The Macro Compass

131 episodes — Page 2 of 3

The De-Dollarization Fairytale

Brazilian President Lula recently asked the following questions:‘’Every night I ask myself why should every country have to be tied to the US Dollar for trade?’’‘’Why can’t we trade in our own currency?’’‘’Why can’t a BRICS Central Bank have a currency to finance trade between BRICS countries?’’Lula’s speech sparked yet another mediatic hype on the upcoming De-Dollarization.So, let’s explain how today’s USD-centric system works and why it’s been impossible to replace in 50+ years.Before we dive into it, a quick reminder: if you enjoy these educational pieces and you haven’t subscribed yet to The Macro Compass premium platform……well, what are you waiting for?Come join thousands of investors receiving unique, jargon-free macro insights and actionable investment strategy for their portfolios every week!For more information, here is the website.Now, back to it.In a globalized economic system you want to trade with as many partners as possible in a seamless way.When Brazil exports its commodities to China or Japan and the trade happens in USD, Brazil accumulates Dollars – it might also use them to buy goods or services it needs from other countries.In other words, today the US Dollar is the Global (Reserve) Currency of choice: over 80% of global FX transactions and 50%+ of global trades and payments happen in US Dollar.More importantly, in the last 30 years competitors could not alter this massive USD dominance: why?Well, it’s because being the US Dollar seems fun from the outside.But it ain’t easy.Let’s start from the asset side.When Brazil exports commodities in USD more than spends USD to import stuff from the outside, the country accumulates USD foreign exchange reserves.These USDs enter the domestic banking system, and ultimately the local Central Bank is responsible for managing this FX reserve buffer – that means keeping these US Dollars safe and liquid.In our monetary system, keeping money ‘’safe and liquid’’ means avoiding credit risk and investing in deep and liquid markets that guarantee a painless turnover if necessary (either via selling or repo-ing securities).The US Treasury market stands out as the global leader in this field: as big as 20+ trillion in size, liquid and underpinned by a deep repo ecosystem it ticks all boxes.No capital controls, democratic roots and the rule of law reinforce the case.Most importantly, an ample supply of US Treasuries (read: deficits) provide to the rest of the world what they need: a safe and liquid asset where to recycle the USD proceeds from their global trades.But so, what’s the potential alternative?Japan? Its government bond market is 60%+ absorbed by the BoJ, and there have been multiple days in a row (!) where no trade happened in the JGBs – how can you store your FX reserves in such an illiquid market?Europe? With such a fragile monetary but non-fiscal union, and the only AAA countries potentially able to provide the world with safe collateral (German Bunds) instead sticking to austerity for decades?China? Brazil? Russia? You are facing a combination of capital controls (China), lack of democracy/rule of law (Russia), corruption and frequent episodes of double-digit inflation (Brazil) – do you want to take these risks when storing your hard-earned FX reserves accumulated from selling your goods and services abroad?The truth is that US Treasuries don’t have a valid competitor as a global vehicle where to invest FX reserves.And this is also true for the other side of the coin: debt.USD-denominated foreign debt is huge, and it makes an orderly De-Dollarization not more than a fairytale.Entities sitting outside the United States have accumulated $12 trillion of USD-denominated debt: this is because to finance global businesses that sell stuff in US Dollars…well, you need US Dollar debt.I can’t stress how important it is to understand this concept: if you want to break this system and ‘’De-Dollarize’’, you need to deleverage a $12 trillion debt system.Brazil walking away from USD-denominated trades would hamper its own organic inflows of US Dollars, and Brazilian corporates would be choked under USD scarcity as they need to repay and refinance their USD debt.When you de-leverage a debt-based system, you are either bidding up the debt denominator (the USD) or you are witnessing tectonic geopolitical events (e.g. wars) where the world order is at stake.An orderly unwind of the US Dollar is a fairytale: there is no valid alternative for a smooth transition, and de-leveraging the global USD debt based system would be a very painful process.And this is why you keep hearing about the De-Dollarization, but it never happens.If you have enjoyed this piece, consider joining The Macro Compass premium platform.The best investment you can make is in your own macro education, and TMC is trusted by thousands of worldwide investors to deliver unique and actionable macro insights every week.For more information, here is the website. This is a public episode. If you would like t

5 Things Hedge Funds Are Watching

Hedge funds are often called fast or smart money because they are one step ahead of herd market thinking.I am blessed with the opportunity to have several of them as clients, and pick up their brains on what they are watching in markets and what the next big macro trade might be.In this piece, I will share with you 5 macro developments and charts hedge funds are watching.1. Are you watching the deflationary tails?!The Minneapolis Fed runs an excellent algorithm that plots the market-implied distribution for 5-year ahead expected inflation in the US (here).It uses options on inflation-linked products to determine what investors are expecting as base case, and what they are willing to pay for upside (hot inflation) or downside (disinflation) in US CPI over the next 5 years.If we compare today’s distribution (blue) versus 2 years ago (red) we notice that the median base case for investors is that US inflation will average around 2.25% over the next 5 years: quite a comfortable sight.But the devil is in the (de)tails.While 2 years ago the 10th percentile of the distribution settled at 1.56%, today is sits at 0.63% - quite close to actual deflation.The ‘’hot inflation’’ tail (90th percentile) is also a bit higher at 4.63% vs 3.76% in 2021.While the base case for inflation ahead is very benign, today investors are more worried about tails than they were in 2021.And in particular deflationary tail risks are staging a comeback.2. Bond market volatility: look under the surface…As the banking crisis was unfolding, bond market volatility literally exploded: the cost to hedge against an abrupt Fed cutting cycle skyrocketed, and bond market liquidity quickly evaporated.Lately, as we find out the world is not coming to an end anytime soon bond market volatility is quickly receding…but are we out of the woods?This chart shows the 3-month market-implied volatility in US 2y rates (orange, RHS) and 30y rates (blue, LHS).Bloomberg users can find the tickers here: USSN0C2 BGN Curncy and USSN0C30 BGN Curncy.If you don’t have Bloomberg, you can find and chart these tickers on our Volatility-Adjusted Market Dashboard (tickers: US 3m2y Swaption ATM Vol, US 3m30y Swaption ATM Vol).This chart is interesting because it shows that while front-end bond market volatility (orange) receded but remains elevated, the long-end (blue) seems to be much less uncertain about future outcomes.Why?As this hedge fund client eloquently puts it: the Fed can have a strong influence on 2y rates, but 30y rates are rather based on investors’ expectations and uncertainty about future growth and inflation.And there is not much to be uncertain about there – the Fed is on a mission to kill growth and inflation, 30y rates know it and you never fight the Fed.Which brings me to the 3 most crucial charts hedge funds are watching to find the next big macro trade, and that you should care about too.Let’s dig in…Eager to read the remaining part of this macro report?Come join The Macro Compass premium platform to get access to Alf’s full-length timely pieces, actionable investment strategy and much more!Check out which subscription tier suits you the most using the link below.For more information, here is the website. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit themacrocompass.substack.com

The Long Term Debt Cycle

Hey guys! Before we start, an important announcement: welcome to the first piece of the TMC Macro Education Series!Once a week, I will deliver some bonus educational content covering big picture macro trends, the bond market, monetary mechanics, risk management and more in a quick, 5-min read.Financial education is a key TMC principle – hence the Macro Education Series is and will always remain FREE.I hope you enjoy it!Long-term, structural economic growth is mostly driven by two factors: demographics and productivity.Both peaked in the late 80s, and we chose to fix the problem with a ton of debt.It worked until now, but we are at very late stages of the long-term debt cycle.Healthy demographics and high fertility rates facilitate a growing labor force: retirees are more than offset by new young workers, and hence the share of working-age population as % of total increases.More workers, more potential for growth.Over the next decades though, the share of working-age population will decline across many countries: for instance, the Chinese workforce is likely to shrink by 250-300 million people – a hard hit for global growth.Total factor productivity (TFP) growth measures how productive are capital and labor resources.Effective capital allocation and technological progress contribute to achieving positive productivity growth.As the marginal benefit from technological progress declines over time and capital misallocation took center stage over the last 1-2 decades, TFP growth stagnated around 1% per year – not exciting.As per the early 90s, labor force and productivity growth trends weakened materially.Potential GDP growth started declining to socially and politically unacceptable levels – so, how did we fix that?With a ton of debt.Public + private debt levels as % of GDP amongst developed economies skyrocketed from Be it mostly through government (Japan) or the private sector (China), credit creation was the ‘’easy fix’’.To be precise: cheaper and cheaper credit.Real interest rates relentlessly declined for 3 decades, allowing a system with lower structural growth offset by more and more leverage at cheaper and cheaper borrowing costs to thrive.The more unproductive debt, the lower real yields must be for the system to survive.This long-term debt cycle is at its very last innings.Fighting inflation requires higher real yields, and our over-leveraged system can’t bear that.And once you deleverage a credit-based system, it’s hard to get it back on its feet.Just ask Japan.If you have enjoyed this piece, consider joining The Macro Compass premium platform.The best investment you can make is in your own macro education, and TMC is trusted by thousands of worldwide investors to deliver unique and actionable macro insights every week.For more information, here is the website. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit themacrocompass.substack.com

