Eurodollar University

1,418 episodes — Page 29 of 29

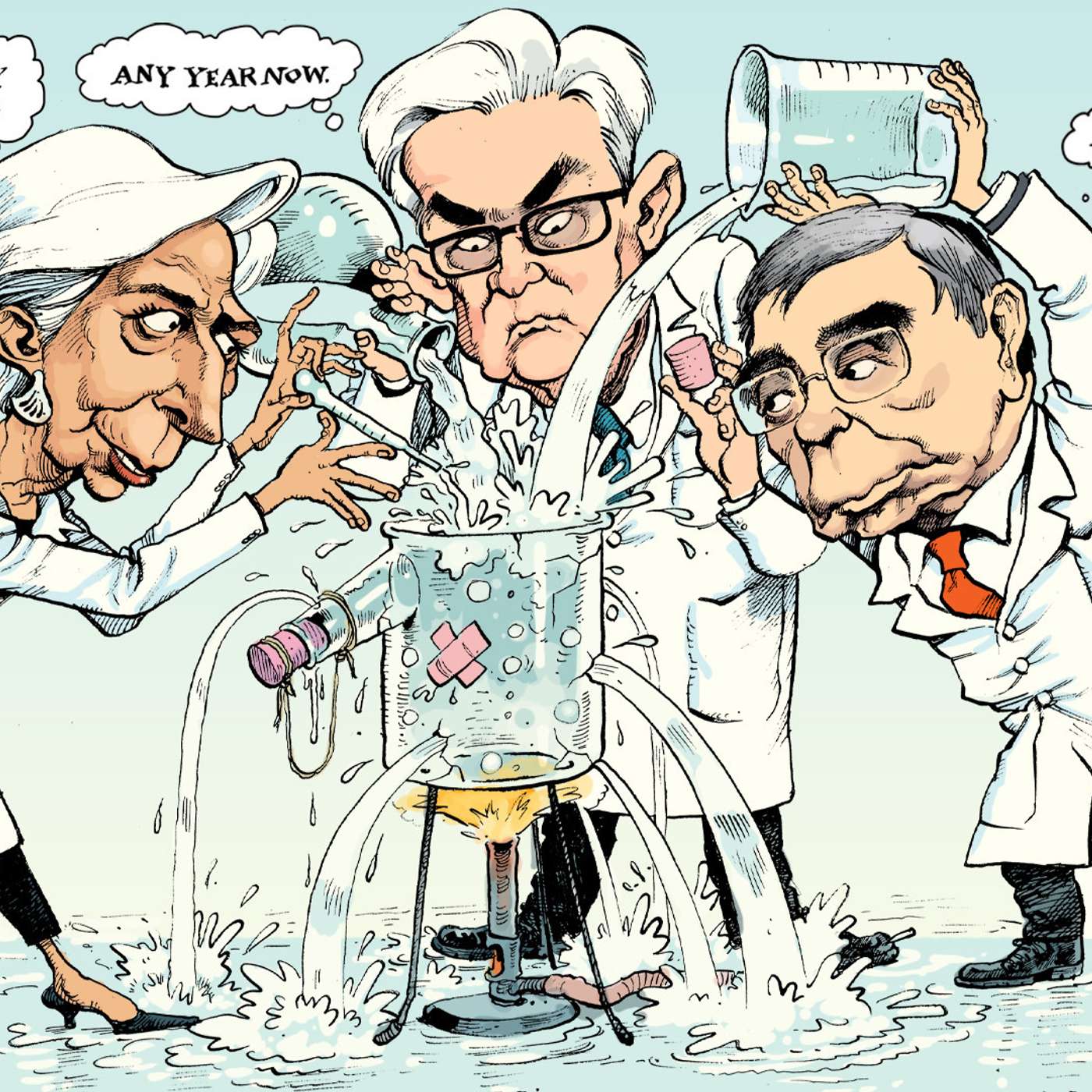

Ep 18The Fractured Flask

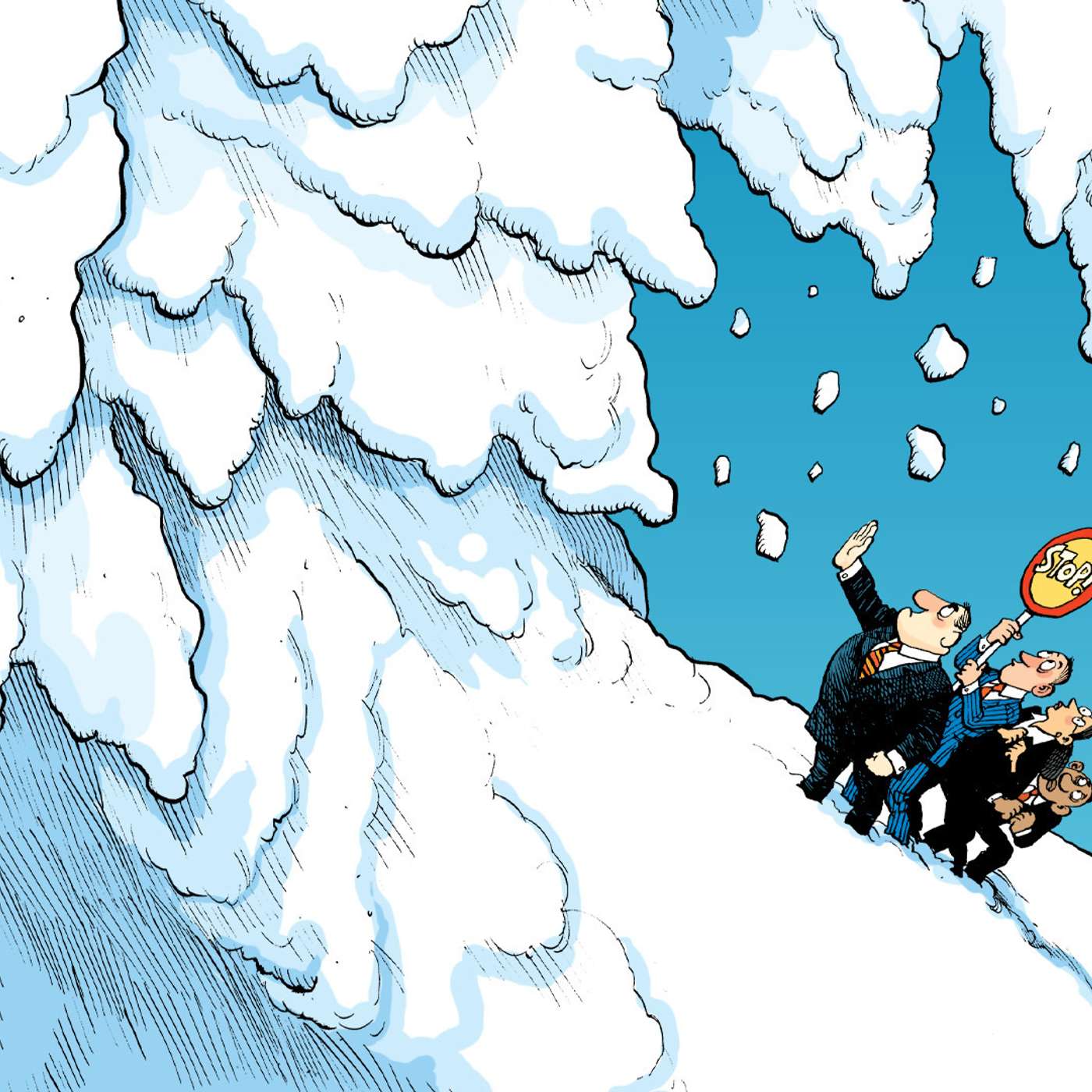

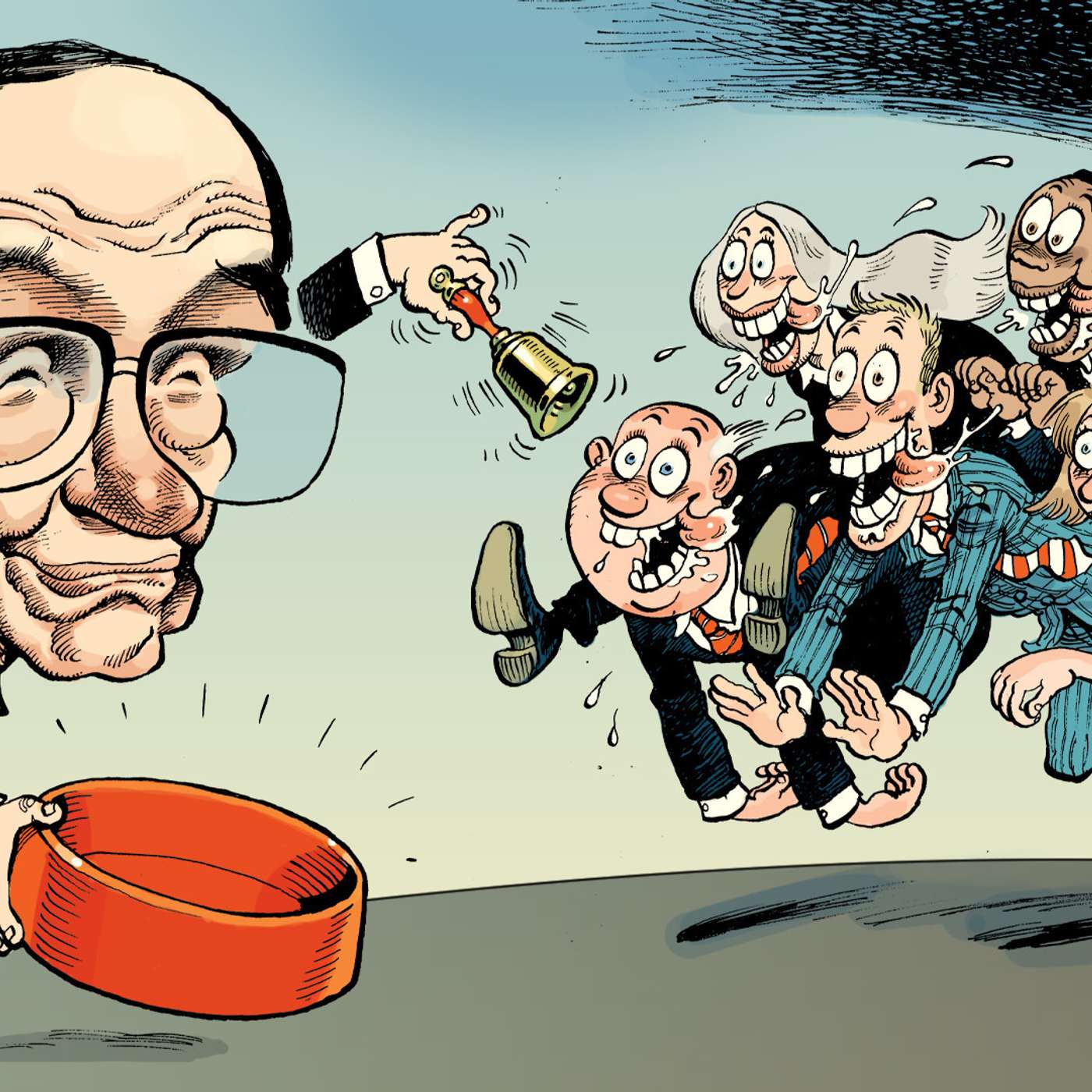

2008. Albuquerque, New Mexico. The first business meeting of what would become the best-known chemist team since Nobel-prize winners Molina, Crutzen and Rowland was not auspicious. Pinkman wanted to cook as an artist, with chili powder. White, called Pinkman's chili-p recipe -- garbage. In-turn, Pinkman dismissed White's science; all he needed was a big jar. He was actually referring to a volumetric flask, which as - the appalled chemistry teacher Mr. White responded - is for general mixing and titration you wouldn't apply heat to it. That's what a round bottom 5000 millilitre boiling flask was for. Pinkman's flasks almost certainly fractured often and leaked out.It is the metaphor of the fractured flask, the punctured pail - the leaking bucket - that Jeff Snider uses, in this the 18th episode of Making Sense, to explain why the inflationary concoction created by monetary technocrats isn't boiling over. First, we discuss why the Federal Reserve's monetization of debt isn't inflationary. Second, we review the latest inflation readings from the United States. Finally, Snider explains why the accelerating size of the US Treasury's checking account isn't inflationary either. It is all about the metaphor - technocrats and politicians pour inflationary water in yes, but not only is the bucket not a full one, ready to spill over, but it's perforated.Well, to head off a letter writing campaign, this podcaster acknowledges that a fair number of you dear listeners