The Flying Frisby - money, markets and more

612 episodes — Page 6 of 13

The solution to all your Christmas present problems

What are you getting people for Christmas this year?I have the solution.Forgive me for going full salesman, but read on and you’ll see why I do that. This is life mission stuff. First, there are all sorts of goodies in the Dominic Frisby shop, which I think you may like. We have CDs of all my various albums, the latest (and probably best yet) being Gammon and Proud. Digital versions are also available at Bandcamp.There is Contains Swearing, an EP of unbroadcastable songs for the discerning listener. I daren’t release digital versions of this online for fear of the repercussions. You can only get the CD.My other albums are there in the shop too.The best thing I’ve ever doneAnd so we come to Kisses on a Postcard, which is the musical based on my dad’s story of his experiences as a vacky in World War Two, that I’ve been working on for so long. It has been my life’s mission to get this made and I consider it to be, artistically, the best thing I’ve ever done or been involved with.But trying to get people to listen to it has been really hard. In the last few weeks, however, I’ve appeared on Triggernometry, James Delingpole and Lawrence Fox’s shows to talk about it and, suddenly, some real interest has ignited. I am getting constant notifications on my phone telling me we have sold another CD and I have been getting some of the nicest messages“I spent most of today binge-listening to the podcast on the Apple platform and it has been one of the happier days of my life thus far,” Daamini from Dubai“I just wanted to congratulate you on such a wonderful and beautifully touching musical. I was enthralled, I cried, I laughed, I spent my whole Sunday GLUED to this amazing show. A real quality production. I think this should be essential viewing for younger generations. It HAS to be in the West End, just HAS TO BE”. Angela from Ascot.“A heartwarming, delightful musical that keeps you right to the end. The characters are wonderful. There is tragedy, heartbreak, bigotry, compassion, courage, joy and laughter and it is narrated beautifully. Thank you for giving it to us to enjoy, a real gift”. Nat from PenrynPeople really like it - and that’s because it is really good. As I’ve said, artistically, Kisses on a Postcard is the most special thing I have ever been involved with, I urge you, if you haven’t already, to listen.A Kisses on a Postcard CD - first edition - will make the most special Christmas present, especially for anyone you know who was some way connected to the evacuation. The artwork, says Ian from from Cheltenham, is “wonderful. Such a special gift.”So I hope you don’t mind me going full salesman, but you can probably see how much I care about this project. You can find out more at the website here and you can order CDs either there or in the Dominic Frisby shop. Thank you. This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit www.theflyingfrisby.com/subscribe

Developments in the murky world of geo-politics

Some interesting developments in the murky world of geopolitics to report on this week, as the currency wars heat up.WWIII has already started. So says US economist Pippa Malgrem, who was Special Assistant to US President George Bush for Economic Policy and a former member of the President's Working Group on Financial Markets.“We are in a hot war in cold places: Space, Cyberspace, Underwater, and high places, including the Arctic, and the Himalayas, and in proxy conflicts in places the media give a cold shoulder to like Africa.” (Not to mention the Pacific). A cold war in hot places then - as well as a hot war in cold places.We are also, of course, in a very hot currency war.Vladimir Putin goes down the bitcoin rabbit holeThis week, with the aim of limiting Russia’s ability to finance its war in Ukraine, the G7 Nations, the European Union and Australia set a price cap of $60 a barrel on Russian crude oil. This follows the EU's embargo on Russian crude imports by sea, with similar pledges from the US, the UK, Canada and Japan.As you would expect, Russia has said it will not abide by such price caps, even if it has to cut production.Meanwhile, the world’s largest oil importer, China, seems to be slowly opening back up. Cities are easing COVID-19-related restrictions in the wake of recent protests, and it seems the country is set to further relax curbs as soon as today. I think it’s fair to say that if China had not locked down, oil demand would have been a lot higher - and so the oil price would have gone a lot higher. Same goes for metals, in fact most other commodities. And then we have another part of the puzzle. Russia’s President Vladimir Putin did his best bitcoin maximalist impression last week, as he called for an international, independent, blockchain-based settlement network. (Spoiler alert: it already exists. It’s called bitcoin).“The technology of digital currencies and blockchains can be used to create a new system of international settlements that will be much more convenient, absolutely safe for its users and, most importantly, will not depend on banks or interference by third countries,” he said. “I am confident that something like this will certainly be created and will develop because nobody likes the dictate of monopolists, which is harming all parties, including the monopolists themselves.”Here’s the link to bitcoin.org, Vladimir, in case you have self-googled and are now reading this.Where is this all going?I have a few ideas. So does Credit Suisse’s answer to Led Zeppelin, analyst Zoltan Pozsar.Tell your mates about this amazing article.You want my oil? Give me your gold.“The oil market is tight,” he says. The oil price is lower than it might otherwise be not just because of China lockdowns, but because of the US release of its strategic reserves (SPR), as well as from OECD countries. But Saudi Arabia is now low on spare capacity and the SPR is finite. You can’t print oil after all. “Recent releases have brought reserves down to levels we haven’t been at since the 1980s. The 400 million barrels left in it isn’t much: it could help police prices for a year if we released 1 million barrels per day (mbpd), half a year if we released 2 mbpd, and about four months if we released 3 mbpd”.Short of a sudden new surge in supply (where from?) or a sudden reduction in demand, it would seem then that the oil price is going higher.Russian crude already sells at a $30 discount relative to Brent, which currently sits at $83, he observes with China and India the main buyers. “In the case of India, it is widely understood that Indian refiners are turning some of the imported oil into diesel for re-export. Buying Russian crude at $60 per barrel (pb) and selling diesel at $140pb makes for a nice crack spread, the petroleum market’s equivalent of 100 bps of spread in the land of OIS-OIS cross-currency bases. India and China thus serve as matched-book commodity traders (instead of Glencore or Trafigura), the former dealing in oil and the latter in LNG, keeping commodities in circulation.”But Putin may be happy to sell to India or China at that discount - he won’t however cap prices to sell to Europe on point of principle.Meanwhile, the US needs to replenish the SPR, especially if it wants to control domestic oil prices. “Gone are the days when the U.S. Deputy National Security Advisor warned India and other countries of sanctions if they bought Russian crude oil. The change in tune could be one backdoor mechanism to refill the SPR, and given the $30 dollar discount to Brent that India is paying for Russian oil, this would be below President Biden’s $75 target.”But if Russian oil is exported for the purpose of replenishing the US SPR, Putin’s not going to like that either. What to do then? Only accept payments in gold, says Pozsar, not dollars or rupees. Sound a bit fantastic? “No it is not”, says Pozsar. “Look at the tit-for-tat measures so far: you invade Ukraine, I freeze your FX reserves; you freeze my FX

