, and a complete lack of monetary policy discipline, or we can choose to build our way out of the situation through entrepreneurship, innovation, and technology. The default state for any human is entropy. A society is no different. If we do nothing, the economic pain will be brutal. We can look to numerous examples around the world where this has already happened. If we don’t want our fate to follow these failed economies, then we must create a renaissance of innovation. Rebuild our national infrastructure. Rebuild our military industrial base. Create the next 100 companies that reach $1 trillion market cap. Ensure we are the leader in aerospace, bitcoin, artificial intelligence, virtual reality, nuclear power, and a plethora of other important technol

Investors Are Dropping Bonds & Buying Bitcoin?

Today’s letter is brought to you by Trust & Will!Trust & Will is the most trusted name in online estate planning and settlement.The company has helped hundreds of thousands of families create their estate plans, and they’re just getting started. Trust & Will enables every American to create a plan that’s customized to fit their needs, their life, and their legacy.Their mission is to make estate planning simple, affordable, and inclusive.All of Trust & Will’s documents have been designed and approved by estate planning attorneys to meet the highest legal standards. Their process is simple, secure, complete, and customized for your specific needs and state requirements.To investors,The idea of safe haven assets is not new. These are assets that should retain or increase their value during times of uncertainty. Historically, US Treasuries have served as the ultimate safe haven because the bond came with a fixed rate of return if held to maturity and the only way you would not be paid back your principal is if the US government defaulted.Given the low likelihood of this situation, investors have been pouring capital into US Treasuries for decades whenever things got shaky in financial markets.But something weird has been happening over the last two years—US Treasuries are starting to lose their appeal as a safe haven asset. If this trend continues, it will force investors to recalibrate how they think about risk, safe havens, and capital allocation.For example, Arthur Hayes points out that TLT - the US Treasury ETF - is down approximately 16% since Russia invaded Ukraine and the same ETF is down about 3% since Hamas killed hundreds of civilians in Israel. US Treasuries being down in value weeks or months after these geopolitical events would not necessarily be noteworthy if all asset prices were down collectively. You could blame the macro market conditions, certain actions from the Federal Reserve, or claim that investors were spooked across the board. That is not what has happened though.At the same time that US Treasuries are falling in value during uncertainty, bitcoin continues to rise in value. These two assets have decoupled and investors appear to be treating bitcoin as the safe haven asset. In a way, investors are dumping bonds to buy bitcoin.Since the Russia/Ukraine conflict started, bitcoin has appreciated around 50%. Since the Hamas/Israel conflict started, bitcoin is up about 24%. Not only is bitcoin up materially on both time frames, but remember that bitcoin has appreciated at the same time that TLT has gone down. This development is surprising enough that people across the market are starting to verbalize their surprise. Mohamed El-Erian, the Chief Economic Adviser at Allianz, recently was on CNBC and said the following about US Treasuries losing their safe haven status:“We haven't seen the flight to quality and the flight to safety that you would expect, given what's happening in the world…So yes, it should be the safe-haven, it should have already benefited. But the reality is that the 10-year yield today is a good 70 basis points higher than it was before this latest conflict erupted.”El-Erian also pointed out that bitcoin and US equities appear to be the beneficiaries of this trend change, which each asset class becoming more of a safe haven in the minds of investors.In my opinion, US equities will always have a bid in the market. It goes back to the idea of Warren Buffett’s famous line: “Never bet against America.” Whether Buffett is right or wrong, an entire generation of investors are going to heed that advice. The more interesting conversation is around bitcoin. Why is a “risk asset” going up in value during times of uncertainty and tight monetary policy? The simple answer is that investors are starting to recognize that bitcoin is not a risk asset at all. In fact, these professional investors are actually warming up to the idea that bitcoin is the ultimate safe haven asset. As I wrote in March 2021, bitcoin already proved to be the best safe haven asset coming through the first 12 months of the pandemic crisis. But many people, including some of the smartest investors in the market, brushed this price performance off as an anomaly. It is getting harder to do that with each passing day. Take Blackrock CEO Larry Fink as the prime example. He previously said bitcoin was an “index of money laundering,” but has changed his tune in recent months and recently stated that bitcoin was a flight to quality. Fink is not an insane anon on the internet. He is the leader of the world’s largest money manger. So why is Larry Fink and the rest of the financial industry waking up to bitcoin’s role as the ultimate safe haven asset?Bitcoin provides certainty and predictability regardless of what is happening in the world. Whether there is peace or war, and whether we are in loose or tight monetary regimes, bitcoin will continue to produce 900 bitcoin per day until the next halving. At that point, bitcoin wi

Millions Finally Realize Bitcoin Is Certainty In A World Of Chaos

Today’s letter is brought to you by Trust & Will!Trust & Will is the most trusted name in online estate planning and settlement.The company has helped hundreds of thousands of families create their estate plans, and they’re just getting started. Trust & Will enables every American to create a plan that’s customized to fit their needs, their life, and their legacy.Their mission is to make estate planning simple, affordable, and inclusive.All of Trust & Will’s documents have been designed and approved by estate planning attorneys to meet the highest legal standards. Their process is simple, secure, complete, and customized for your specific needs and state requirements.To investors,There is chaos and uncertainty in the world right now. Russia and Ukraine. Hamas and Israel. China and Taiwan. The southern border. Our national debt. Housing affordability. Inflation. A lack of leadership. Undisciplined monetary policy. Loss of trust in mainstream media. The list seems to go on forever.In times of uncertainty, humans have a desire to take action so they can feel some semblance of control. This is most obvious in central bank’s constant reaction to whatever is happening in the world. If an outlook looks bleak, they will cut interest rates and print money. If an outlook looks strong, they will raise interest rates and sell assets off their balance sheet. The entire world runs off a reactive monetary policy which requires humans to understand complex situations, while predicting how their decisions today will affect the future.This is not only insane, but it has proven to be nearly impossible over the years. Humans are horrible at understanding complex situations. Try to get a group of people to agree on how to handle Russia, Hamas, our national debt, or inflation. It won’t happen. Thankfully, the world is realizing we have another option—bitcoin. The decentralized currency benefits from an algorithmic monetary policy that has become the most disciplined central bank ever created. Bitcoin’s monetary policy does not change, regardless of what happens in the world. Changes in geopolitics, consumer demand, or articles in the media can not influence what the software is designed to do. The idea of a disciplined central bank becomes incredibly important in a world filled with undisciplined central banks, which are obviously unprepared to deal with the ever-changing cocktail of chaos and uncertainty. Don’t take my word for it though. The market is screaming this message at the moment. Bitcoin’s price has appreciated more than 20% in the last 7 days. Some of that appreciation is due to speculation around the spot bitcoin ETF approval, but some of the global interest is being driven by the increasing global chaos and uncertainty. There is never one single thing that drives the movement of asset prices and bitcoin is no different.Upon further analysis, you will find some very interesting data points regarding bitcoin. For example, Dylan LeClair pointed out that treasury bonds are now down more than bitcoin. Think about that for a second. We have been told for decades that bonds were the safe investment. People flee to bonds in times of chaos and uncertainty. At least that is what the market analysts, investors, or economists would tell you.Again, the market is telling us something different. We have to listen or we risk misunderstanding the current situation.Another interesting data point related to the recent rise in bitcoin is how China’s current economic environment could be impacting the digital currency. Tyler Durden points out that “every time China FX outflows surge, bitcoin erupts.”This chart shows an acceleration of capital flight from China last Friday, which is quickly followed by the recent price appreciation of bitcoin. Chinese investors are not the only ones participating in the fun though. Speculation around a spot bitcoin ETF in the United States continues to drive significant interest domestically as well. Yesterday, news broke that Blackrock has successfully obtained a CUSIP number for their bitcoin ETF (normal part of the process) and they also amended their filing to state an intention of seeding the fund with capital before the end of October.Neither of these developments are a surprise, but any updates or movement on the ETF front will continue to elicit interest from various groups anticipating the spot bitcoin ETF approval. As if these data points were not enough, the bitcoin supply is highly illiquid at the moment. The total supply held by long-term holders is the highest it has ever been in history. More than 56% of all bitcoin in circulation has not moved in the last two years, which is despite the volatility associated with an approximately 80% drawdown in price from the previous all-time high of $69,000.That is a level of conviction from bitcoin holders that can not be found in any other financial asset. Because of this market illiqudity, Bloomberg’s Jamie Coutts points out:“For half a year, this