feel your podcasting team missed the opportunity to employ the metaphor of the leaky cauldron. To cast central bankers as a coven of warlocks preparing a witches brew of inflation. However, your podcaster prefers the analogy of the fractured flask. The technocrats style themselves as scientists, not magicians. They surround themselves with very rare 800 millilitre Kjeldahl-style recovery flasks and dynamic stochastic general equilibrium models, Griffin beakers and Erlenmeyer flasks. The tragi-comedy is that despite the scientific accouterments, they go about it in a Pinkman-like manner. Heating volumetrics, adding adulterants like yield curve control, bank reserves and chili-p.----------WHERE----------AlhambraTube: https://bit.ly/2Xp3royApple: https://apple.co/3czMcWNiHeart: https://ihr.fm/31jq7cICastro: https://bit.ly/30DMYzaTuneIn: http://tun.in/pjT2ZGoogle: https://bit.ly/3e2Z48MSpotify: https://spoti.fi/3arP8mYCastbox: https://bit.ly/3fJR5xQBreaker: https://bit.ly/2CpHAFOPodbean: https://bit.ly/3enSAkrStitcher: https://bit.ly/2C1M1GBOvercast: https://bit.ly/2YyDsLaSoundCloud: https://bit.ly/3l0yFfKPocketCast: https://pca.st/encarkdtPodcastAddict: https://bit.ly/2V39Xjr----------WHAT----------So Long As The Bucket Is Full of Holes, Treasury Demand Comes FirstTransitory, The Other WayWait A Minute, The Dollar And The Fed’s Bank Reserves Are Directly Not Inversely RelatedA General Sense of Treasury’s General Account----------WHO----------Jeff Snider, Head of Global Investment Research for Alhambra Investments with Emil Kalinowski, Pinkman. Artwork by David Parkins. Podcast intro and outro is "Full House Dusk" by River Foxcroft, at Epidemic Sound.