Helium can only go higher

Today we consider the coldest substance on earth.Which is?I knew you knew. Liquid helium. I have been covering helium for several years now, and it’s time to revisit the theme today. The reason? I keep reading articles about helium shortages (and these have nothing to do with the controversial cryptocurrency of the same name).Bull markets come along every few years in some niche but strategically important commodity. I’ve seen it in cobalt, lithium, graphite, phosphate, uranium, rare earth metals, tin and others besides. The story is almost always the same. Years of underinvestment have led to a shortage of supply of the said commodity. Government stockpiles are exhausted. And, now, suddenly, the commodity is essential to some new technology. Cue the bull market. What do we need helium for - and why is there a shortage?Helium is the second most common element in the universe, so how can there be a shortage?You could say the same about hydrogen and that’s even more common. There may be plenty of it up there, but there isn’t plenty of it down here and down here is where we need it.Nor is helium a huge market. Annual global demand is estimated at around 6 billion cubic feet (Bcf) or 170 million cubic metres (m3). It’s hard to establish just what the current price is because prices tend to be agreed by contract between buyer and seller, but Cliff Cain, CEO of rare gas consultancy Edelgas Group, which studies the market and consults with most of the companies operating in it, gives me the figure of $1,800 per thousand cubic feet (mcf). A year ago the price was closer to $500/mcf.The entire global market for bulk liquid helium is probably around $3bn.Demand keeps growing though, mainly from the medical, tech and aerospace sectors, and “it will keep growing”, says Cain.Helium is seven times less dense than air. Replace the air in a hard drive with helium, there is less turbulence, the discs spin better and so more discs can be packed into less space, while consuming less power. Helium-filled hard drives increase capacity by 50% and energy efficiency by 23%. Thus almost all high-quality data centres now use helium-filled high-capacity hard drives. It’s also used in barcode readers, computer chips, semiconductors, LCD panels and fibre optic cable.Another rapidly growing industry that’s gobbling up helium is the space sector. Helium is used in fuel tanks for rockets and satellites. Physics requires it in particle accelerators. Its low density means it also finds use in deep sea diving, but perhaps its most essential use is as a coolant, especially for the magnets in MRI (magnetic resonance imaging) machines. They must be kept near absolute zero to maintain the magnets’ quantum properties and not lose their potential. A typical MRI machine needs 2,000 litres of liquid helium.As someone who has recently broken his ankle, and also only discovered that I broke my neck in my younger days (it was never properly diagnosed), I can tell you the importance of MRI machines and the diagnostic clarity they bring. Some 38 million MRI examinations were carried out in the United States last year. Forbes suggests helium shortages may be the world’s next medical crisis.“Given the importance of MRI in the medical profession,” it says, “the helium crisis should be front and centre for politicians, policy makers, physicians, patients, and the general public to discuss and find sustainable solutions for. The scarcity of helium is a serious matter and affects all of us directly or indirectly.”And then there are the party balloons.Subscribe now to this amazing publication.Where do we get helium from - and why its price is going upAs Cain points out to me, if you are an aerospace company whose business relies on putting satellites in space, ideally as many as possible, or an MRI manufacturer whose business relies on selling MRI machines, you are not going to let helium shortages get in the way of your business. You are not going to stop producing the machines you produce - you are going to want to produce more and more of them. You will pay whatever price is necessary for the helium and pass the cost on. “Phones, computers, all modern life – it requires helium,” says Cain. “There’s no substitute. Without it, we go back to the Stone Age.”Helium is produced as a byproduct of natural gas refining. The world’s largest producer is the United States (roughly 40% of supply), followed by Qatar, Algeria, and Russia. However, the world’s largest single source of helium for the past 70 years, the US National Helium Reserve, recently stopped its supply. It is letting its staff go and the pressure has come off in its pipelines. “It is now at 700psi when it needs to be at 1,200 to be producing,” says Cain. The system is now for sale, at least in theory. The paperwork has met with delays in the White House, this is likely to take some time to resolve and we won’t see any market until it does. Prospective buyers should also beware of contaminated supplies a

17 Ways Bitcoin Makes the World Better

This was supposed to go out to one and all last week, but for some reason it didn’t. So today we try again - and the article can also be the Sunday morning thought piece.What problem does bitcoin solve? How does it make the world better?Merryn posted those questions on Twitter yesterday.It being Twitter, as you might expect, as well some measured, sensible stuff, it met with a barrage of outrage too, with responses ranging in scope from “it’s a Ponzi scheme” to “it’s destroying the planet” to “it’s going to give us world peace”.I thought I’d answer Merryn’s questions today, sheltered from the mania of Twitter, in the calm surroundings of this blog.I have been trying, on and off, to orange-pill Merryn since about 2014 and I think it’s fair to say, Merryn gets it. She gets fiat money, inflation, money printing, the harm it does, all that stuff. Not only does she get it, she was several years ahead of most of us on that one. She gets the need for apolitical money, lower taxes, less state, less central banking, fewer capital controls - all that stuff too. Cripes, she’s been writing about it all long enough.She just isn’t crazy about bitcoin. I don’t want to put words in her mouth, but I think her objections come, broadly speaking, under three main headers.First, she doesn’t like all the Wild West scams, blunders and ensuing losses that have accompanied this new financial technology. The FTXs, the Mt Goxs, the hacking, the extortions - and all the rest of it.Yes, these are not bitcoin, but bad actors operating in and around bitcoin, but bitcoin has still been the enabler. Two, she doesn’t like the volatility. The price needs to be more stable, if it’s to be a legitimate form of currency or cash.Three, even though bitcoin is, in theory, open to all, in practice it is only open to those technologically savvy or organised enough to be able to store keys, passwords, wallets, seed phrases and so on safely. Those - and there is no shortage of them - who are not comfortable with all of that tend to use third-party providers, which, in the unregulated world of crypto, leaves them vulnerable to those factors listed under “First” - and we are in a loop.I think/hope I’ve summarised Merryn’s core objections - there’s probably something I’ve missed. They are all though, I think, legitimate.So … here, in no particular order, are 17 ways bitcoin makes the world better. Tell your buddies about this amazing article.1. It separates money and state.If one body in a society has the power to create money at no cost to itself, while the rest of us must expend energy to earn it, it is inevitable that body will have disproportionate power and influence within that society. If you want to know why Western states have grown so large, bloated and invasive, look no further than fiat money systems and the power they give to the state. That money goes on welfare, waste, wars, wokery, whatever. You might agree with some ways that money is spent, or you might not; depends on your politics. Doesn’t matter: fiat centralises power in state.Bitcoin removes the ability of the state, and those who operate in it, to print or debase money for their own political agenda.Money, therefore, remains money. It cannot be a political tool.2. It provides a lifelineYou tend to see high bitcoin use under regimes that have seen the greatest destruction to their national currencies - Turkey, Venezuela, Argentina. Bitcoin has provided citizens with an escape. 3. You can send any amount anywhereSending money across borders is hard, even today, whether for large amounts or small. If I want to return the five dollars that somebody in New Orleans gave me last month when I forgot my wallet, or a pound to my friend in India to buy him a cup of coffee, or a thousand pounds to my friend in Iran, I am not entirely sure how I would do all those things. There are forex and other charges. There are processing fees. There can be capital controls. There might be a lot of admin and forms to fill in. Bitcoin is international, borderless, instantaneous and cheap.4. No more capital controls.Governments cannot control the flow of bitcoin capital in or out of the economy. 5. It obviates central banking.The bitcoin inflation rate is transparent and set in code. The central bank can’t start using dodgy inflation measures. It can’t set the price of money too high or too low for too long. There is no scope for human or policy error.6. It increases financial inclusionAround a quarter of the adult population remains unbanked. Around 1.5 billion people around the world (more women than men) still do not have access to basic financial services, such as a bank account. This, more than anything, roots them in poverty. Yet almost everyone (over 90%) now has a smartphone. All you need to participate in crypto, to start sending and receiving money, is an internet connection. Bitcoin banks the unbanked.7. It provides privacy. As the world goes cashless, your every transaction now relies on third pa

How to lose weight

You can read an update to this article here.Over the last year, I’ve lost over 2 stone - 14kg or 30lb, to be precise. I say over the last year, truth is I’ve been trying, unsuccessfully, to lose weight for three years - in fact, since practically forever. Given that most of us want to be somewhat lighter than we are, I thought I’d share my experiences with you today. They may be of some use.BackgroundWhile I don’t really like going to the gym, I do quite a lot of exercise, I always have. I run, I play football, I walked the dog, but I always seemed to be 5-6kg (about a stone) heavy than is ideal. I have a sweet tooth, but not as bad as some. I like beer and I like wine (not so much of a spirit man). I also have a tendency to eat and drink late at night, particularly coming home after gigs. I suspect it was a combination of eating too late at night and booze which left me in that semi-permanent state of slightly heavier than I would like.I’ve tried all sorts of diets in the past. I lost loads of weight on the Atkins diet back in the early 2000s - that’s basically a low carb, high protein diet - but I also felt fatigued, weak and, as soon as I stopped, I put all the weight back on again and more.I also lost loads of weight on the 5:2 diet in the 2010s. Again as soon as I stopped fasting, I put it all back on again. I would also piss off my partner on fasting days, by not participating in the communal activity that is eating.After seeing Fat, Sick and Nearly Dead five or six years ago, I did the juice diet and lost more weight more quickly than with any other diet I have done. You can lose as much as a kilo (2 pounds) a day. It’s very hard to sustain though, and your kitchen quickly gets swamped with juiced vegetable remains. Again, a few months after stopping, I was back where I was weight-wise and some.Between 2020 and 2021, I took up the 16:8 diet, where you fast 16 hours a day and eat only in 8 hour windows. I would have my first meal at lunchtime - 12-1pm and try not to eat or drink anything after 8 or 9. However, this is hard when you’re doing gigs and I often found myself breaking the rules. I lost a couple of kilos, then plateaued. It meant, though, that I got into the fasting state every day, and I got used to the feeling of being hungry. It became normal. Then I actually started putting on weight. I think it’s because my body got used to fasting, so it did all the things it did - conserve energy and calories - then I would consume too many calories in the evening, close to bed-time, and so, in this state of efficiency and fasting, the body conserved more calories than it otherwise would have and I ended up putting on weight.I was fatIn September 2021 I went the wrong side 90kg (over 14 stone or 200lb). Too much for a man of my 5ft9 frame. A change of strategy was needed. 16:8 wasn’t working, but I was convinced of the efficacy of fasting, so I went back to 5:2.Within a couple of weeks I shed 3-4kg (half a stone), but then I plateaued again. For many months. There was probably still too much of the eating and drinking in the mid to late evenings, especially after gigs, on non-fasting days. I was presenting Headliners on GB news at the time, and I would get home at 1am, not want to go to bed and often then crack open a bottle of red wine. To avoid doing this, I took up fasting on the days I was presenting Headliners. On fasting days, it’s best to go to bed early. Presenting a TV show at 11pm having not eaten all day meant I was almost falling asleep, as it ended. Not ideal.I left the show in March or April, and it was after that that the big weight loss suddenly accelerated.In my new less employed state, I had a bit more time on my hands and I took up playing tennis twice a week with a chap I met on Facebook. I had fewer late night gigs, so less late night calorie consumption. I then got involved in a swimming challenge, so I started training for that. I also continued playing football once a week.It was the combination of increased activity and fasting on the same day that made the weight fall off me. I got caught in this virtuous loop. As I started to feel fitter, on my way to tennis, I would cycle up a really steep nearby hill four or five times and get in some HIT. On non-fasting days I now found myself consuming less anyway. I would skip meals, especially breakfast, so found myself doing a mild version of 16:8 as well.England cycling coach Philip Brailsford used to talk about the “aggregation of marginal gains”. So it is with dieting. There are lots of small things you can do, but it is when you put them altogether that the big changes occur. (The same happens in reverse).So here in bullet points is the Dominic Frisby Diet.Subscribe to this amazing publication.1. Indoctrinate YourselfI would say this is almost the most important part. Find a diet that works for you. A lot of people swear by protein diets, for example. I find them too hard to practically sustain. I like fasting. It works. It’s prov