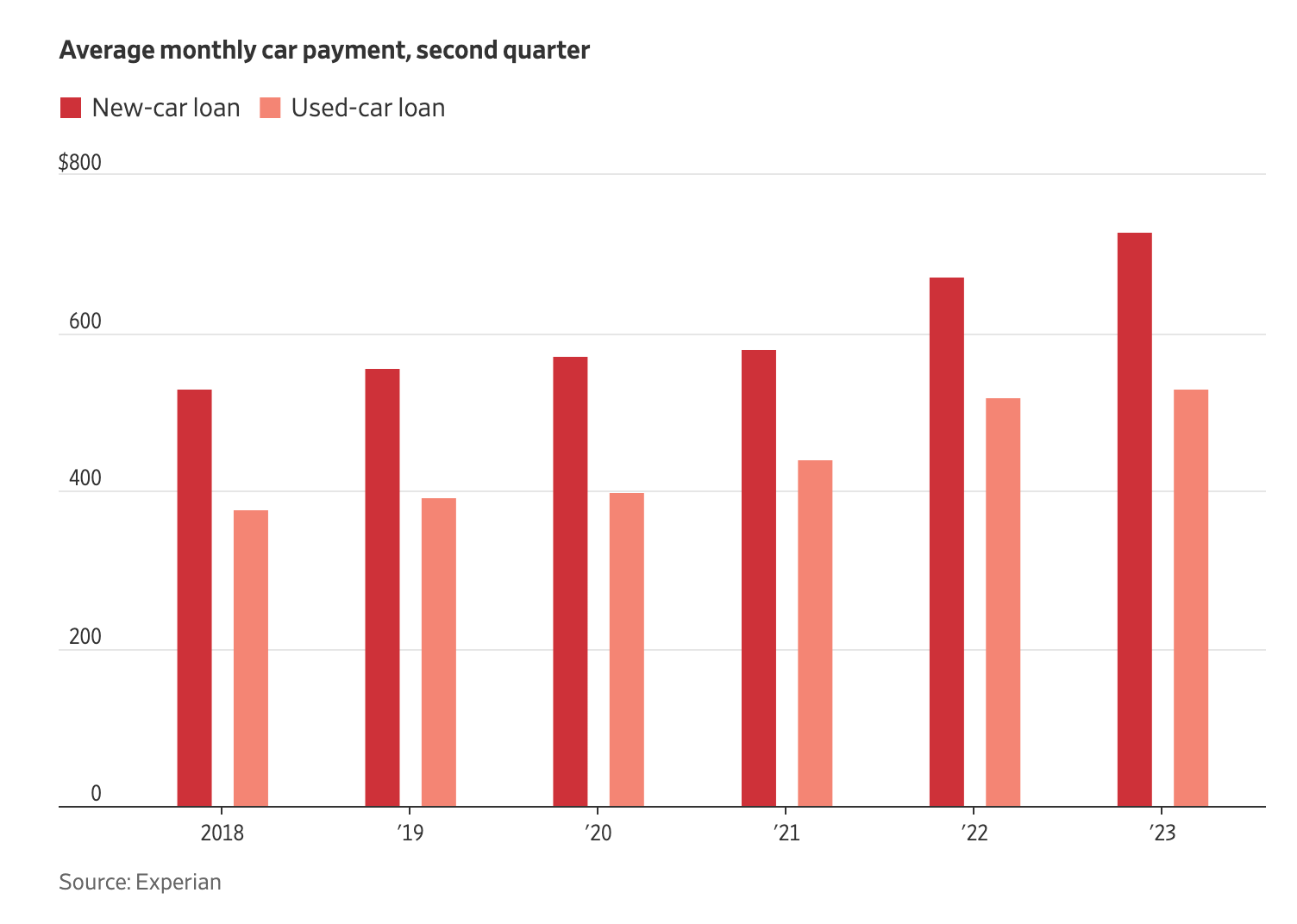

US Consumers Are Economic Punching Bags

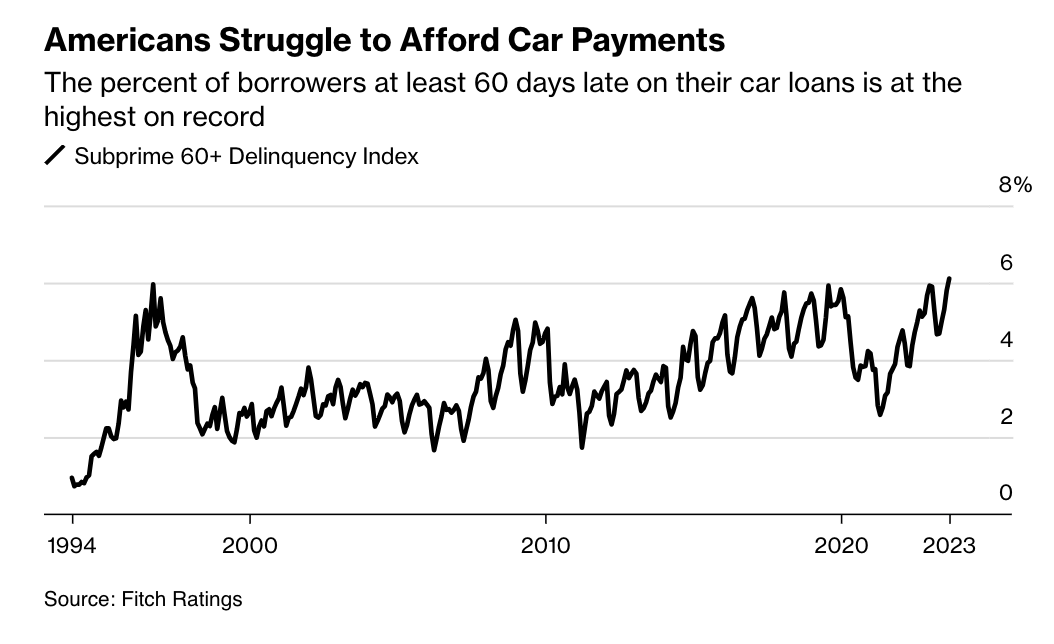

Today’s letter is brought to you by Trust & Will!Trust & Will is the most trusted name in online estate planning and settlement.The company has helped hundreds of thousands of families create their estate plans, and they’re just getting started. Trust & Will enables every American to create a plan that’s customized to fit their needs, their life, and their legacy.Their mission is to make estate planning simple, affordable, and inclusive.All of Trust & Will’s documents have been designed and approved by estate planning attorneys to meet the highest legal standards. Their process is simple, secure, complete, and customized for your specific needs and state requirements.To investors,The Federal Reserve pledged to “destroy demand” in early 2022 when they revealed their plan to begin hiking interest rates. For once, the Fed did what they said they would do and their actions had the intended consequences on the American consumer. These rate hikes did not simply destroy demand, but rather they turned the American consumer into an economic punching bag.For example, we can look at car loans. Financing for new cars can range from just over 5% for a great borrower (based on credit score) to 14% for the worst credit scores. Used car loan interest rates are slightly over 7% for the best borrowers and more than 21% for those on the other end of the quality spectrum. Imagine paying 21% interest on a loan for a used car — insane. These rising interest rates are forcing borrowers to miss their payments at a record rate. Claire Ballentine at Bloomberg writes “the percent of subprime auto borrowers at least 60 days past due on their loans rose to 6.11% in September, the highest in data going back to 1994, according to Fitch Ratings.”It makes sense that more consumers will fall behind on their payments as the payments become more expensive. But remember, majority of Americans need their car to get to work, school, the grocery store, etc. These are usually not exotic purchases, especially at the subprime level, rather they are for a car that is essential to the livelihood and survival of the owner. The Fed’s interest rate hikes has beaten up car owners.This is not the only place we can see this issue. Credit card delinquencies have been an interesting development. The second quarter credit card delinquency rate sat at 2.8%, which is not particularly concerning given that the delinquency rate was 6.8% during the Global Financial Crisis. The concerning aspect is how quickly the rate has almost doubled from 1.6% in 2021 to 2.8% in 2023.You can see the historical context and the rate of rapid acceleration in these charts from the St Louis Fed. Speaking of Fed data, one of the wildest charts is how depleted the personal savings of the American consumer has become. As interest rates have risen, coupled with the persistent appreciation of consumer good prices, citizens have to spend the money that is available to them, including from their hard-earned savings. The last time that the personal savings rate was this low? Leading up to the Global Financial Crisis. That doesn’t exactly instill confidence in market participants who are watching the American consumer get punched over and over again from every angle as interest rates rise.Related to consumer prices, food continues to be an area of concern for the American consumer as well. We have seen inflation ravage this area of citizen’s budget. There were times in the last 12 months where food prices has increased by more than 10% over the preceding year. According to the most recent data, food prices are up almost 4% in the last 12 months, which is slower growth than we have had previously, but the dirty secret is that none of the past price increases to food are going to be rolled back. Once food prices increase, they create a new normal at the elevated level.As Bloomberg showed, food price growth can fluctuate from year-to-year but the aggregate prices of food only continues to grow at a ridiculous rate. Food prices grow faster than wages, so people have a more difficult time affording food each year. This is just another example of the American consumer becoming a punching bag for the US economy. There is no end in sight for the economic pain that citizens are feeling right now. To make matters worse, there is an elevated chance of a recession on the horizon, which would punish consumers who are already in a precarious financial position. The Fed’s mandate to get inflation under control has worked to a degree, but there are concerns that much of the “wins” that have been attributed to the Fed can be explained by high base effects in the CPI numbers. Regardless of whether you think the Fed has done a good job or a bad one, it is objectively true that the American consumer is on the losing end of the current economic situation. We didn’t even get into the fact that according to the US government’s data, $1 in 2020 is worth only $0.83 today. These economic data points showcase why Ameri

