The Macro Compass

131 episodes — Page 1 of 3

Run It Cold Now, Run It Hot Later

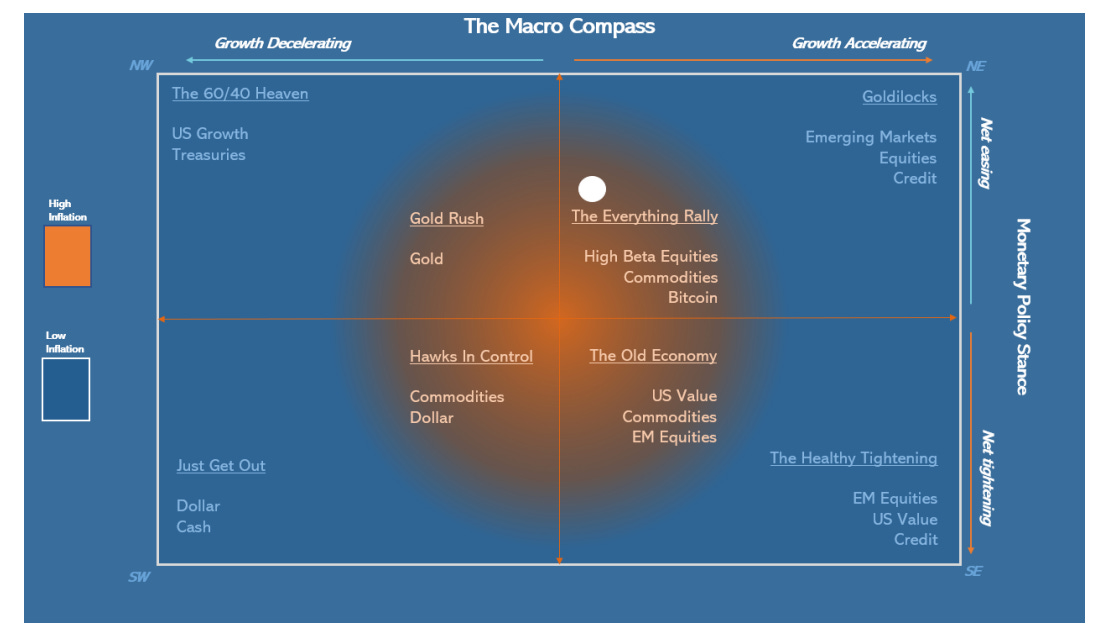

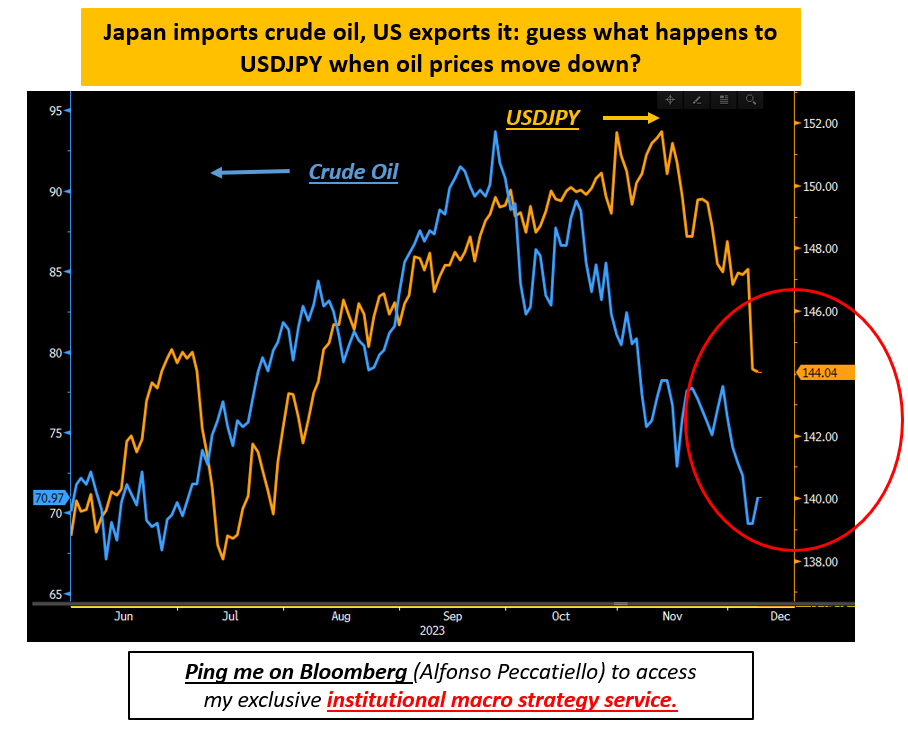

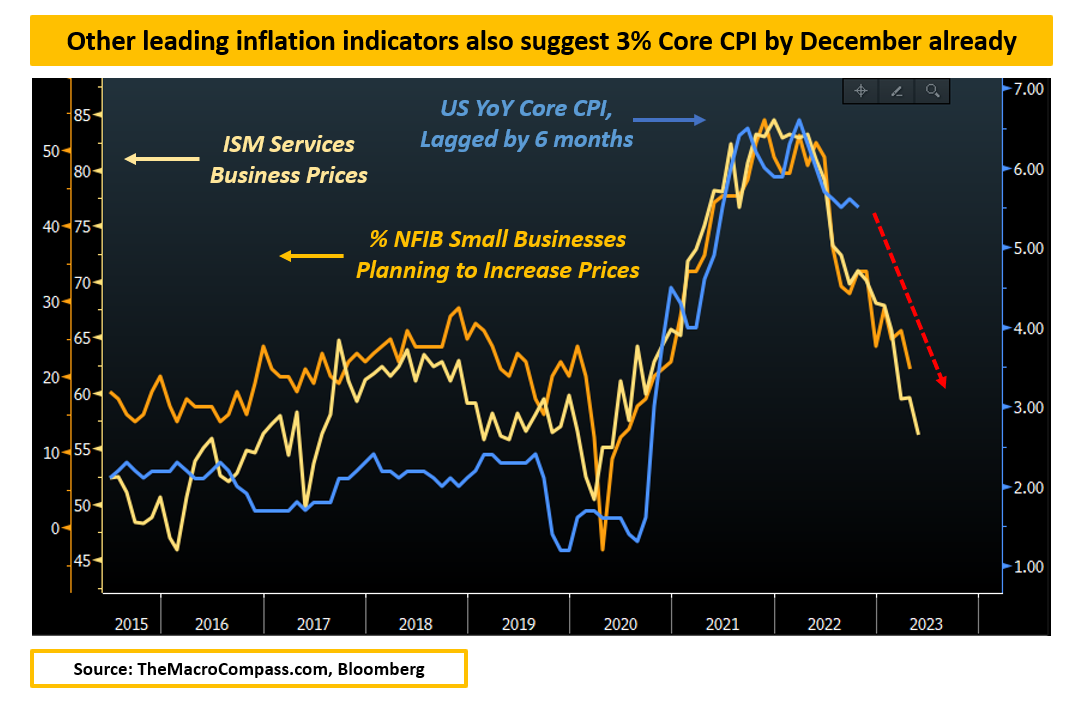

Hi everyone - this is Alf.I hope you’re having a great day.My macro models have been suggesting a bi-modal framework to approach markets for the near future: Run It Cold Now (growth My Run It Cold Now theory has been increasingly vindicated by labor market data, and markets are often busy trading what’s in front of them rather than looking through a potential reacceleration in 2026.This is why it’s vital to figure out:1. How early/late do we sit within the ‘’Run It Cold Now’’ period;2. How much has the market priced in by now;3. Consequently: is it still worth getting engaged in Run It Cold trades, or shall we look at Run It Hot Later ideas already?As a reminder, my macro models suggest tariffs will act as a fiscal tightening mechanism until year-end.By early 2026, the OBBB fiscal impulse will offset and Trump’s new initiatives alongside lowered Fed Funds and private money creation should propel a Run It Hot Later period.First, some evidence that US labor demand is really weak: extrapolating benchmark revisions from April 2025 onwards, the US has been consistently shedding jobs!To get a broader perspective on the labor market we can rely on unrevised data which incorporates demand and supply for labor: for example, unemployment rate and its important subcomponents.The chart below shows the number of long-term (27+ weeks) unemployed Americans as a percentage of the total labor force. At 1.14%, this number is already as high as in 2002 or summer 2008 – in both cases, a recession was already visibly hitting America:Why is US labor demand so weak?Due to tariffs, the US is going through a slowdown of its primary fiscal impulse: the 2025 primary fiscal deficit sits almost 20 bps below last year and markedly below the 2023 pace.Tariffs are effectively acting as a tax on US companies and consumers:This seems to be confirmed by ‘’the best economist Druckenmiller knows’‘: the internals of the stock market.The chart below shows (in white) the ratio between an index of the 5 largest US payroll processors companies and the equal-weight SPX, plotted against 2-year Treasury yields (in green).If there are no new jobs, the largest payroll processors companies in the US will suffer - and indeed, their stocks are trading very weak.This is an example of how the internals of the stock market suggest the US labor market is very weak, and that the Fed will be soon called to ease more:The US economy is ‘‘running cold’’ now, yet stock markets are roaring and risk sentiment remains very aggressive - why?The private sector money printer is going BRRRR, led by AI.The chart below shows the big-tech announced capex spending as a % of their EBITDA – it’s already over 65% on average, exceeding the AT&T spending of 1998. To keep up this pace next year, companies will have to resort to debt-funded AI capex:AI Capex mechanically adds to US GDP even before we get to talk about the ROI.But the biggest issue with AI Capex is that it doesn’t really add jobs for the median American for now, and hence we are left with two economies: a hot AI-related economy, and a broader labor market struggling under the fiscal tightening induced by tariffs.The stock market is not the economy, and the gigantic AI capex effort coupled with large global fiscal stimulus programs continues to support risk sentiment.Our global real-economy money printing index is very strong.We tracked the YTD pace of inflation-adjusted $ money creation around the world, and this year we have scored an impressive 5.77% increase in real-economy money printing around the world.This comes after 3 weak years led by the gigantic Chinese housing deleveraging, and the YTD pace in 2025 is in line with the ‘’concerted global growth’’ pace of 2017.The global pace and acceleration is quite robust, and its mainly driven by China which has restated its credit engines after 2-3 years of robust housing deleveraging.Despite being crippled by tariffs (e.g. a large tax), US money creation is accelerating led by the AI-related debt-funded capex spending on data centers.And money printing is only set to accelerate going forward.From a fiscal standpoint, we are 100% sure that from early 2026 we will see:- Germany adding to money creation via a large increase in primary spending;- The US OBBB kicking in with its fiscal stimulus offsetting tariffs money destruction;- Korea, Sweden, and many other countries kickstarting deficit spending programsWe might be looking into a scenario where the Fed cuts rates but global money printing accelerates.If we dust off my TMC Quadrant Asset Allocation Model, that puts us in the top-right quadrant:In short, historically the best asset allocation for such an environment involves selling IOUs and paper assets, and buying tangible risk assets.Basically:* Sell USDs and bonds, * Buy stocks and assets linked to nominal growthThe most painful outcome for institutional investors would be an equity rotation towards EM/Value + a commodity rally.These are very underowned asset class