Ep 17Communism - Don't Call it a Comeback

Plato, Kant, Nietzsche, Buddha, Confucius, Rousseau, Aristotle, Bastiat, Molinari, Cicero, Hegel, Hobbes, Kant... LL Cool J. The contemporary philosopher sits on the social and political branch of the Western tradition. He began releasing treatises in 1985 after collaborating with Def Jam. Radio was his first. Two years later, Bigger and Deffer. But 1989's Walking with a Panther was 'too pop-y', said the Philosophical Review. 'So much empty fluff,' pondered the British Society for Phenomenology. Dialectica wouldn't even look at it. His fourth commentary however, returned him to the top. Both the album and its most famous song were titled Mama Said Knock You Out. The single famously begins with, "Don't call it a comeback, I been here for years".Singing that tune these days are Communism, Marxism and Socialism. In this, the 17th episode of Making Sense, Jeff Snider explains how to understand their philosophy and why their recent popularity is not a comeback despite the doctrine's body of work. Marxism was never gone, it was waiting for the club of mostly wealthy nations to reach the end of their capitalist potential. Well, a thirteen year depression on par with the 19th century's Long and the 20th century's Great depressions is making a good case. So then, how to counter the argument? But that's for the back-half of the show. First, a Catch-22 like paradox in bond markets. Safe sovereign and risky corporate bonds both display falling yields. Why? We look back to the last worldwide depression for answers. Then, yield curve control. This podcaster has a feeling it'll be the must-have toy for central bankers by Christmas. We look back at the US experience with the policy during the 1940s. Then Marx, Lenin and Mao take the stage, grab the mic and start spitt'n.----------WHAT----------Don’t Low Rates On Junk Bonds Mean Fed-fueled Credit Bubble? No. Precisely The OppositeYield Cap History Is Rock Solid, Just Not At All In The Way They Are Telling YouYield Caps = ToddlersFrom QE to Eternity: The Backdoor Yield CapsSocialism Would Have Been Easy to Discredit, Had There Been GrowthBrent Johnson & Jeff Snider "Breaking Down Eurodollars" Webinar by BlockWorks GroupReddit Late Stage Capitalism Thread 549,000 Strong----------WHO----------Jeff Snider, Head of Global Investment Research for Alhambra Investments with Emilulous. Artwork by David 'Straight Outta London' Parkins. Podcast intro and outro is "Callin Shots" by Damma Beatz at Epidemic Sound.

Ep 16What is... Eurodollar Mailbag?

After half-a-century, some 8,000 episodes and numerous tournament of champions the American television game show Jeopardy! decided to hold its definitive contest to determine its ultimate victor. The trial featured three accomplished champions: Ken Jennings, Brad Rutter and James Holzhauer. The selection of these three remains one of sports' great scandals -- right up there with the Czechoslovakian judge in Lillehammer. The three contenders were fine, having won more than a 100 contests and $10.7 million dollars between them. That's not bad... as far as humans go. Who should have been in the tournament?The first contestant most clearly deserved to be Phil Connors. Connors, initially a Pittsburgh weatherman stuck in a time loop, eventually attained the status of god. Not the God - at least he didn't think so - but a god. And as a deity not only did Connors know every answer in "Lakes & Rivers" - What is Mexico? What are the Finger Lakes? What is Titicaca? - he knew the question before the answer was even given: What is the Rhône?The second contestant was god-like in its knowledge: Watson. The likely forerunner of HAL-9000, this question-answering computer system already beat both Jennings and Rutter in an exhibition match for a million dollars. A eurodollar realist and having no use for a pyramid of physical bills, Watson promptly set the money alight and was heard walking off stage saying, "It's not about the money - it's about sending a message."The third contestant inhabits that shimmering space between reality and myth called "legend": Clifford C. Clavin, Jr. The part-time Boston-area mailman and full-time bar patron appeared on Jeopardy! in 1990, where he feasted on the categories like a walrus in a bed of bivalve mollusks, which is the mammal's preferred food you know. "Civil Servants", "Stamps from Around The World", "Mothers and Sons", "Beer", "Bar Trivia", "Celibacy".It is in the spirit of these latter three - as legend, as eurodollar realist, as living through a monetary time-loop - that Jeff Snider confronts listener questions in a Jeopardy!-style show in this, the 16th episode of Making Sense.----------WHAT----------Alhambra Investments BlogRealClear Markets EssaysYield Cap History Is Rock Solid, Just Not At All In The Way They Are Telling You----------WHO----------Jeff Snider, Head of Global Investment Research for Alhambra Investments with Emil Kalinowski, the Vanna White of Eurodollar Jeopardy! Artwork by the Phil Connors-like, preternatural David Parkins. Podcast intro and outro is "Come 2gether" by Ooyy at Epidemic Sound.

Ep 15Hey Kid, Want Some Communism?