The National Debt Should Fear A Recession

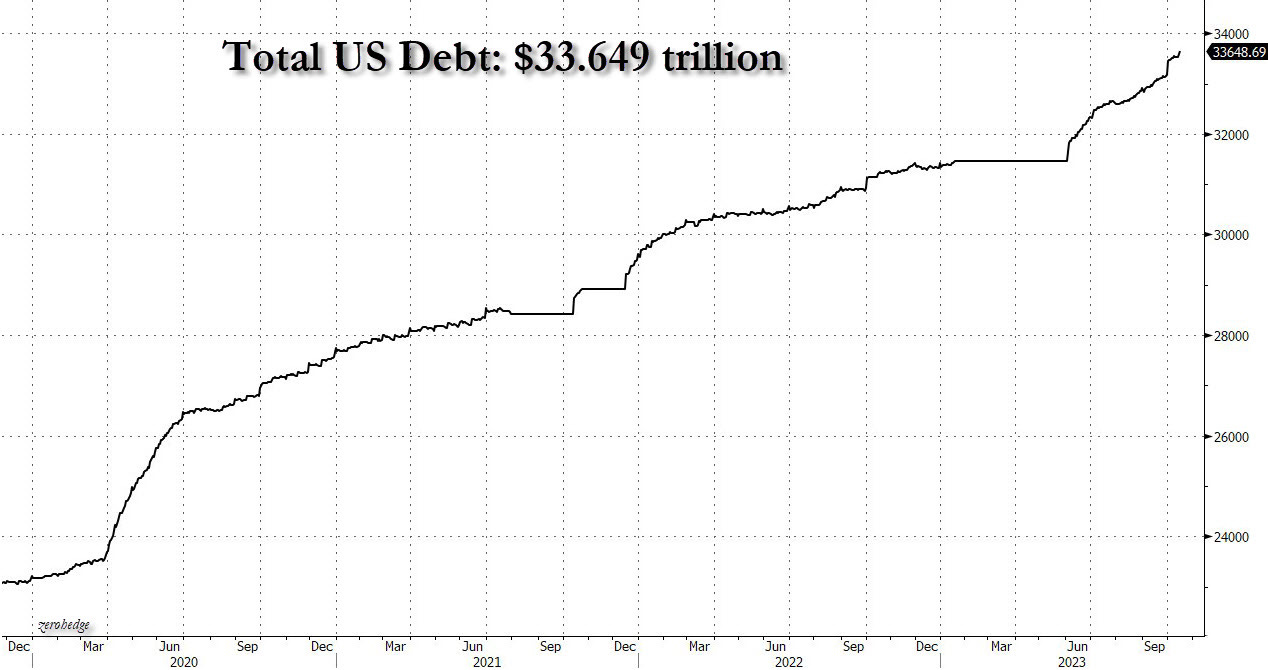

Today’s letter is brought to you by Sidebar!Ready to accelerate your career? As we all know, navigating a big career transition is hard to do. It’s one thing to set a lofty goal, and it’s another thing to have the support system for yourself to follow through.Sidebar is a private, highly vetted leadership program for those who want to do more, do it better, and do it faster. Sidebar’s approach to helping members level up their careers is focused around small peer groups, a tech-enabled platform, and an expert-led curriculum. Members say it’s like having their own Personal Board of Directors. 93% of members say that Sidebar has made a significant difference in their career trajectory."Providing and receiving support from others who play a similar role to you is one of the best ways to grow your capabilities and succeed." - Vice President, Roku“The facilitation has been great. I love the timer bar, the way the conversation is structured, the commitment and accountability.” - Vice President, Clip“I've been impressed by Sidebar’s technology platform. The real time agenda tracker at the top of our weekly meetings really helps the group stay on track.” - Senior Director, MicrosoftNothing will get you further in your career than learning from your peers - it’s a true competitive advantage. Join the growing waitlist of top senior leaders, and apply to become a founding member.To investors,The national debt has increased by more than $600 billion in the last month. That is $20 billion every day or $833 million every hour. We are now at a total of $33.65 trillion. It is hard to wrap our heads around how insane this pace has become. Unfortunately, there is no end in sight.At the same time as the debt is exploding higher, the US economy is showing signs of an incoming recession. Take the inverted yield curve as an example — short-term Treasury yields are higher than long-term Treasury yields.Over the last 55 years, every inversion between the 3-month and 10-year yield curve was followed by a recession. The shortest lag between inversion and the recession was 3 months and the longest lag was 15 months.But an economic indicator like yield curve inversion seems to be at odds with the public narrative that a soft landing will be possible, right? Well, Bloomberg recently did a study that showed a rapid increase in articles talking about a soft landing was usually followed by a recession. You can see the large spike in recent articles mentioning a soft landing would suggest that a recession is incoming. Humans are optimistic and like to think that bad things are not on the horizon, but this study shows that we should be fearful when others are not. Anna Wong and Tom Orlik have also pointed out that American household’s savings is beginning to run out. This savings had drastically increased during the quantitative easing period related to the pandemic, but households can only hold on for so long before the money starts to run dry.To recap, we have yield curves inverting, a spike in soft landing articles, and households running out of money — what is the Fed going to do?The answer is easy: If we enter a recession, the Fed will be forced to cut interest rates and print money.Herein lies the problem. The national debt has been growing at a rapid pace, so any additional money printing would only compound the problem. Without this acceleration in debt accumulation, we are on pace to hit $41 trillion by simply extrapolating the last month’s growth rate for the next 12 months.The number gets even more concerning if the Fed is forced to combat a recession in the US economy.As if that situation is not difficult enough to navigate, the Fed is not operating in a vacuum of economic data. The United States is also providing monetary support to two international conflicts in Ukraine and Israel to the tune of hundreds of billions of dollars. Each of those wars does not appear to have a clear objective or end date, so we run the risk of new forever wars putting a financial strain on an already bleak US financial health outlook.Lastly, the United States is going to be faced with hard decisions domestically as well. The southern border has become porous and there are reports that hundreds of thousands of migrants are crossing the border each month. These individuals, who are mostly seeking a better life provided by the democratic and capitalist society of America, are arriving in cities that are ill-equipped to properly support them, which has led to a series of calls from local and state leaders for more federal aid.This obviously adds to the financial strain on the national financial situation and accelerates the national debt issue.There are many people who will argue that the national debt does not matter. We are the controllers of the global reserve currency and we can print money whenever we want. My response is always the same, “if the national debt doesn’t matter, then we should print $500 trillion tomorrow and solve all of our problem

Will We See Interest Rates Cut Aggressively Soon?

Today’s letter is brought to you by Trust & Will!Trust & Will is the most trusted name in online estate planning and settlement.The company has helped hundreds of thousands of families create their estate plans, and they’re just getting started. Trust & Will enables every American to create a plan that’s customized to fit their needs, their life, and their legacy.Their mission is to make estate planning simple, affordable, and inclusive.All of Trust & Will’s documents have been designed and approved by estate planning attorneys to meet the highest legal standards. Their process is simple, secure, complete, and customized for your specific needs and state requirements.To investors,We don’t have to look far to realize that George Soros nailed the concept of reflexivity. Let’s go back to March 2020. The Federal Reserve perceived a major issue, so they conducted two emergency interest rate cuts to arrive at 0%. As any student of reflexivity knows, I use the term “perceived” because it ultimately does not matter whether there was a true crisis on their hands or not. As long as the Fed believed a crisis was on their hands, they were going to act.And act they did.Those emergency rate cuts, coupled with a level of money printing we have not seen in my lifetime, created the perfect storm for an explosion in asset prices. It was a great example of reflexivity…asset prices had fallen from the sky in March 2020 as fear set in, but they came roaring back once everyone realized the world was not ending. That period will likely not be the last example of the 2020s. Here is an interesting question—does the concept of reflexivity suggest the Fed will have to aggressively cut interest rates soon?Maybe.The Fed’s interest rate cuts back in 2020 were met with the reflexive response of the fastest interest rate hikes in history, which started almost exactly two years later in March 2022. Just as fast as rates went down, rates skyrocketed in an attempt to get inflation under control.This boom-bust cycle is the perfect example of what happens when humans, who have been tasked with the impossible job of managing an economy, begin to make rash decisions based on perceived knowledge. If rates went down aggressively, followed by an aggressive raising of rates, should we now expect another round of aggressive rate cuts? I am not positive, but the odds of that scenario appear to be increasing. The decision-making process of Fed officials is not going to change any time soon. These are humans who are forced to make decisions today based on backwards looking data, which is dependent on a perceived understanding of reality. There is a nearly 0% chance that the Fed, or almost any other market participant, could correctly articulate the current economic situation and what is going to transpire over the coming 6-12 months. Ignore Soros’ politics for a second. As I mentioned at the start of today’s letter, he seems to have nailed this idea. Add in the fact that the US national debt is accelerating to the tune of hundreds of billions of dollars per month at the moment, which is partially due to our decision to fund the war in Ukraine, and it is easy to see a scenario where the Fed has to conduct significant quantitative easing to be better positioned to monetize the debt. This analysis doesn’t even include potential future monetary support for Israel or Taiwan either. Think that is not going to happen? President Joe Biden was on 60 Minutes last night confirming his intention to ask Congress for billions of dollars in support of Ukraine and Israel. And Treasury Secretary Janet Yellen said in an interview this weekend that “we can certainly afford two wars.”Interestingly, Yellen did not mention in the interview that the US government almost shut down a few weeks ago because we couldn’t afford to operate domestically for a few days. Not sure what money she thinks we have, unless she is imaging all of the future dollars that the US will have to print out of thin air.That means the debt will have no end in sight.Ok, let’s get back to interest rates. These rates were reflexive from 2020 through 2023. If I was a betting man, I would be willing to bet the odds are over 50% that the Fed will have to reverse course and drop interest rates faster than expected as the government continues to spend like drunken sailors. You can’t have a government engaged in multiple violent conflicts as a financial sponsor if said government is spending more money on national debt interest payments than their defense budget. It is ridiculous that I even need to call that out, but here we are. There are very few people talking about a scenario where rates continue to be reflexive and the Fed is forced to drop interest rates aggressively. The theory of reflexivity suggests more of us should be considering the possibility and the math behind the aggressive growth of the national debt is simultaneously smacking us in the face.Hopefully this letter makes you think more deeply a