May The Odds Be Ever In Your Favor

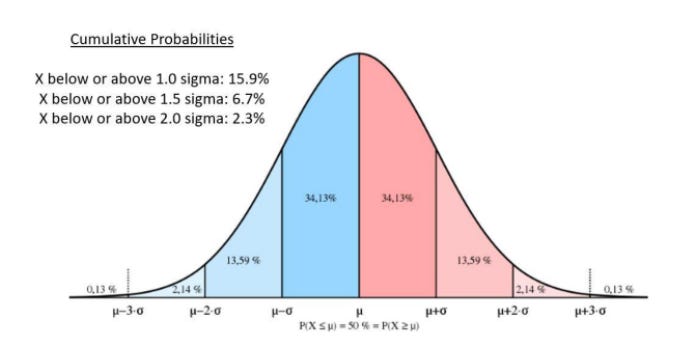

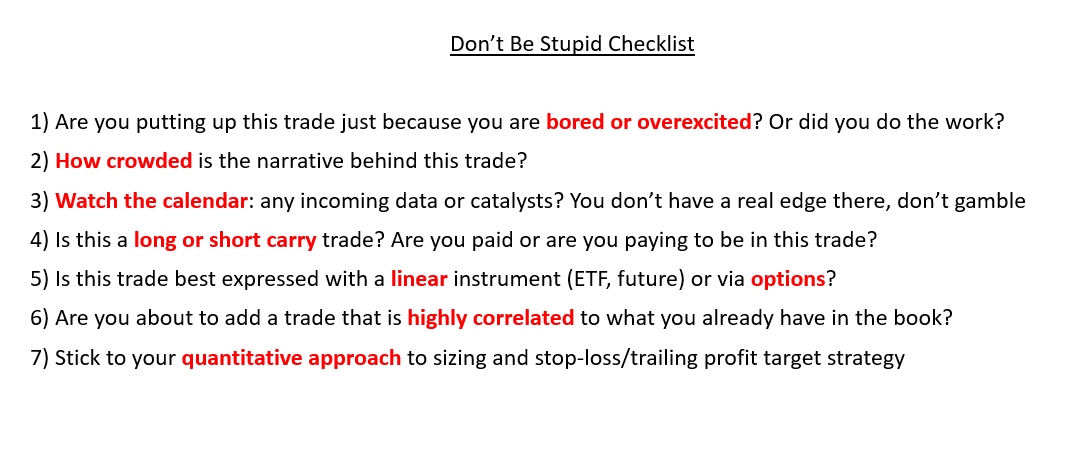

Hi everyone - this is Alf. I hope you're having a great day.‘’I compile statistics on my traders. My best trader makes money only 63 percent of the time. Most traders make money only in the 50 to 55 percent range. That means you’re going to be wrong a lot. If that’s the case, you better be sure your losses are as small as they can be, and that your winners are bigger.’’ – Steve Cohen.This is a hard truth to accept for many macro investors: we will be right only about 50-55% of the times.If your win rate is much higher than this, I suggest you extend the sample of trades you are analyzing or assess whether you are not trading macro but rather just selling optionality – short vol/option strategies have win rates as high as 90%+, but they wipe you out completely when you are wrong.In the last 10 years, I scored a 52% long-term win rate on my directional macro trades. Once I realized that and given that the year-end P&L formula can be written as follows:I knew I’d better make sure the size of my losses doesn’t get out of control.This can be achieved in two ways: sizing trades correctly and designing a system that lets your winners run. We are going to talk about my approach to both angles in a second, but first another important remark.To step up the win rate on macro trades from 50% to say 55% over a long period of time, you need to gain some edge over other macro investors.What could that be?- A data-driven approach with superior macro models- The ability to assess the gigantic amount of cross-asset market signals via quantitative tools- A particular edge in a niche market that you have learnt to navigate well over time- Be less stupid than othersMacro models help a lot, but my ‘’don’t be stupid checklist’’ adds value too:Points 1-3 keep my emotions in check and ground me to a more rational assessment of the trade.Points 4-6 are about implementation.A warning: short carry trades (and long options) are expensive to hold over time if nothing happens.A reminder: in very choppy markets, you can get quickly stopped out with linear trades even if your thesis proves to be correct – consider whether the market regime favors linear or option implementations.Don’t be stupid: check whether the trade you are about to add is not just another expression of a trade you already have on – I have seen people blow up as the 10 trades they were running were just…the same trade.But it’s point 7 that sticks out: sizing and risk management define most of your P&L at year-end.Here is how I approach them through a practical example. Say you think that the S&P500 will keep marching higher over the next month: how many SPYs do you buy?You could be in the right or left 50% of that distribution: when you pull the trigger, you don’t know that. And because you don’t know that, you want to standardize your ex-ante sizing.One effective way to standardize the sizing of each tactical trade so that they don’t excessively weigh on your year-end P&L is to do volatility-adjusted sizing: let’s go through the SPY example.You could be in the right or left 50% of that distribution: when you pull the trigger, you don’t know that. And because you don’t know that, you want to standardize your ex-ante sizing.One effective way to standardize the sizing of each tactical trade so that they don’t excessively weigh on your year-end P&L is to do volatility-adjusted sizing: let’s go through the SPY example.Let’s set our stop at 1.5 standard deviations, and our defined time horizon in this example will be 1 month. For the SPY, using a 5-year lookback the typical 1.5x monthly negative sigma event would be a -7.6% decline.You can play around with the lookback period if you want more history and/or assign different weight to more recent periods if you think today’s vol regime is more relevant (grey boxes).If returns are normally distributed, we will be stopped out 6.7% of the times in our defined time horizon. But as returns often follow other distributions, it’s good practice to check the actual empirical probability of being stopped out against the theoretical 6.7% probability (orange boxes).Finally, define what’s the fixed % of AuM you are willing to lose on any given macro trade.A fictitious $1 million trading account willing to lose max $20k per trade which is bullish on SPY with a 1- month horizon would buy 571 SPY shares at $437 and be stopped out at $402 (-7.6% = 1.5x sigma event) hence losing $20k (= 2% of AuM).Congratulations, you just applied volatility-adjusted position sizing!What are the advantages of this approach?1) You remain agnostic to ‘’volatility luck’’: if you size all positions the same, being right/wrong on the most volatile assets will make/break your P&L at year-end and that’s all about luck. Don’t gamble.2) You remain agnostic to your ‘’conviction’’ level: the truth is that ex-ante you don’t know when you’ll be in the right or wrong 50%, so why would you over or under size a trade based on your ex-ante conviction levels? You shouldn’t.3) T