Polyamorous geeks, psychopaths and perhaps the greatest fraud in history

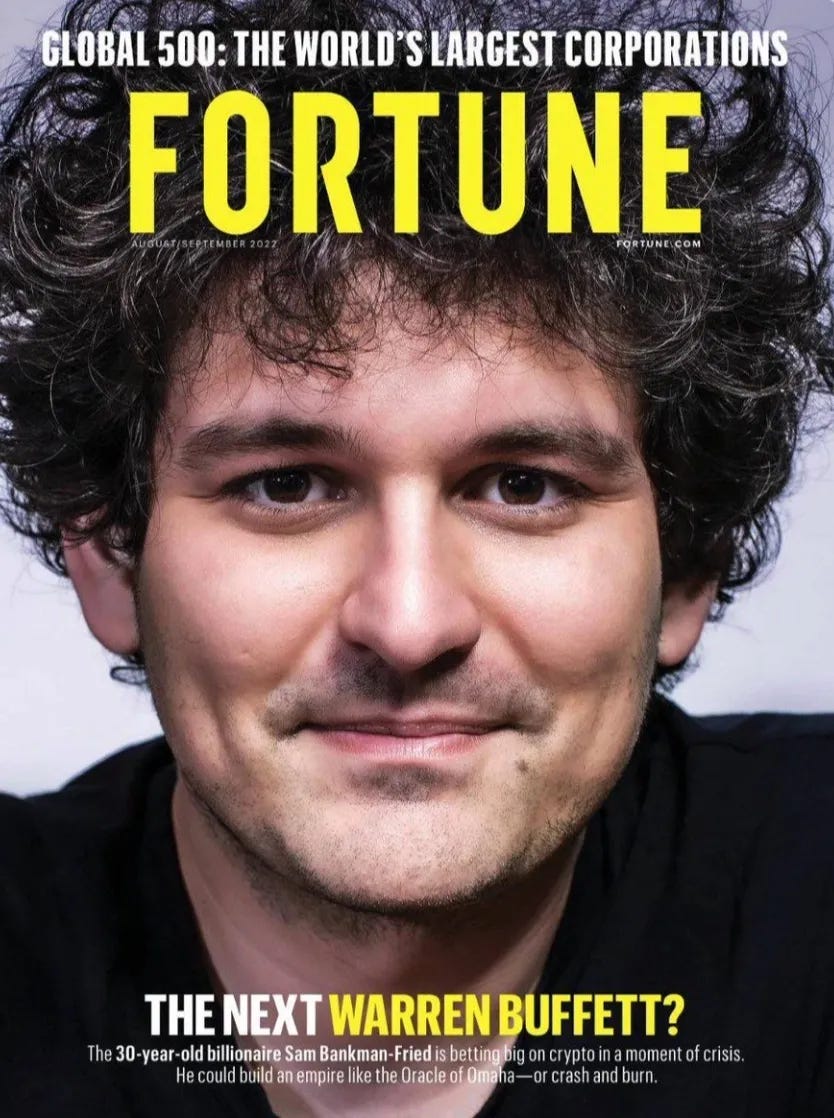

I’m delighted to report that The Flying Frisby is now a Substack Bestseller. Thank you to everyone who supports this bestselling publication!By popular demand, today we consider bitcoin - and the amazing story that is FTX.Gosh, this is some story - it’s difficult to know where to start. The more you dig in, the more that comes out. It’s a cautionary tale of the madness that engulfs crowds during investment manias and bubbles, of greed, delusion, risk, and more besides.I’m sure many of you already know the story, even though there are new developments every day, so I’ll recap it quickly, before moving on to what it means for bitcoin.Tell everyone you know about this amazing article.The story of FTXSam Bankman-Fried was a geeky young crypto “entrepreneur”, born to an upper-middle-class Jewish family in California. His parents were both professors at Stanford Law School. Ironic.In 2017 he set up the quantitative trading firm (that would be trading based on mathematical models) Alameda Research . Then, in 2019, came FTX, a crypto exchange that became phenomenally successful, phenomenally quickly. In July 2021, barely two years into its existence, FTX raised $900m at an $18bn valuation. That was Series A. Three months later came Series B - $420m at a $25bn valuation. Three months after that, in January of this year, it raised another $400m. This time the company was valued at some $32bn.To put those numbers in some kind of context, the likes of Barclays, Soc Gen and Deutsche Bank - banks that have been around forever - all have smaller market caps in the $20-30bn range. $32bn would be more than the UK collects in stamp duty in a year. Or fuel duty or alcohol and tobacco duties. It’s roughly five times what it collects in inheritance tax.Bankman-Fried himself was worth $16bn, and at the age of 30, was on the front cover of Fortune Magazine, along with a headline asking if he was “The Next Warren Buffett?” FTX’s blue-chip and “smart money” investors included Japan’s SoftBank, venture capital firm Sequoia Capital and hedge fund Tiger Global. Even the Ontario Teachers’ Pension Plan put in $95mn. (What has your pension fund manager been doing with your money?)There were rumours of another $1bn raise in September. However, that didn’t materialise and the bitcoin bear market meant the tide was going out in the crypto industry. We would soon learn who had been swimming naked.Subscribe to this amazing publication. It’s a Substack bestseller.FTX suffers in the bitcoin bear market Some started asking questions about FTX’s accounting and other practices. Short sellers also started taking notice - they expose frauds more quickly than anyone. Negative coverage started to appear. On November 6 an article at Coindesk raised doubts about the balance sheet of Bankman-Fried’s sister company, Alameda. Then things started to unravel quickly. Changpeng Zhao, CEO of Binance (the world’s biggest crypto exchange), which had been an early investor in FTX, announced that Binance was selling all its FTT coins - as much as $2bn worth. (FTT coins are part of the plumbing of the FTX exchange). The value of FTT started to fall.Suddenly there was a scramble to withdraw assets from the exchange. It was thought to have had the assets to back the liabilities, Bankman-Fried tried assure everyone that client funds were safe, but it seemed this was no full reserve exchange and FTX didn’t have the funds to meet the run. In fact, it seems FTX had been using some of the funds - as much as $10bn - to shore up sister company Alameda, which had suffered significant trading losses over the past year. (Watch the interviews with 28-year-old Alameda CEO Caroline Ellison - said to be in a polyamorous relationship with Bankman-Fried - describing how she “doesn’t like stop losses”. Turns out she had barely any risk management at all).Chain analysts noted that FTX didn’t have the funds to cover withdrawals. On November 8th Bankman-Fried said he had “enough to cover all client holdings” and that “he doesn’t invest client assets”, but the run continued. That evening withdrawals were halted. In an attempt to restore confidence, Zhao and Bankman-Fried announced that Binance would be acquiring FTX soon after. However, the following day, Zhao said that having done his due diligence, Binance would not be acquiring FTX. A day later, FTX filed for bankruptcy. Easy come, easy go: Bankman-Fried’s net worth went from $16bn to zero in barely 72 hours. Reports are FTX had $900m in assets against $9bn in liabilities.And then, the day after that, some $600m in crypto was hacked from FTX’s wallets and syphoned lord knows where - Panama, Bermuda and Cayman, presumably. Apparently the hacker isn’t even that sophisticated and numerous Twitter feeds are now following the stolen crypto.This story’s amazing - you need to share it on Twitter, LinkedIn or Facebook.As FTX unravels stories start to emerge Since then all sorts of stories have emerged. Weird sexual goings on at the companies