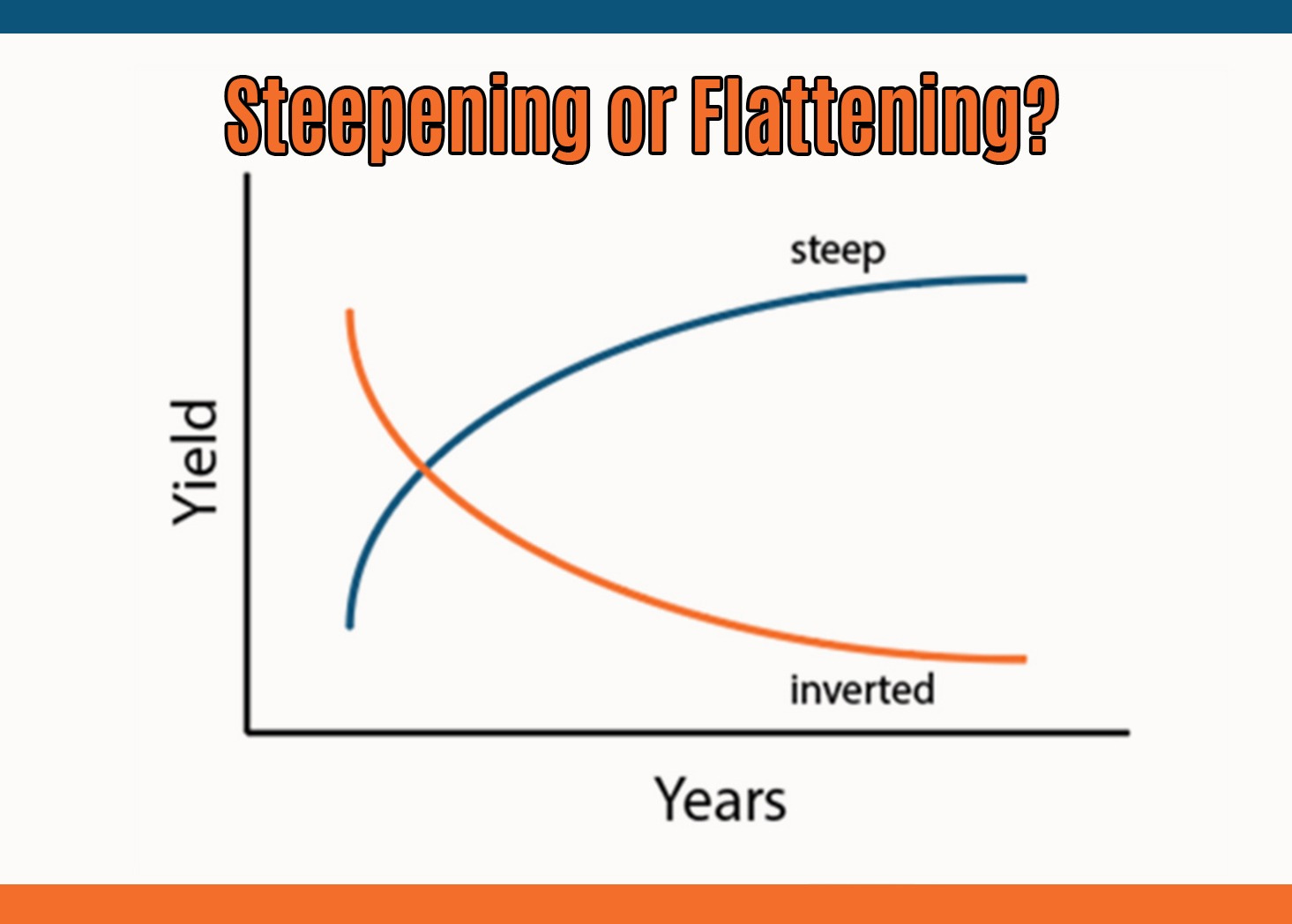

The Big Yield Curve Shift

Before we start, a quick announcement: starting this week, I’ll be kicking off The Macro Education series!I will publish short and educational pieces covering the bond market, monetary mechanics, portfolio construction, risk management and much more.It will be and it will forever remain FREE.Looking forward to share some educational macro insights with this nice community!When the yield curve flattens and eventually inverts, you worry.But it’s when a recession hits, the Fed cuts rates and the curve steepens that you become s**t scared.Yield curve dynamics represent a crucial macro variable, as they inform us on today’s borrowing conditions and on the market future expectations for growth and inflation.An inverted yield curve often leads towards a recession because it chokes real-economy agents off with tight credit conditions (high front-end yields) which are reflected in weak future growth and inflation expectations (lower long-dated yields).A steep yield curve instead signals accessible borrowing costs (low front-end yields) feeding into expectations for solid growth and inflation down the road (high long-dated yields).Rapid changes in the shape of the yield curve at different stages of the cycle are a key macro variable to understand and incorporate in your portfolio allocation process.Hence, in this piece we will:* Quickly walk you through the different yield curve regimes (i.e. bull steepening, bear flattening etc);* Analyze 50+ years of asset classes returns through these different regimes;* Assess where we stand today, and what the labor market is telling us about the macro cycle;* Conclude with our actionable investment strategy.* Bull Flattening = lower front-end yields, flatter curves.Think of 2016: Fed Funds already basically at 0% and weak global growth. Yields stay put at the front-end and could meaningfully move lower only at the long-end, hence bull-flattening the curve.* Bull Steepening = lower front-end yields, steeper curves.Late 2020, early 2021: the Fed was keeping rates pinned at 0% and stimulating via QE but the economy was flooded with fiscal stimulus and ready for reopening. The friendly borrowing conditions and the massive upcoming growth boost could mostly be reflected through higher long-end yields, while 2-year interest rates were pinned at 0% by the Fed. Bull-steepening of the curve.* Bear Flattening = higher front-end yields, flatter curves.2022 was the bear flattening year: Powell raised rates aggressively to fight inflation, but he ended up choking the economy off. This was reflected in lower future growth and inflation expectations at the long-end of the curve. Front-end rates went higher, but the curve bear-flattened.* Bear Steepening = higher front-end yields, steeper curves.Do you remember 2009? The worst of the GFC was behind us and (monetary-mechanics-illiterate) investors were afraid that QE would lead to runaway inflation and the Fed would be forced to start acting on it. Front-end yields moved a bit higher, but long-end yields took most of the hit as investors (mistakenly) bumped the inflation risk premium up = the curve bear-steepened.Rapid changes in the shape of the yield curve when growth is at turning points are a key variable to consider for a successful asset allocation process.We looked at 50+ years of cross-asset returns through different growth and yield curve regimes, and here is what we found:The implications from this table are crucial for your portfolio allocations.Let’s dig in…Eager to read the remaining part of this macro report?Come join The Macro Compass premium platform to get access to Alf’s full-length timely pieces, actionable investment strategy and much more!Check out which subscription tier suits you the most using the link below.For more information, here is the website. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit themacrocompass.substack.com