Published in 1862, Les Misérables by Victor Hugo is "the novel of the century" according to David Bellos, professor of French and comparative literature at Princeton University. When asked on The Great Books podcast what qualifies this novel to be on the show Bellos responded, "It tackles a huge range of human experience, with an enormous amount of passion. If there ever was a great book, it must be Les Misérables." The story focuses on 'the suffering ones', 'the humiliated'. It's set in the social, political and economic upheaval of early-nineteenth century France. 'The poor people who are worthy of our pity' were caught up in the consequences of what Jeff Snider calls the first modern business cycle. Michael Pettis, in his 2001 book The Volatility Machine, identifies it as the first modern deglobalization. And Friedrich Engels called it "the first general crisis". Engels is, of course, the co-author of the Communist Manifesto, published in 1848 in response to the shocking, worldwide disorder. Karl Marx and Engels are said to suggest that capitalism has an expiration date; that capitalism was an ahistorical phenomenon which would burn up the limited fuel of labor and then sputter. And at that point communism would take over and redistribute the existing wealth equitably because there was a limit to human wealth creation.This, over the long sweep of history, is a pessimistic view of human character and potential. But humans don't live across history, they have a handful of decades. And when capitalism does find itself in a cul-de-sac as it did during the first general crisis, and the Long Depression, and the Great Depression and now this -- Year 13 of the Silent Depression, well then terminal capitalism sounds perfectly reasonable. In this the 15th episode of Making Sense, Jeff Snider discusses the barricades and autonomous zones of Les Misérables, Marx and Engles' thesis, late-stage capitalism, the Soviet Union, and present-day China; but all in defense of capitalism without denying that it's going down the wrong road -- toward the barricades.----------WHERE----------Apple: https://apple.co/3czMcWNiHeart: https://ihr.fm/31jq7cICastro: https://bit.ly/30DMYzaTuneIn: http://tun.in/pjT2ZGoogle: https://bit.ly/3e2Z48MSpotify: https://spoti.fi/3arP8mYCastbox: https://bit.ly/3fJR5xQStitcher: https://bit.ly/2C1M1GBOvercast: https://bit.ly/2YyDsLaPocketCast: https://pca.st/encarkdtPodcastAddict: https://bit.ly/2V39Xjr----------WHAT----------The Economic Boom You Heard About Never Really Was A Massive Problem That Has Them Searching For One----------WHO----------Jeff Snider, Head of Global Investment Research for Alhambra Investments with Emil Kalinowski, manning the barricades in the CHAZ (Cayman Highball Armorik Zone). Artwork by David Parkins, a modern-day Émile-Antoine Bayard. Music track "The Ministry" by Howard Harper-Barnes at Epidemic Sound.

Ep 14Reading Tea Leaves

Your podcaster shunned traditional university education and instead sought a guild apprenticeship. Drawn to parapsychology and the occult even as a sma' one, it was natural this podcaster's inclinations were in alchemy, phrenology, gryphography, cryptozoology and economics. However, The Inquisition and Salem Trials had somewhat narrowed opportunities in these first options; opportunities which are now reserved for only the most gifted. With an aptitude optimistically scored by one high-school counselor as "average", your podcaster nevertheless found a welcome home in economics. That field was supplemented with a minor in tasseomancy.Sometimes called tassology or tasseography, it's the study of tea leaves for the purposes of divination, fortune telling and interpreting the political economy of China. Yes, any economist can tell you about last month's results for industrial production, retail sales and fixed asset investment. And Jeff Snider does, in this the fourteenth episode of Making Sense. We first steep and then drink West Lake's famous Dragon Well tea while discussing April's Treasury International Capital report, the echoes of 2013 and the Oktoberfest-in-June-like optimism of German Financiers. But then conversation turns to the political intrigue surrounding President Xi and Premier Li. Peering inside our porcelain cups the upward strokes of the leaves indicate a stabilized GDP level. The flourishes on the lower zone denote meticulous, yet highly creative accounting. But if one observes the overall slant and the pressure of the leaves there's a suggestion of acute overcapacity, a complete lack of recovery, and a pronounced inclination toward stagnation.If the monetary shadows are your fancy then the next time someone asks, 'Would you care for some tea or coffee? Something stronger perhaps?' - you know what to say.----------WHAT----------Still TIC’ed Off In The Shadows In AprilWhen Sentiment FliesA Chinese Outbreak (of Li v. Xi, Round 2)----------WHO----------Jeff Snider, Head of Global Research at Alhambra Investments with Emil Kalinowski, who prefers his tea by leaf not by the bag. Artwork by the Yellow Mountain Fur Peak of the paintbrush, David Parkins. Song "Asian Fork Fight" by Lenzer at Epidemic Sound. Apologies to Michele Mulroney and Kieran Mulroney, screenwriters for Warner Bros' Sherlock Holmes: A Game of Shadows.

Ep 13The Great Portnoy

Upon its release the book was met with popular indifference. And no wonder. A cautionary tale about indulgence, extravagance and social upheaval? Right into the racing heart of the Roaring Twenties and its cloche hat wearing flappers, smoking Lucky Strikes and listening to jazz? No thanks. When Fitzgerald asked his editor about the book's reception he was told, "Sales situation doubtful, but excellent reviews." The author, in response, closed with, "Yours in great depression." It wasn't until the consequences of the Great Depression that the book achieved the acclaim it holds today. Only in retrospect did perception resonate with plot. Only in retrospect did the era seem an empty phantasm.Our own 'Roaring Twenty' has no such excuse. Unlike 1925 when economic depression was five years in front of those enormous yellow spectacles, our economy is 13 years in Daisy's rear-view mirror -- run over, killed. But you wouldn't know it if your radio was tuned to the business network. When it was reported in early June that the US economy unexpectedly added 2.5 million jobs for the month of May it set off an orgy of dip buying, lest there be no dip left to buy. David Portnoy, the Gatsby of our day and host of this stock market party leaves the invitation open to all via livestream and will tell you stocks only go, "Up! Up! Up! Up! Up!"In this episode we discuss how even establishment-economist forecasts -- forecasts in which the economy runs pure -- implicitly anticipate a worse experience than 2008. An experience from which the world never recovered; not really. In this episode we emerge from sheltering in place and survey the landscape. We see the Great Portnoy, hosting an elaborate party, in the Valley of Ashes.----------WHEN----------00:32 US Employment | Establishment / Household Survey02:52 US Employment | Initial & Continuing Jobless Benefit Claims04:59 US Employment | Economically Unemployed vs. Exogenous Shock Unemployment12:51 World Economy | Consensus Two-Year Outlook for GDP 16:38 World Economy | The OECD W-Shaped Recovery Doesn't Factor in a Second Economic Wave19:04 World Economy | World Bank Forecast as Warning that V is very L22:09 US Consumers | Revolving Consumer Credit Being Extinguished by Consumers27:22 US Yield Caps | Talk of Yield Curve Caps and What About Yield Curve Control in Japan32:01 US Yield Caps | World War II Experience with Yield Curve Ceilings35:31 World Economy | The Worst is Behind Us Now We Survey the Damage----------WHAT----------What Did Everyone Think Was Going To Happen?This Thing Is Only Getting Started; Or, *All* The V’s Are Light On The RightAttention All “V” PeopleA Second Against Consumer Credit And Interest ‘Stimulus’OMG The 30s!!!From QE to Eternity: The Backdoor Yield Caps----------WHO----------Jeff Snider, Head of Global Research at Alhambra Investments with Emil Kalinowski, someone that's not invited to the party. Artwork by David Parkins, the Francis Cugat of our Roaring Twenties.