Plumbing Risks Ahead

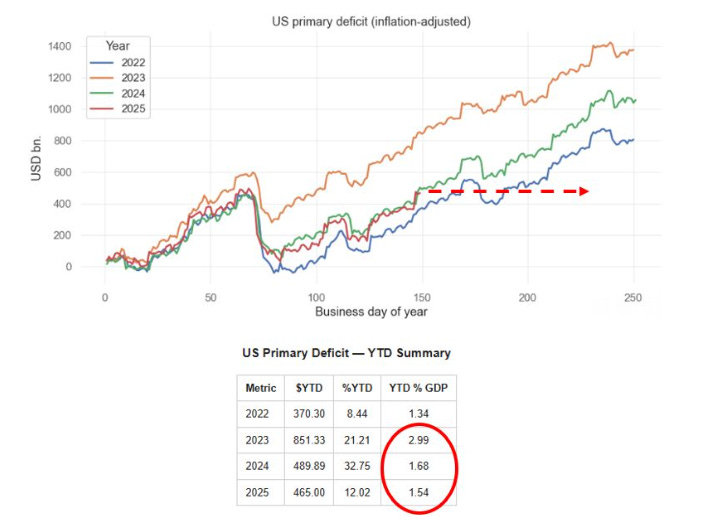

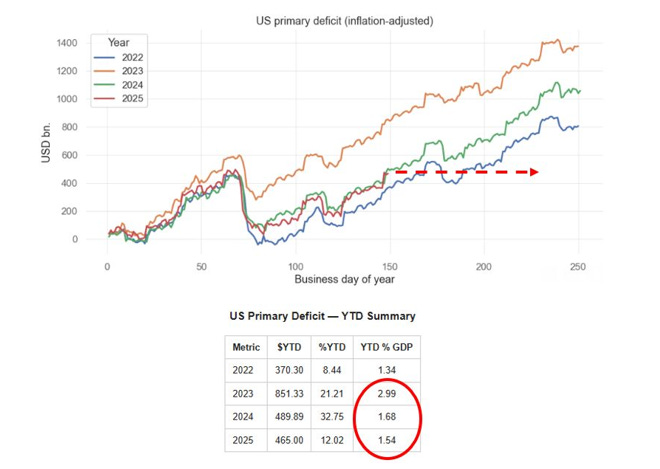

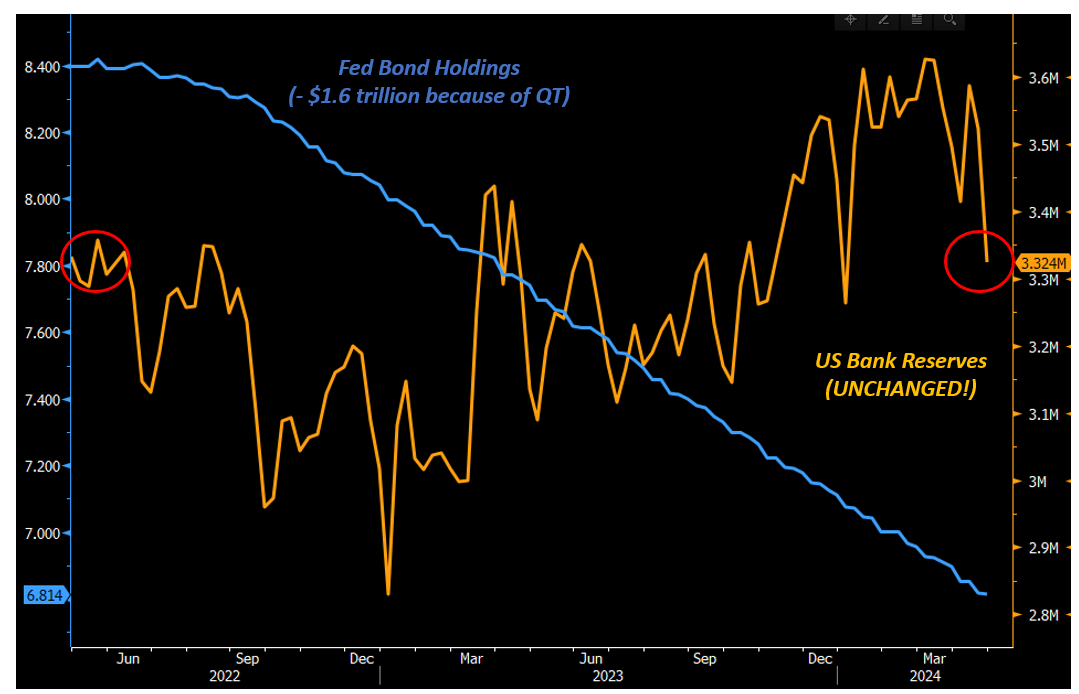

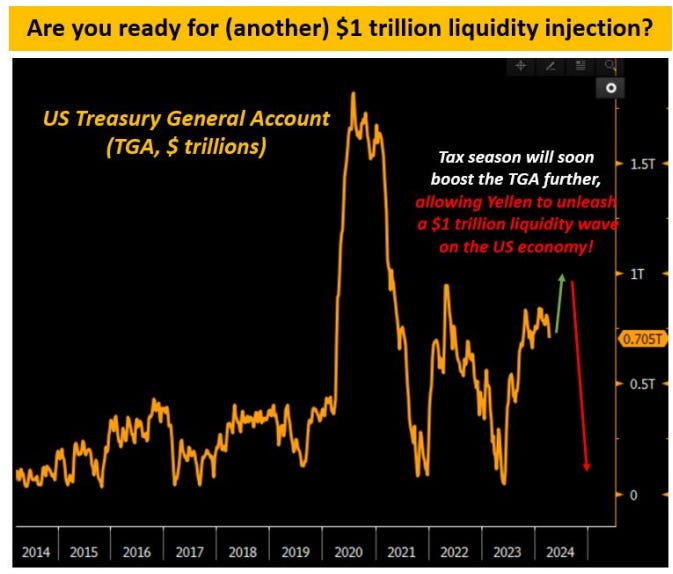

Hi everyone - this is Alf. I hope you're having a great day.The US economy and markets might face a double negative whammy over the next 2 months: a large reduction of the fiscal impulse and the aggressive rebuild of the Treasury General Account (TGA).A slowdown in real-economy money creation (primary deficits) could result in an economic slowdown, which will coincide with a drainage of bank reserves (TGA buildup) from markets.Our US primary deficit tracker stands at 1.54% of GDP as per last week, already lagging behind the 2024 pace and way behind the 2023 staggering pace.Tariffs came in at almost $30bn in July, and were this pace to continue we’d effectively face an additional $150bn of fiscal drag until the end of the year.That alone means the US primary deficit might shrink by 15% from $1 trillion in 2024 to $850 billion in 2025:As a reminder, primary deficit spending = money being injected in the real economy.Literally, we are talking about money printing.As step 1 the US government spends money (e.g. cuts taxes) which increases the bank account of households which receive an injection of net worth – they pay less taxes, hence their bank accounts are fatter. Bank deposits grow at commercial banks, which as a result see their reserves at the Fed grow too.Step 2 describes the bond issuance pattern: the US government issues bonds to ‘’fund’’ deficits, and banks swap reserves for bonds at auctions.This slide comes from my Monetary Mechanics course, in which I cover all the plumbing topics and variations you can ever imagine – take a look here if interested:So the private sector will receive a smaller injection of wealth from the US government going forward.Money creation will still happen, but at a reduced pace – but how should we think about the TGA rebuild?When the government wants to rebuild its Treasury General Account, it issues bonds but not for the purpose of ‘’financing’’ money creation – rather simply to rebuild its coffers at the Fed (TGA).As you can see from the T-Accounts at page 2, a TGA rebuild ends up with a reduction in bank reserves (steps 2 and 3) and no creation of money for the private sector.TGA rebuilds are not uncommon, but as we sit at $421 billion now and the Treasury targets $850 billion by the end of September, the $400bn+ increase in 8 weeks would be one of the most aggressive TGA rebuilds over the last 10 years:Bank reserves are currently sitting at $3.3 trillion, and given the ongoing QT and large TGA rebuild they could drop below $3 trillion soon. That would be the equivalent of less than 10% of nominal GDP:The last time we experimented with bank reserves below 10% of nominal GDP was in 2018-2019, and this eventually led to pressures in the repo market in September 2019.This excellent speech from Waller encapsulates how the Fed thinks about an adequate level of reserves.A scarce level of bank reserves means US banks would be more reticent to engage in the repo market (lend reserves against Treasury collateral) and more conservative in their risk-taking.As Waller stated in his speech: ‘’I think of ample reserves as the threshold below which banks would need to scramble to find safe, liquid funding, something that would drive up the federal funds rate and money market interest rates across the economy.’’Also, the Fed can’t really do much to slow down the bank reserves destruction from the TGA rebuild.Quantitative Tightening is running at $40bn/month, but $35 billion of QT is linked to mortgage-backed securities (MBS) which the Fed wants to get rid off from its balance sheet.And the Reverse Repo (RRP) facility is only at $80 billion, so there is little left to drain there as an offset to the TGA rebuild.If the Treasury really goes for a such a fast TGA rebuild alongside with the reduced fiscal impulse coming from tariffs, the US economy could face a soft patch right when bank reserves fall towards scarce levels leaving banks more reticent to provide repo funding and to oil the leveraged financial system.This potential plumbing issue alongside the net fiscal drag leaves me defensive on US economic growth prospects for the next 2-3 months at least.This was it for today. Be nimble, and remain hungry for macro.I This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit themacrocompass.substack.com

Policymaking Protest Assets (PPAs)

Amidst all the noise, markets haven’t had time to digest 5 key macro news:1) Elon Musk announces formation of ‘’America Party’’2) Speaker Mike Johnson: "We're gonna have a second reconciliation package in the fall, and a third in the spring of next year..."3) President Trump: ‘’ “Stock markets are now at all-time high -- we’re going to maintain it, believe me.”4) Bessent: We could appoint new Fed chair in January, nominating in October5) OMB Director Vought sends official letter to Powell saying ''Chairman Jerome Powell has grossly mismanaged the Fed''Musk’s America Party might as well cost the Republicans both the Senate and House in the 2026 mid-terms. That’s a big political risk for Trump.The response from the Trump administration is very clear - run the economy hot. More fiscal stimulus with reconciliation bills on the table again, and dovish pressure on the Fed.The interference with the Fed independence is increasing by the day, with clear attempts to find ''cause'' to fire Powell (e.g. ''gross misconduct'' mentioned by Vought).If you run the economy hot with inflation already above target and force a dovish reaction function at the Fed, our asset allocation model moves towards the ''Everything Rally'' Quadrant:Historically, the best asset mix for this scenario is to get rid of USDs and underweight long-end bonds and buy:1) Assets denominated in USD that produce inflation-proof cash flows;2) PPAs: Policymaking Protest AssetsWhy do these assets perform well in such a macro environment?Trump's plan with tariffs, fiscal and lower front-end real rates means that real growth remains ok as the tariff passthrough hits consumer spending, but rounds of fiscal stimulus preserve real purchasing power for consumer and capex for companies. It holds fine.Nominal growth is instead more robust in the 4-5% area as inflation remains sticky due to tariffs and fiscal. And you make sure that real yields remain compressed.Basically: you run it hot.In such an environment, specific stock markets composed of companies with strong pricing power (e.g. tech) fare very well as it happened in 2003-2006 and 2013-2019 ''Run It Hot'' experiments. But the two prior experiments were run with inflation at or below target, no tariffs, no attacks on the Fed independence, and no hostile policymaking against the rest of the world.Today, I believe a mix of such investments and PPAs (Policymaking Protest Assets) would work better.PPAs are assets denominated in USD that represent a release valve against unorthodox policy mix such as forcing real rates too low vis-à-vis the level of nominal GDP, manipulating long-end yields via reducing issuance or encouraging banks to buy (SLR reform), or incentivizing foreign countries to diversify away from USD investments.Gold and metals in general are the longest-standing PPAs, and needless to say Bitcoin is also a valid contender for PPA properties:The questions we should all be asking ourselves are:A) How long the USD am I in my portfolio? (Probably too much)B) Do I have enough assets producing inflation-proof cash flows? (Probably not)C) Do I have enough PPAs in my portfolio? Gold, metals, Bitcoin? (Probably not)If you enjoyed this piece, please share it with a friend you know will enjoy it too.For questions/remarks/grandma pizza recipes, feel free to drop me an email at [email protected] humble in markets,Alf This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit themacrocompass.substack.com

Null Komma Null

Hi everyone - this is Alf.I hope you're having a great day.Alongside with running my hedge fund, I work as a consultant and external advisor for some of the largest pension funds, asset managers, banks and funds in the world.Arrangements are flexible: from access to my institutional research + daily access to me all the way to monthly or quarterly calls and sitting through your investment committees.If you think I could add value to your firm, simply reach out at:[email protected] state your name, company, and how you think I could help.And now, to today's macro research piece.Let’s start this macro piece with a little game.Below you find two tables representing 3 consecutive prints of core CPI in the US including its subcomponents: core goods and core services (with a separate mention for ‘’supercore’’ CPI).Without using Bloomberg or Google, are you able to tell which 3-month core CPI streak belongs to the pre-pandemic period and which one to today?I wasn’t, and some of the hedge fund PMs I asked the same question ended up making a mistake.In both cases, core CPI MoM prints were averaging 0.15-0.20 which is broadly in line with the annual 2% inflation target and the subcomponents painted a picture of 0% goods inflation with core and super-core responsible for the quite muted inflationary pressures.The answer: section 2 covers the Jun-Aug 2019 period, and section 1 shows Core CPI for Mar-May 2025.I think we should take some time to reflect on this.In early 2019, Powell pivoted dovish with a clear speech highlighting the tightening cycle was over and the Fed was all about accommodating financial conditions.Core inflation averaged 0.2% MoM in summer (higher than today), unemployment rate was 3.7% (lower than today, and stable), and the Fed moved on to cut rates from 2.25% to 1.50% in Q3 2019.Fast forward to today: the last 3 core inflation prints averaged 0.14% MoM with weaker services inflation, unemployment rate is steadily climbing up at 4.24%, and Fed Funds sit 200 bps above summer 2019.The Fed might soon capitulate dovish.Also, amidst this tariff noise it’s helpful to take a step back and remember core goods only represent ~20% of the core CPI basket.The real action lies in services and housing (dis)inflation.The guys at WisdomTree developed a real-time core inflation metric that uses actual housing inflation rather than the lagging shelter CPI metric:Core CPI using real-time shelter inflation (blue) has been around 2% for 18 months already, but the lagging nature of shelter CPI (grey) pushed official core CPI higher limiting the ability for the Fed to cut.The lagged disinflation in housing seems set to continue, which means the official core CPI measure might keep declining based on official shelter inflation dropping (it’s 35-40% of the core CPI basket: it matters).Notice how using real-time shelter inflation works both ways.The red circle highlights the mid-2021 period when the housing market was ultra hot but shelter inflation didn’t yet show up in the official core CPI – which tricked the Fed into mistakenly delaying the hiking cycle.The opposite has happened in 2024, but the last 3 core CPI prints are now decisively dovish.It’s time to follow the Fed very closely to grasp when the dovish turn might come.The title of this piece is ‘’null komma null’’, a German expression which means 0.0 and we can say the excess inflation today compared to pre-pandemic periods is actually null komma null.But there is another ‘’null komma null’’ which is crucial for markets and asset allocation.A close friend, mentor and hedge fund PM recently had a chat with a German pension fund manager and asked him how much additional USD hedging they have done given the correlation break between EURUSD and risk assets.‘’Null komma null’’. Nothing, no additional hedging has been done.Basically, pension funds and insurance companies remain very long (and hurting) the US Dollar:The reason is very simple: FX hedging costs are still high, and pension funds/insurance companies have return targets to meet.Picture this: the standard return requirement for a pension fund is 6.5/7.0%, and if you are in Switzerland or Japan hedging your USDCHF and USDJPY exposure for the next 12 month costs 3.5-4.0%.That’s quite a hefty negative carry to pay, and this deters pension funds managers from hedging.But.In a scenario where:* The Fed turns dovish and starts delivering cuts* USD hedging costs start to drop* The USD depreciates further, reminding foreign pension funds of their losing long USD positionWe could see a fast acceleration in USD hedging demand from foreign whales around the world.Such hedging activity would compound USD weakness very rapidly.If such an outcome unravels, the market implications are pretty straightforward.Short the denominator, long the numerator.The US Dollar remains the denominator of most financial assets out there, and the combo of a dovish Fed turn + Trump policies + hedging activity would definitely ‘’wea