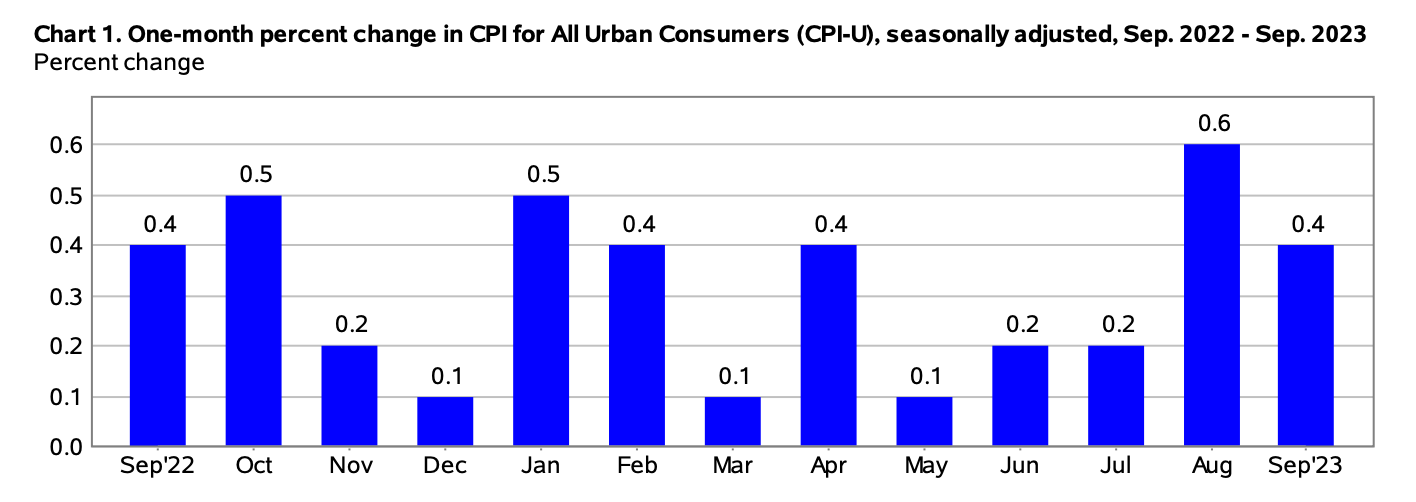

Paul Krugman Is Wrong About Inflation

Today’s letter is brought to you by Dream Startup Job!* Dream Startup Job is the premier marketplace for connecting ambitious job-seekers with the world's most innovative companies.* Search over 1,000 roles and apply quickly to cutting-edge companies like Traba, Varda, Eight Sleep, Flowhub, and many others.* If you're looking to join a team that is making a difference in the world, create a job-seeker profile in minutes and start applying for roles.* If you're a startup, post your open roles today or schedule a call with the Dream Startup Job team by clicking here.To investors,Paul Krugman is a famous economist who teaches economics at the City University of New York. He writes a column for The New York Times. And in 2008, he won a Nobel Prize for his work on international trade and the distribution of economic activity globally. Krugman is also wrong in public A LOT. Take, for example, his analysis of the internet in 1998:“The growth of the Internet will slow drastically, as the flaw in ‘Metcalfe’s law’—which states that the number of potential connections in a network is proportional to the square of the number of participants—becomes apparent: most people have nothing to say to each other! By 2005 or so, it will become clear that the Internet’s impact on the economy has been no greater than the fax machine’s.”This could be cited as one of the all-time great bad takes. Not only does Metcalfe’s law remain intact, but Krugman’s analysis that “most people have nothing to say to each other” highlights a serious misunderstanding of how humans and societies function.Krugman has not been a fan of bitcoin either.He wrote column’s titled Adam Smith hates Bitcoin and Bitcoin is Evil in 2013. The digital currency has appreciated thousands of percent since these inaccurate public declarations. That hasn’t stopped Krugman from doubling and tripling down on his disdain for bitcoin. But nowhere has Krugman’s horrible takes been more apparent than on Twitter/X.Yesterday, Paul Krugman gifted us with one of his best (worst!) takes in years. He tweeted a chart of CPI excluding food, energy, shelter, and used cars, while exclaiming that the war on inflation is over.This is so ridiculous that it may not be worth responding to, but I honestly can’t help myself. The first problem is that Krugman is correct inflation is down as long as you don’t include anything we actually need to live, such as food, energy or shelter. That horrific take alone should be disqualifying, but I’m not done yet. As for Krugman’s comment that “we won at very little cost,” he must be forgetting that we widened the income inequality gap, made housing unaffordable, and destroyed billions in retirement savings over the last three years. Again, not a big cost as long as you aren’t one of the hundreds of millions of Americans being affected by the undisciplined monetary policy coming from the Federal Reserve. Lastly, the Bureau of Labor Statistics would like a word with the perpetually wrong economist regarding his commentary that the war on inflation is over. We saw a 0.6% increase in the month of August and a 0.4% increase in September of this year. Not many people are arrogant enough to claim victory when inflation is still increasing by half a percent each month. Now I don’t want to be too harsh on Paul Krugman. Everyone, including myself, is wrong in public if you play the investment game long enough. We shouldn’t condemn someone for inaccurate thoughts or predictions, especially since we are all trying to learn alongside each other, but we should vehemently call out the intellectual dishonesty that comes from a tweet like Krugman’s yesterday. The inflation concern is not over. Our national debt is exploding to the tune of hundreds of billions of dollars per month at the moment, so the Federal Reserve and US government will be forced to debase the dollar in response given enough time. That easing of monetary policy, coupled with the recent month-over-month increases in CPI metrics, should be a word of caution to every economist. Paul, if you’re reading this, buy some bitcoin, slow down on the ridiculous tweets, and stop fighting the inevitable. We either debase the currency to save our country and economy, or we risk falling victim to the same errors of past great civilizations. Hope you all have a great weekend.-Anthony PomplianoDarius Dale is the founder & CEO of 42Macro. In this conversation, we talk about their Weather Model, economy & financial market conditions, how US fiscal policy reacts to conflicts around the world, and how investors can think through various outcomes.Listen on iTunes: Click hereListen on Spotify: Click hereEarn Bitcoin by listening on Fountain: Click hereHow Markets Are Reacting To Global ConflictPodcast Sponsors* Trust & Will - Estate planning made easy. They are fast, secure, and simple to use. Get your will or trust created today.* Auradine - A new bitcoin miner powered by the world’s first 4 nanometer silicon chip techno

Housing Affordability Is The Worst It Has Been This Century

To investors,Housing affordability in the United States has become a national crisis.It is harder to own a home today than it has been in the last 40 years. Approximately 50% of American citizens are 40 years old or younger, so this is the worst housing affordability period in their lifetime thus far. When a national crisis arises, it is imperative that entrepreneurs spring into action. They can use the private market and economic forces to create meaningful change. It only takes a few courageous individuals with a good plan and an appetite for risk to build something that can have national impact. I deeply believe this. That is why we are announcing a brand new company today — ResiClub. My team and I have partnered with the number one residential real estate reporter in the country, Lance Lambert, to create a data-driven media outlet exclusively focused on this market. Lance, formerly at FORTUNE, is widely recognized for his incredible work on housing inventory, residential demand, geographic trends, interest rate changes, and mortgage implications. He has been covering this market for years and brings a level of professional journalism that is desperately needed to tackle a problem that affects millions of Americans.But Lance is not simply covering the market — he is betting his livelihood on this.Lance quit his job at FORTUNE recently to go all-in on this opportunity. He has burned the boats and there is no turning back. This either works or Lance is in a bad spot. That is the exact type of entrepreneur that I like to partner with — one who bets on himself.With his expertise in the housing market, and our expertise in operations, revenue, and growth, we believe that together we can increase awareness about the lack of housing affordability very quickly.Once we raise awareness, we plan to empower market participants with proprietary data products. Lastly, if we are fortunate enough to find success in those two avenues, we may even look to tackle real-world solutions through the building of affordable housing nationally. Before we get there though, we have to nail the media platform. If you are interested in staying on top of the housing market, interest rates, mortgage trends, or inventory impacts, I ask that you subscribe to Lance Lambert’s ResiClub today.The first piece of content will go out later today for subscribers. This will be high-quality information and analysis that you can not find anywhere else.If you aren’t into the housing market, but just want to back a founder who is betting his career on creating something that could solve a problem for many people, you should consider subscribing too. I am excited to work with Lance on this new company. He is the best in the world at what he does. It is going to be fun to turn it into a sustainable business that gives millions of people the information they need to make informed decisions. You can read the full press release below.I hope you join us.-Anthony PomplianoFOR IMMEDIATE RELEASE: Introducing ResiClub: New outlet tracking the U.S. housing market amidst unprecedented affordability challenges In a period characterized by soaring mortgage rates, overheating house prices, and dwindling affordability, October 2023 has emerged as the least affordable month for U.S. housing this century. The scorching pace of house price growth during the pandemic, coupled with a significant spike in mortgage rates from 3% to 7%, has pushed housing affordability beyond the levels seen at the peak of the housing bubble in 2006. Faced with this challenging housing landscape, Lance Lambert and Anthony Pompliano have joined forces to co-found ResiClub, a groundbreaking media and research company dedicated to in-depth tracking, reporting, and analysis of the U.S. housing market. Lance Lambert, the renowned outgoing real estate editor of Fortune Magazine, will lead the charge as ResiClub's editor. Lance Lambert has solidified his reputation as the nation's foremost data journalist and beat reporter in the residential real estate space, bringing a wealth of knowledge and expertise to ResiClub's endeavors. ResiClub's Mission: ResiClub will serve as an indispensable resource for both industry professionals and everyday Americans looking to navigate the complexities of today's housing market. The company's mission is to provide comprehensive coverage and insights into the U.S. housing sector, with a particular focus on: U.S. homebuilders, institutional homebuyers, proptech startups, and regional housing data.Research and Data Analysis: ResiClub will conduct its research, gathering proprietary local market data and producing in-depth analyses that will enable individuals and professionals to make informed decisions in an ever-changing housing environment. Lance Lambert, CEO/editor at ResiClub, expressed his excitement about the launch, saying, "The U.S. housing market is undergoing profound changes, and ResiClub's mission is to be at the forefront of providing insights and info

Global Conflict Will Create More Inflation

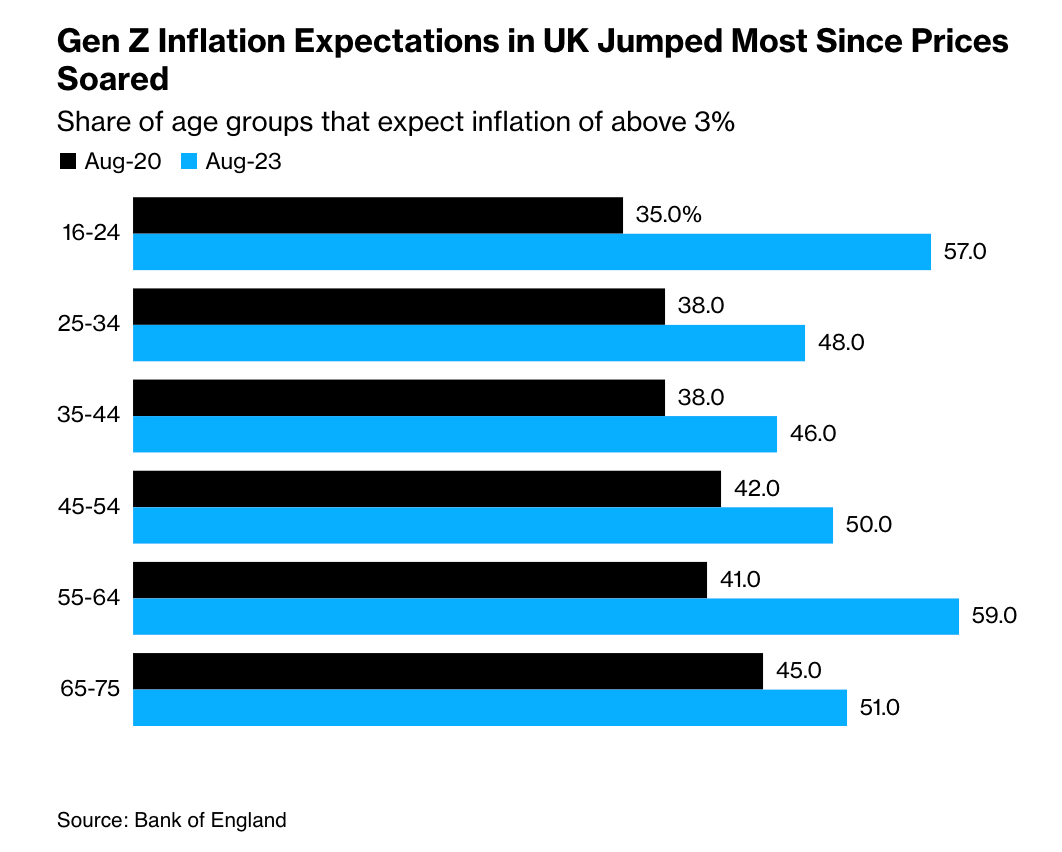

Today’s letter is brought to you by Trust & Will!Trust & Will is the most trusted name in online estate planning and settlement.The company has helped hundreds of thousands of families create their estate plans, and they’re just getting started. Trust & Will enables every American to create a plan that’s customized to fit their needs, their life, and their legacy.Their mission is to make estate planning simple, affordable, and inclusive.All of Trust & Will’s documents have been designed and approved by estate planning attorneys to meet the highest legal standards. Their process is simple, secure, complete, and customized for your specific needs and state requirements.To investors,Tom Rees wrote an article in Bloomberg recently titled, “Gen Z Will Carry the Deepest Psychological Scars From Inflation.” My first reaction was to point out how ridiculous it would be for young people to claim psychological scarring from an economic event. This just reinforces the idea of a generation of kids who have become soft and weak, right?Maybe.Put aside the use of the phrase “psychological scars” and focus on Rees’ larger point—young people have higher inflation expectations than any other generation. That doesn’t seem like such a ridiculous claim. These young people just lived through the highest inflation in decades, while not having a lengthy personal experience living through an economy with low inflation.You can only base your future expectations off your personal experience.The Bank of England conducted a study recently that shows at least 50% of people from ages 16-75, except those 25-44 years old, expect inflation to be over 3% in the future.This makes sense given the older generations lived through the high inflations of the 1980s and the younger generation had their formative years during the high inflation of the 2020s. So why is this important?It has long been the position of central banks that inflation expectations drive inflation outcomes. If a business owner believes higher inflation is on the horizon, then the business owner will begin to raise their prices in anticipation. If a consumer believes inflation is coming, they may start to buy more goods in bulk or change their consumption behaviors. Economies are complex machines. There is no right answer on how to handle these situations. Central bankers have two tools in their toolbox—expand/contract the money supply and increase/decrease interest rates. At the same time that central bankers are trying to manage the economy, which is a nearly impossible task by itself, they will also have to be cognizant of the increasing chaos and conflict around the world.For example, the United States is being forced to drastically increase our national debt in response to our geopolitical strategy. Here is how it works:War breaks out somewhere in the world. Other nations ask the US for weapons & money. The US gives the weapons and money to other nations. Then the US begins to run low on weapons & money. More war breaks out globally because the US is weakened. Other nations ask the US for weapons & money. The cycle repeats. As the US gets weaker, and the world becomes more chaotic, we are forced to increase our national debt at a furious pace in order to pay for all the weapons and money we are giving everyone else. You can see this happening with the conflict in Ukraine already. There has been more than $500 billion added to the national debt in a matter of weeks (not all for Ukraine but a material amount in response to that conflict). Some estimates are that the US will add $1 trillion to the national debt in a single month for the first time in history.This is insanity.Add in the fact that Israel is now asking the US for weapons and money, along with potential conflicts that could kick off in Taiwan and other geographic regions, and it is not hard to see a situation where the US gets stretched thin. We can’t fund every war on Earth without printing ourselves into ruin. You are watching a global chess game between superpowers. China and others never have to enter into direct conflict with the US to secure victory if they can simply watch us bleed ourselves dry. It is imperative we do not repeat the mistakes of the great civilizations that came before us.But here is the crazy part—remember the gen z crowd with high inflation expectations? They are probably going to end up being right. Central banks can not continue to print trillions of dollars annually without driving prices higher. Instead of laughing at the young generation because a journalist used the phrase “psychological scars,” we will be better off trying to understand what the young people know that we don’t.Hope everyone has a great start to their week. I’ll talk to you tomorrow.-Anthony PomplianoEmma Hinchliffe is a senior writer at Fortune, where she covers women in business. She also is the author of the 5-time a week newsletter called "Broadsheet." Emma recently wrote an article "Kim Kardashian turned Skim