Hold on to your oil, gas and coal stocks

A number of people have asked me to cover bitcoin after this week’s insanity - and I will very soon, I promise, but today we consider fossil fuels once again.While the oil and natural gas prices have not done a great deal these last six months - up a bit, down a bit, then sideways - the associated companies have done very well: the producers, the service companies and so on.Many years of bear market and belt-tightening are now paying off.However, we are not yet, I would suggest, at that point of excess and decadence that marks the end of a cycle - crazy mergers and acquisitions, insane valuations and Bacchanalian behaviour from the executive classes. So I venture today, as last week, that there is still plenty of gas left in the tank of this bull market.With that in mind I wanted to share a few charts with you today that give an idea of what is possible.Oil and gas stocks are on the rise The first of them shows the ratio between energy stocks and the rest of the market. Indeed, without energy stocks there would not be a rest of the market. A simple point that many, especially those who make policy, seem oblivious to. The world we live in today and the economic benefits we enjoy, relative to our ancestors, have been made possible by fossil fuel.So here is the energy sector relative to the the S&P 500. The higher the chart goes, the bigger the relative market cap of energy stocks. You can see that, even with the rally we have seen in energy companies since 2020, on a relative basis, energy companies are, give or take, where they were at the turn of the century, when oil itself was around $10/barrel and that secular bull market was only just getting started.You can also see that we are in an uptrend. Energy stocks are increasing in value, while the broader S&P500 is flat or falling.It’s also worth noting that the relative market cap was almost three times as large in mid 2008, when oil went to $147/barrel. The inference is that the bull market has a lot further to run.Tell the world about this amazing article.Oil versus stocksNext we consider the ratio between oil - West Texas Intermediate - and the S&P 500. You would expect this chart to trend lower over time because oil production and extraction techniques should improve over time, while broader economies and the companies who operate in them grow. Nevertheless we are below the levels we were in the early part of the century. You can see how high this ratio went in 2008 - and how low in Corona panic of 2020, when oil futures, somehow, went into negative territory.It feels a bit like, as far as this ratio is concerned, we are in late 2003.Relative to the S&P 500, oil is roughly where it was three or five years ago - I’d say it’s at its 3- or 5-year average. And it’s a lot cheaper than it was throughout that entire 2003 to mid-2014 timeframe. So even with the gains of the last two years, oil does not look expensive relative to the S&P 500. It is at the cheaper end of the range. Another sign there is more gas left in the bull market tank.Here now we look at oil relative to gold. These two - as hard commodities - tend to trade in a much tighter range over time, but my observation again is that it is in the low to middle of the 20-year range and not at one of those points of extremity whereby you might consider rolling out of one and into the other.For sure we are nothing like where we were went oil went to $147 in 2008. In fact, we are below where we were for most of the 2000s. On the basis of this chart, oil is probably the cheaper of the two.Trade of the lustrumAs regular readers will vouch, oil is a drum I have been beating since 2016 when it was $25 or so, declaring it our “trade of the lustrum”. A lustrum is a five-year period - a useful and underused word I’d say.That lustrum is now becoming a decade. We continue to beat the drum on oil, gas, coal and the related companies. Fossil fuel demand will continue to grow until at least 2030, the IEA has forecast (2040 in the case of natural gas). That means it is not just enough to maintain current production levels, they need to increase. Yet there have been seven or eight years of underinvestment - leading to today’s shortages. Partly because of ESG deterring investment, partly because so much capital has gone into green energy related companies instead and partly because of the excesses of the previous bull market still needed to be purged. The bull market conditions are still good and longer term, I think fossil fuel stocks go higher.I’m a big believer in narratives within markets. The fossil fuel story is only slowly starting to change. Many are realising just how important they are and what they have made possible. Indeed, that there is a strong moral case for them, not against them.But the narrative is not yet at end-of-cycle levels. When people start talking about Peak Oil again - that’s the sort of thing you want to be looking out for. That the need for alternative energy sources is not because fossil fu

What happened there could soon happen here

Today’s missive comes to you from the Galapagos Islands out in the eastern Pacific, where two stories of noble energy initiatives reflect the broader realities of energy policy around the world. We tell these stories with a specific question in mind: how much gas, so to speak, is left in the tank of this energy bull market?The Galapagos population is only around 30,000, but, as a fully functioning society, the same dynamics observed in this small ecosystem occur elsewhere, even if less visibly, so it serves as a useful case study.So we come to the first of our two stories.Not so green transport in GalapagosIn order to limit traffic, protect the environment in this most ecologically delicate of places and protect the taxi industry, the local government made it extremely difficult to get a vehicle licence. All sorts of problematic bureaucratic hurdles had to be jumped, and most people ended up using bikes or public transport.But then in 2016 the powers that be, with a brighter, greener future in mind, decided that anyone could get a licence to own a vehicle, no permit required - as long as it was an electric vehicle. There was just one condition. The buyer had to have a family. Given that most people on the islands have relations, that was a pretty easy condition to meet, even for the single folk. There was a great deal of PR and fanfare about this new initiative: clean, green, sustainable - all that stuff - and a blind eye was turned to the increase in traffic, or of roadkill to the many tame birds on the streets of the island (this is a major problem).At this point it’s worth reminding ourselves that there are, around the world, three main areas of energy consumption - transportation, heating and electricity. While cleaner forms of energy, such as nuclear or wind, might be increasing as sources of electricity, 84% of global energy still derives from the burning of fossil fuels, as the graphic below from Our World In data shows.Even electricity, despite its green credentials, still relies on fossil fuels. The burning of the fossil fuel may be out of sight and, therefore, out of mind, but over 60% of global electricity still derives from it, as our second graphic shows. Wind and solar between them account for barely 10%.Sign up to The Flying Frisby.As we are all now discovering to our cost, despite many years of considerable investment, some might say over-investment, in green energy, there have, simultaneously, been many years of underinvestment in fossil fuel exploration and extraction, nuclear power (the use of which in electricity has, on a relative basis, been declining since the 1990s) and public grids. Hence the current energy shortages especially in Europe. The Galapagos Islands followed the international trends in this regard - which is one reason this story makes for such an interesting case study.Here on the Galapagos Islands, the majority of electricity, despite what you may read, is produced by burning diesel. And at this point we deviate to story number two.The Galapagos wind turbines.There were, once upon a time, some wind turbines built by a consortium of overseas energy corporations, looking to advertise their green credentials to the world. Said corporations conducted a one-year study of wind on the island and concluded that next to the airport (where they would also conveniently be seen by everyone arriving at and leaving the islands) was the best place to erect the turbines. The turbines were duly installed, the publicity was had - here is the world’s first airport that runs 100% on wind and solar, all that stuff - and the energy companies retired back to their nation states.It turned out that year of the study had been an outlier for winds, and they hadn’t built the turbines in anything like the windiest spot. Then the wind turbines stopped working, but nobody on the islands knew how to fix them. Nor was it clear whose responsibility they were. Ever since, the turbines have sat there, stuck - even when the wind is blowing up a storm. Ask a local for the story, and you’ll get a wry shake of the head and a smile at the stupidity of it all. Lord knows how much fossil fuel was burnt mining the necessary materials, manufacturing the turbines, transporting them to the islands and erecting them, only for them not to work, but that is, despite the good intention, what has happened. There they remain, motionless, like statues from a fallen empire. But how now to get rid of them?The episode is neither clean, green nor sustainable.Tell the world about this amazing articleSo back to story number one and the attempt to make the islands greener with electric vehicles (EVs). With the easing of regulation in 2016, the locals who had previously wanted a vehicle but couldn’t get one (a lot) piled in and bought electric vehicles, much to the benefit of the EV manufacturers.But as diesel is the major source of electricity on the islands, so more diesel than ever was now burnt. Again, neither clean nor green.