On The US Downgrade

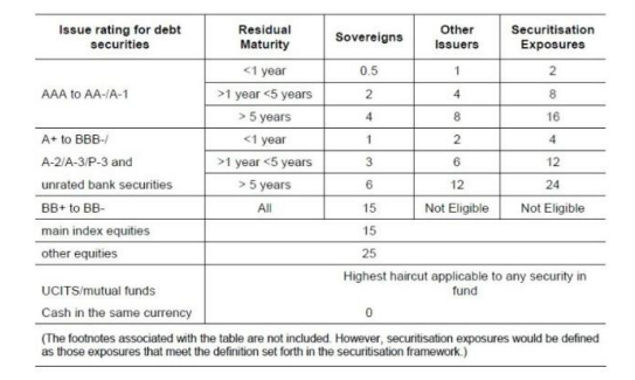

Hi everyone - this is Alf.I hope you're having a great day.On Friday, the credit agency Moody’s downgraded the US rating by one notch to Aa1 (equivalent to AA+).By now, you’ve probably read tens of opinion pieces arguing this is the beginning of the end, and that there will be dire consequences for the US Treasury market.In this piece, you’re going to read a more sober and data-driven approach to this downgrade.The first thing to understand is why Moody’s downgraded the US: ‘’ Successive U.S. administrations and Congress have failed to agree on measures to reverse the trend of large annual fiscal deficits and growing interest cost’’.The mainstream take here is that this makes sense because the US will never be able to repay its debt and because interest costs have now exceeded $1 trillion per year.Once you understand the monetary system, both these assertions don’t make any sense:Any government doing deficit spending and issuing bonds in its own currency (like the US) is not walking into an abyss of doom – it’s just choosing to stimulate the economy by printing money for the private sector.It doesn’t have to repay anything – if it tries that via budget surpluses it will cause the opposite effect and end up hurting the private sector (via higher taxes).The process of fiscal deficits creating money for the private sector is explained in the T-Account chart.Step 1 is the government blowing a hole in its balance sheet to print money for the private sector (aka deficits), which adds net worth for households and corporates which see their net bank deposits increase. These deposits end up at banks, which in turn also see their assets (reserves) increase.Banks will then swap these reserves for bonds at auctions where the US governments funds its deficits via issuing bonds and primary dealers (banks) plus foreign investors show up to buy bonds – step 2.Ok fine, ‘’US debt levels are too high now’’ is a groundless worry touted by rating agencies and mainstream commentators but surely paying $1+ trillion in interest costs must be a scary proposition?Not really: for every $ the US pays for interest on debt, there is an investor making $ on risk-free interest rates she is collecting by owning Treasury bonds.Repeating this concept is useful to demystify the monetary system: yes, government debt and US interest payments are rising but it’s not like the US needs to ‘’choose’’ between spending on interest and spending money for healthcare – the government balance sheet doesn’t work like ours.The real limitation to uncontrolled deficit spending is inflation and scarcity of resources (2021-2022 prime example) and not some budget constraints typical of a household.Ok, but how does the Fitch downgrade affect investors and market participants?The key point is that US Treasuries are now rated AA+ instead of AAA.US Treasuries are the most widely used form of collateral in the world due to their high rating, liquidity, deep repo market and solid democratic foundations/rule of law.Does the downgrade affect that?Commercial banks are huge buyers of Treasuries: they use them as regulatory liquid assets (HQLA), as collateral and also sometimes as an asset to hedge interest rate risk on their liabilities.The Basel regulatory framework introduced 10 years ago has 0% capital requirements for government bonds rated between AAA and AA- for its standardized approach: the downgrade to AA+ wouldn’t make any difference. Most banks actually choose an internal-rating based (IRB) approach based on internal models and in that case most jurisdictions apply an exception for any investment-grade rated domestic government bond which automatically assigns them a 0% risk weight.Bottom line: for banks this downgrade makes no difference at all.Treasuries are also widely used as collateral in repo transactions: for instance, pension funds and insurance companies lend their unsecured cash parked at a bank against collateral to upgrade the safety of their ‘’cash’’ deposits in a so-called reverse repo transaction.A secured loan with UST as collateral (e.g. reverse repo) is safer than parking cash unsecured at a bank.Does a downgrade affect the collateral status of US Treasuries?The table above shows the Basel committee recommended haircuts for repo transactions.As you can see, bonds rated between AAA and AA- fall in the same bucket (little haircut required).The Moody’s downgrade doesn’t affect the role of US Treasuries in the financial plumbing world: banks still face 0% risk-weights when buying Treasuries, and the role of US bonds as the main collateral underlying the global repo market remains intact.People will now try to compare the short-term bond market reaction to 2011, the last time when US Treasuries received a surprise and significant rating downgrade. Yet, the comparison makes no sense.Remember that 10-year government bond yields can be decomposed as:The downgrade can only directly impact the third component – term premium, which measures the compensa

How The Whales Could Dump More US Dollars

Hear, hear: the US Dollar is going down. Investors love to attach an ex-post narrative to any price action, and this time the blame was on Trump’s erratic policies, the reduced attractiveness of US assets, and ‘’China dumping’’. Two of these actually make sense (you can easily guess which ones).But there is a much bigger catalyst for the USD to sell-off more: FX hedging flows from proper ‘’whales’’. These whales control $30 trillion (!) in USD-denominated assets, of which 13 trillion in equities and the remaining portion in fixed income instruments. You may know these whales by their common names: GPIF, Norges Fund, CPPIB, APG, SuperAnnuation… Foreign pension funds, insurance companies and asset managers are the true whales that could dump more US Dollars in an attempt to correct their sizeable and secular ‘’under-hedging’’ of USD risk:In this article I will try to explain why these FX hedging flows (sell USD) could be triggered, quantify how big these flows could be, and assess which countries and currencies could represent the bulk of it. The analytical process requires us to identify how big their USD asset pool is (in % of their domestic economy) and how much under-hedged they are. But first – why do foreign whales actually ‘’under-hedge’’ their USD risk exposure?Imagine you are the CPPIB – Canada’s biggest pension fund with $500bn+ in AuM.You have to generate a consistent return of ~6-7% to be able to service your liabilities (future pensions), which means you’ll invest in a portfolio of stocks, bonds, real estate and alternatives. Your liabilities are in CAD (as you’ll pay pensions to Canadians) but your assets can’t only be CAD-denominated because to satisfy your investment needs you’ll need to look into the US stock markets, $- denominated hedge funds, Treasuries etc. But by investing in USD-denominated assets, you are also implicitly getting exposure to USDCAD risk. So – how much USD risk should you hedge? Or namely, how much USDCAD should you sell as a hedge? The study above from Schroeders details the industry-standard approach: the top chart looks at the correlation between USDxxx (e.g. USDCAD) and your investment asset class (e.g. equities). Recently, the USD has ‘’always’’ rallied when stocks sold-off as the world scrambled towards the safety of US assets backed by sound policymaking (= USD smile), and therefore being ‘’under-hedged’’ was great. On top of it, given a currency like CAD (table below) is commodity/risk-on cyclical, during equity sell-offs having an active ‘’long’’ USDCAD exposure through under-hedging worked even better – and so the suggested USDCAD FX hedge ratio for a 60/40 portfolio is 40%.But what happens when the USD does not rally (!) during risk-off environments, exactly as we are witnessing recently?In that case, being under-hedged (= actively long USD) becomes painful as it compounds negatively alongside equities (and perhaps also bonds) losing value.And that’s when these foreign whales would be forced to hedge, and kickstart a substantial USD firesale process.Let’s dig into the data and find out:A) How big these USD selling flows could beB) Which currencies would be involved the most and whyThe full macro research piece is available to the TMC institutional tier subscribers - a subscription costs several thousands of dollars per year.But you don’t have to pay that - if you act now.As we are getting a large influx of institutional demand for The Macro Compass research, we might be soon closing to subscriptions at retail-friendly prices.This is why today I am telling you: go for it today.The first 20 Substack TMC readers who will use the code USD20 for our All-Round tier will get 20% OFF the (already retail-friendly) subscription price.You’ll end up paying only EUR 999/year.That’s only ~19 EUR/week to read my institutional-grade research every week.The offer is valid only for TODAY!Use the link below. Be amongst the 20 who get in: This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit themacrocompass.substack.com