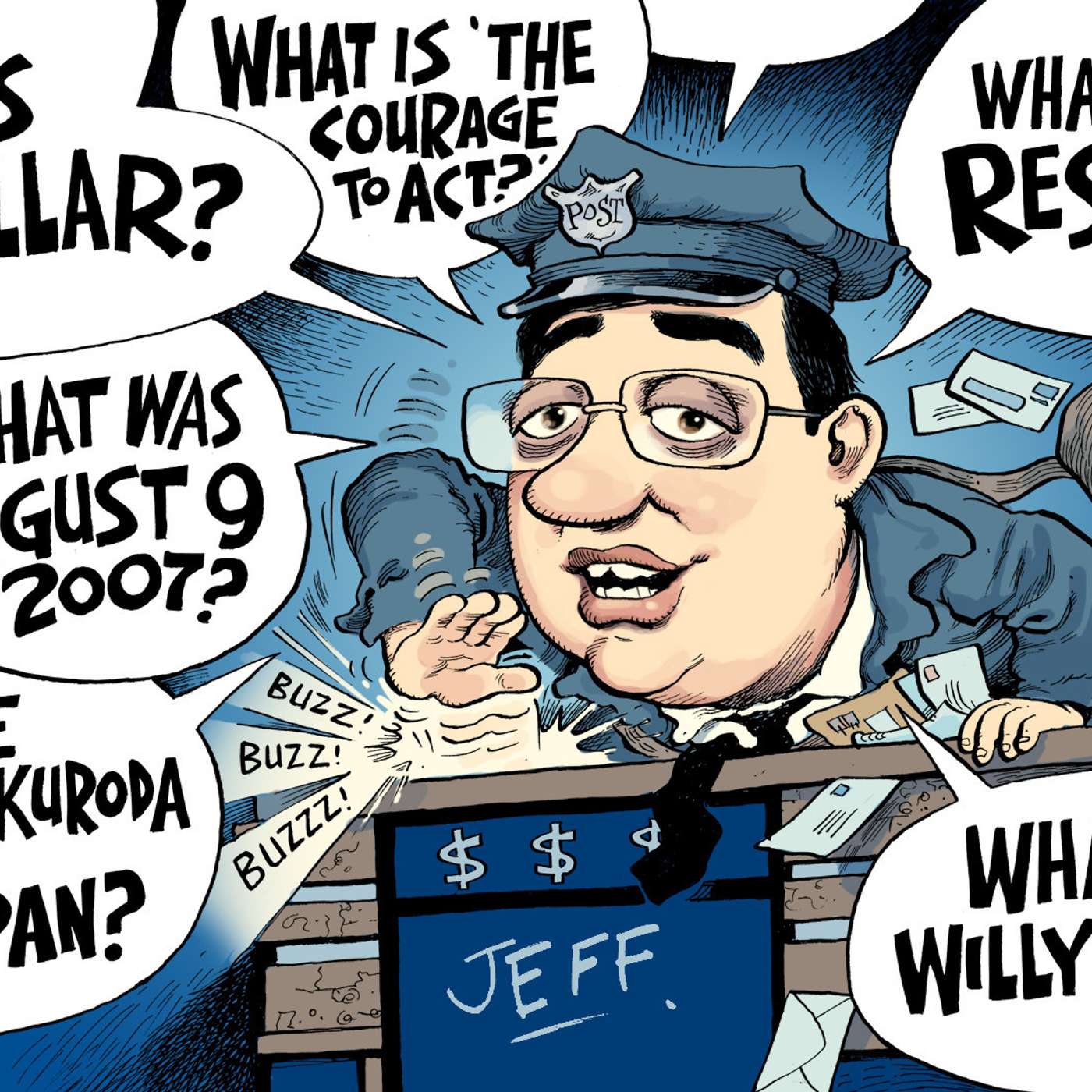

Ep 12Mailbag

Legendary figures took on the mantle of "Mail Carrier!" including: founding father Benjamin Franklin, Wells Fargo cowboys of the Pony Express, and nice guy Mr. McFeely from Mr. Rogers' Neighborhood. In more recent decades the profession saw its reputation sullied. Represented at one end of the spectrum by the austere, virginal, trivia-oracle Clifford C. Clavin, Jr. and at the other end the covetous and lurid Newman.But in this episode of Making Sense, Jeff Snider endeavors to bring back the profession's good name, just like Kevin Costner did in The Postman, a 1997 escapist fable about a post-Apocalyptic America that begins to find its soul thanks to a mailman. The film takes on a more documentary-like tone these days. Snider as itinerant nomad, wandering the dystopian monetary order delivering long lost answers to bewildered people asking why -- in a world where a smokey haze obscures the horizon -- oil is more valuable underground and stock prices are lighter than air. "Why? Why?! Why!"Sure, Rotten Tomatoes gave The Postman an 8 percent rating with one reviewer thinking, 'Relative to this, Waterworld is Citizen Kane.' Well, this podcaster disagrees and gives the movie 100 percent for British actress Olivia Williams alone.Is the US Treasury deluge good? Are banks opting out of the game? What's the deal with foreign central banks and their dollar reserves? Can the banking system function without central bank reserves? Why buy lower-yielding sovereign debt from Europe or Japan instead of the US Treasury? How to animate reserves? Should we add asset managers to the Primary Dealer pool? Is inflation low due to Chinese goods? Why is the Federal Reserve buying mortgage backed securities? Is it a violation of the Federal Reserve Act to buy risky assets? Why is the S&P500 exploding higher? Why was there inflation in the 1970s?WHATAlhambra InvestmentsRealClear MarketsMetals & Markets BlogWHOJeff Snider, Head of Global Research at Alhambra Investments with Emil Kalinowski, not mailman material. Artwork by David Parkins, il primo ballerino of the colored pencil.