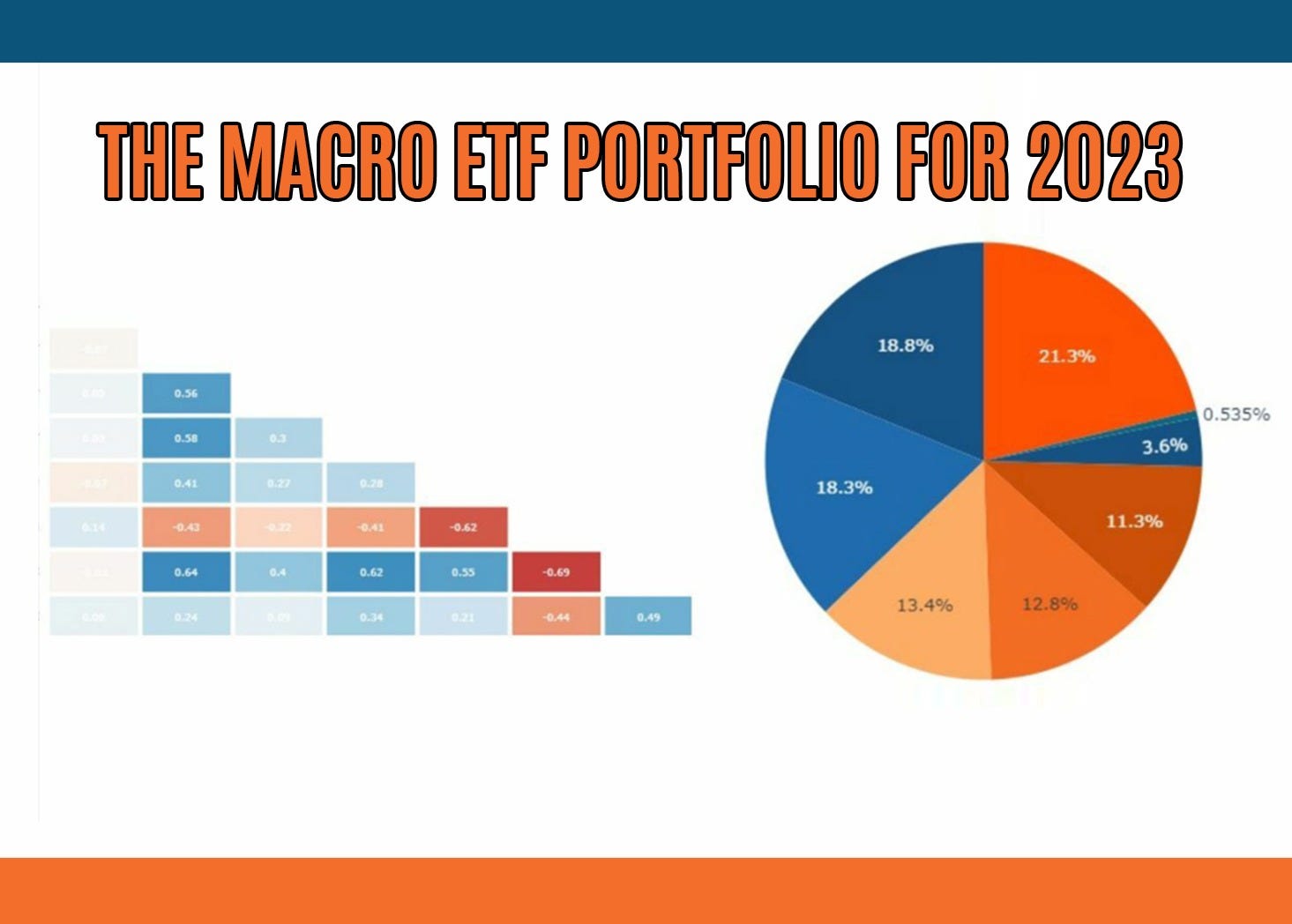

How To Invest In Q2

Soft landing, no landing at all, banking crisis leading to an immediate recession.Chinese reopening yes, reopening no.S&P 3850, 4200, no again 3850, wait it’s back up to 4150.Push & pull macro and market dynamics dominated Q1, leaving investors confused on how to approach Q2.This is why in this piece we will:* Quickly review Q1 through the lenses of Volatility-Adjusted market performance across asset classes;* Refresh the key variables behind our quantitative TMC Asset Allocation Model;* Reflect on asset classes valuations and conclude with our ETF Portfolio allocation to kickstart Q2.For long-term macro investors, Q1 brought mildly positive returns with a truckload of volatility and went away without marking the start of any major macro trends.Reminding ourselves that US cash equivalent products yield ~5%, there was little to be excited about.Our Volatility-Adjusted Market Dashboard (VAMD) screens global macro asset classes returns from a risk-adjusted performance, and it shows a 3-month Z-Score no major vol-adjusted action.Rather than in being outright long or short a certain asset, the most significant Q1 macro trend was a rotation in US equity sectors.Tech and Consumer Discretionary largely outperformed defensive sectors like Healthcare and Utilities.But why?This excellent chart from Goldman explains why: mechanical re-leveraging flows, not fundamentals.Back in November, Powell was channeling his inner Volcker – no end in sight for the hiking cycle, and the most hated assets in such macro environments are high-beta, unprofitable tech/meme companies.Fast forward to early 2023: disinflation first and a more prudent Fed after the SVB saga bring in systematic flows and ‘’pivot buyers’’, leading to a massive short squeeze.Nothing to do with fundamentals, but a good reminder to respect the power of macro-insensitive flows.So, with that in mind how do we approach Q2?First: the macro fundamentals.The TMC Quadrant Asset Allocation Model (QAAM) blends together monetary policy and economic growth indicators to identify the prevailing Macro Quadrant and hence the most appropriate asset allocation tilt.It combines that with an assessment on valuations, correlations and portfolio volatility to come up with the final allocations depleted in the Long-Term Macro ETF Portfolio.The Y-Axis of our QAM tells us the global monetary policy stance remains tight due to elevated and sticky real yields, and about to get tighter as the flow of financial money turns more negative.Long-dated real yields are now positive and above equilibrium in many jurisdictions, and that is negative for growth and markets as our debt-based system struggles to roll over cheap leverage.In the US, sustained periods of above-equilibrium real yields lead to poor market performance (2015, 2018).In 2022, it was the rate of change in real yields that scared markets: going from the -0.75% March YOLO levels to the +1.50% October ‘’Powell = Volcker’’ levels in only 6 months required tectonic adjustments in valuations.Since then, real yields have stabilized but have averaged a tight +0.93% for 6 months already.In Q2, real yields are likely to remain in tight territory again.And markets don’t like tight conditions, especially if they last for a long period of time.Ok.But what are we really doing QT or are Central Banks printing money?How does that affect macro and markets in Q2, and how to best position portfolios?Let’s dig in…Eager to read the remaining part of this macro report?Come join The Macro Compass premium platform to get access to Alf’s full-length timely pieces, actionable investment strategy and much more!Check out which subscription tier suits you the most using the link below.For more information, here is the website. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit themacrocompass.substack.com