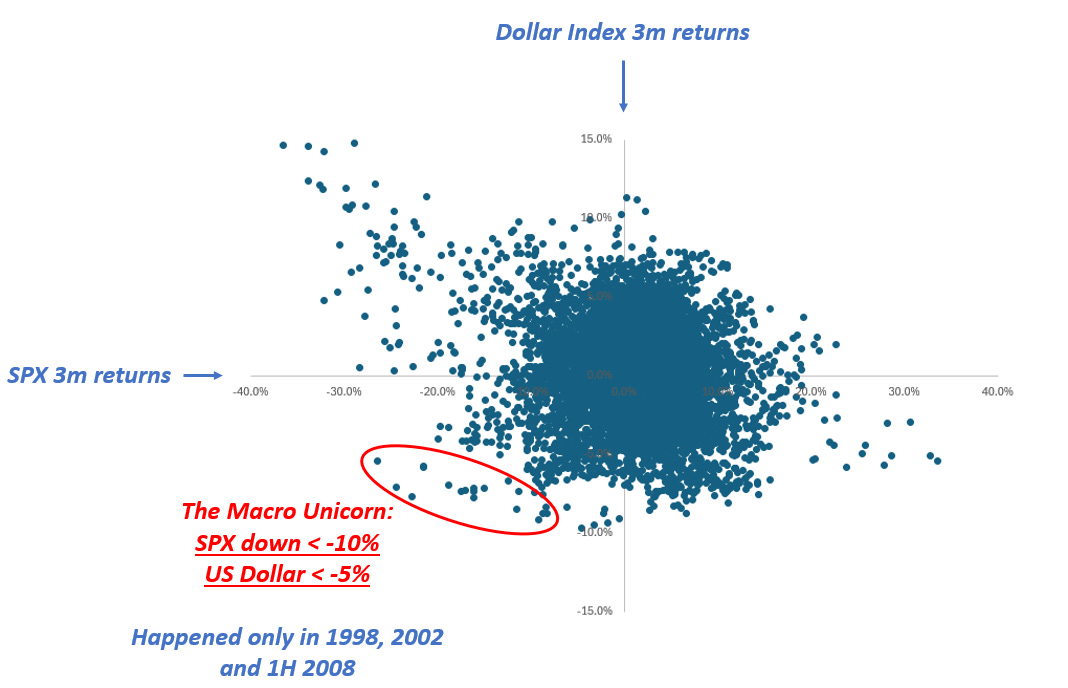

The Macro Unicorn

Hi everyone - this is Alf. I hope you're having a great day.‘’There are decades where nothing happens; and there are weeks where decades happen’’ – Vladimir Lenin.Markets were sleepwalking into April 2nd before we had a decent sell-off in US stock markets on Friday.But the size of the YTD sell-off (a mere 5%) masks a very interesting pattern happening below the surface.For the first time since the first half of 2008, we are observing a rare macro pattern – almost a unicorn.The S&P 500 and the US Dollar are going down at the same time:The chart at page 1 shows the 3-month rolling returns for the US Dollar Index (DXY) and the S&P 500.Historically, large SPX drawdown (left part of the scatter) tend to see the USD rallying heavily: the most convex USD appreciation (upper side of scatter) tends to coincide with bad equity drawdowns.This also implies that the upper-left quadrant (SPX down a lot, USD up a lot) experiences the most elongated tail of all the quadrants.The ‘’Macro Unicorn’’ bottom-left quadrant with SPX drawdowns happening alongside a weak USD is not very populated. It’s crucial to remember the last Macro Unicorn dot goes back to July 2008.Why was it so hard for the USD to weaken while the S&P 500 was going down?This is because of three reasons:1) After 2008, the Eurodollar system blew up in size and never looked back;2) The US aggressively swallowed global trade surpluses, and in exchange became the epicenter of all global financial flows into Treasuries and US stock markets;3) Policymakers applied growth-friendly disinflationary policies and politicians postured towards defending Pax Americana on the geopolitical frontWith such a combination of factors, the USD tends to appreciate during risk-off events.A portion of the 12+ trillion dollars of USD debt issued by foreign entities has to be refinanced in any given year, and a risk-off environment which threatens to slow down global trade means all foreign entities rush to buy USDs to service their debt.Foreign investors buy Treasuries because the Fed has your back and it will cut rates if financial conditions materially worsen – cross-border buying of US Treasuries strengthens the USD as money flows in the US.The same foreign investors are reluctant to wind down their US equity exposures because Fed cuts will ultimately restore confidence.Net-net, the USD goes up in risk-off events.The only periods when the USD weakened alongside the SPX were 1998, 2002 and H1 2008.These are all periods where US bubbles ended up deflating rapidly: think of the Dot Com bubble burst in 2001 or the US housing market crash of H1 2008 – before it turned into a global financial crisis.These episodes all have one thing in common: a US idiosyncratic crisis.And today, US policymakers seem to be doing all they can to generate one.On the macro front, the US administration is injecting a large amount of uncertainty.The ‘’no-visibility’’ approach from Trump on tariffs brings big unpredictability – and it’s also nearly impossible for US companies to plan capital expenditures and hiring given there is no visibility on tariffs.To that business uncertainty, you need to sum up the leaked White House memo to the Washington Post (here) which aligns with the recent Musk interview highlighting a 25-35% cut to the federal workforce to achieve budget savings close to $1 trillion/year by the end of May.Former Linkedin Chief Economist Guy Berger looks at a variety of high-frequency leading job market indicators, and I respect him as a non-biased non-alarmist economist.He just produced the chart you see below:Quoting him: ‘’The diffusion index of future headcount plans is now worse than it was immediately prior to the election. Additionally, and concerningly, that pessimism about the future is also affecting the present: the diffusion index of recent employment actions is trailing a year earlier by more than pre-election.’’And this is before the Trump administration starts slashing ~800k federal employees.To add to the potential ‘’Macro Unicorn’’ move which stems from a US idiosyncratic crisis, we are witnessing the very first signs of the unwind of the gigantic long US equity position held by foreign investors.As shown by my friend Brent Donnelly, it is very rare to experience a month when the DAX is up while the SPX down – and we just experienced it:If you take a step back, you realize that foreign investors have accumulated a gigantic amount of US securities since 2010. Trade surpluses came with a USD surplus for countries like Germany or Norway, which then recycled these excess USDs back into US Treasuries and US stock markets.Canadian and Swiss investors own US securities to the tune of 100%+ of their GDP:What if some of these foreign whales decide to reduce their exposure to US assets?It would make sense given the new US geopolitical stance, the non-supportive policy mix (non-proactive Fed and tighter fiscal stance), business uncertainty from tariffs and still elevated valuations.And wha

Here Are My Top Macro Ideas

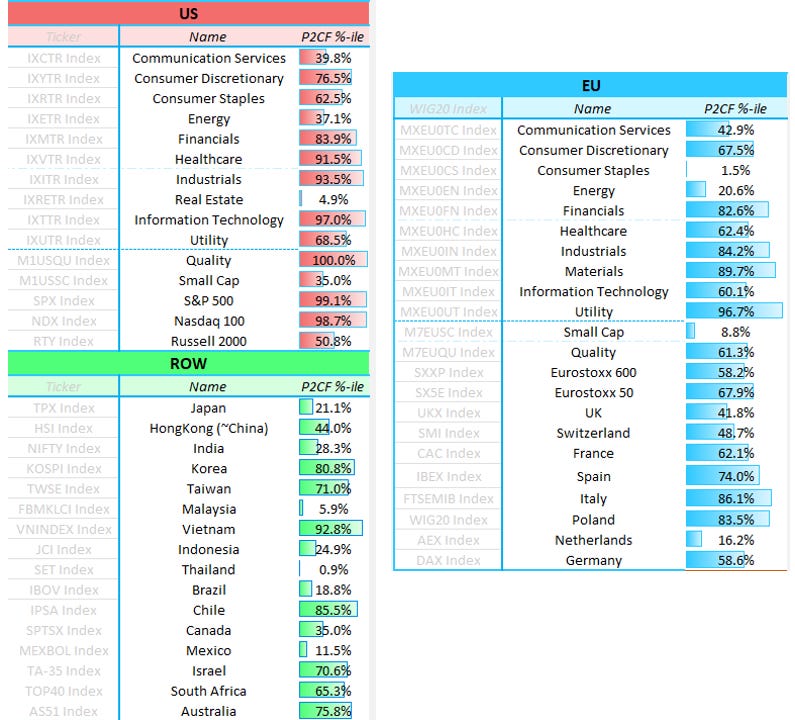

Hi everybody, Alf here - welcome back to The Macro Compass!Before we go into today’s piece, a short announcement.I advise several institutional investors on a bespoke basis.Clients include Canadian pension funds, one of the biggest tech companies around, and top 3 multimanager hedge funds in the world.Services go from sitting on the investment committee as an independent advisor, to constructing specific macro portfolios/hedging programs and consulting on a day-to-day basis (i.e. act as their independent macro analyst).Are you are interested in my macro advisory services?Please shoot an email with your request at: [email protected] warning: it’s not cheap, and it’s only for institutional investors.Now, to the piece.The first 5 weeks of the year have seen international equities outperforming the S&P 500: European and Chinese stocks have rallied harder than US stock indexes, and certain emerging markets like Chile or Poland are doing even better. My main thesis for the first half of the year remains to be positioned with an ‘’International Risk Parity’’ portfolio: long US bonds, and long stocks around the world.Let’s take a look at why.The chart above shows that the US growth exceptionalism might be over. The Aggregate Income Growth series is a great proxy for nominal growth in real time: it includes private sector job creation, workweek hours, and wage growth – effectively reflecting the growth rate of nominal income US workers are bringing home. Today, it sits at 4.5% which is exactly the average level it recorded in 2014-2019.These are the Goldilocks growth conditions and controlled inflation that international stocks enjoy.Let’s now perform a data-driven analysis of what asset classes perform best during this prevailing macro conditions, and specifically when:* Core inflation is in the 1.75-2.25% range;* Real growth is in the ~1.50-2.50% range.Here is what we found:On a risk-adjusted basis, bonds do well - especially the long-end.Stocks perform well too, with international stocks performing slightly better than US stocks: in our sample, European stocks pop up very often with CEE countries (higher beta like Romania or Hungary) leading the table.To do well, international stocks need a combination of: * Goldilocks growth conditions (no US exceptionalism); * (On the way to be) controlled inflation and predictable Central Banks; * Reasonable valuations and a new narrative replacing the existing stale one.Which brings us to the other required conditions: friendly developments in inflation coupled with a reasonable Central Bank, cheap valuations and a new narrative prevailing. What are the best countries to look at today? Let’s have a quick look at valuations:The table above shows the forward P/E ratio for various international equity markets, and the most right column shows the 10-year percentile of valuations. Broader European equities are still reasonably valued (Stoxx 600 more than Stoxx 50 which tends to give more focus to large cap German and French companies), but the standout country remains Poland. Outside Europe, several countries in Asia and LatAm show cheap valuations.Price-to-earnings ratios alone are not enough as a metric for valuations, and to broaden up the valuation assessment I like to look at Free Cash Flow Yield too.FCF yield is the ratio between free cash flows and enterprise value, and you can think of it a measure of the amount of net cash genetated by the company and literally available to stock investors divided by the enterprise value.The table below shows the 10-year percentile of FCF yield for different US and EU sectors, and different stock indexes around the world - the lowest the percentile, the cheaper the valuation:If you consider valuations, policymaking and narratives my shortlist for international equity markets includes:* Developed markets: Europe, Japan, and Canada* Emerging markets: China and MexicoEurope, Canada and Mexico were ‘‘priced to die’’ under the tariff threat, but as time goes by without much being done there investors are slowly realizing that inflation is under control and Central Banks are acting dovish. That supports stock markets.In Japan, valuations are still broadly attractive because investors are growing nervous on how hawkish the BoJ will be - yet nominal growth is doing great (~5%+) and Ueda already verbally intervened to put a cap on bond yields. Strong nominal growth and a cap on excessive tightening will benefit Japanese stocks.Despite the big rally, Chinese stocks are still reasonably priced - the PBOC remains ready to ease, some fiscal spending is happening, and investors are largely underallocated.In short: our analysis suggests that an ‘‘International Risk Parity’’ portfolio built with long US bonds and long international equity markets will perform well in H1 2025.Thanks for reading!If you enjoyed this piece, please share it with a friend:Before you go, don’t forget this.I advise several institutional investors on a bespoke basis.Cli

Bond Market Rally Next?

Hi everyone, Alf here - welcome back to The Macro Compass!And now, to the piece.Our main macro thesis for the first half of 2025 is that another disinflationary wave will hit the US.We expect core PCE to annualize at or below 2% in H1 2025.Our Leading Inflation Indicator suggests we might be due for one last wave of disinflation in the first half of 2025:To add some substance, this Leading Inflation Indicator is built using the 7 most statistically significant forward looking indicators for core US inflation.The most recent dip is mostly attributable to leading indicators of shelter inflation, which represents 30%+ of the core US inflation baskets.As you know, official shelter inflation tends to incorporate on-the-ground rent growth with a delay due to its methodology and series like the Zillow Rent Index have been used to predict where shelter inflation will go.The CoreLogic single family rent index is one of the best predictor of shelter inflation, and it just printed at the lowest level in 14 years:Some weakness in the housing market is starting to emerge - as evidenced by other leading indicators as well.One of the main reasons why the housing market held up so well despite high mortgage rates was the gigantic backlog to work through.During the pandemic, the demand for housing was super hot but supply bottlenecks and labor shortages lengthened the housing construction cycle - and this led to large backlogs which kept the housing market afloat.Big US homebuilders like D.R. Horton are now reporting their backlogs have returned to 2019 levels, so this tailwind seems exhausted:Additionally, yesterday's JOLTS report shows that the job openings for the construction sector are shrinking fast (see chart below).The construction sector is key to the US business cycle, and cyclical weakening there has always been an early signal of a broader softening in US growth conditions.Just to be clear: construction workers aren't getting laid off yet.But it seems that the conditions are in place for a slowdown in the housing sector, which also leads to disinflation through the rent of shelter component:Incoming data on inflation, growth and the housing market suggest a disinflationary slowdown in growth could be ahead of us. In that case, the Fed could quickly switch to a quarterly pace of cuts and reassert the Fed Put. This ‘’proactive risk management’’ dovish stance would ease financial conditions = stocks and bonds rally:Looking at the relative valuations across stocks and bond markets, the best risk/reward lies in fixed income.At the moment, this is what the market is pricing the Fed to do over the next 2 years:The Fed is priced to be on hold in March, deliver maybe 2 cuts in total this year, and pretty much stop there.The terminal rate is priced around 3.90% - and that’s where the Fed cutting cycle stops.Given the odds of Fed hikes are relatively small as long as Powell remains Fed Chair until May 2026, bonds offer an interesting risk/reward if my disinflationary thesis proves correct.This was it for today, thanks for reading.If you enjoyed the piece, please share it with a friend: This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit themacrocompass.substack.com