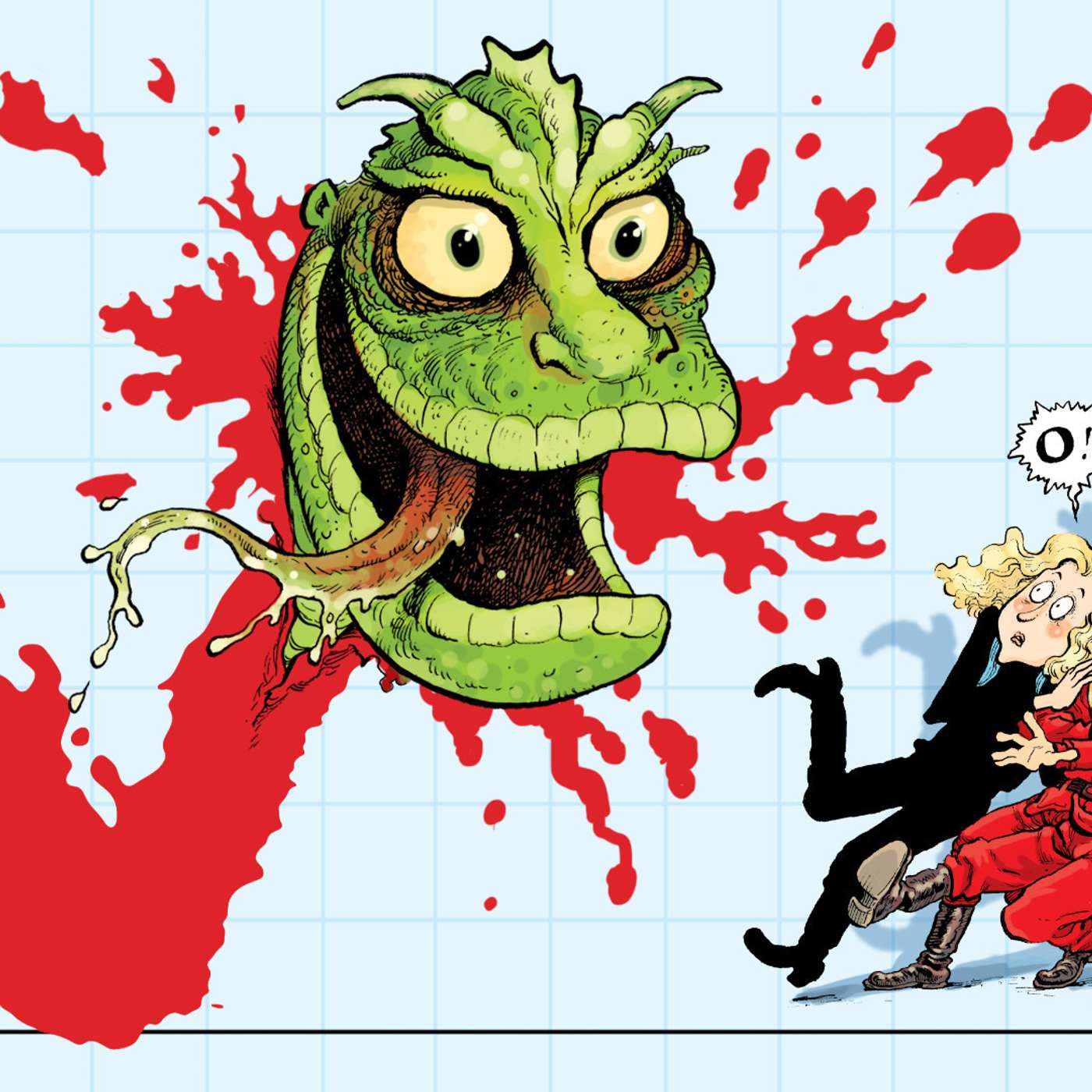

Ep 11The Worst V Since "V"

In the mid-80s parents allowed their children to watch an innocent-looking television program titled V thinking it was some kind of Sesame Street offshoot. Imagine little Johnny and Suzy Q's horror when, instead of Reading Rainbow, they were watching a sci-fi melodrama about disguised reptilians. The Visitors, presenting themselves as competent, benevolent beings here to teach the backwards ape a few things, were hiding behind masks -- including their beautiful smokeshow of a leader Diana -- and had actually come to harvest Earth's water and snack on humans. A sophisticated allegory about economists? Perhaps...The mini-series had been the reigning champion of "Worst V of All Time" until the 2007-09 financial crisis, which sent the global economy off its post-World War Two trend. Unlike all downturns since 1945, this one was different in that a plurality of economies representing a majority of global gross domestic product never regained their pre-crisis trend growth. The V-shaped recovery that three generations had come to take for granted turned out to be a grossly misshapen, lizard-like L that was visible beneath the mask of positive numbers in all manner of broad economic accounts, including: global foreign direct investment, world merchandise trade, the 35-country Organisation for Economic Co-operation and Development industrial production index, etc.In this eleventh episode of Making Sense, Jeff Snider, Chief Investment Officer of Alhambra Investments (and Resistance Leader) explains why 2020 may surpass the intergalactic reptiles AND dethrone 2007-09. We review the US Congressional Budget Office's very un-V forecast through 2021, estimate in trillions the depth of the contraction in the US, put into context Washington D.C.'s inadequate-sized stimulus and review the Euro Area's broad survey of economic confidence.No iguanas were hurt in this episode.WHATGetting A Sense of the Economy’s Current Hole and How the Government’s Measures To Fill It (Don’t) Add UpThe *Optimists* Have Some Terrible News For the ‘V’What Would The Hole Be Without The ‘L’?What Flood?WHOJeff Snider, Head of Global Research at Alhambra Investments with Emil Kalinowski, still working on his ABCs. Artwork by David Parkins, mammal.