Look Beyond

The world is big, and macro investment opportunities pop up where you least expect them.Looking beyond the US and focusing on true global macro is an underrated and fruitful exercise.So, let’s do that.In this piece, we will cover the latest macro developments and discuss trading opportunities in Europe, China, Japan…and yes, ok, we will sneak in a quick word about US liquidity too – very important for global markets.China - Opportunity or Bull Trap?Let’s start from China: what about the reopening trade?The Chinese Communist Party’s plan put in motion back in 2021 had as its first objective to clamp down speculative behavior in sectors that weren’t considered ‘’in line’’ with the CCP’s views for China: excessive animal spirits in the real estate and tech sectors were to be tamed.And they were – a substantial deleveraging was achieved, which brings us to the second step.The Chinese reopening: bring back domestic consumption and steer growth where you want to see it.So, where do we stand there?Chinese official data is often to be taken with a pinch of salt, but here is an interesting take on PMIs:The New Orders subindex just printed at multi-decade highs (orange), while the Exports subcomponent has rebounded but not nearly as much (blue): the Chinese reopening is real, but it’s been met by sluggish global growth and hence exports struggle to pick up.Don’t trust Chinese official data?Alternative data show how domestic flights are up 40% YoY, and a pickup in international flights should follow with holiday season and higher temperatures.On top of it, China has pre-emptively stimulated in H2-2022 delivering a solid flow of credit to corporates.As this interesting chart from Clocktower shows, once China credit creation picks up (purple) it’s only a matter of time before Chinese equities (blue) rally.Chinese equities continue to look attractive over the medium term here, with stock indexes still well below the January highs and with a 10%+ potential upside based on broader macro data further reflecting the reopening trends in Q2 and supportive credit creation.This view is reflected in our Macro ETF Portfolio, where…Eager to check out Alf’s Macro ETF Portfolio and trade ideas?Want to keep reading his global macro analysis on Europe, Japan and the US?Come join The Macro Compass premium platform to get access to Alf’s full-length timely pieces, actionable investment strategy and much more!This article is available to the All-Round subscribers - get in that premium TMC tier using the link below. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit themacrocompass.substack.com

Follow The Money

In 1992, judge Giovanni Falcone was killed by the Sicilian mafia.Falcone and his colleague Borsellino were at forefront of major investigations that uncovered much of the mafia’s business and led to the incarceration of many criminals.His method was pretty simple: follow the money, find the mafia.The same methodology can be very useful in understanding the real extent of today’s banking stress, which is crucial for macro and markets going forward.Follow the money, assess the banking stress.That’s why in today’s piece we will:* Show you how to ‘’follow the money’’, explaining which reports to focus on and how to analyze them week by week to assess the depth of the banking stress;* Refresh our market views and actionable long-term macro ETF portfolios.Let’s follow the money together.If banks are under stress from deposit outflows, they sure will be tapping the available liquidity facilities.So, have they? And by how much?Before we answer this question let’s first define which liquidity facilities are available to US banks – they differ in conditions, eligible collateral, loan tenors etc.A) The Discount Window (Fed): very wide set of collateral accepted (not limited to Treasuries and MBS, but also some loans) at market value, max 90 days term lending at top of Fed Funds range (5% now); it comes with a strong stigma from the GFC.B) BTFP (Fed): newly created Fed facility that accepts Treasuries and MBS without any liquidity or market haircuts (!) and lends for up to 1-year at 1y OIS (~Fed Funds) + 10 bps (4.75% now);C) FHLB Advances (not Fed): the Federal Home Loan Banks program that allows member banks to post collateral with haircuts (UST, MBS and some mortgage loans) and at market value to get funding (‘’advances’’). Funding duration is flexible, but FHLB advances are relatively more expensive.Here is a very handy table from JP Morgan summarizing the 3 facilities:So, let’s now follow the money – did banks use these facilities, and by how much?The Fed’s H.4.1 report is released every week (here) and it informs us on the Discount Window and the BTFP.Banks drew $160 bn from these facilities in the SVB debacle week, and net zero (!) the week after.We also know that First Republic Bank drew about $110 bn from the Discount Window, which means all other US banks only drew $50 bn from the combined Fed facilities 2 weeks after the stress started.Not much, really.But maybe banks used the third option - FHLB Advances more aggressively?FHLB disbursed loans to commercial banks are only reported quarterly, but you can track the amount of money FHLB is raising through bond issuance here – even if not fully distributed, it gives us an idea about the potential incoming demand FHLB expects.Now, stand ready for the number.The FHLB has raised as much as $300 billion in the last 7-10 days, largely outpacing its normal issuance pace.A huge figure.So, are US banks truly experiencing severe stress after all?Let’s keep following the money together to find the answer to the most important question for markets right now…Eager to read the remaining part of this macro report?Come join The Macro Compass premium platform to get access to Alf’s full-length timely pieces, actionable investment strategy and much more!Check out which subscription tier suits you the most using the link below.For more information, here is the website. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit themacrocompass.substack.com

Powell Strikes Again

The Fed understands that banking stress is ultimately disinflationary as the flow of credit to the real economy slows down and so does economic activity, and inflation with it.Markets are now busy interpreting what it all means, and this is why in this timely piece we will:* Discuss the 2 most important takeaways from the Fed meeting;* Assess market reactions across asset classes, with a particular focus on the bond market;* Disclose the resulting tactical trade ideasWait: Have We Broken Something Here?“Recent developments are likely to result in tighter credit conditions for households and businesses and to weigh on economic activity, hiring, and inflation.”With inflation sticky and still trending above 5%, for the Fed to come out of the gate with a forward-looking statement like this is quite something.Powell & Co deeply understand the disinflationary nature of banking stress.This was also reflected in the economic forecasts, and particularly in the uncertainty surrounding them.Due to the banking stress, a large number of FOMC participants is worried about downside risks to GDP growth while less and less participants expect upside surprise on inflation.In other words, the FOMC is more worried about a disinflationary recession than anything else.“The Committee anticipates that some additional policy firming may be appropriate to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time.”From “ongoing rate increases” to “some” and “may”.Again, this shows that the Fed will be on the lookout for signs that they might have done enough damage through this banking stress.This is something deeply new, as until now the Fed was effectively on autopilot: keep monetary policy incrementally tight until you get people unemployed and inflation comes down.Don’t make any assumptions, just get the job done.Here, we are looking at a different Fed.And the Summary of Economic Projections (SEP) clearly shows it.Despite predictions for lower unemployment rate and higher core inflation in 2023, most likely to account for the banking stress uncertainty the median Fed Dot for December 2023 wasn’t revised higher.This is a proactively cautious Fed looking to assess the damage despite inflation still running hot.But the second point was even more important, as it led to crucial market moves and therefore opened the door to some interesting market opportunities.Let’s dig in…Enjoyed it so far and eager to read the remaining part of this macro report?Come join The Macro Compass premium platform to get access to Alf’s full-length timely pieces, actionable investment strategy and much more!This article is available to the All-Round subscribers - get in that premium TMC tier using the link below. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit themacrocompass.substack.com

What Now?

The giant Swiss bank Credit Suisse is no more.Central Bankers have announced several facilities during weekends to calm markets down.The 2008 vibes are very strong – what now?In this piece, we will provide you with a level-headed analysis of:* The Credit Suisse deal, including its repercussions on the broader European bank and credit markets;* The scope and effectiveness of the Fed’s BTFP facility and the reactivation of global $ swap lines;* How are we managing our portfolio, and what lies ahead for markets.Credit Suisse has been acquired by UBS for $3.3 billion in a deal brokered by the Swiss government over the weekend – the deal also includes about $10 billion the Swiss government will cover for potential CS losses hitting UBS and around $108 bn of liquidity facilities the Swiss National Bank will make available to UBS.This is a decent deal for UBS, and yet markets were unhappy because of one important detail.While CS equity investors got (some small) residual value out of the deal, $17 billion of CS’ Additional Tier 1 bonds (a “hybrid” instrument between bonds and equities) were completely written down to zero.Regulators decided to sweeten the deal for UBS by sacrificing AT1 investors denying the standard waterfall.Investors were busy extrapolating that AT1 are now a no-go if regulators can subordinate these bonds to equity capital in events of stress – returns don’t warrant the risk in these bonds, and the AT1 market in Europe is pretty big at $275 billion.That’s an incorrect extrapolation, in my opinion.If they did their homework (I doubt…), CS AT1 investors knew already the risks they were running: the absence of “write-up” mechanism is very clear for these bonds, which means the risk of getting marked down to zero if a Viability Event/AT1 Trigger (read: bank about to go belly up) occurs is high.Such a permanent write-down in AT1s is NOT the standard in Europe, as you can see below:So, yes: CS AT1 investors have been penalized but they knew they were running permanent write-down risks.And no: the AT1 market in Europe is not dead and the spill-over risks in the banking sector are low.After the GFC, the bilateral unsecured exposure between banks has been massively reduced: unsecured interbank loans through the Euribor/Libor markets are mostly a thing of the past, and regulators ensured banks are highly penalized for holding uncollateralized bonds issued by other banks (like AT1s).In other words, that means the direct contagion from the CS debacle within the banking system will be low.Central Banks have announced plenty of facilities during recent weekends.After the SVB debacle, no other US banks have capitulated yet and the Credit Suisse saga has been solved.So why are markets still so stressed?Is the bond market smelling something bad?Let’s dig in…Enjoyed it so far and eager to read the remaining part of this macro report?Come join The Macro Compass premium platform to get access to Alf’s full-length timely pieces, actionable investment strategy and much more!Check out which subscription tier suits you the most using the link below.For more information, here is the website. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit themacrocompass.substack.com