How To Prepare For Tariff Day

Next week will be crucial for markets as Trump is set to announce (or disappointingly not announce) tariffs.In this piece I will highlight the rationale behind my base case scenario and its impact on markets.Before we do that, I want to share something with you.I am offering a FREE trial to my institutional macro research service!The service includes:* Multiple macro research pieces per week;* Timely coverage of important events and market implications;* Direct access to meIf you are a HNW private investor, a family office or an institutional investor feel free to request a free trial using the link below:FREE Trial to Alf's Institutional Macro ResearchAnd now, back to the article.1. Recent economic data provides Trump with cover to go big on tariffsThe biggest risk Trump runs with tariffs is a bond market insurrection: if investors perceive inflation as too high, tariffs can generate an injection of risk premium that launches bond yields to the moon.In turn this would tighten financial conditions, slow down the economy, hamper Trump’s plans to reduce borrowing costs for the US, and just make him quite unpopular (people hate inflation spikes).Luckily for him, the recently released inflation report suggests core PCE is trending at 2.3% - not bad:Additionally, the latest job market report was encouraging and the control group of retail sales is running at 5.4% - around 2018 levels, when the pre-pandemic economy was considered strong. The economic momentum and a 2.3% trend in core PCE inflation provide Trump cover to go big on tariffs.2. To increase his negotiating power, Trump can target vulnerable economiesAs the Fed hiked rates, all other Central Banks around the world merely followed the same strategy. The big issue here is that not all economies were equipped to handle such an abrupt increase in rates.After the GFC, the US economy has deleveraged its private sector – private debt to GDP is down in the US. The US private sector also borrows mostly on fixed rate for long tenors (think about 30-year mortgages). The US also issues bonds in the global reserve currency, so bond vigilantes are unlikely to go after the US.But what if another economy had high private sector debt, or upcoming refinancings, or floating rate mortgages and corporate borrowing which makes the passthrough of rate hikes fast and furious?In that case, the economy will prove quite vulnerable to a prolonged hiking cycle.The BIS just updated their private sector Debt Service Ratio (DSR) for H2 2024 – this snapshot allows us to verify in which countries households and corporates are under pressure from a prolonged hiking cycle.Red or green colors refer to how much the DSR is above or below its long-term average in that country:Notice how Canada and China are under increasing pressure.And it would make sense for Trump to go after them – negotiating with a weak counterpart is always better. But identifying vulnerable economies is not only about the Debt Service Ratio – politics also matters.For example, Germany is very unlevered as an economy: the German DNA prevents (for now) any proper deficit spending, and the private sector is also relatively conservative on how much it leverages.As a consequence, the DSR doesn’t really pick up – yet the German economy is vulnerable.Its business model of cheap energy imports and outsourcing production and manufacturing has been challenged by the pandemic, and China has made huge progress as a competitor for car exports. The German economy has taken a major hit, and people aren’t happy.New elections are planned for February, and negotiating with a country in political turmoil is always better. From a game theory perspective Trump could decide to focus on China, Canada and Germany.3. A tariff strategy to raise the most amount of money, and take the smallest amount of risksEven if Trump wants to target the most vulnerable economies, he must be careful.Let’s take a look at the countries the US imports the most from, and in which categories of imports:The car, pharma, oil and household/tech goods industries are by far the largest import sectors for the US. And Mexico, China, Canada and Germany the top 4 countries that exports the most volume to the US.If Trump’s intention is to raise the most amount of money through tariffs on the most vulnerable economies, basic logic imposes equally heavy tariffs on all these 4 countries above.But there is a risk in going huge against China from the get-go. While it’s very unlikely that Canada and Europe will protect their currencies, China could decide to do it.And if we get 25%+ tariffs on China from the get-go but the CNY doesn’t weaken, US consumers will feel it. Higher import prices on Chinese goods without an offsetting move up in USDCNY = US consumers will take the hit out of Chinese tariffs, and not China.Here, game theory would hence suggest Canada and Europe are the prime candidates for heavy tariffs.Conclusions and market implicationsGiven that:1) Soft inflation and

What To Buy For A Macro Portfolio In 2025

Good morning, this is Alf - welcome back to The Macro Compass!I wish you a fantastic year ahead: follow your passions, keep learning, and don’t drink cappuccino after 11am.In this macro piece, we will cover the biggest market mover for H1 2025: tariffs.We will also investigate what’s the most attractive asset class today.But before we start, here is a present for you to kickstart this new year.Early next week, I’ll publish my top 3 macro trade ideas for 2025.If you want to:* Read my macro research multiple times per week;* Have access to my long-term macro ETF portfolio;* Receive all my tactical trade ideas (including next week’s)You can now sign up to the premium TMC tier for 30% OFF.For the first 30 users, 30% OFF. First come, first serve.Discount Code ‘‘HNY’’. Use the link below:Now, to the piece.What if tariffs end up being non-inflationary and negative for growth?And what if Trump focuses on short-term painful policies first in H1, to then deliver tax cuts in H2?Consensus isn’t ready for this.Let’s disentangle the thought process behind the concept of ‘’disinflationary tariffs’’.This paper from the new Council of Economic Advisor (CEA) Chair Steve Miran covers it – I’ll summarize.The main idea is very simple.In his previous term, the Trump administration increased the effective tariff rate on Chinese imports by 18%.During the same time span, the US Dollar appreciated by 14% against the Chinese currency.It basically means the after-tariff price in USD to import Chinese goods was almost unchanged.As long as the USD appreciates, US consumers aren’t going to feel much inflationary pain from tariffs:Yet we also know that tariffs are negative for business sentiment, investment, and growth.Even if tariffs are phased in gradually as a negotiation tactic, the message will be clear: if you want to export your stuff in the US, you need to re-think your business model or cut your profits.Additionally, it’s well documented that a super strong US Dollar acts as a drag for earnings growth in the US:US companies generate about 60% of their revenues outside the US, and a strong USD doesn’t help there.The charts above prove that was indeed the case in 1996-2001 and 2021-2023: a relentless USD appreciation (orange line down) slowly but surely weakened earnings growth (blue) for US companies.Under the assumption that countries hit by US tariffs will accept a currency devaluation without a fight, there are reasons to believe that tariffs can be non-inflationary and negative for growth.But can we safely assume China isn’t going to push back?Why would China not try to stabilize their currency and export some inflation and pain in the US?Let’s try to think this out as if we were Chinese policymakers.We have three options:1) Accept the hit: let the CNY weaken2) Fight back: protect the CNY by selling down USD FX reserves, and hit back the US3) Play the long gameI believe China will opt for 3: play the long game. And here is what I mean.Chinese policymakers don’t face elections, but the Trump administration does – US midterms in 2026.Rather than going for the extremes (1 or 2), China could decide to apply a long-term strategy that relies on two pillars.A) Allow a steady CNY deval, and plug the hole with fiscal stimulus where neededAs China can afford to play the long-game from a political standpoint, they could opt for a middle ground between a full CNY devaluation and a strenuous defense of their currency by selling USD reserves.B) Keep using ‘’middlemen’’ to dodge tariffsWe had some fun testing this hypothesis: can we show that China used ‘’friendly neighbors’’ to re-route their goods into the US as a way to circumvent tariffs?Since the first round of Trump tariffs went live in 2018, China (and Hong Kong) now import a volume of goods in the US which is 5% lower than the pre-tariff era.But at the same time, Vietnam + Korea + Thailand + Malaysia have all increased their trade flow with the US.Coincidence?Or China trying to dodge some tariffs by re-routing their goods exports to the US through ‘’middlemen’’?Consensus is strongly positioned for tariffs to be:* A big macro event* Negative only for the rest of the world (US growth exceptionalism to continue)* Adding to inflation uncertainty in the USI think there is space for consensus to be caught offside on all the above.I could foresee a world where Trump phases in tariffs, China dodges most of them through middlemen countries, the anticipated inflation volatility doesn’t realize, but growth slows down because business investments are hit by uncertainty.Given today’s pricing, the most attractive asset class in this scenario would be bonds.Our models show that the option-implied probability for the Fed to hike (!) over the next 12 months is priced at 40%. That’s quite high, and it show the extent of hawkish pricing people pushed into the front-end of bond markets.And not only that: the curve has bear steepened, and term premium has been injected in the long end too.With Fed Funds

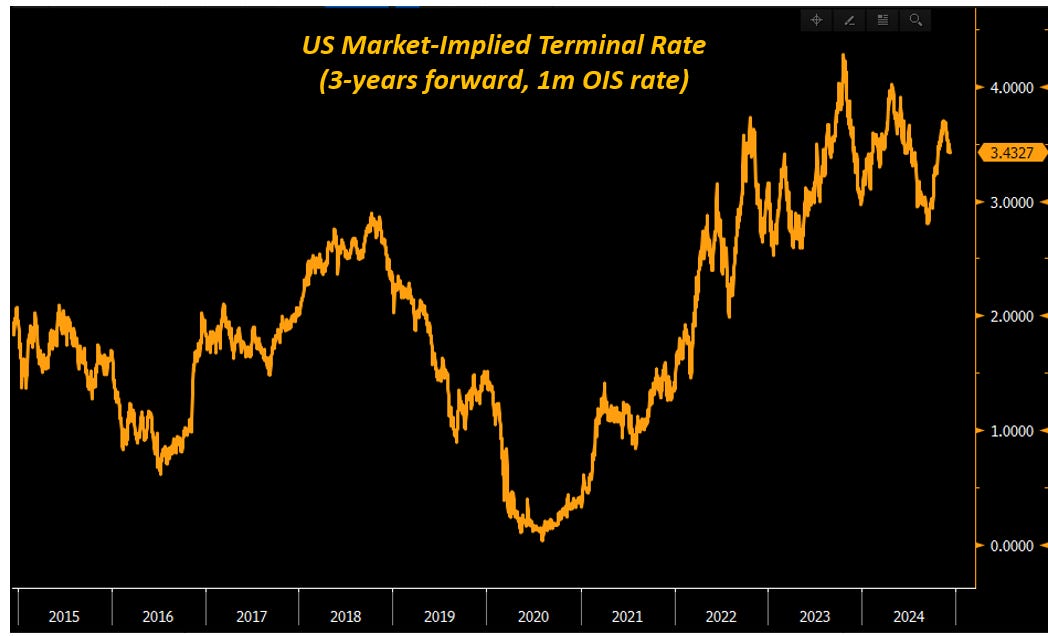

A Fresh Look At Bond Markets

Looking back at the 2015-2021 period when I traded bond markets at a large bank, it was quite boring.Rates were mostly stuck around 0% at the front-end, and to make money you had to find small dislocations and monetize them with leverage hoping volatility would remain low forever.Today, the story is different: bond markets are truly exciting.So let’s have a fresh look at them.Before we do that though - an important announcement.My macro hedge fund Palinuro Capital is going live in January.This is a dream coming true for me.Do you want to be updated about the performance and progress of my hedge fund?Fill in the form below and I will include you in the distribution list:I expect the Fed to cut rates again in December.Why?See the chart below:Even after the recent Fed cuts, today’s Fed Funds (orange) are still markedly above the underlying trend of core PCE inflation (blue).The Fed is a simple animal: their dream is to have a stable labor market with predictable inflation.And today, the main risk they see isn’t an inflation pick-up.Instead, risk management forces them to protect the US economy against a deterioration in the job market.Running a real Fed Fund rate (bottom chart, black) at +2% for several quarters on end is an exercise which was last performed in 2007.I don’t think the Fed sees major benefits in running such a tight policy.Hence, I believe they will cut rates by 25 bps in December.But here is an argument for them to feel confident the US doesn’t need a major cutting cycle in 2025:This chart looks at the US private sector (orange) and government (blue) debt to GDP since the 1990s.It’s an incredibly important chart to approach US bond markets today.The US went through two clear macro phases before today.In phase 1 (before GFC), the US government refused to lever up: government debt as a % of GDP was at or below 60% and deficits were seen as a bad thing.As the private sector didn’t receive any stimulus from government deficits and it grappled with declining demographics and productivity, it used leverage to achieve higher growth.In phase 1, the US private sector was forced to lever up aggressively.Until in 2008 excessive private debt and loose credit standards led to the Great Financial Crisis.This kickstarted phase 2 of the long US macro cycle – the post GFC period.Between 2009 and 2012 the US government printed money (read: deficits) to stabilize the US economy.This allowed the US private sector to de-leverage: private sector debt as a % of GDP fell below 150%.But this fiscal profligacy didn’t last for long: between 2014 and 2019 the US primary deficit as a % of GDP was less than -2% on average – mildly supportive for the private sector, but nothing special.So we sat there in this limbo of acceptable GDP growth, but as neither the US government nor the private sector levered up aggressively we lived through a ‘’meh’’ US growth cycle.Finally, C-19 hit and the game might have changed for good (phase 3).Since 2020, US deficits have exploded and this has allowed the US private sector to de-leverage.US private debt as a % of GDP is now the lowest since 2003 (!).So: why does this matter for bond markets?Because in a world with less private sector leverage, ceteris paribus interest rates can be a bit higher.When there are less mortgages and corporate loans to refinance vis-à-vis higher nominal wages and earnings, the equilibrium interest rates at which the economy can function should be higher.The flipside is obviously that an increasing load of government debt will have to be refinanced at higher rates.In the US case though, that’s more manageable than for other countries due to the reserve currency status.This is why the market feels quite strongly about terminal rates being well above 3% this time.As per today, markets expect Fed Funds to still be at 3.50% in 3 years from now.The most important implication for investors is this.If the Fed embraces this new narrative, we are looking at few (if any) cuts left in 2025.This is because if neutral rates are considered to be higher, the Fed doesn’t need to cut rates much more to achieve a neutral policy stance.With euphoric expectations about earnings growth, nosebleed valuations and a less friendly Fed overly bullish investors might be disappointed in early 2025.This was it for today. I hope you enjoyed this macro piece.Please share it with a friend:And also, don’t forget.Do you want to be updated about the performance and progress of my hedge fund?Fill in the form below and I will include you in the distribution list:Have a fantastic day ahead,Alf This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit themacrocompass.substack.com