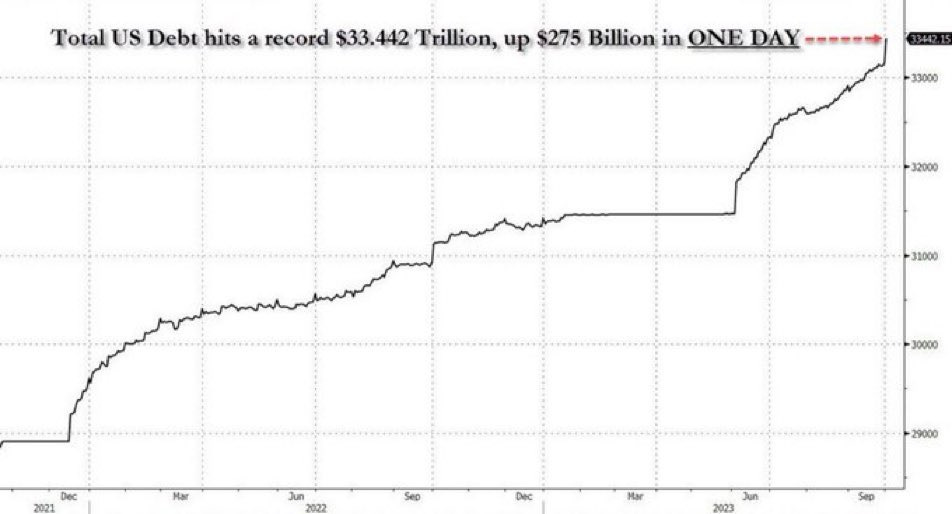

The National Debt Is EXPLODING Higher

Today’s letter is brought to you by Sidebar!Ready to take your career to the next level? Make your transition successful by leveraging a Personal Board of Directors. A trusted peer group, with battle-tested perspective, and proven playbooks, to have real, tactical discussions with to propel you forward.With Sidebar, senior leaders are matched with a small group of highly-vetted, private, and supportive peers to lean on for unbiased opinions, diverse perspectives, and raw feedback. Everyone has their own zone of genius. Together, we’re better prepared to navigate professional pitfalls and push each other to do more, do it better, and do it faster. “Providing and receiving support from others who play a similar role to you is one of the best ways to grow your capabilities and succeed.” - Vice President, Roku“You’re the average of the people you keep closest; Sidebar helps you raise that bar.” - Global Director, Reddit“Tap into a new level of coaching support, professional development, and peer-driven accountability.” - Senior Director, Credit KarmaWhy spend a decade finding your people – join Sidebar today. Join the growing waitlist of over 5,000 top senior leaders, and apply to become a founding member.To investors,The national debt problem is very quickly getting much worse. We saw an increase of $275 billion added to the debt in a single day and as it was pointed out online, the US is on track to add $1 trillion to the national debt in a single month.This is bonkers. The United States now has $33.442 trillion in debt. We have not run a budget surplus since 2001, which means we have had 22 years of mismanagement, regardless of which political party is in power. Last year, the national government collected $4.9 trillion but spent $6.27 trillion. This created a budget deficit of $1.38 trillion, which is the fourth-highest of the 21st century.Not all of the politicians are asleep at the wheel though. Earlier this week, in a story that went largely uncovered, Indiana Congresswoman Victoria Spartz threatened to resign unless a national debt commission is formed. Here was part of her statement:“I’ve done many very difficult things being one woman standing many times with many very long hours and personal sacrifices, but there is a limitation to human capacity. If Congress does not pass a debt commission this year to move the needle on the crushing national debt and inflation, at least at the next debt ceiling increase at the end of 2024, I will not continue sacrificing my children for this circus with a complete absence of leadership, vision, and spine. I cannot save this Republic alone.”That is what we call a strongly worded statement. The problem is just starting though. High interest rates are creating a horrible feedback loop of high interest payments on the national debt. According to Scarlet Fu at Bloomberg:“The US government is currently spending more to pay interest on its $33 trillion national debt than it does on national defense, according to the US Treasury’s monthly statement. In the current fiscal year through August, the Treasury has spent $807.84 billion in interest on its debt securities. The Department of Defense’s outlay for military programs totaled $695.44 billion in the same period.”Spending more money on interest payments than the defense budget seems outrageous. Then again, it is 2023 so are we actually surprised by anything insane these days?I have a confession to make—I was shocked to see $275 billion added to the national debt in a single day. There are few things that surprise me anymore, but that one had my jaw on the ground.I wish I knew the solution. Unfortunately, it appears that a perpetual deficit is the name of the game for the government. You have to wonder if we would even know what to do with a budget surplus if we pulled off a miracle and created one. As the old saying goes, “no one is coming to save you.” You have to start thinking about how you will save, invest, and drive income in a world with an ever-increasing national debt. Because that is exactly where it looks like we are headed.Hope you have a great day. I’ll talk to everyone tomorrow.-PompLulu Cheng Meservey is the Executive Vice President of Corporate Affairs and Chief Communications Officer at Activision Blizzard. This conversation was recorded at the BUILD Summit in New York. In this conversation, Lulu breaks down how you can cut through the noise and make people care about what you're doing, how to tailor your message to people externally & internally, tactics you can use, how to prepare for a crisis way before it comes, and Lulu breaks down why there is no peace time.Listen on iTunes: Click hereListen on Spotify: Click hereEarn Bitcoin by listening on Fountain: Click hereHow To Handle The Mainstream Media As A Startup FounderPodcast Sponsors* Trust & Will - Estate planning made easy. They are fast, secure, and simple to use. Get your will or trust created today.* Auradine - A new bitcoin miner powered by the