The Moment of Truth

Market pressures on US banks are now spreading to Europe, where the already troubled Credit Suisse asked the Swiss government for help and got a liquidity boost.Investors are asking the tough questions now, which means the moment of truth looms large.Data-driven, holistic macro analysis is crucial to correctly answer these questions.In this piece, we will:* Review the current banking situation, assessing the widely different degree of tightness in regulatory and accounting frameworks US and European banks are subject to;* Do the heavy lifting on digging up the real metrics you need to monitor when assessing the vulnerability banks have to higher interest rates (spoiler: not HTM unrealized bond losses…);* Conclude with the big picture macro take on banks, and important changes in our Macro ETF Portfolio allocations.Nothing like a front page of The Economist to tell us we have moved to the panic phase.Let’s review where we stand, starting from the US.The US banking regulation and accounting frameworks have some pretty big flaws.Yep, you read that right.1. Banks with a balance sheet below $250 bn can act a lot like cowboys…No need to adhere to NSFR (Net Stable Funding Ratio), a rule that forces large banks to have a good proportion of their liabilities in sticky, long-term funding which limits liquidity risks.No need to adhere to LCR (Liquidity Coverage Ratio): ‘’small’’ banks can buy a disproportionate amount of less liquid securities like corporate bonds or mortgage-backed securities instead of Treasuries.The problem is that a $249 bn balance sheet bank is not small.For reference, a top 3 German bank has a balance sheet of less than $200 bn – seriously, top 3 in Germany.This lax regulatory treatment for ‘’small, but not so small’’ banks is very dangerous.2. Even large banks booking bonds in HTM are disincentivized (!) to hedge interest rate risksHTM = friendly accounting: book bonds there, forget about them as they are valued at amortized cost.Prudent risk management still suggests you should hedge interest rate risk.Yet, US accounting rules disincentivize interest rate hedging for HTM bonds – nuts.But the cherry on the cake…3. No proper interest rate risk stress testing (!!!)Guys, this is out of this world.As we will discuss, Europe has a quite extensive framework to stress test the interest rate risk that European banks take on their aggregate balance sheets (the net exposure deriving from loans, mortgages, bond investments, bond issuance, long-term liabilities and swaps).It’s called IRRBB (Interest Rate Risk in Banking Books) stress-testing.The US equivalent? It doesn’t exist!Here is the IMF calling US regulators out on the topic:Please take a second to reflect on how bad this is.‘’Small’’ US banks are subject to much laxer regulatory requirements.But even large US banks are disincentivized from hedging rate risk on HTM bonds and even worse they are not subject to extensive stress testing on the overall interest rate risk they run on their balance sheets.Europe has much tighter regulatory standards and accounting framework, and yet the panic seems to be spreading there too.So, here are the key questions.What’s the correct approach to assess how and which US and European banks are really vulnerable to higher interest rates and liquidity risks?And what’s the big picture macro take here when managing a long-term ETF portfolio?Let’s dig in…Enjoyed it so far and eager to read the remaining part of this macro report?Come join The Macro Compass premium platform to get access to Alf’s full-length timely pieces, actionable investment strategy and much more!Check out which subscription tier suits you the most using the link below.For more information, here is the website. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit themacrocompass.substack.com

Contagion Risks

If a couple of regional banks were so bad at managing their interest rate risk and deposit outflow risk to blow up in a few hours, how can we really be sure other banks won’t face similar problems?Having run a large investment portfolio at a European bank and been part of the management for the Treasury department, I will try to use my practical experience to provide you with:* A quick primer on how banks approach risk management of a large securities portfolio;* A level-headed analysis of the damage that higher interest rates do to a banks’ balance sheet, and the resulting assessment of broad contagion risks;* An update on inflation and the likely Fed reaction function in this environment.Banks buy bonds for two main reasons: clipping coupons and regulation.When you attract deposits and do nothing on the asset side, you are going to accumulate reserves at your domestic Central Bank.But banks want to make money, and bonds generally yield more than Central Bank reserves (chart below).Sum up regulation (LCR) forcing large banks to own ~20% of their balance sheet in liquid assets (read: bonds) and there you go: banks have huge investment portfolios to clip coupons and meet regulation.How do banks approach the risk management of such gigantic portfolios?A prudent bank hedges most if not all its interest rate risk coming from the securities portfolio with swaps.The bank buys bonds (receives fixed rate) and pays swaps (pays fixed rate) against them as a hedge.Banks earn the (credit) spread between bond yields and swap yields, and that’s it.But now comes the trick: accounting.Swaps are derivatives, and their standard accounting treatment is to directly hit the P&L of the bank hence causing quite some immediate volatility for the financial results of the bank.Banks don’t like that at all.That’s why the regulator allows for something called hedge accounting: if you buy bonds and put them in Available-For-Sale (AFS) and use swaps to hedge the interest rate risk, all that P&L volatility is gone.The small volatility of offsetting bonds and swaps hits the capital position of the bank.Easy-peasy, no drama: little volatility as risks are hedged, and friendly accounting treatment (no P&L vol).But what happens if you book bonds in Held-To-Maturity (HTM) instead?In the US, once you book bonds in HTM the accounting rules are such that hedging the interest rate risk on these bonds is quite punitive.Swaps hedging HTM bonds do not receive the friendly accounting treatment and hence hit the P&L of the bank – but bonds don’t, which creates a massively inconvenient asymmetry and P&L vol that banks hate.The result is that US banks end up NOT hedging the interest risk on HTM bonds.This is important because the HTM losses accumulated on these bonds can be very large.P.S. My spreadsheet failed me on Schwab. The bank’s capital is 25+ bn, not 8. Hence losses are about 50%+ of capital, not 171%.Even for systemically important banks like Bank of America these losses could wipe out half of their capital!So, are large US banks at risk of going belly up too?And given today’s inflation print, what will the Fed do?Let’s dig in…Enjoyed it so far and eager to read the remaining part of this macro report?Come join The Macro Compass premium platform to get access to Alf’s full-length timely pieces, actionable investment strategy and much more!Check out which subscription tier suits you the most using the link below.For more information, here is the website. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit themacrocompass.substack.com

Banking Crisis?