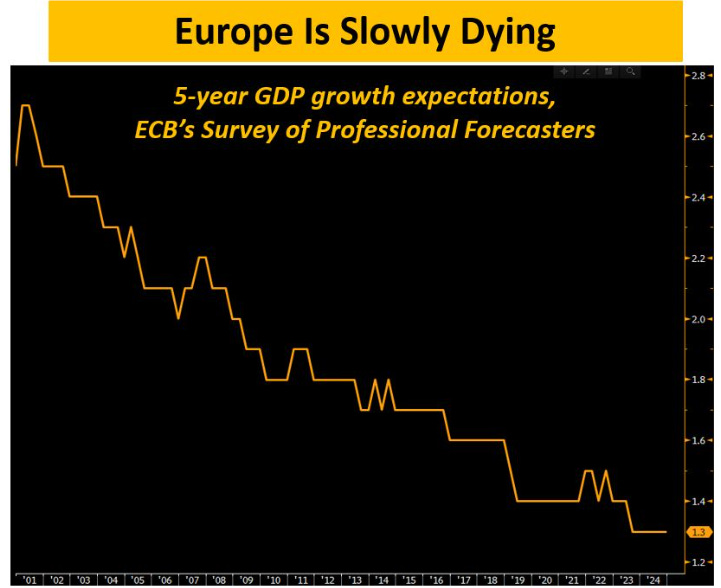

Macro Clouds On The Horizon

The key macro event of 2024 is approaching: US elections are around the corner.Next week I will release a deep research piece on US elections, which will be centered around the key questions looming large.How to trade different scenarios?What happens to markets if Trump secures a Red Sweep? And what asset classes to prefer if instead Kamala wins?This special election piece will be ONLY available to my private distribution list.Sign up for FREE here:Macro clouds remain on the horizon.Wherever you look at, you see unsustainable economic models: we are either relying on debt-fueled growth (US), trying to squeeze exhausted growth models (China), or succumbing to a slow and painful death (Europe).Today, let’s take a step back and talk about the business models that Europe and the US are pursuing.Let’s unpack them together, and understand what lies ahead and how to prepare portfolios accordingly.Europe is slowly dying.To prove my point, here is one of the most depressing chart you'll see today:The chart above shows an uncomfortable truth for Europe.ECB's Professional Forecasters now expect 5-year GDP growth in Europe to come in at only 1.3% - the lowest level ever.Prior to the Great Financial Crisis, this number used to be consistently above 2.0% in real terms.So while we are talking about the ''Roaring 20s'' for the US, and while we are watching countries like India perform particularly well we are left to answer some tough questions in Europe.Why is growth so low, and expected to remain so sluggish?1️⃣ An imperfect European infrastructure, and no improvement in sight: we run a ''union'' under one monetary policy, different fiscal policies, and without a banking or capital markets union.2️⃣ Poor productivity, and no structural reforms: while touted the whole time, European politicians are really not busy with reforms to structurally improve productivity. Over the last 20+ years, European productivity growth has been a meagre ~1% per year.The US is becoming increasingly more productive at a much faster pace:3️⃣ Bad demographics, and worsening;Low birth rates imply that Europe will see its labor force shrink by 25% (!) over the next 20-30 years:Not only that - it’s also a matter of putting people to work in the first place.In Italy, women labor force participation rate is not even at 60%.4️⃣ No appetite for true innovation, and instead an insatiable appetite for more and more regulationEurope is slowly dying.Yet markets are still in La-La Land.This week, the ECB cut interest rates once again but nominal rates remain still too high versus the underlying trend in inflation.As the chart below shows, Europe instead needs interest rates below (!) the level of inflation to have a monetary policy loose enough to stimulate at least some growth:The chart below is another way to picture this inconsistent bond market pricing.The long-run equilibrium nominal rate represents the nominal interest rate that allows an economy to operate smoothly and deliver its potential growth rate while inflation hovers around 2%.Think of it like the interest rate which ‘‘balances’’ the economy.Prior to the pandemic, the average pricing for the long-run equilibrium nominal rate in Europe was +0.5%.Today, it’s over +2.0%.What has changed in Europe so that the economy can structurally handle higher interest rates way better than before the pandemic?In my opinion: nothing.If anything, things look a bit worse now:Patient Europe is dying.Better make sure your portfolio is prepared for it.Let’s chat about the US economic model now.Here are some staggering statistics about the US economy - since mid-2020: 1) US nominal GDP has grown by ~7 trillion 2) US total debt has grown by ~8.5 trillion Debt-fueled economy, debt-fueled growth:Look at this excellent chart from E.J. Antoni. It shows how US nominal growth (blue) has increased less than the increase in federal government debt (red). If you add in private sector debt, the red bar crosses the 8 trillion mark.Should we worry about this debt-fueled growth model?Look: our monetary system is centered around debt/credit creation to sustain economic growth. There is nothing inherently bad about that, but the key is to use new debt to fund productive investments and reforms. We got worse and worse at that:As the chart above shows, for every new $ of debt we end up creating way less than a new $ of GDP growth! So: yes, the US economy has done incredibly well since 2020. But more than organic growth, this is once again debt-fueled growth.Whoever wins the US Presidential Elections, you can rest assured there will be more and more debt creation to try and fuel US economic growth.Can this model continue to thrive?I’ll cover this in next week’s flagship US election research piece.You can only access it registering at the link below.It’s FREE.Don’t miss it - register at the link below:This was it for today.I am counting on you to share the article with friends and colleagues so we can make The Macro Compass newslette

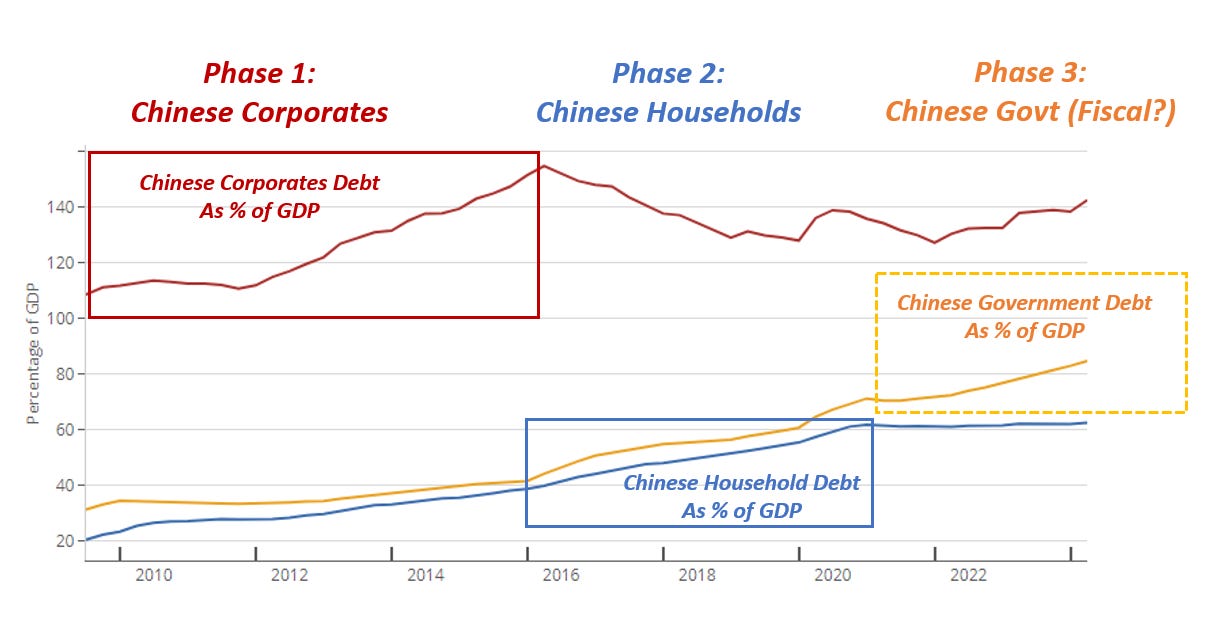

The Big Chinese Bazooka

The Chinese real estate market is de-leveraging very hard. Economists estimate Chinese households have suffered $10+ trillion of wealth losses as a result. There is now a strong urge to stop the bleeding amongst Chinese policymakers.Last week, China unleashed a ‘‘stimulus bazooka’’.But what were the measures all about?And will they be effective to fix the Chinese economy?Chinese policymakers announced the following package: A) More interest rate cuts B) The Chinese version of the ''Fed put'' C) Vague wording about fiscal stimulusInterest rate cuts and the ''backstop'' facility are propping the Chinese stock market to the moon. Yet they are very unlikely to work in a balance sheet recession. In the 90s, Japan cut rates aggressively and that wasn't the solution to the problem:Cutting rates won’t encourage households or corporates to leverage: corporates were tapped out in 2016 already, and households have just been burnt with excess debt so we shouldn’t count on them.Lowering interest rates in combination with the new ‘‘PBOC Put’’ can instead help reinstate animal spirits.Chinese authorities set up a BTFP-like facility which allows you to pledge collateral (cash, bonds etc) and get funding to go and buy Chinese stonks.Yet, this is unlikely to solve the structural malaise affecting the Chinese economy.Fiscal is the only real fix, and here is why. There have been 3 key phases of Chinese leverage: 1) Corporates (red) 2) Households (blue) 3) And now fiscal is the only solution (orange) 10 years after entering the WTO in 2001 and once the demographics dividends were exhausted, China embarked in massive leverage to sustain their growth targets. Phase 1 saw Chinese corporates (red) tap up leverage aggressively (2010-2016). Once corporates’ appetite for debt was exhausted, Xi Jinping tapped Chinese households (phase 2). This led to the creation of a massive real estate bubble which China is trying to deflate now. The only agent left to pick up the slack is the Chinese government – fiscal deficits are key here (phase 3?).So while the ''bazooka'' has been excellent at restoring market confidence, there is only one real fix for the Chinese economy here. It's a large, large fiscal stimulus package.Will China actually implement it?Reuters ran a piece discussing a $284 bn fiscal package.This would be very much unlikely to sort things out.Size matters here: consumers and corporates have been hit by a $10 trillion de-leveraging in the housing sector, and so the fiscal stimulus needs to be large and targeted to make the difference for the Chinese economy.While we keep monitoring any concrete announcement on fiscal stimulus from China, it’s worth remembering how Chinese policymakers love a ‘‘counter-cyclical’’ Bazooka:China loves to stimulate (for real) when the global economy is weak. This way, they can get the best ROI on their money creation and go buy cheap foreign asset/strengthen their trade position/gain shares in crucial markets. Until the global economy slows down further, China might not be interested in proper stimulus but rather in ''controlling the bleeding'' and get investors occasionally stopped out in their China shorts - a story we've seen happening for 18 months already.China matters for the world.China needs a large fiscal stimulus.Large. Fiscal.These are the two key words you should be focusing on.If you enjoyed this piece, feel free to share it with a friend:And remember: my macro hedge fund Palinuro Capital goes live next week!If you are a professional investor and you wish to remain updated on my fund, from now onwards you can only do that if you access my private distribution list.To remain updated on my Macro Hedge Fund, please leave your info here.This is your last chance.It only takes 2 minutes. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit themacrocompass.substack.com