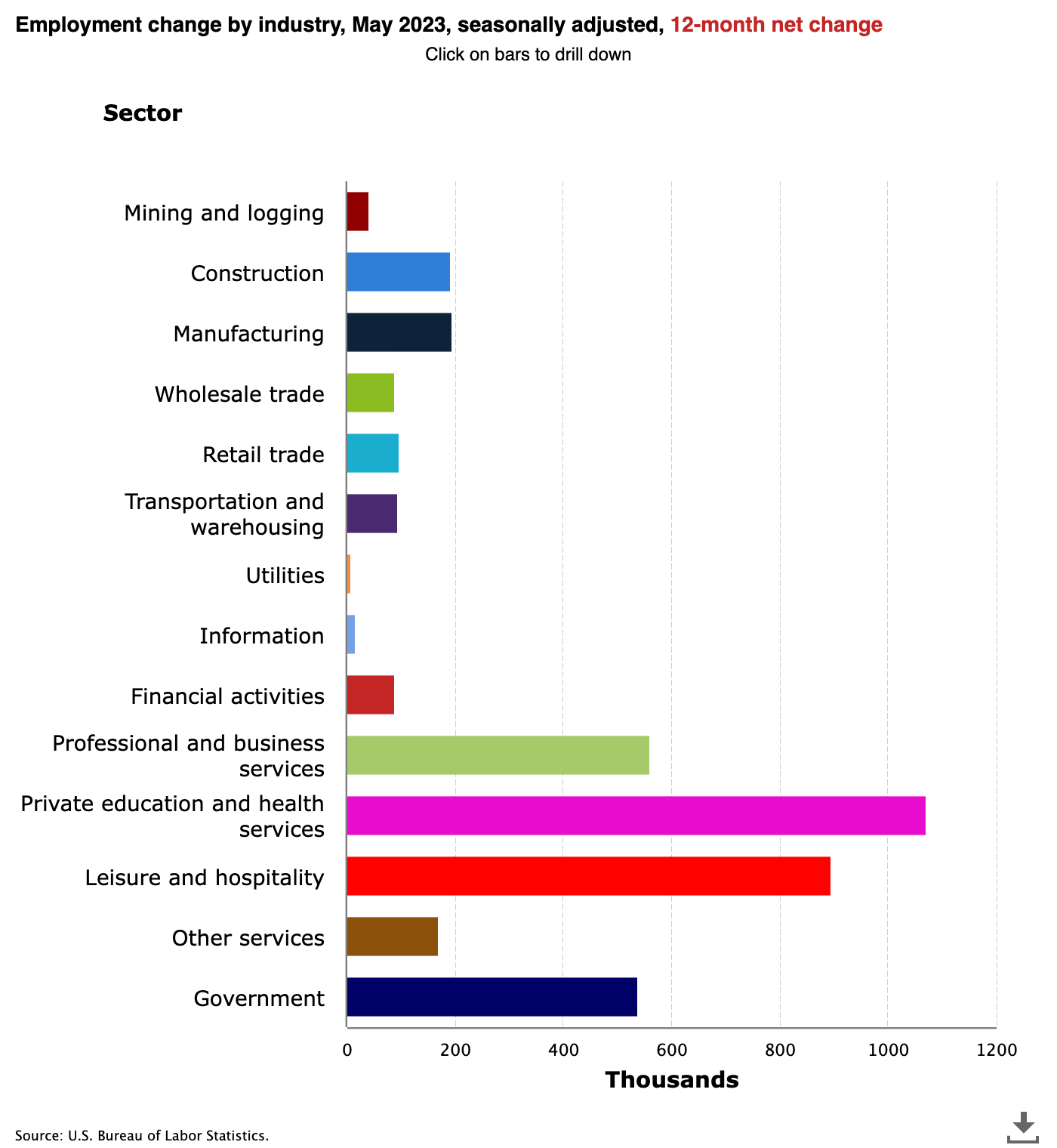

How To Get More People Working In The American Economy

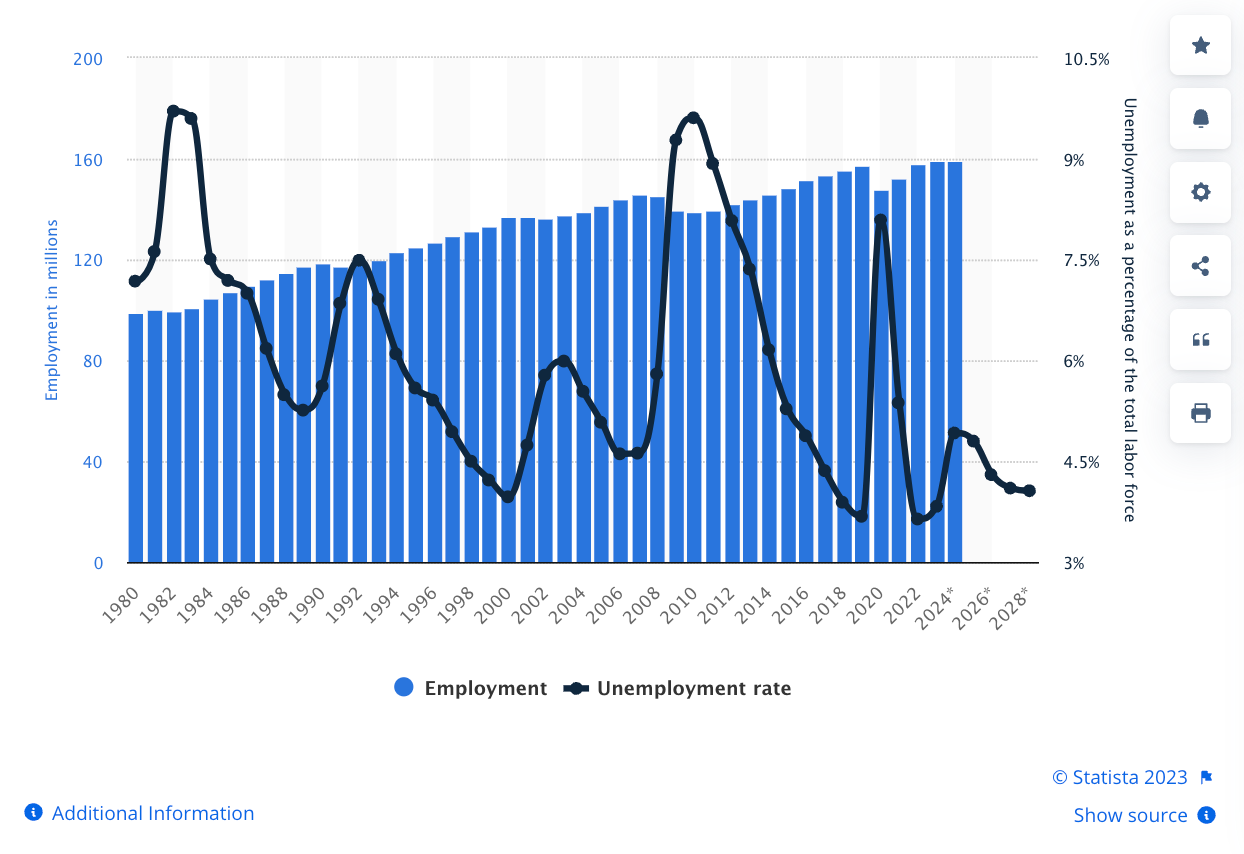

To investors,The number of people employed in the American economy has grown from just under 100 million in 1980 to approximately 160 million today. It doesn’t hurt that the current unemployment rate is sitting at under 4%, which remains near historic lows. Total employment and the unemployment rate in the United States from 1980 to 2022, with projections until 2028Even though unemployment is low and almost half the total US population is employed at the moment, there are still 8.8 million open roles in our country. I believe getting more people to work in the economy can help alleviate a number of problems we face as a society. GDP will grow faster. Companies will make more profits. Wages will increase. The inequality gap will shrink. And the US government will have a smaller burden placed on it for various social services. But I am not merely talking about a problem from afar. For the last two and a half years, my team and I have helped thousands of people get a new job. We lost count last year around 2,000 cumulative new hires and believe the number to be approximately 3,000 people today. Some of these individuals I personally trained so they could upskill and transition into the digital assets industry. Others were able to leverage a job marketplace we built to connect with a new employer. And even more people were placed in their new job by Proof of Talent, a recruiting firm we acquired.Think about this for a second — a small team of less than 20 people were able to help about 3,000 people get a new job over a two and a half year timeline. That is around 3 people per day, every day, for a few years. Imagine what we could do with a broader mandate than just bitcoin and digital assets?Well, we are about to find out. Today we are announcing that our job marketplace is expanding its service area to include any innovative startup company. The marketplace is rebranding under the name Dream Startup Job (website) and it is completely free to use for anyone who wants to get a new job in the startup world. I believe that startups are the single greatest tool we have to change the world. The definition of insanity is a small group of people believing they can create something from scratch that disrupts a group of incumbents and is adopted by millions of people globally. The odds are low, but the potential reward is high. These innovative startups need the best talent they can find. Every job role is applicable. Whether you are an engineer, an operations manager, an accountant, or an entry-level customer service agent, there is a startup out there that is looking for you. If you want to check out some of those open roles, you can now do so at Dream Startup Job.We still have hundreds of open roles at the top bitcoin and digital asset companies, but today we are launching the expansion into industry-agnostic startups with our partners at Eight Sleep, Varda, Flowhub, and Traba. The pool of potential companies to work at is now bigger, so my goal is to eventually help 10 people per day get a new job. Slowly, but surely, we will keep making progress.The more people employed in the American economy, the better off we all are. Hopefully our team can do a small part in cranking that employment rate even higher. If you have ideas on how we can partner, or how we can improve our solutions, please don’t hesitate to reach out. If you would like to list your open roles at your startup, you can do that by clicking here.Have a great day. I’ll talk to everyone tomorrow.-PompAvlok Kohli is the CEO of AngelList. This conversation was recorded at the BUILD Summit in New York. In this conversation, we talk about the culture of shipping speed at AngelList, fundraising environment, how cap tables are usually wrong, treasury management, hiring, private equity, and numerous industry trends.Listen on iTunes: Click hereListen on Spotify: Click hereEarn Bitcoin by listening on Fountain: Click hereHow To Improve Your Startup ImmediatelyPodcast Sponsors* Trust & Will - Estate planning made easy. They are fast, secure, and simple to use. Get your will or trust created today.* Auradine - A new bitcoin miner powered by the world’s first 4 nanometer silicon chip technology.* Velo Data: Do you want faster, easier crypto data? Sign up for Velo Data, a new product that we have been working on to solve this problem.You are receiving The Pomp Letter because you either signed up or you attended one of the events that I spoke at. Feel free to unsubscribe if you aren’t finding this valuable. Nothing in this email is intended to serve as financial advice. Do your own research. This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit pomp.substack.com/subscribe

High Interest Rates Usher In New Normal For Young People

Today’s letter is brought to you by Sidebar!Ready to take your career to the next level? Make your transition successful by leveraging a Personal Board of Directors. A trusted peer group, with battle-tested perspective, and proven playbooks, to have real, tactical discussions with to propel you forward.With Sidebar, senior leaders are matched with a small group of highly-vetted, private, and supportive peers to lean on for unbiased opinions, diverse perspectives, and raw feedback. Everyone has their own zone of genius. Together, we’re better prepared to navigate professional pitfalls and push each other to do more, do it better, and do it faster. “Providing and receiving support from others who play a similar role to you is one of the best ways to grow your capabilities and succeed.” - Vice President, Roku“You’re the average of the people you keep closest; Sidebar helps you raise that bar.” - Global Director, Reddit“Tap into a new level of coaching support, professional development, and peer-driven accountability.” - Senior Director, Credit KarmaWhy spend a decade finding your people – join Sidebar today. Join the growing waitlist of over 5,000 top senior leaders, and apply to become a founding member.To investors,Federal Reserve officials are now saying the quiet part out loud—they intend to keep interest rates high for an extended period of time. This strategy is in-line with the central bank’s commitment to get inflation in the US economy under control. After manipulating the cost of money to 0% for years, the Fed had to reverse course at a record pace. The rise in interest rates from 0% to 5.25% happened at a pace that was never seen before, yet the estimated damage to GDP growth and the labor market never materialized. The economy is still growing and unemployment is under 4%.But consumers are now realizing that a long-term shift has happened in the economy. Originally, many citizens planned to wait out the Fed’s interest rate hikes. They thought they could buy a home or car next year. They could use their savings built up during the pandemic to outlast any negative wage growth. And they saw increased interest rates as a way to drive a little extra income from holding bonds.The problem is that the Fed has been in demand destruction mode for almost two years now and yesterday’s press conference signaled a long-term commitment to keeping rates high. This means the American consumer has a choice. They can continue to put their life on hold for a few more years or they can throw their hands up and subject themselves to more expensive capital. As Gina Heeb pointed out in the Wall Street Journal this morning, consumers are spending more of their income to cover housing costs, being forced to pay more on their car loans, and their credit card debt is exploding higher. Based on this data, it appears that consumers are finally starting to live their lives and deal with the cost of capital increase. This makes sense from a psychology standpoint. It wouldn’t be too difficult to convince someone to put off the purchase of a home or car for a few months, but once you begin to talk about years, people don’t have the patience.The average cost of a home, a mortgage payment, a car loan payment, and other ordinary living expenses will continue to rise nationally as rates remain persistently higher than they have been for the last decade.The interesting part is that current interest rates are not necessarily higher than the historical average, but there is an entire generation of millennials who have spent their adult lives in a low interest rate environment. It had become the new normal. Every investment decision was based on an assumption of low interest rates. So was every purchase decision. Now that rates are higher, and the Fed is signaling a commitment to long-term higher rates, this generation of consumers and investors will have to recalibrate. The irony of the situation is that boomers were slow to acclimate to low interest rates because it was foreign to their lived experience, but now millennials are likely going to be the ones who are slow to acclimate to high interest rates. There is no specific cure to the problem. The pain will continue until young people realize the world has changed and they now live in a new regime. Their investment decisions now have to account for 5% interest rates. Their car and mortgage payments are going to be higher than they anticipated.But that is the price for living today. It may not seem fair, but the worst mistake would be sitting around complaining rather than living life. Time is the most finite resource we get. Letting the central bank steal it from you because they made capital expensive sounds like a bad plan.It won’t be easy for many people to figure it out, especially because we are talking about income and rising expenses, but it is possible. And all we can ask for is a chance to live an extraordinary life that makes us happy. Hope you all have a great day. I’ll talk