Silicon Valley Bank went belly up in about 30 hours.And no, it’s not the Fed’s fault.It’s the result of a very concentrated funding base, embarrassingly bad market risk management and a ton of moral hazard at play.This piece will attempt at answering the questions all of us have been asking:* What exactly went so wrong for a $200bn+ balance sheet bank to go down so fast?* How serious are the spillover risks? Is the entire US banking system in trouble?* How will the Fed and markets react?Disastrous Risk ManagementWhat SVB did with their investment portfolio is either a signal of enormous incompetence or of outright moral hazard at play – gamble away billions as policymakers will rescue you anyway.I can’t believe incompetence reaches these levels, and there are some clear hints moral hazard was at play.First of all: why do banks buy all these bonds?Post GFC, regulators forced banks to own an amount of high quality liquid assets (HQLA) at least big enough to meet a stressed outflow of deposits for 30 days => Liquidity Coverage Ratio (LCR) above 100%.What qualifies as HQLA?Reserves at the Central Bank, Treasuries, but also corporate bonds and MBS to a certain extent.As a result of LCR regulation, banks all over the world have flushed their balance sheets with trillions of bonds. Such a large amount of bonds on the balance sheet also comes with risks though, right?Interest rate risk comes to mind: if you purchase Treasuries and yields rise, you lose money.That’s why banks hedge (!) the lion share of the interest rate risk coming from their HQLA investments.The mechanism is simple.When you buy Treasuries, you lock in a fixed yield you receive and rising interest rates represent a risk.To hedge that risk, you enter into an interest rate swap: this time, you pay away a fixed yield and receive variable payments in exchange.There you go: you received a fix rate when buying Treasuries and you pay a fixed rate in the swap – a hedge.Treasuries generally yield a bit more than swaps, and that’s where you make your money (swap spreads).In this example, SVB (A) would buy 10-year Treasuries and enter into a swap to hedge interest rate risk.SVB (A) pays a fixed 10-year rate (OIS) in the swap, and receives the variable overnight Fed Funds rate for the next 10 years plus a spread (swap spread).This would allow SVB to hedge the interest rate risk and earn a small spread on their HQLA portfolio.The problems?SVB had a gigantic investment portfolio as a % of total assets at 57% (average US bank: 24%) and 78% was in Mortgage-Backed Securities (Citi or JPM: around 30%)……and most importantly they DID NOT hedge interest rate risk at all!The duration of their huge portfolio before and after interest rate hedges was…the same?!Effectively, there were NO hedges.This means SVB was not applying basic risk management practices, and exposing its investors and depositors to a gigantic amount of risk.Economically speaking, a $120 bn bond portfolio with a 5.6y non-hedged duration means that every 10 bps move higher in 5-year interest rate lost the bank almost $700 million.100 bps? $7 billion economic loss.200 bps? $14 billion economic loss.Basically the entire bank’s capital wiped out.As the tech/IPO boom faded, deposits stopped coming in 2022.Recently, depositors started taking their money away and forced SVB to realize this huge losses on bond investments to service deposit outflows.The concentrated nature of the deposit base and awful risk management meant SVB went belly up real quick.Many people are now calling for a blanket bailout.But the evidence that moral hazard was at play are too big to be ignored.And we should not reward moral hazard.Moral HazardCompanies go belly up – it happens.Perhaps it was just huge incompetence at work, or bad luck.But please consider the evidence that moral hazard played an important role.Here are 3 interconnected facts which are hard to ignore:1. The outrageous use of accounting tricksHQLA investments can be booked either under the Available For Sale (AFS) or Held To Maturity (HTM) accounting regimes.AFS investment unrealized gains/losses do not hit the P&L of the bank, but they do show up in the capital position of the bank.Booking bonds in HTM instead prevents gains/losses from showing up at all – convenient, right?See for yourself: SVB had a gigantic bond book and made an unusually large use of the convenient HTM accounting regime.The unrealized losses as per Dec 2022 in the HTM portfolio alone amounted to $15 billion, enough to wipe out the bank’s capital but conveniently hidden through the abnormal use of this accounting trick.You don’t book $90 billion of unhedged (!) bonds in HTM by mistake or incompetence – this is moral hazard.2. Not hedging: just ignorance, you say?In December 2021, SVB had about $10 billion of interest rate swaps.Probably way too little to hedge the entire interest rate risk, but that’s not my point.In their financial statement, they show a clear understanding of what these swaps ar

Money

Money creation is king.It leads economic activity and therefore financial markets performance.That’s why despite following countless macro data, market practitioners often pay particular attention to indicators tracking ‘’money printing’’.But money isn’t a trivial topic: how do we correctly measure money creation for the real economy?Which countries are printing more or less money today?What does this imply for growth and markets ahead?This article answers all these questions by:* Walking you through the principles behind the construction of my flagship Global Credit Impulse index;* Providing you with the most recent money creation figures both at a country level (US, China, EU, UK) and at an aggregate level;* Discussing the implications for economic growth and asset classes performance.Let’s start with a 3-months old chart that speaks very loud about the importance of ‘’money printing’’:The TMC Global Credit Impulse index (orange, left-hand side) accurately predicted the direction of travel for S&P500 earnings per share growth (blue, RHS) with a few quarters of lead time.Back in late summer 2022, analysts were expecting EPS to grow healthily in 2023.Our flagship money creation indicator instead suggested 2023 EPS would contract and perhaps turn negative already by March.Well, it turns out our flagship indicator was right.But how do we actually measure real-economy money creation?First, let’s set the record straight: commercial banks and governments print money we can use, not Central Banks – they print money for banks, also known as bank reserves.Here is how banks and governments print real-economy money:When the banking system extends a loan or a mortgage, it creates a new liability for the consumer (loan/mortgage) but also a new asset (a new bank deposit).That newly created credit is money that didn’t exist before, and it is used to purchase a new car/house.Bank credit creation = real-economy money printing.When the government spends more money than it taxes us for (deficit), it blows a hole in its balance sheet and throws net wealth at the private sector.Lower taxes or stimulus cheques increase the real-economy money available for the private sector.Government deficit spending = real-economy money printing.Take a look back at the first chart: the more real-economy money sloshing around the largest economies in the world, the more economic growth ahead and vice versa. It makes sense, right?We have established that bank credit creation and government deficits are key pieces of the puzzle to track real-economy money creation.But what else is needed to build a proper money printing indicator?How has the TMC Global Credit Impulse index changed with the latest data update?And what does it mean for growth and markets ahead?Let’s dig in…Enjoyed it so far and eager to read the remaining part of this macro report?Come join The Macro Compass premium platform to get access to Alf’s full-length timely pieces, actionable investment strategy and much more!Check out which subscription tier suits you the most using the link below.For more information, here is the website. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit themacrocompass.substack.com

Nope

Hi everybody, and welcome back to The Macro Compass!Economic data is surprising on the upside, and markets are busy trying to digest what this means for the Fed. Terminal rates are now priced well over 5% in the US and now around 4% in Europe, and bond traders are quickly dismissing all cuts in 2023 too.So, have we avoided a recession for good and how resilient is the global economy to higher interest rates? The answer to this question will be vital for portfolio performance in 2023.Hence, in this piece we will: * Discuss the recent upside surprise in macroeconomic data – how resilient is the global economy?* Dig deep into Dr. Yield Curve – what’s this PhD in economic telling us now?* Conclude with our assessment and portfolio construction going forwardRecently, macro data has been surprising on the upside: retail sales, PMIs, housing data all look better. And this is why.US financial conditions have materially eased from November to early February. A sharp loosening of financial conditions is often associated with an improvement in macro data with a 1-2 months lag.The chart above proves the point: the US NAHB Housing Index (blue, RHS) readily responded to looser financial conditions (orange, LHS) with a small time lag exactly like it did in 2021 and 2022. The mechanism is easy to understand: lower interest rates and easier access to credit allow more home buyers to step in, hence leading to improved sentiment in the housing market. Looser financial conditions also help companies and consumers via cheaper access to leverage, higher equity prices and a weaker USD and hence feed into better PMIs for instance.Should we expect further upside surprises in economic data?For soft indicators (e.g. PMIs) the lag is pretty short, while coincident indicators (e.g. labor market, industrial production) take a little longer to react – March might bring some more positive news…but. Financial conditions have aggressively tightened again in the last two weeks. And March data releases cover February data, where the major seasonality boost from January could reverse.The January Non-Farm Payroll numbers were boosted by a much lower amount of post-holidays seasonal layoffs than usual – February NFPs (released on March 10) could disappoint if seasonality trends reverse.So, further upside surprises or not?Lack of conviction is the name of the game recently. We went from pricing a 40-50% chance of a near-term recession in December to pricing away all 2023 Fed cuts in early February.The results of this poll are very telling – I asked FinTwit whether they’d buy or sell 30y Treasuries here. Over 13,000 people replied and basically they have no clue.I am showing you this so you can zoom out. In this business we are often overwhelmed with information – or rather with noise, I should say. This is why I like smoothing macro data: it allows me to take a step back from the noise of daily data and ever-changing narratives and have a panoramic view.So, let’s:* Look at the big picture for macro data;* Ask the PhD in economics Dr. Yield Curve a couple of questions;* Conclude with our assessment and portfolio construction going forwardEnjoyed it so far and eager to read the remaining part of this macro report?Come join The Macro Compass premium platform to get access to Alf’s full-length timely pieces, actionable investment strategy and much more!Check out which subscription tier suits you the most using the link below.For more information, here is the website. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit themacrocompass.substack.com

Yes, But What About Europe?