China Is Imploding

The news of the week is NOT the Fed cutting 50 bps - yes sure, that’s important but there is something much more relevant going on.The Chinese economy keeps imploding from within.And we should pay attention.The Property Price Index for Chinese tier-1 cities keeps making new lows, and it’s now approaching levels last seen 8 years ago!At this point you might ask yourself: well, is it so bad if house prices drop a bit?In standard circumstances I’d tell you this is not a disaster.But for Chinese people, things are different:Chinese households hold 60%+ of their wealth in Chinese properties.This is way higher than in the US, where households only hold 23% of their wealth in properties while the majority sits in the stock market or retirement plans.Now imagine if your stock portfolio dropped back to 2016 levels.How would you feel about it?That’s how Chinese households are feeling!But why is China imploding this fast?It’s because Xi Jinping wants to engineer a new ‘‘common prosperity’’ economic model which relies less on leverage, tech bubbles, bridges in the middle of nowhere and frothy house prices and more on internal consumption.The problem is that when you deleverage a 50 trillion (!) worth real estate market inflated with absurd levels of leverage…well, that’s not an easy task to achieve.China is cutting interest rates aggressively to try and limit the slowdown: Chinese 10-year interest rates just dropped below 2% for the first time..ever?Yet cutting interest rates while the real estate market is deleveraging won’t help much.Ask Japanese people in the 1990s for reference:China keeps imploding from within and this matters for the rest of the world.For example, China is the number 1 trade partner for many countries and for specific jurisdictions it represents a very large importer for the commodities they produce.See Brazil for instance:Everybody is talking about the Fed.But the real macro mover to watch here is China.Keep it on your radar!And of course - who am I not to spend a few words on the Fed as well.This week's 50 bps cut was initially celebrated by markets: after all, if the Fed proceeds with such a sizable cut what's not to celebrate?The problem with such a simple narrative is that the Fed's monetary policy needs to be measured against the underlying growth conditions.Fed Funds at 4.75% can be:- Still loose: if the US economy is running ultra-hot- Still tight: if the US economy is rapidly weakeningIn other words: the monetary policy looseness/tightness needs to be measured taking into consideration the ongoing economic conditions.The chart above does just that, and it compares Fed Funds (orange) with the underlying trend of US nominal growth (blue).The US nominal growth proxy is built using core PCE - the Fed's official target for inflation - and the NBER gauge for US real economic growth.Why the NBER gauge and not real GDP?Because the NBER is the body that ultimately determines whether the US is in a recession, and they do so using a broad basket of 7 indicators tracking every sector of the US economy (from consumers to industrial production to the labor market).The outcome of this analysis is straightforward.There is nothing to celebrate.The Fed's policy is still dangerously tight.As you can see, it only rarely happens that Fed Funds (orange) sit close or even above US nominal growth (blue) for a prolonged period of time.And when that happens, it's never good news for the economy.The Fed needs to do more.Or it risks falling further behind the curve.And now, some big news - adding even more value for you…FOR FREE!If you enjoyed this piece, you should know I launched a YouTube channel for my weekly show The Macro Trading Floor with Brent Donnelly.Every week we discuss a ton of macro with supporting charts, trade ideas, and trading/risk management education.Click below to watch our first video which just went online: I appreciate you!Please share this post with a friend/colleague if you want to support my workEnjoy the weekend, and don’t drink cappuccino after 11am. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit themacrocompass.substack.com

This is a True Regime Change

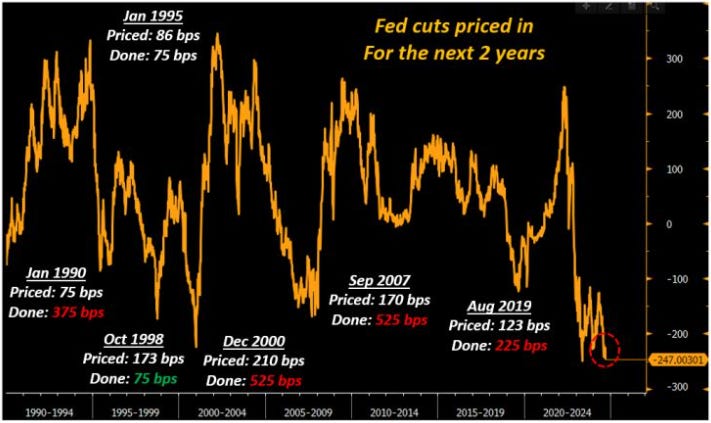

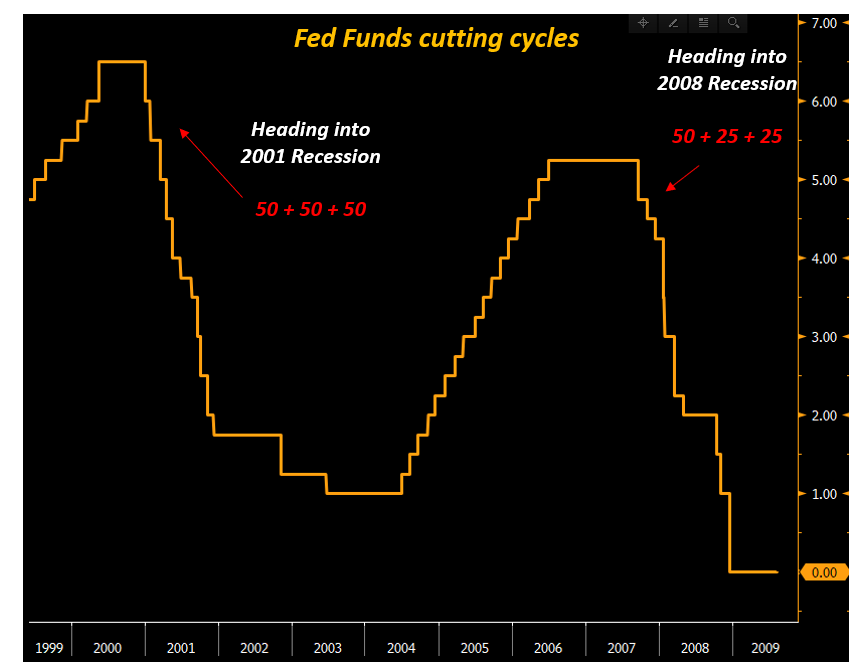

We are observing a true regime change in markets.And for macro investors, it’s incredibly important to stay vigilant and on top of our game at this stage.It all starts with this: the Fed is behind the curve, and it is playing with fire.Consider this.The recently released US job report showed the US private sector is only adding an average of 96,000 jobs per month over the last 3 months.Such a weak pace of job creation has last been seen in summer of 2007.The last CPI report also showed another friendly and disinflationary print: core CPI raised less than 0.2% on a MoM basis which is a trend in line with pre-pandemic ~2% yearly inflation trend the Fed targets.So, why is the Fed playing with fire?The chart below shows you why.Fed Funds at 5.25% while core PCE is convincingly sub-3% represent a real Fed Fund rate of 2%+.Real rates are what matter for the economy:* Investors care about their (risk-free) returns after accounting for inflation* Debtors care about their inflation-adjusted borrowing costsWith real rates now at 2%+ for quite some time, it's important to look back at past episodes and see what happened when the Fed forced such a tight policy for too long:A) In 1999-2000, the Fed kept real rates at 3%+ for a sustained period of time and a crisis unfolded in 2001;B) In 2007, the Fed kept real rates at 2%+ for a while and a crisis unfolded in 2008;C) In 2024, the Fed is keeping real rates at 2%+ and...you get it.On top of this, the Fed is also keeping policy very tight while the US job market is showing clear signs of weakness.The Fed is behind the curve, and it is playing with fire here.And when this happens, the bond market takes over.The chart above goes back to 1989 and it looks at the amount of rate cuts/hikes bond markets were pricing for the subsequent 2 years.I focused on periods when the bond market was very, very dovish and it priced in a robust amount of cuts.The big question is: what did the Fed ACTUALLY deliver?Did one make or lose money by buying bonds when markets were already super dovishly priced?Let's look at the data:1️⃣ January 1995, October 1998Cuts priced for the next 2 years: on average 130 bpsCuts delivered by the Fed: 75 bpsIf you bought bonds while markets were already at peak dovish pricing, you lost money (cuts delivered were less than priced in).2️⃣ January 1990, December 2000, September 2007, August 2019Cuts priced for the next 2 years: on average 145 bpsCuts delivered by the Fed: 412 bps (!)If you bought bonds while markets were already at peak dovish pricing, you ended up making a ton of money.The results are very interesting. As a rule of thumb, I always advocate that in macro you don’t make money by only ‘’being right’’. That’s a necessary but insufficient condition: you also need to surprise consensus, or in other words see something before the crowd does + position correctly for it + monetize when they converge to your view.Yet it seems like the bond market is quite good at sniffing when something is about to go wrong.The bond market is sending a loud message: are you listening?But it’s not only about the bond market here.It’s also about cross-asset correlations suggesting tectonic shifts are happening:We are witnessing a massive regime change in markets.Recently we experienced another large drawdown in equity markets lead by tech stocks - specifically, NVDA stock prices dropped by almost 10% in a single session.But the big news for investors is that bonds have started to exhibit one of their key features again.For the first time in a few years, bonds are acting again as a hedge against stock market drawdowns.Or in other words: after a period of positive correlation which wrecked 60/40 portfolios, the stock/bond correlation is turning negative again.This is a huge deal.The chart above shows the 6-month (120 trading days) correlation between the S&P500 and 10-year Treasury future prices.The correlation was negative for most of the last 15 years: this means investors could count on bonds acting as a diversifier during periods of equity drawdowns. But as you can see from the chart, this wasn’t always the case: for most of the ‘80s and ‘90s bonds and stocks were doing pretty much the same thing at the same time – they were positively correlated. The same happened in 2022-2023 as inflation was out of control.Hear me out now, because this is the key message you should bring home.When the stock/bond correlation changes sign, we are looking at tectonic macro shifts with huge implications for cross-asset portfolios.This is because ''bad news is good news'' doesn't work anymore.The market has switched into a regime in which:Bad news is actually bad news.Once bonds start acting as a diversifier for risky assets, it's likely we are on the verge of a massive regime change in macro and markets.Macro tectonic shifts are happening.The launch of my Macro Hedge Fund is now imminent.If you are a professional investor and you wish to remain updated on my fund, from now onwards you can on

Panic Monday! (What Now?)