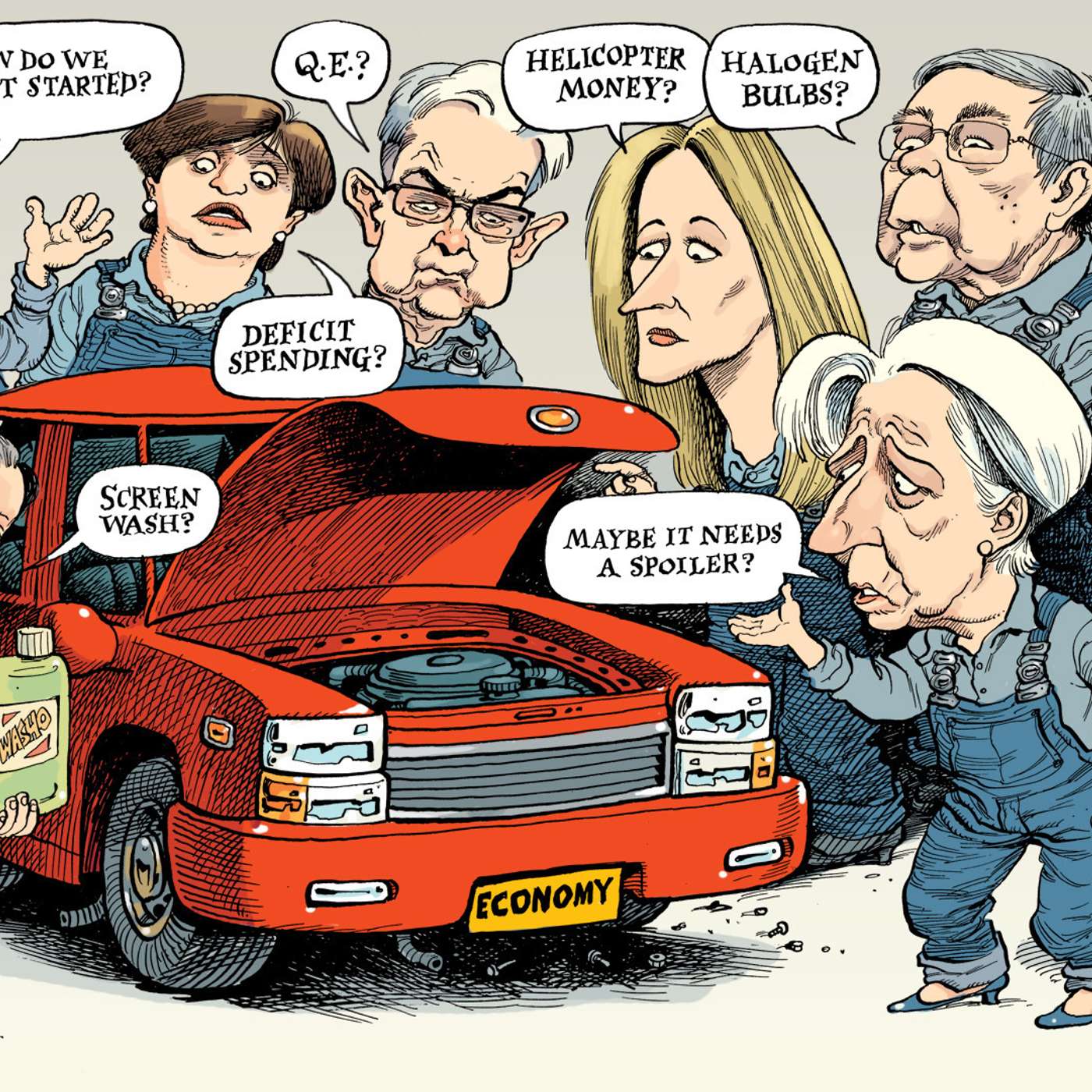

Ep 10Stock Magiq

We are informed by the financial press the agitated creation of reserves are, to capital market participants, a mix of whiskey and Felix Felicis; liquid courage and luck. The first manifestation of the wealth effect, which will encourage households to consume and corporations to invest. The financial market animal spirit. The economist's Patronus Charm. But what did the Federal Reserve do - and more importantly not do - in 1929, 1987 and throughout 2008-20 to support US stock markets? When was there a direct link between bank-created money and the stock market? And when was there nothing more tangible than "expectations policy" - the modern equivalent of the warlock's frantic charms, hexes, jinxing and spell-casting? Also, Federal Reserve Chairman Jerome Powell was interviewed on the American news program 60 Minutes this week. He said, the Fed saw the market meltdown coming, that the central bank increased money supply - he says they can print 'real' money too, you know - that there's no limit to what they can do to support the economy (and also that the said economy may not 'get back to zero' until the end of 2021). We review the interview by pointing out what the smoke is obscuring, where the mirrors have been placed, and discuss how "theatricality and deception are powerful agents to the uninitiated." WHATStocks Haven’t Been MoneyedThe Reason For So Many Lies: He Finally Realizes He’s In Way Over His HeadWHOJeff Snider, Chief Investment Officer of Alhambra Investments with Emil Kalinowski, a physical (precious metals) man; artwork by David Parkins, sculptor of the color wheel.

Ep 9Japanification

It is often said that there is, "nothing new under the sun", and with a few exceptions (e.g. negative nominal interest rates, negatively priced oil, TikTok) that is true, even with a monetary gewgaw like quantitative easing. Japan, so as to revive its economy, has been implementing different flavors of QE for just under two decades now (that's all one really needs to know about its effectiveness). In this episode we explore what lead up to the first QE program with a tour guide: Milton Friedman.What was Friedman's analysis of 1970-90 from the perspective of money supply and economic activity? How did the Bank of Japan seemingly lose its way during the 1990s when it had 'got it all right' during the 70s and 80s? Why did Friedman believe that QE would be the solution? Why did the Japanese bond market disagree from the get-go? Why is a sovereign bond market important anyway? Why do low rates - not high - signal monetary tightness and vice versa? On the other side of the Pacific, in late 2001, with the Good Ship Q.E. having already been launched, researcher Mark Spiegel from the Federal Reserve Bank of San Francisco raised a critical question: what if private banks don't want to put this newly 'printed money' to work? In Japan that question has remained unanswered for two decades. In the United States and Europe? Over a decade. Is it a matter of difficulty or ideology that impedes the answer? We believe it is the latter.WHATThere Was Never A Need To Translate ‘Weimar’ Into Japanese by Jeff SniderReviving Japan by Milton FriedmanQuantitative Easing by the Bank of Japan by Mark SpiegelA Tally of 23 Japanese QEs by Jeff SniderWHOJeff Snider, Chief Investment Officer of Alhambra Investments and Emil Kalinowski, not bad at fantasy football. Artwork by David Parkins, curator of the illustrated aesthetic.

Ep 8Mailbag

Will unlimited dollar swaps by the Federal Reserve solve the dollar shortage? How does collateral shortage in the repo market affect, for example, equities? Why does the gold price plunges when there are collateral fails in the repo market? Does re-pledging and/or re-hypothecation take place in the repo market? If there's liquidity crisis, why do corporations get such cheap loans still? Interest rate swaps go negative; what does it mean? Why aren't bank reserves useful to the monetary system? Why does a financial entity sell cash to buy a Treasury to put it up as collateral to get cash; wut? What is an individual to do in this chaos? Does stress in the interbank markets reach the real economy and if so, how? What is your definition of inflation and does asset inflation factor in?Sadly, we did not get to each inquiry. Also, some did not really pose questions but took the opportunity to send death threats and ransom notes; we love the passion! (But yes, we didn't get to those either.) However, please continue asking questions on Twitter and YouTube, and if we - or someone from the community - don't answer there, we hope to do so on a future show. WHATAlhambra InvestmentsRealClear Markets Metals & Markets BlogWHO@JeffSnider_AIP, Head of Global Research at Alhambra Investments with @EmilKalinowski, professional gentleman of leisure. Artwork by David Parkins, paintbrush performance artist.

Ep 7No Modern Weimar Republic Here

Quantitative easing, like foie gras, is controversial. The gavage-based production of duck and goose livers is considered cruel to the animal, gorged helplessly as it is in a pen. Central banks likewise perform a force-feeding, a monetary gavage of reserves forced onto the private bank balance sheet. What makes it a peculiar practice is that the monetary farmer expects this gorged banking goose to then dance around carefree - honking out credit at every passing leaf or tussled blade of grass. Since 2001 this 'monetary husbandry' has failed. In Japan, the United States, Britain and Europe. (Worse still, the result isn't a rich, buttery and delicate specialty that could be enjoyed with some mustard seeds and green beans in duck jus.) In this episode we review three articles that delve even farther back in history, to the Great Depression, to show that similar sounding solutions didn't work then either. The fear of unchecked inflation - "Weimar", for short - now that fiscal authorities and central banks are both encouraging the leaden economy to flap its wings is therefore misplaced. At least, not until wholesale reform of process and procedures within the modern central bank. Not until credibility and competence is prioritized over its credentials.WHERE@JeffSnider_AIP@EmilKalinowskiWHATWeimar Ben Didn’t Happen, So Now Weimar Jay?Weimar Thirties Didn’t Happen Because It’s What You Don’t See Everyone Knows The Gov’t Wants A ‘Controlled’ WeimarChicago Fed's Monetary Policy in a Lower Interest Rate EnvironmentWHOJeff Snider, Head of Global Research at Alhambra Investments with Emil Kalinowski, one of several people - along with Archibald Leach, Bernard Schwartz and Lucille LeSueur - who've never been in your kitchen. Artwork by the Brunelleschi of our day, David Parkins.