The Way We Help People Does Not Help People

The highest form of charity, argued the 12th-century Jewish philosopher Maimonides, is when the help given enables the receiver to become self- sufficient.But our systems of state charity - aka welfare - have too frequently had the opposite effect: they have actually created dependency. It is time to re-think the way we help people.I suggest something that may be heinous to some, but it’s this: welfare would be more effective, more varied, more widespread and affordable if there were no state involvement.People instinctively think that without a welfare state, the poor and needy would not be looked after. At such an unacceptable prospect, people then become fervent in their defence of state welfare systems. You can see the passion people feel about this erupting all over the Twitter and the blogosphere.Before we start, I want you to get your head around one thought - suggesting that the welfare system is not working and that we should do away with it is not the same as suggesting the poor and needy should not be looked after. Not at all - in fact, quite the opposite.The provision of care is a delicate, complicated and unpredictable process. Sometimes money might help the recipient towards self-sufficiency, but sometimes not. Giving money might lead to a temporary lessening of suffering, but often it can lead to greater dependency and less self-reliance. Sometimes something local is required, sometimes something practical, sometimes something psychological or emotional, sometimes something specific to the individual's circumstances - sometimes what's needed is a proverbial kick up the backside. Different circumstances require different forms of care.The dignity of the recipient also needs to be considered. It can be demeaning to receive charity. On occasion anonymity might be required - but on other occasions it might not be.How on earth can anyone hope to design a top-down, one-size-fits-all, system of state welfare that can meet all these varying needs consistently over time?Then there is the matter of the giver. He or she must also be considered.Compassion, care and the giving of charity and care are essential human functions - they are a part of human nature. People need to give as much as they need to receive. You just need to see the pleasure children get from giving as evidence of this. Even perhaps the most ruthless, murderous drug-trafficker that ever drew breath, Pablo Escobar, was a prolific giver. He built houses, churches and schools in his native city of Medellin on a scale unmatched by the Colombian government.In the charitable process, the giver has needs too. Sometimes the giver wants to be anonymous - sometimes they want recognition. Sometimes he or she likes to be involved with the recipient in some way, sometimes not.But, in the process of state care, the giver's needs are not even considered. Taxes are taken and that is it. We are given no real say in how the money we have earned is spent, bar a vote of dubious effect every five years. Often the giver is morally opposed to what his taxes are being spent on!The forced giving that is taxation actually destroys the altruistic satisfaction that people get from giving voluntarily. To help others and to share with them is part of humanity. But, in a world in which government is responsible for the care of the poor and needy, that compassion is removed from life. As a result, the state now has a near monopoly on compassion!if you find this interesting, please share .In fact it is even more bizarrely specific than that: the pro-large-welfare-state left wing has the monopoly on compassion. Anyone who doesn't agree with the concept of a large, generous welfare state is deemed heartless and selfish.While you have to pay the government through tax to provide welfare (or heathcare or education) your ability to provide any of these things for yourself or your family is reduced, because you have less money. After taxes are taken from you, you often you can't then afford to pay for your children's school, your doctor, your hospital, your home, or your charity to others - so you find yourself depending on the state help in some way. And so more and more people, in some way or other, are caught in the ever-growing dependency net.What's more, if the state is providing care to the needy, you are then absolved of the responsibility to do so.Meanwhile, government welfare, as well as being inflexible, is expensive . The large organizations, such as the NHS or the DWP, through which care is administered can be inefficient and wasteful. Worse yet, they are be prone to corruption and rent-seeking (people gaming the system in some way).If you look at food, clothing or technology - essential human needs that, largely, are not supplied by the state - we have, over the last thirty of forty years, seen dramatic falls in price and dramatic improvement in quality. Competition has driven costs lower. Yet welfare has not experienced the same improvements. Why not? Because