Hi everybody, and welcome back to The Macro Compass!Most macro commentary focuses on the US.But over the last few months, the real golden kid has been Europe.Recently the EUR has appreciated 10%+ against the US Dollar, macro data seems to suggest a recession has been avoided and the European stock market is on a roll having outperformed the S&P500 and other peers.For foreign macro practitioners, the complex European architecture and its many dimensions appear like an unattractive black box to analyze.This is why in this piece, we will:* Discuss the main drivers behind the recent European macro and market outperformance;* Answer the big question: where do we go from here?September 2022.European stock markets in free fall, EUR/USD at 0.95 – will Europe be able to keep its lights on this winter? These worries were justified by the complex macro and energy picture back then.But while not good at long-term policymaking, Europe is great at avoiding last-minute disasters.The chart above shows the gargantuan amount of GDP per capita allocated by different European countries to households and firms in an attempt to fight the energy crisis.On average, countries allocated ~5% of GDP per capita against the energy crisis: that’s a huge figure.To put it in context, an entire year’s Italian fiscal deficit ranges about EUR 50-60 bn and Italy allocated over EUR 90 bn (!) solely to shield consumers and firms from higher energy prices. Wow.Again, Europe is bad at long-term policymaking but good at emergency measures.Using public finances to shield the private sector from a structural trade/commodity problem isn’t a viable long-term solution, but it sure works in the short term because it fixes terms of trade.What’s that?Terms of trade indices measure the relative performance of a country’s export and import prices.Better (higher) terms of trade = the value you get out of your exports is outperforming the value of the stuff you need to import from outside, and vice versa.Terms of trade are important for the currency: deteriorating/improving ToT often involve a weaker/stronger currency since the country has to spend more/less to import the same amount of products.I mean, this chart is quite telling: as soon as Europe massively intervened and terms of trade (orange) started improving, the EUR caught a relentless bid.A stronger EUR and better sentiment underpinned the recovery in European risk assets too, but the kicker was that government intervention also killed the recessionary vibes.The extreme pessimism around the manufacturing industry was now less justified as input and energy costs were subsidized by governments, and so an immediate earnings recession had to be priced out.European stocks staged a massive rally and outperformed many global peers.On top of it, soft macro data started validating this new narrative as PMI surveys saw more optimistic answers about future economic growth. This begs the question: where do we stand now, and what’s ahead for Europe?The chart below is an eye-opener…Enjoyed it so far and eager to read the remaining part of this macro report?Come join The Macro Compass premium platform to get access to Alf’s full-length timely pieces, actionable investment strategy and much more!This piece is reserved to All-Round Investor subscribers - check out the product clicking on the button below.For more information, here is the website. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit themacrocompass.substack.com

When To Buy Bonds?

Hi everybody, and welcome back to The Macro Compass!There is a time to be long, a time to be short and a time to go fishing.As inflation skyrocketed and the Fed turned hawkish, bonds were kryptonite for investors for most of 2022: it was time to be short.Between October 2022 and today we have instead seen inflationary pressures somehow moderate but the economy hanging in there, with 10y Treasuries stuck between 3.50% and 4.00%: time to go fishing.With long-dated Treasury yields once again approaching 4%, might this be the time to go long?In this piece, we will:* Look at history and identify what were the ideal conditions to buy bonds (you’ll be surprised);* Focus on the present, and assess whether these conditions are met today;* Answer the big question: is it time to buy bonds?Let’s say you were looking for a 10%+ return by buying bonds and holding them for 12 months.Your objective is to capture that initial, vicious 100+ bps move down in 10-year Treasury yields.Now imagine somebody asked you this question.In hindsight, what were the prevailing conditions in that very perfect moment when to go long bonds and harvest a 10%+ return in the subsequent 12 months looking at the past 3 decades?Don’t cheat.You probably said ‘’when the Fed announced QE’’ or ‘’right at the beginning of the 2001 or 2008 recession’’.And while these periods were good for bonds, they didn’t deliver that banger return you’re looking for.The best periods to buy bonds were when:* Nobody wanted or thought he needed bonds at all;* A few quarters before companies started losing money and people started losing their jobs.Let’s talk about the chart and the table above.Buying 5-10 years US Treasuries in April 2000, March 2007 and October 2018 delivered a subsequent 12-month return north of 10% - in medium term bonds, that’s quite a banger return.Notice: no QE was announced in the immediate aftermath, and neither we were in a recession already.Instead, the first common feature across these periods is that everybody hated bonds.In April 2000 the Fed was still hiking rates as core inflation had upside momentum, animal spirits were still running wild in the Dot-Com space and the economy was holding on okay – nobody needed bonds.In March 2007 we were in the midst of the US real estate miracle (read: bubble) with unemployment rate at cycle lows and the S&P500 in an unstoppable march higher – who needed bonds, again?And do you remember October 2018? Ongoing QT, Powell talking about a higher neutral rate, and a strong labor market – nobody wanted bonds.The second common feature is that the odds of negative EPS growth and higher unemployment rate were rising rapidly.Basically, nobody wanted bonds but everybody would soon need them.For all these period in the subsequent 4-5 quarters earnings growth didn’t look good, the labor market cooled off and core inflation stalled.Macro data was unequivocally showing a nominal growth slowdown, which in 2 out of 3 cases morphed into an outright recession (2001, 2008).History shows the best moment to buy bonds is right at the intersection when nobody wants them, but macro data will soon remind investors they do instead need bonds.So, with 10-year Treasury yields fast approaching 4% again……is it now time buy a truckload of bonds?Let’s dig in together…Enjoyed it so far and eager to read the remaining part of this macro report?Come join The Macro Compass premium platform to get access to Alf’s full-length timely pieces, actionable investment strategy and much more! Check out which subscription tier suits you the most using the link below.For more information, here is the website. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit themacrocompass.substack.com

FREE Article - To YOLO or Not To YOLO?

This is a free full-length piece available to everybody.If you find it valuable, consider subscribing to the premium TMC service.On the premium The Macro Compass platform, we do the hard work to deliver high-quality macro insights, tools and actionable investment strategy week in and week out.Institutional-level macro strategy in plain English at a fraction of the cost.Hi everybody, and welcome back to The Macro Compass!The YOLO crowd is back with a vengeance.Over the last month we have seen nearly bankrupt companies rallying 100%+ in a single day, and companies reporting awful earnings staging a 20%+ rally the day after.In other words: YOLO is back, bro.In this piece, we will:* Look back & quantitatively assess the mechanics behind this big Meme Rally;* Answer the big question: if bonds yields are rising and cash-like products now yield 5%, how on Earth is it that we are witnessing such a high-beta rally? And is this the start of a new bull market?Let’s take a step back in time – precisely to early November 2022.The leading narrative was that ‘’Powell is channeling his inner Volcker’’: as the momentum of core inflation kept increasing (orange), the Fed was revising their expectations for the terminal rate (blue) higher & higher.The Fed was all about tighter financial conditions, which is jargon for less animal spirits: a stronger US Dollar, higher borrowing costs and lower multiples.Higher borrowing costs are lethal for very leveraged, interest-rate sensitive sectors like real estate, (unprofitable) tech and Meme/YOLO stocks.Not only that: uncertainty around the Fed terminal rate led to highly volatile bond markets.Rising bond market volatility hurts risk sentiment as the backbone of many institutional portfolio (fixed income) doesn’t dampen overall portfolio volatility but instead contributes to it.Hard to take additional risks in such an environmentBut then, something abruptly changed.We got a couple of ‘’disinflationary’’ prints, and before the recent revisions it even seemed that Powell’s preferred measure of sticky inflation (core services ex-housing) was decelerating on a trending basis.On the backdrop of these disinflationary prints, the bond market staged a relief rally...…and Powell didn’t fight back, at all.And this is when the magic starts to happen: mechanical buying flows from leveraged investors kick in on a very large scale.Here is how it works.Commodity Trading Advisors (CTAs), risk parity and volatility-targeting funds often use volatility as one of their buying/selling signals: the more implied volatility drops and realized volatility keeps declining, the more these accounts can lever up and buy.These mechanical flows can be very large – I estimate these systematic strategies could be easily lifting $1-2 billion (!) of US stocks per day, and the more volatility remains compressed the longer these buying flows last.Why do these mechanical flows matter?Their model-driven, valuation-insensitive nature has a disproportionate effect on two type of stocks:* The most shorted and hated stocks out there;* The least liquid and more flow-prone sectors in the market.Think back in November: what sectors qualify for this definition?Yes: homebuilders, Meme/YOLO stocks, unprofitable tech & co.The short squeeze has been gigantic so far, and it’s well reflected in these two charts from Goldman Sachs.Macro investors were caught very short Tech between November and January, and given the mechanical systematic buying flows we discussed above the need to cover shorts has been big.Particularly over the last 2 weeks, the extent of short covering in Tech has been almost unprecedented.To further validate this thesis, the worst performers in 2022 (left side of the quadrant) happen to be exactly the best performers of 2023 YTD (top side of the quadrant) with the YOLO guys standing out in the crowd.Now, to the big question.Our interactive Volatility-Adjusted Market Dashboard points to some interesting inconsistencies.On a 1-month rolling basis, US front-end nominal rates have moved by over 2 (!) standard deviations and most importantly long-dated real yields trade above 100 bps – that’s quite a restrictive level.The US Dollar is strengthening against most major currencies.Bond, stock and FX implied volatility has stabilized and struggles to decline further.Systematic vol-targeting accounts might have exhausted most of their buying needs, and yet……the Nasdaq and the Russell are 3-6% up over the last month.Can this continue?Look, there are two realities to face.1) Markets can remain irrational longer than we can remain solvent;2) Long-lasting bull markets require rapidly expanding valuations and/or strong earnings growth.The Dot-Com bubble and the US housing market frenzy happened with Fed Funds around 5-6%, not 0%.Animal spirits can be hard to contain, but the Fed doesn’t really have a choice.After the recent revisions, core services ex-housing CPI (the sticky inflation) is still running at over 4% annualized levels a