Ep 6Fragile, Complex Systems

In 1929 a plague struck Florida resulting in an overwhelming government response. The consequences were not only agricultural but financial as banks, heavily exposed to the Sunshine State's horticulture sector, approached insolvency. Bank stability, Federal Reserve responses and a suitcase stuffed with six million dollars are all part of the thrilling story. But so is the notion of bureaucratic delay, wild swings from hope to despair (and back), contemporary titans of industry offering reassuring words, and the impotence of human effort against the monstrous chaos of a complex system reverting back towards simplicity.In today's day, the US Treasury bond market was warning for the better part of two years that the monetary, financial and economic - to say nothing of the political and social - facets of our system were fragile. Weak. Already enervated by six years of political upheaval and a dozen years of monetary disorder. The virus was the banana peel upon the wall that Humpty Dumpty was dancing on.The United States and European Union GDP estimates for the first quarter corroborate the bond market's opinion. Though the virus, and the government response to it, only took hold in the final month of the quarter (with exceptions of course, Italy for example) the result was catastrophic nonetheless. In other words, the US and EU economies were already stumbling about the street, late at night after a 12-year bender when Corona stepped out from the shadowy alleyway with a billy club and an appetite for mayhem.1929 Florida Plague as ParableBond Markets Dismiss FedQ1 US GDPQ1 EU GDPJeff Snider, Head of Global Research at Alhambra Investments and Officer of the Offshore with Emil Kalinowski, Getting His Pump On. Artwork by the Caravaggio of caricature, David Parkins.

Ep 5Modern Myths

The Earl of the Eurodollar Jeff Snider (@JeffSnider_AIP), Chief Investment Officer at Alhambra Investments and Emil Kalinowski (@EmilKalinowski) discuss the four topics.First, what happened this past week when the price of oil to be delivered in May was priced at a negative $50(ish) dollars per barrel? And much more importantly than the bizarre price, what does the back-half of the oil futures curve say about the medium-term condition of the global economy? Nothing good unfortunately.Second, why do well respected names in the financial industry continue to believe that US Treasury yields will rise? They are called Bond Kings and one of them recently had to take off his crown (temporarily). But was it the Fed's changing policy that caused the change of heart? Or was it the bond market all along who was signaling the bond kings wore crowns but nothing else?Third, the important German ZEW survey shows very sharp pick-up in optimism. No surprise, ZEW survey respondents traditionally respond very positively to central bank 'liquidity' programs, even if the real economy does not follow through. It is the legendary Greenspan Put gone international.Fourth, the multi-decade Japanese experience regarding 'overwhelming' purchases of stocks and bonds is instructive for investors counting other advanced economy central banks buying financial instruments. It seems bullish, on the surface at least. But recently the Bank of Japan opened the taps and increased their equity purchases to record amounts. The result? A 31 percent decline. You're welcome.Alhambra Investment articles discussed:Let Japan Show You Again Just How Laughable The Idea That Central Banks Can Support MarketsThe Greenspan BellThe Fallen Kings & The Bond Throne of CollateralWhat Was Monday’s Negative Oil, And Why It Was Overshadowed On Tuesday

Ep 4Oil Bears, Equity Bulls

Jeff Snider, Chief Investment Officer of Alhambra Investments and Baron of the Balance Sheet @JeffSnider_AIP and Emil Kalinowski, Not Hard on the Eyes @EmilKalinowski.The World Trade Organization offered two outlooks for 2020-21, one that is not terrible and the other distinctly so. Jeff and Emil discuss how getting back to previous levels would be an impressive achievement in itself and how it suggests that central bank actions are limited in their impact on the broader economy.The US labor force shrank a horrifying 1.6 million people in March which is almost as much as the entire 2007-09 contraction. Jeff explains what the difference is between unemployment and exiting the labor force entirely.The oil market has experienced a conniption fit over the last month but in the last couple of weeks only the front half of the futures curve is still having a full body dry heave. The back half, the half that represents market expectations of future economic activity levels, has settled down. Where it has gotten cozy offers no inspiration about the economic outlook.

Ep 3Confronting the Dollar Bull

We draw on five articles posted at Alhambra Investments to draw out the difference between a central bank - central to money supply - and a bank authority - central to a smooth functioning banking system. Jeff notes that we are not facing a local banking crisis that requires a banking authority but an international 'money' supply problem (there's not enough of it). Not only is the Fed not central to that money supply but nobody is. Interestingly Jeff is not concerned about another banking crisis per se as the banks have been barricading themselves behind "fortress balance sheets" for a dozen years now. Also, Jeff explains why he's not - for now - concerned about a sovereign debt default cycle nor a corporate credit default cycle. Instead he fears a 2008-style (or worse) liquidity crisis. This entirely plausible - and perhaps straight up probable - crisis would then starve perfectly healthy businesses of the required funding to keep operating.Articles covered include: "What Is The Fed’s New FIMA? The Potential For A SHADOW Shadow Run Is Very Real", "Banks Or (euro)Dollars? That Is The (only) Question", "(No) Dollars And (No) Sense: Eighty Argentinas", "Dollar, Not Bank" and "The Empty Bank".

Ep 2Greatest Liquidity Event Since Noah?

Jeff Snider, Alhambra Investments Chief Investment Officer (@JeffSnider_AIP) and Emil Kalinowski (@EmilKalinowski) review three topics. We review three articles Jeff wrote this week, trying to explain them a bit more than perhaps may be apparent at first glance. Firstly, why repurchase agreement stresses materialize prior to quarter-end. Secondly, why low-low-low-limbo-proof interest rates (e.g. effective Federal Funds, overnight repo market rates) are not signalling success but further interbank stress. Thirdly, why LIBOR and near-month Eurodollar futures are rising despite the "greatest liquidity event since Noah".

Ep 1QE-Infinity is a Laundromat Token

This inaugural episode discusses the goal of building a collaborative, educational community to discuss the creation, destruction and redistribution of modern monetary formats throughout the global economy. A strange kind of money, so unlike what we're used to seeing in our pockets, but a money that is needed to finance activity, trade and progress. We briefly touched upon the nature of money, the un-centralness of central banks and identified the financial collateral markets - not cash or bank reserves - as the source of the monetary disorder that has spilled out into the broader economy in conjunction with the developing international health emergency. The disorder is in the repurchase agreement market and it lies with collateral, specifically there's not enough of it. Hence, these intermittent liquidity squeezes that have over the past 12 years spread like contagion into the wider economy. "You can't take out your spine and hope to stand up; that's really what the [repurchase agreement] market is. The way the repo market functions is more collateral-based than it is bank reserves or cash. The lack of collateral is a massive, massive problem."