How the nature of money has changed - and what it means for you

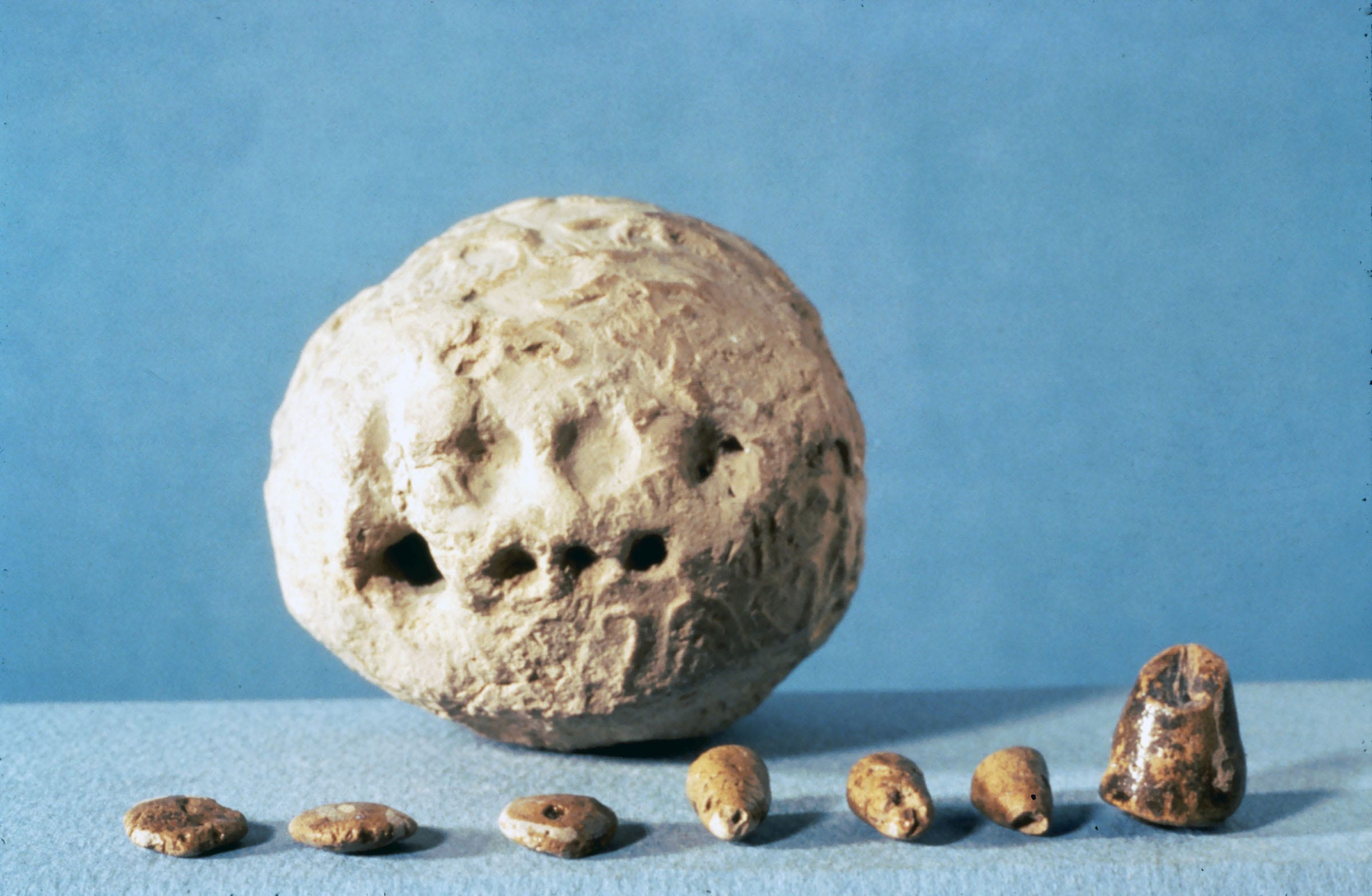

Money evolves constantly. Every day there is some tiny new fintech development, but it’s only when you take a step back and look at the ten-, twenty- or thirty-year picture that you realise just how much things have changed. What is money today is a far cry from what was money when I was a child. Digital technology barely existed back then. We used cash and these things called cheques. You’ve probably heard of them.It’s not just what we use as money that evolves. How money is created - that changes too. And just this decade there has been a major evolution. That’s what I am going to talk about today.Thank you for reading The Flying Frisby. This post is public so feel free to share it.The creation of money and debtOnce upon a time you would create money by mining gold and silver. But debt-based money systems have also existed since the dawn of civilization, when clay tokens representing valuable items such as barley or sheep would be baked inside clay balls. When the debt was settled the clay balls would be smashed open.Humans, being the ingenious folk they are, especially when it comes to money, soon found that it was quicker to simply inscribe the clay with pictures of said items and so did the first systems of writing develop - hieroglyphics. Coins came along, and then the printing press, both remarkably long-lived technologies, but behind it all there was always metal.Western Europe abandoned gold in 1914 so it could print the money to pay for the First World War, and the United States did the same in 1971 amidst spiralling welfare costs and the conflict in Vietnam. Both years were landmarks in the evolution of money creation.This became the fiat era, when money became debt. Some physical cash was printed or minted, but money for the most part was created when loans were made. You borrow a thousand pounds to buy a house, the bank created that thousand pounds using the house as collateral and suddenly there was a thousand pounds in the housing market that wasn’t previously there. That’s why houses kept on rising in value - the constant introduction of newly created money through mortgages. Introduce debt into a market and prices rise. If houses were cash based, they’d be a lot cheaper. Something similar happened in the bond markets and the financial markets with the use of leverage. Leverage is just a fancy term for debt.There were occasional moments of credit tightening, but the broader trend, especially as economists and governments became obsessed with what they call growth, was for ever expanding credit.Human beings, being the greedy folk they are, especially when it comes to money, took the whole thing too far, 2008 came along and the bubble went pop.Then a whole way new to create money was invented: Quantitative Easing. Central Banks now started creating money, and they bailed out the financial system with it. Then they started using the money to buy government bonds - so they effectively printed money to pay for government spending. They also bought other financial assets. And so lots of newly created money went into the financial system and from there to the expensive houses in which many of those who work in finance live, and we got another decade or more of rising prices.But because all this newly created money went into financial assets and housing, it didn’t show up on the inflation numbers. Central bank inflation measures don’t include houses or financial assets. So they said there was no inflation. Then Covid came along. Central banks could now print money and it doesn’t create inflation, they thought. They forgot about the sleight of hand that was their inflation measures. So they printed more money and the government handed it out to people. That money made its way into the real economy and now we have inflation. And they are all scratching their heads and blaming Vladimir Putin.But the nature of money creation has changed. Now money is not just debt. Governments are creating it to fund their activities. And when central bank digital currencies come along, they are going to do that even more. As a result governments, are going to play far greater role in where capital gets allocated. We turn to the wise old owl that is financial historian Russell Napier. “By issuing state guarantees on bank credit during the Covid crisis, governments have effectively taken over the levers to control the creation of money”. They said it was temporary, but, to quote the great Milton Friedman, “nothing is so permanent as a temporary government programme”.We now have the War in Ukraine and with it spiralling energy costs - another emergency. How to deal with it? Keep with the programme. Lend money and guarantee loans. Russell Napier again: “By telling banks how and where to grant guaranteed loans, governments can direct investment where they want it to, be it energy, projects aimed at reducing inequality, or general investments to combat climate change. By guiding the growth of credit and therefore the growth

Talking mining with Brent Cook and Kai Hoffman

Here at the New Orleans Investment Conference, I met up with veteran geologist and mining newsletter writer Brent Cook of Exploration Insights together with not-so-veteran, but equally on-it investor Kai Hoffmann of SF Capital. What followed is a 20-minute chat about the state of the mining markets. Those of you that are interested in the state of mining - enjoy! This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit www.theflyingfrisby.com/subscribe

Notes from New Orleans

Back in the 90s, when we were in our 20s, all my university buddies and I wanted to do was travel. We wanted to go everywhere and see the world. The problem was how to pay for it.My solution was to work all year, save up, then, having spent Christmas with my folks, get a flight somewhere on Boxing Day or the day after (flights were always cheap then) and come back at the end of January. The business I was in at the time – voiceovers – never really got going until mid January, so I would end up with almost six weeks of backpacking and only miss a couple of weeks of work, if that.My best buddy, who is now a big cheese at Channel 4 so I won’t mention his name, went several stages further. He got a job compiling guide books for many years. As a result, he has been to more places than anyone I’ve ever met – across Asia, Africa, Europe, the Americas, you name it. And, of all of them, he says he reckons New Orleans was the best.So, imagine my delight when I got an invitation to come and speak at the New Orleans Investment Conference this year. Do I want to come? You betcha!The conference took place last week and I thought it might be of some use or interest to you if I shared some of my observations.Will the Fed keep raising interest rates?First up, I had a great time. The conference, organised by Brian Lundin of the Gold Newsletter and his supremely competent team, lasted four days. There were workshops and events galore, plus a host of great speakers – from celebrated resource investors such as Rick Rule, Brent Cook and Sean Broderick to macro strategists such as Danielle DiMartino Booth, Peter Boockvar, James Grant and Jim Iuorio to the unorthodox with the likes of Jim Rickards, George Gammon, Dave Collum and Robert Prechter. Over 600 people came and there were 100 exhibitors. I would say the bulk of the attendees were American, over 50 and male. There were a lot of gold bugs in the room. I felt well at home. Plus there was plenty of fun to be had in this most musical of cities by night – and great food too.I would say the overriding theme of the conference – the subject that would not go away – was the Federal Reserve Bank. How long does it continue to raise rates for? When does it pivot? At what point do debt levels become unsustainable? The US has interest to pay on $31trn of debt – that surely caps how much further it can raise interest rates? But then it has made it clear that fighting inflation is its number one priority. Round and round the subject went. Some argued that it pivots, others that it keeps on raising.There was also plenty of talk about falling real estate prices; commodities – especially base and battery metals, not to mention energy; the strong dollar and the Ukraine war. I found myself on a panel with George Gammon and Jim Rickards about the threat of imminent nuclear war that got very tin-foil hat. When I suggested that, to everyone’s surprise, Russia was losing the war in Ukraine, Rickards declared that I had fallen for the propaganda and had become a mouthpiece for the globalist agenda and the New World Order. Each to their own, I guess.Opportunities for investors in the UKAnother theme that cropped up a couple of times was investing in the UK and the opportunities there – or here, I should say. The yields on real estate investment trusts (Reits) are incredible, said Peter Boockvar, and, unlike New York where a lot of commercial property is sitting vacant, while many continue to work from home, in the UK it’s mostly being used again. Perhaps most importantly, UK property is looking very cheap to our transatlantic friends thanks to the strong dollar. I warned about the potential for rising rates here in the UK and the damage it could potentially do to real estate, whether commercial or residential, but Boockvar still felt the UK is looking like an attractive proposition at the moment. We have a tendency to denigrate ourselves here in the UK, which is why it’s so good to go abroad and meet people who see the UK in a much more favourable light.A lot of North American money is going to make its way to Europe and the UK, not to mention Japan, in the not too distant future, I would venture.I focused my talk on subjects that I have been covering quite extensively on these pages in recent weeks – energy; gold and its relevance (or lack thereof) in today’s world and China’s monumental gold holdings; and the strong dollar superseding all.There were plenty of mining companies there too exhibiting their wares. I think my favourite was probably a silver mining company by the name of Sierra Madre Gold and Silver (TSX-V.SM), which has a dynamic young management, good broker backing, some promising exploration properties and has just acquired a silver mine from First Majestic Silver (Toronto: FR, NYSE: AG) that it is now putting back into production. Pending the closing of this transaction, the stock is currently halted, which is what all silver companies should be – it removes the temptation to buy th