"When The Facts Change, I Change My Mind"

To investors,John Maynard Keynes once said, “When the facts change, I change my mind.” This classic investment advice is equally true in our personal lives, so Keynes’ words rang in my head as I left New York City at the end of 2020. The city had become a skeleton of what it once was. I had lived on the island of Manhattan for years and fell in love with the density of ambitious people, the contagious energy of every day life, and the serendipity that comes from packing 8.5 million people into 300 square miles.New York City was home. I never thought I would leave. But here I was leaving the island for South Florida.I didn’t feel guilty. I had given New York a chance during the pandemic. My wife (Polina) and I got married in Manhattan with no guests in July 2020. I was almost late to the ceremony because I was stuck in an Uber that couldn’t get around a miles-long protest. Polina and I stayed in our apartment the entire year. We had not followed in our friends’ footsteps as they fled to rural Airbnbs or returned to their childhood bedrooms for months. We were New Yorkers. And New Yorkers can handle anything. But as weeks turned into months, and months turned into almost a full year, we realized things were only going to get worse in the city that we loved. On a spontaneous trip to see a friend in Miami during November 2020, we decided that we would move to South Florida for the winter. “Just a few months,” we told ourselves. We will come back to NYC once it gets warmer.Newsflash, we never came back. The unconstitutional mandates took hold. The crime got worse. People continued to flee the city in droves. And on the opposite end of the country, Miami was booming. It seemed like someone new was moving to town every day. Founders. Venture capitalists. Hedge fund mangers. Movie stars. Musicians. Professional athletes. You name an industry and someone well-respected from it was moving to South Florida. The good times were rolling.As Polina and I settled into our new Miami life, we felt it was important to be all-in on living there. We bought a home. We bought a car. We had our first child at Jackson Memorial Hospital. We opened up an 8,500 square foot office in the heart of Brickell. It was a real-time creation of the perfect life. Unfortunately, something felt off. We noticed it fairly early into our stint in the suburbs. Could it be a monotony that came with seeing fewer people every day? Did we miss being able to walk to a coffee shop downstairs? Maybe we were just nostalgic about our past life and the addition of a new child was messing with our minds? None of it made sense, but you know when something is off. It took two trips to NYC to realize what had happened. We had used our brains to move to Miami. Every aspect of our new life made rational sense. The weather was amazing. The taxes were low. The business was growing. But our hearts were still in New York City. Every single decision point told us that Miami was the better place to live, yet when we visited New York City, we felt more alive than ever. The city has an energy to it that is impossible to describe if you have never experienced it. We needed to leave to fully appreciate what it really means to live in the greatest city in the world. I was a big believer in Miami’s growth story. I still am. People and capital are still moving to the city. F1 racing. Citadel. Messi. The list goes on and on. But those positive things can be true, while it is also true that Polina and I are personally happier in New York City. As Keynes said, “When the facts change, I change my mind.” We made the decision to move to Miami with our brains. We are making the decision to move back to NYC with our hearts.Dear New York — “We’re back.”If you see me on the street, stop and say hello. Many of you do this already and I love meeting each of you. If you have an event that you’re putting together, send me an invite. If you have a company that is interesting, send me a message. Polina explained her perspective on our move, which I highly suggest reading.And I’ll leave you with a sentence someone recently told us, “New York City is the modern-day Rome.” And that is exactly where I want to be.-PompPeter Johnson is the Co-Head of Venture Investments at Brevean Howard Digital.In this conversation we talk about the epic rise of stablecoins, how they have become the killer app of blockchain technology, where stablecoins are being used, why they are being used, and who is using stablecoins.Listen on iTunes: Click hereListen on Spotify: Click hereEarn Bitcoin by listening on Fountain: Click herePomp’s Appearance on Fox Business with Liz Claman YesterdayPodcast Sponsors* Velo Data: Do you want faster, easier crypto data? Sign up for Velo Data, a new product that we have been working on to solve this problem.* Range - Get started today with code POMP15 for 15% off any quarterly plan for your first year.* Auradine - A new bitcoin miner powered by the world’s first 4 nanometer silicon chi

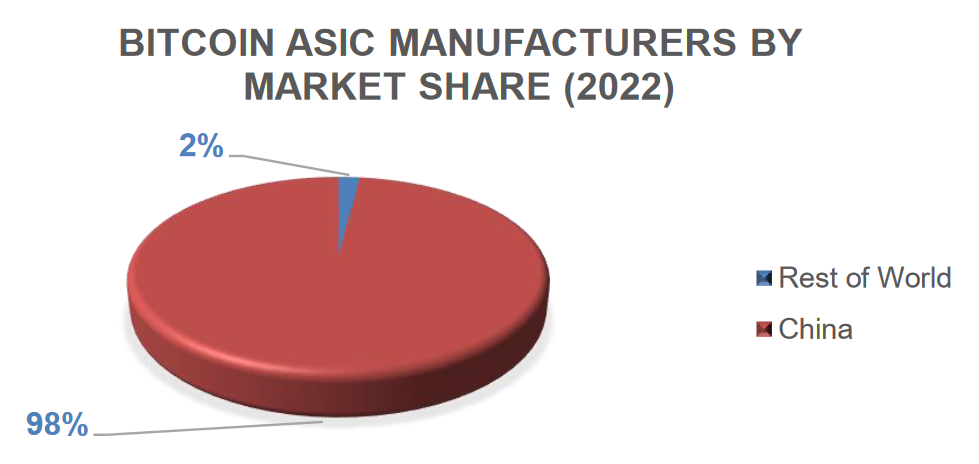

American Companies Must Manufacture Advanced Semiconductors and Systems for Bitcoin Mining

Today’s letter is brought to you by Sidebar!Ready to take your career to the next level? Make your transition successful by leveraging a Personal Board of Directors. A trusted peer group, with battle-tested perspective, and proven playbooks, to have real, tactical discussions with to propel you forward.With Sidebar, senior leaders are matched with a small group of highly-vetted, private, and supportive peers to lean on for unbiased opinions, diverse perspectives, and raw feedback. Everyone has their own zone of genius. Together, we’re better prepared to navigate professional pitfalls and push each other to do more, do it better, and do it faster. “Providing and receiving support from others who play a similar role to you is one of the best ways to grow your capabilities and succeed.” - Vice President, Roku“You’re the average of the people you keep closest; Sidebar helps you raise that bar.” - Global Director, Reddit“Tap into a new level of coaching support, professional development, and peer-driven accountability.” - Senior Director, Credit KarmaWhy spend a decade finding your people – join Sidebar today. Join the growing waitlist of over 5,000 top senior leaders, and apply to become a founding member.To investors,It has become obvious to me that American manufacturing is an essential component of our national security strategy moving forward. We need American companies building American technologies, including semiconductors. As I researched this topic more, I was introduced to the team at Auradine. They are tackling two things I am interested in — American manufacturing and bitcoin mining. The founders are highly successful Silicon Valley entrepreneurs who are dedicating their time and resources to tackle a very difficult problem.I asked Viswesh Ananthakrishnan, Head of Product Management, at Auradine to write a guest post on why it is critical to have US suppliers design & manufacture advanced semiconductors and systems for Bitcoin mining. Here are Viswesh’s thoughts:Advanced semiconductors are crucial components in Bitcoin mining solutions, providing the computational power necessary to solve complex mathematical problems and earn mining rewards in the form of Bitcoins. At present, China has a manufacturing monopoly on ASICs used in Bitcoin mining. However, the size of the Bitcoin mining industry (by market capitalization) outside China is disproportionately much larger.This lopsided distribution shows that even though China may have a stronghold on the manufacturing front, other countries and regions are contributing significantly to the overall growth, development, and profitability of Bitcoin mining. The decentralized nature of Bitcoin allows participants from around the world to engage in mining activities, resulting in a diverse and widespread ecosystem beyond the borders of any single country. It only makes sense that the design and manufacturing of Bitcoin mining ASICs should follow suit.Unfortunately, the US semiconductor industry’s share in global semiconductor production capacity has seen a sharp decline over the last 30 years, falling from 37% to just 12%. This decline has been driven by increased competition from other countries and a lack of investment in domestic manufacturing capabilities. Recent events have demonstrated how vulnerable US businesses are to supply from overseas ASIC manufacturers. The COVID-19 pandemic had a significant impact on the semiconductor supply chain, causing disruptions and shortages that have affected a wide range of US industries.Indeed, it has become crucial for the US to invest in and support its domestic semiconductor industry to ensure long-term growth and stability, in general for the broader economy and also specifically for the Bitcoin mining industry.“Making more semiconductors in the United States […] will strengthen our national security by making us less dependent on foreign sources”– Joe Biden, 46th President of the United States, July 2022In response to these challenges, the Biden-Harris Administration has launched efforts to bring semiconductor manufacturing back to America through the CHIPS and Science Act. While these efforts represent important steps forward, there is still much work to be done to rebuild the U.S. semiconductor industry and ensure its long-term competitiveness.Meanwhile, the economic significance of the Bitcoin mining industry in the US cannot be overstated, with a projected compound annual growth rate (CAGR) of 9.3% between 2023 and 2029, starting at $9 billion in 2022. The maturation of capital markets and the development of financial instruments have played a key role in the quick ascent of the Bitcoin mining industry in the U.S. In recent years, there has been a surge of interest in Bitcoin and other cryptocurrencies from institutional investors. Recently, several asset management firms, including BlackRock and Fidelity, have filed applications with the SEC to launch Bitcoin ETFs.“The role of crypto is digitizing gold. […]