On raising money and distorted incentives

I was listening to an interview the other day with entrepreneur Balaji Srinivasan, in which he argued that there are two ways by which you can raise capital: one is through investment, the other is through charity.If you are raising capital through investment, the incentive is to demonstrate strength, competence, ability, prowess, honesty and many such other qualities. The more competence you demonstrate, the more likely people will invest in you and the more they will invest. Broadly speaking, this applies to gaining employment too.On the other hand, if you are looking to appeal to people’s charity, then the opposite applies. You must demonstrate that you need and deserve this charity, and so the incentive is to demonstrate weakness, affliction, victimhood and so on. Many of these messages of affliction have made for some of the most powerful ad campaigns ever conducted. Young children and animals are probably the most evocative - from the starving Ethiopian children that inspired Live Aid to the battered seals of anti-fur campaigns.Welfare and, to an extent, healthcare can be seen as forms of charity, even education in a way. In the 19th century responsibility for the provision of welfare, healthcare and education mostly lay with the church, the friendly societies and other private bodies, but in the 20th they, for the most part, became the domain of the state.Today there are countless institutions that rely on government subsidy for their existence - from those fighting climate change or promoting green energy to those fighting perceived inequalities such as Stonewall to many in the arts. All rely on demonstrating affliction to fund themselves and exist. Meanwhile, charity has become an enormous business in the developed world, and all sorts of scandals are starting to emerge of corruption, of the huge salaries many of those who work in it enjoy (get paid lots and be virtuous) and the fact that so little of money donated actually reaches the intended recipients - less than 50% is the key stat from the David Craig book, The Great Charity Scandal: What Really Happens to the Billions We Give to Good Causes? Some charities rely on donations and subscriptions, many rely on the state and its subsidies, many on both. And the industry is heavily regulated by state (with questionable results if the above is to be believed). Regulation also costs a lot of money to adhere to.As those who read my stuff, especially Life After the State, will know, I constantly argue the state is not the best means to provide these things to the highest possible standard at the lowest possible cost, that in fact, for all its good intentions (let’s assume they’re good) the state often causes more harm than good and its role in exacerbating the health, wealth and opportunity gaps is demonstrable and large. Thus we should shrink the state as much as is possible.But because the state has grown so bloated in the West, and because it is the main provider of this second form of capital - charity - whether by subsidy or through its other systems, and because the solution to pretty much any social problem that arises is that the government “must do something”, I suggest we are getting caught up in an extremely unhealthy psychological loop. Rather than incentivising strength, competence, excellence and so on, our systems are incentivising behaviours by which that second form of capital be raised - weakness, victimhood and so on. That’s why there is so much of it about.New afflictions are being found all the time, as “entrepreneurial” spirits try and find new means to secure special favour, protection and subsidy.Thus, by shrinking the state do we shrink victimhood. We want people to be the best they can be, surely? Not the opposite.Thank you for reading The Flying Frisby. This post is public so feel free to share it. This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit www.theflyingfrisby.com/subscribe

Gold: the disconnect between the price and what is happening in the physical markets

Today we turn our attention to the physical gold markets.There is, as veteran dealer Ross Norman of Metals Daily puts it, a “disconnect between the gold price and what is happening in the physical markets.”“Our biggest challenge,” says Joshua Saul of the Pure Gold Company, “is finding enough stock on a daily basis to sell. There is a long line of demand, but very little supply. There’s more demand than at the height of Covid.”These situations don’t occur very often, but they do occur. The gold price is falling, but demand for physical gold is highI remember 2008 like it was yesterday. Gold cratered along with everything else in the second half of that year. It lost around 30% – falling from north of $1,000/oz to $720/oz. The mining companies fell by a lot more.Yet there was a scramble in the physical gold markets. Bullion dealers had never been so busy. The general public were rushing to get their money “outside the system” into an asset that was nobody else’s liability. Gold would later turn up long before most other assets. November was the low, while the S&P500 carried on lower until the following March. But the fact was there was a scramble to buy physical gold even as the price was falling.It happens. “Coins and bars,” says Norman, “are just a subset of a much bigger industry.” That industry includes the futures markets, exchange traded funds, institutional buying and selling, central bank buying and selling and, of course, jewellery. Ordinary investors may look at the state of the world and think, “I need to buy some gold”. They may be doing that at unprecedented levels. But that is not enough to balance out institutional investors who are, says Norman, “selling three to ten tonnes a day.”As I say, these disconnects do happen, but they don’t necessarily last.The US dollar has stolen the showIt’s all about the US dollar, as we have been saying on these pages for many months. In the year to date, gold is up around 13% in sterling. That’s an almost stellar return compared to stock and bond markets. But against the dollar it’s down some 8%. How long does the dollar stay so strong? That’s the question we must ask ourselves. On current form, a while longer it would seem.Norman, who has an extraordinarily good forecasting record, agrees. “The rampant dollar looks like it might be here for a while,” he says.You don’t need to look further than US interest rates relative to European interest rates and US energy dependency relative to Europe’s, to understand why we are where we are.“Never in my career did I think we’d see the circumstances we are now in and gold behaving like it is,” says Norman. “It’s extraordinary. The dollar has stolen the show. But nuclear war is a real possibility!”Gold, by the way, will survive a nuclear explosion, and none of the three types of radiation that follow – alpha, beta and gamma – will affect it.Smart investors are still buying gold bullionBut one of the few bright spots in this market is what Norman calls “the literate investor” who continues to support it.Saul of Pure Gold makes a similar observation. His company makes a point of talking to clients as they buy and sell, to understand their motivations. As a result, they build up a lot of qualitative data.“Everyone’s looking to protect their wealth in a time when things are really uncertain”. But there have been two notable trends he has observed.First, there has been a notable increase in buyers from the financial world. “Traders, investment bankers, financial services, accountants, lawyers – they’ve been buying large sums. I find this notable: “Their trade sizes are bigger. The median trade size is probably three times bigger than it was a year ago – and during Covid.”Saul says many of them are worried about what is going on behind the scenes at the banks. “These are considered investments, where there is a lack of alternatives.”The Flying Frisby is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.Money is moving out of property and in to goldThe second notable trend is the exodus of money from real estate – whether commercial or residential.“Property investors normally like to remain liquid, so they have cash on hand ready for the next deal. Buy-to-let landlords, commercial landlords, people who buy big buildings and let out floor by floor, developers. Companies and individuals. A lot of them have a lot of cash. They have an appetite for debt, but the increased cost of debt, plus the possibility that the underlying asset will fall in value means there is too much risk for them. They’re now parking that cash in physical gold.”“We are also seeing a growing amount of people with properties on the market, who when their property sells will move their capital into gold. Many are removing their exposure to debt that they might have taken two or three years ago.”What we are seeing then is capital flowing from finance and from real estate into gold. I find that te

Mind The Gap

I stumbled across this 2013 blog earlier today. I’m posting it because I thought you might enjoy it, and partly because it’s relevant to a thought piece I’ve been working on that I’ll be posting later in the weekOoh, what fun There's nothing surer The rich get rich and the poor get poorerPeggy LeeMost of us now enjoy luxuries that would have been unheard of a hundred years ago - running water, electricity, computers, phones, cheap food and clothing. Yet, despite all this, there is discontent. Huge amounts.The problem is inequality. Inequality is everywhere, it is increasing and it comes in many different forms.There is the wealth gap.The wealthiest 400 people in the world are worth more than the poorest 140 million.70% of the land in the UK is owned by less than 1% of the population.When once CEOs of major corporations earned 20 times more than their employees, now they can earn a thousand times more. A Burberry sales assistant (according to Glassdoor) earns £16-17,000 including commission. The Burberry CEO, Angela Ahrendts, received £16.9 million last year. I shudder to think what the Burberry factory worker is getting.Over fifty per cent of young people believe they will never own a house, while the average age of the first-time buyer in London is now over 40. He or she'll be a pensioner before they can start a family.We can build a decent house for less than a hundred grand, and only 2.5% of the UK is actually built on, so how can we have a society in which houses have got so expensive that most young people think they will never own one?There is the health gap.Unbelievably - and despite best intentions - health inequality, as measured by life expectancy, has actually increased since the founding of the NHS in 1948. There is also huge discrepancy in the quality of care received between the top and bottom of society.And we have the opportunity gap.Despite billions being spent on education, despite more and more taxation, subsidy, legislation and regulation all with the intention to spread wealth and bring equality of opportunity, the top positions in just about every area of the economy you can think of - politics, law, media, finance, medicine, even manufacturing - are dominated by the 7% of the population who went to public school.Even in the Olympics you were five times more likely to win a medal if you went to public school.Something is wrong. People are, rightly, angry about it.Tax the rich more. Stop companies like Google evading their tax. Clamp down on immigrants. Stop benefit cheats. Spend more on education, on health care, or is it infrastructure? Increase regulation of banks. Build more houses. Subsidize wind farms or environmental initiatives. More austerity. Everyone has their own idea about what needs to be done and over the last decade a huge ideological battle has been unfolding as people argue about it.But all these ideas and many more besides, some of which come from the left and others from the right, all involve the same thing: that the government does more, that it takes action.I suggest the opposite - that the ONE thing government should do is LESS. I suggest that, counter-intuitive though it may seem, the huge rise in inequality is BECAUSE of government and the unintended consequences of its actions.For a hundred years the state has got more and more involved in our lives. It now look after our birth, our education, our health, often our employment, our old age, even our burial. Through its money and interest rates, through its taxes and subsidies, its rules and regulations, it looks after our economy. The more it does, the greater these gaps have all grown.It's time to try something else - Life After The State.Life After The State by Dominic Frisby is available on Amazon. The audiobook is available at Audible.And if you happen to be in the Louisiana neck of the woods next week, or fancy a trip, I’ll be speaking at the New Orleans Investment Conference, which runs from October 12-15, at the Hilton New Orleans Riverside. There are lots of big names on - Rick Rule, James Grant, George Gammon, Jim Rickards, Doug Casey and many more besides. Come and say hi!The Flying Frisby is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber. This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit www.theflyingfrisby.com/subscribe

Is that it, then? Is the bear market over?

We’ve seen incredible rallies across the board this week.After a worrying sell-off late in the day and into the close on Friday, the Dow and S&P500 all both took off on Monday, rallying by over 3%. They then followed through with gains of another 3% on Tuesday.The Nasdaq was up by even more.Given that tech was so totally beaten up, I guess the bigger rally is no surprise. You could apply the same logic to precious metals. Silver, sold down into the abyss, rose by eight and a half percent on Monday. The call for a multi-week rally in silver is looking good.Even the once internationally sought-after currency that is sterling has seen a barnstormer. A week ago everyone was talking about parity with the US dollar. It was all over the headlines (which usually means it’s time to take the other side of the trade). Even Turkey’s President Erdogan, with a display of hypocritical chutzpah that would capture the admiration of even the most duplicitous of tyrants, was deriding it. It has “blown up”, he said. He’s not been looking in the forex mirror lately at his own lira, it seems.Sterling went from $1.03 almost to $1.15.What we’re looking at is a typical short squeezeI want this bear market over as much as you probably do, and I hate to go all prophet of doom on you, but these kinds of rip roaring rebounds are just that: rebounds. They are not so typical of bull markets.Let me give you some depressing stats. 1929, 1931, 1932 and 1933 were among the worst years of in US stockmarket history. Famously so. Yet, on a percentage basis, the ten biggest rallies in the Dow Jones Industrial Average i n the first half of the 20th century all took place in those years.Prior to this decade, the best days in the stockmarket since 1950 were, says JC Parets of All Star Charts, in 1987, 2002, 2008 & 2009. Again, 2009 aside, not a great time to buy stocks.These kinds of spikes are not typical of bull markets. That’s not to say they don’t happen in bull markets, but they are more typical of bear markets. Bull markets tend to grind higher. Increased volatility, heightened fear and risk, big up days and big down days, short squeezes: these are all things you see in bear markets.Indeed, it’s a typical short squeeze. There have been lots of sellers. There are lots of people with big bets that prices will continue falling – a lot of shorts – and suddenly there are no more sellers in this crowded market. As the price turns, the shorts quickly cover their positions – which means there are suddenly lots of buyers – and the market rockets higher. It’s the sudden and rapid covering of positions that causes the spike up.Of course, sometimes you get these spikes at the final low. March 2009 was one example. March 2020, at the height of the Corona panic, was another. The problem is that on the way to that final low there have been many such up days and down days, so, in real time, you don’t actually know which this is the final one.“From false moves come fast moves in the opposite direction” is a phrase you may have heard me utter on these pages several times. Friday’s move down was one such example. A break down to new lows, below the June lows, everyone thinks we are going lower. Rumours are flying about. There’s an emergency meeting of the Federal Reserve Bank on Monday. Credit Suisse is going under. The implications of this are bigger than Lehman in 2008. Then the market turns around and rips everybody’s faces off.Rip-roaring up-days are are normal for bear marketsAs I write now, most markets have turned down again – though at present it looks more like consolidation action after the gains of the last couple of days.Here’s the S&P500 over the past year. Just look how many rip roaring up-days there have been in 2022, and yet it has been a horrible year for longs.An obvious magnet for this move is that falling blue trend line just around 4,010. Another potential target would be the 3,850-3,900 area.I’ve also shown that false move from which this fast move has come: the break below that dashed blue line which marks the June lows. What do you think? Is the final low or have got more bear market action to come?Price action tends to set the narrative, and the stockmarket tends to lead the broader economy, so even if you are of the mind that this economic downturn is not over, the stockmarket can still quite easily go higher. We are going into a good seasonal period for stocks. There’s probably too much pessimism about. We have the US mid-term elections in a month, which will give us a better idea of where things are going politically. I’ll change my opinions as events develop. I always do. We all do. But for now I think the likelihood is that this is a bear market rally.And, as for silver, I don’t think this is the beginning of the big kahuna to $50. Low- to mid-20s is my target.And if you happen to be in the Louisiana neck of the woods next week, or fancy a trip, I’ll be speaking at the New Orleans Investment Conference, which runs from October 12-1

The end of cheap money: is this finally it for UK house prices?

Back in 2007 comedian Susan Murray phoned me up with a question.She was just arranging a new mortgage and she wanted to know where I thought interest rates were going. Should she get a fixed or a variable rate mortgage?I couldn’t make that decision for her, of course. But I could see there were underlying problems with the economy – quite serious ones – so the safest option, if there was affordable, seemed to be a fixed-rate mortgage. In the event something goes seriously wrong in the broader economy, at least she was protected against spiralling interest rates.Susan went and fixed her mortgage at 6%. Turns out it was pretty much the top of the market for mortgage rates. They duly plunged as central banks slashed rates and then printed money following the financial crisis. She’s never forgiven me. “Cost me a ruddy fortune that bloke” she always complains whenever my name comes up.Cheaper mortgages mean more expensive housesI may have seen 2008 coming – I was such a gold bug at the time – but I did not foresee quantitative easing nor the extent to which interest rates would fall. Money got so cheap.By September 2021, barely a year ago, you could get a five-year fixed rate deal for 1.3%. It seems inconceivable today that money could be so cheap. To be fair, it seemed almost inconceivable at the time. No wonder everyone levered themselves up the eyeballs.I have long argued that, more than anything, it is cheap money that has driven up house prices. Everywhere you look the standard solution to unaffordable housing is that we need to build more, especially in and around London. But London has been a building site for a decade or more. Goodness knows how many new build flats there now are, but all that new build hasn’t brought prices down. As I’m forever quoting: between 1997 and 2007 the housing stock grew by 10%, but the population only grew by 5%. If house prices were a function of supply and demand, they should have fallen slightly over this period. They didn’t. They rose by more than 300%.Then you see that mortgage lending over the same period went up by 370% and you quickly realise it was newly created money that pushed up prices in a decade of loose lending, which gave birth to the national obsession that is house prices. Houses were no longer places to live, but financial assets. If you introduce new debt into a market, the higher prices will go. Look at student loans.Mortgage lending doubled again in the ten years from 2009 to 2019 and house prices rose by over 50%.Cut off the tap that is cheap money, and house prices will quickly come to levels concomitant with earnings. The two have long since been distant friends.In 1995 the house price to income ratio was below three – even in London it was only just above. Now it’s seven. The average house is seven times average income. In London it’s 11. And we wonder why families have got so small.Are interest rates only going one way from here?With inflation spiralling, bond rates rising and the US dollar spiking, money is suddenly not so cheap any more. And it’s getting more and more expensive. The UK is not alone in this, by any means, but the problem is more acute here because our economy is so geared to house prices.The Bank of England has made an absolute mess of protecting the currency, declaring it will not hesitate, while hesitating. Rather like the way it broadcast its gold sales to the market between 1999 and 2002, thereby sending the gold price to all time lows around $250/oz, so it is now broadcasting its gilt sales and quantitative tightening – and it has sent that particular market plunging too. The announcement sparked the sharp sell-off in gilts that began the day before Chancellor Kwasi Kwarteng’s mini-Budget. It’s as though the two departments – the Treasury and the Bank of England – don’t coordinate.The trigger may have been the Bank of England’s announcement, or Kwarteng’s budget. Whatever. The cause is over ten years of QE, zero interest policies and all the rest of it.It’s interesting through. At the first signs of panic, they started printing again. That tells us where they will go. Yesterday morning I would have said that interest rates can only going to go one way, and that means the cheap money taps that drive house prices to such unaffordable levels are now being turned off. Lenders clearly felt the same way. I gather over 900 mortgage products were removed from the market in under 24 hours. Smashing the record around 400 set during the Covid panic.But then the Bank of England started printing again.The UK housing market, particularly in and around London, has been an irrational, insatiable monster for decades. Anyone who calls the top has ended up with egg on their face. But we are levered up to the eyeballs. It’s not just a matter of no more cheap money coming in. There is also the other side of the coin, something I remember from 1989-1993. People can’t make their interest payments, so they start to sell. If house prices come down 10

On PayPal, Toby Young, Bitcoin, Culture Wars and the Separation of Money and State