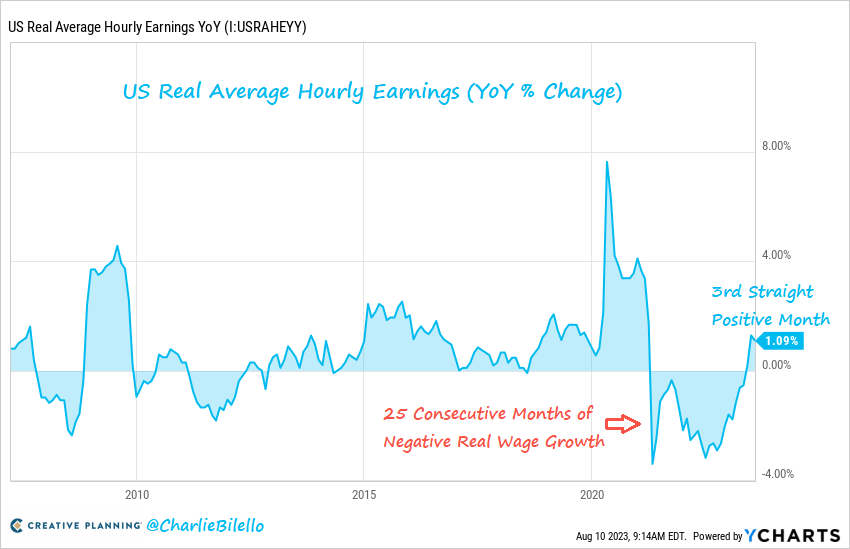

The US Economy Is Drunk & Confused

Today’s letter is brought to you by Sidebar!Ready to take your career to the next level? Make your transition successful by leveraging a Personal Board of Directors. A trusted peer group, with battle-tested perspective, and proven playbooks, to have real, tactical discussions with to propel you forward.With Sidebar, senior leaders are matched with a small group of highly-vetted, private, and supportive peers to lean on for unbiased opinions, diverse perspectives, and raw feedback. Everyone has their own zone of genius. Together, we’re better prepared to navigate professional pitfalls and push each other to do more, do it better, and do it faster. “Providing and receiving support from others who play a similar role to you is one of the best ways to grow your capabilities and succeed.” - Vice President, Roku“You’re the average of the people you keep closest; Sidebar helps you raise that bar.” - Global Director, Reddit“Tap into a new level of coaching support, professional development, and peer-driven accountability.” - Senior Director, Credit KarmaWhy spend a decade finding your people – join Sidebar today. Join the growing waitlist of over 3,500 top senior leaders, and apply to become a founding member.To investors,People have been predicting a recession for months. But the economy doesn’t seem to care. The S&P 500 is up 15% year-to-date and nearly back to all-time highs. Unemployment also remains stubbornly low at 3.5%.As Charlie Bilello points out, “after a record 25 consecutive months of negative real wage growth, wages have now outpaced inflation on a year-over-year basis for 3 straight months. This is a great sign for the American worker that hopefully continues.”But the Federal Reserve is not out of the woods yet. In fact, the Fed is likely in an impossible situation. They have raised interest rates more than 500 basis points in about 18 months, which is the fastest pace on record. Headline inflation has fallen from over 9% to less than 4%, yet there are lingering concerns that inflation could reverse and accelerate again. These inflation fears are largely driven by the fact that numerous economic measurements continue to come in at higher levels than expectations. According to Bloomberg’s Lisa Abramowicz, “investors are throwing in the towel on hopes for near-term central bank rate cuts. Global bond yields are at the highest levels since 2009 as economic data keeps coming in hotter than expected.”She goes on to highlight that “a San Francisco Fed study estimates that US consumers have about $190 billion of excess savings left and that it'll likely be depleted during the current quarter.”Then we can look at something like retail sales — Bilello states “after adjusting for inflation, US retail sales fell 1.3% over the last year, the 9th consecutive YoY decline. That's the longest down streak since 2009. Nominal retail sales increased 2% YoY vs. a historical average of 4.7%.”But Kathy Jones says is more excited about the “large upside surprise in retail sales. Retail sales increased 0.7% vs. an expectation of 0.4% month-over-month. The control group, which feeds into GDP, increased 1.0% vs. an expectation of 0.5%.”So what exactly is going on in the US economy? Are we headed towards good times or bad times? Up or down? Pain or bliss? The short answer is that no one knows. The Federal Reserve has to use these conflicting data points to determine whether they have done enough rate hikes. If they have, then inflation will continue to come down, the Fed will eventually cut rates, and asset prices will continue their decade-long trend of up-only. But if the Fed misjudges this, and they mistakenly pivot now prematurely, then we could see an accelerating inflation trend that catches the central bank unprepared. Jeff Cox wrote for CNBC:“Federal Reserve officials expressed concern at their most recent meeting about the pace of inflation and said more rate hikes could be necessary in the future unless conditions change, minutes released Wednesday from the session indicated.That discussion during a two-day July meeting resulted in a quarter percentage point rate hike that markets generally expect to be the last one of this cycle.However, discussions showed that most members worry that the inflation fight is far from over and could require additional tightening action from the rate-setting Federal Open Market Committee.“With inflation still well above the Committee’s longer-run goal and the labor market remaining tight, most participants continued to see significant upside risks to inflation, which could require further tightening of monetary policy,” the meeting summary stated.”The public narrative in recent weeks has switched from “the Fed will have to continue hiking interest rates and a recession is on the horizon” to “the Fed is done hiking interest rates and the good times are coming back.” These meeting minutes reveal that the central bank has a different view of the economy.It is nearly impossible for a human

These 8 Bitcoin Charts Are Worth Watching

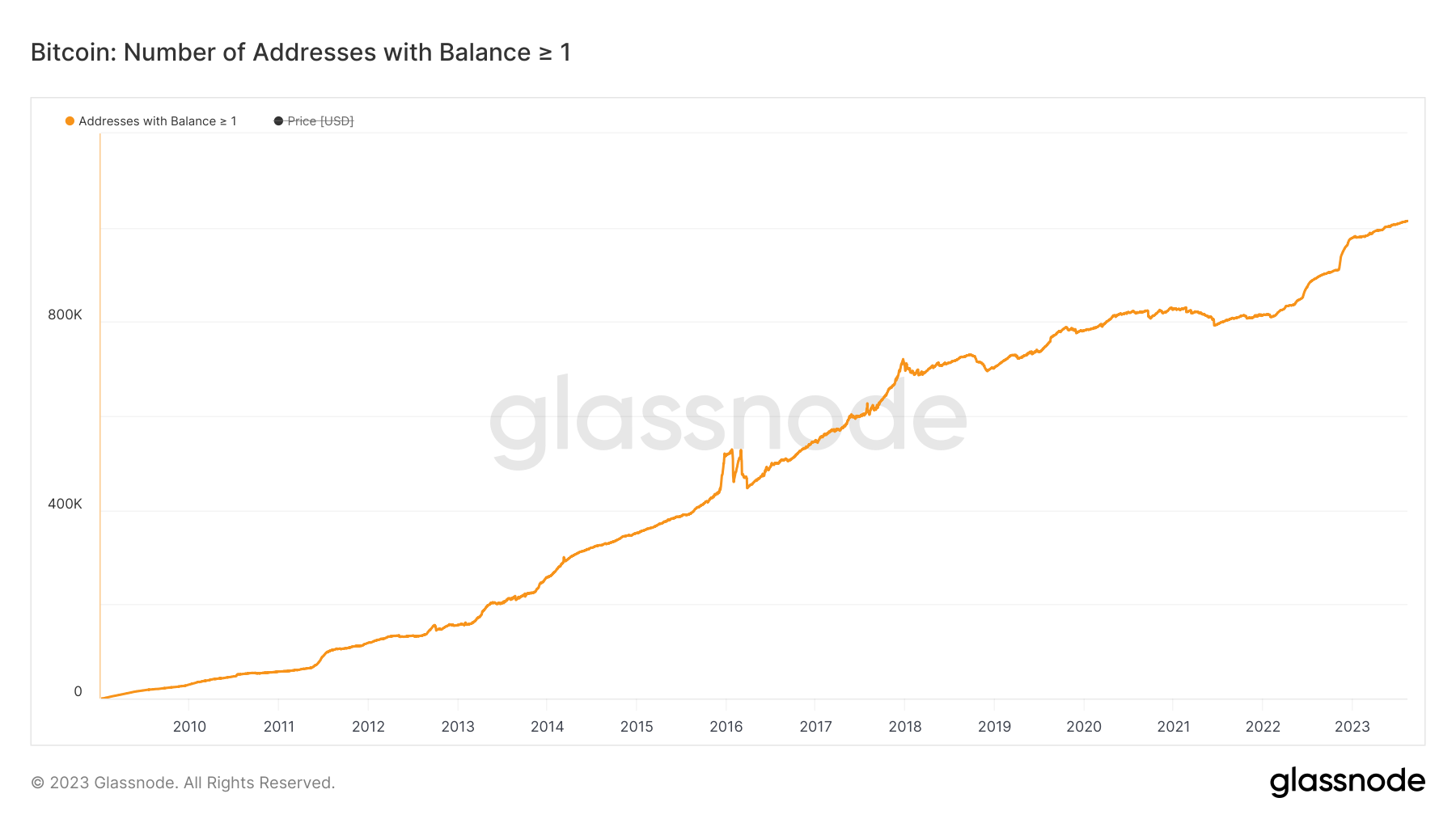

To investors,I found a number of interesting data points while I was digging into the bitcoin market over the weekend. First, there are now more than 1 million addresses on the bitcoin network with at least 1 bitcoin. That is growth of more than 100,000 addresses to this club in less than a year.The percent of bitcoin in the circulating supply that has not moved in the last two years is now at a new all-time high of 56%. This means that more than one out of every two bitcoin in circulation has not moved in two years. The percent of circulating supply that has not moved in 5 years is also at an all-time high of 29%. Over 70% of all bitcoin addresses are “in profit,” which means they acquired the current bitcoin they are holding at a lower price than today’s price point.Although there have been many people selling their bitcoin at a loss in recent months, bitcoin holders who have sold in the last few days are selling at a profit again.Miners had been selling bitcoin throughout the second half of 2022. These same market participants have been buying/holding bitcoin year-to-date. It is a strong sign to see the lack of sell pressure from miners in the market.Using the new data platform Velo Data, we can see the best day for bitcoin futures returns in a given week is Tuesday. The average futures return over the last year on Tuesday is more than double the average return for any other day of the week. Bitcoin is still down more than 50% from the 2021 all-time high in price, but the digital currency’s compound annual growth rate for the last decade remains more than 75%.The narrative over the last few months has been focused on the regulatory environment, along with a continued belief in the mainstream media that bitcoin was a bubble. These data points, along with various fundamental analysis, suggest that bitcoin is actually in a very strong position. Any time you have a highly illiquid asset that could potential see a large influx in demand (Wall Street ETF applications as one example), it is worth paying attention to. The supply/demand lesson you learned in Economics 101 still rules the day.Hope you all have a great start to your week. I’ll talk to everyone tomorrow.-PompAnthony Pompliano breaks down billionaire David Rubenstein’s thoughts on bitcoin, BlackRock, and why he believes bitcoin is not going away.Listen on iTunes: Click hereListen on Spotify: Click hereEarn Bitcoin by listening on Fountain: Click hereJoe Rogan and Post Malone Discuss Risks of CBDCsPodcast Sponsors* Velo Data: Do you want faster, easier crypto data? Sign up for Velo Data, a new product that we have been working on to solve this problem.* StartEngine - Sign up for a StartEngine account today explore live investment opportunities where you can start investing with as little as $100.* Range - Get started today with code POMP15 for 15% off any quarterly plan for your first year.You are receiving The Pomp Letter because you either signed up or you attended one of the events that I spoke at. Feel free to unsubscribe if you aren’t finding this valuable. Nothing in this email is intended to serve as financial advice. Do your own research. This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit pomp.substack.com/subscribe

The Greatest Business Deal of the Last Decade