The Inflation Numbers Explained

Hi everybody, and welcome back to The Macro Compass!We are at that funny phase of the cycle when we look at the most lagging macro indicator (inflation) to assess how late the Fed is going to be this time.In 2021, a gigantic amount of fiscal stimulus and credit creation led to a red-hot economy and yet the Fed was still doing QE and imposing negative real rates – because you know, inflation was subdued.As we speak, the economy is growing very slowly and the housing market is frozen.Still, the Fed is likely to impose 100+ bps positive real rates and QT for much longer than needed while it awaits for the ultimate confirmation that they have damaged the economy for good.And today’s CPI report sent another clear message in that direction.To all the disinflationary soft landing cheerleaders out there: forget about it.In this macro piece, we will:* Have a deep look into the just-released CPI report, assessing its subcomponents according to Powell’s own approach and deriving the likely Fed’s response to these updated inflation figures;* Draw our own conclusions on what this means for macro and markets ahead, with a particular focus on the bond and stock market and considerations on our portfolio strategy.The CPI ReportHow do you analyze inflation numbers?Easy – like the Fed does.It might not be the best way to do it, but it’s the only one that matters.In a speech released a few months ago, Powell told us he divides inflation into three main categories: core goods, housing and services ex-housing inflation.According to the Fed, this is how things stand:* Core goods are in a disinflationary trend due to the post-pandemic economic recalibration back to services and to much easier global supply chains;* Housing inflation lags what happens on the ground, so it’ll keep increasing for a bit and then start declining in line with much softer asking rents we have seen recently;* Services ex-housing is where they pay most attention and want to see sustained progress to 2%.Let’s analyze today’s inflation numbers under the Fed’s approach.Core goods prices are still in a disinflationary trend, but that powerful impulse seems to be alleviating.The excessive imbalance between sizeable goods inventories and rapidly declining demand had led to outright core goods deflation (orange and blue lines), but prices seem to be bottoming here.Nevertheless, freight costs have materially decreased and as shown by the NY Fed the global supply chain keeps normalizing – both positive developments for a continued disinflationary trend in core goods.Core goods inflation is still looking benign for the Fed, but the disinflationary tailwinds might be alleviating.Now, to the hot topics: housing inflation, and most importantly Powell’s preferred measure which is Core Services Ex-Housing inflation.There were important news on both fronts, and the messages coming from the bond market couldn’t be louder.Let’s dig into it, and assess how medium-term investors should approach such a macro environment…Getting access to The Macro Compass full-length pieces requires a paid subscription.On the new TMC platform, you’ll find not only deep and unique macro insights but also ETF Portfolios, tactical trade ideas, interactive tools, and much more.Come join this vibrant community of macro investors - check out which subscription tier suits you the most using the link below.For more information, here is the website. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit themacrocompass.substack.com

What If?

Hi everybody, and welcome back to The Macro Compass!Our base case remains negative EPS growth and higher unemployment rate from May/June 2023. In other words: a recession. But what if we are wrong? In this piece, we will:* Refresh some of our key indicators to assess where are we in this macro cycle;* Update the probability and timing of a US recession;* Unveil our main tactical trade idea.Labor HoardingDuring the pandemic, companies experienced serious staff shortages and faced major challenges when trying to hire new qualified staff. These memories might still be very fresh – look at this chart, for instance.The rapid deterioration in the US housing market (blue) would historically suggest big layoffs in the construction sector which would significantly move the needle for unemployment rate (orange). Some back-of-the-envelope calculations suggest such a frozen housing market should involve roughly 1.5 million job losses in all sectors related to real estate (construction, financials, brokers, ancillary activities). These job cuts alone would put the US in recessionary territory. And instead, the construction sector has been net hiring (?!) over the last 12 months.The only reasonable explanation here is labor hoarding. As companies experienced serious difficulties in hiring qualified staff during the pandemic and perhaps expect this housing market freeze to be short-lived, they are not actively laying off people as they fear it might be hard to get them back. Two confirming factors: wage growth isn’t accelerating and the average workweek hours keep declining. If companies want to hoard labor even if activity slows down, to save costs they will decrease their employees’ working hours and be more mindful about bumping up wages. Labor hoarding seems real, and it might well delay the start of a recession. Ultimately though, it’s a kick-the-can-down-the-road exercise.2. Just Too Much Money? (TMC’s Global Credit Impulse)Let’s now have a critical look at our flagship TMC Global Credit Impulse indicator, and how the Chinese reopening and stimulus interplay with it.And after that, let’s discuss our tactical trade ideas…Getting access to The Macro Compass full-length pieces requires a paid subscription.This article is reserved to All-Round Investor subscribers, which get:* A long-form Macro Report (1x/week); * Timely Tactical Market Reports (additional 2x/week);* Tactical Trade Ideas and the TMC Long-Term ETF Portfolio;* Access to our flagship Interactive Tools to step up your macro investing game;* A Monthly Q&A Zoom call with fellow TMC subscribers and myself;* 50% (!) off any Macro Courses we will ever release.Thousands of macro investors have joined the TMC community already.What are you waiting for? This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit themacrocompass.substack.com

Can You Smell The FOMO?

Hi everybody, and welcome back to The Macro Compass!Last week, FOMO (Fear Of Missing Out) became the prevalent market narrative.As data seemed to further validate the soft landing narrative and Central Bankers became ‘’data dependent’’, markets are FOMO-ing like it’s 2019 again.But 2023 isn’t 2019 – for many macro reasons we are going to touch upon.In this article, we will:* Reflect on last week’s important macro data and Central Bank meetings;* Dig deep into how markets reacted, what’s the new consensus macro regime being priced in and whether macro data will validate it or not;* Assess how to best position portfolios in this environment.Can You Smell The FOMO?In 2019, the Fed pivoted hard and the economy managed a proverbial soft landing.The 2018 hiking cycle which Powell abruptly reversed with his early 2019 pivot slowed the economy down, but not nearly enough to result in a hard landing.The S&P500 earnings growth was only +0.6% (but not negative), core inflation was stable around 2% and the US added 160k new jobs per month: low nominal growth, but not a recession – in other words, a soft landing.But 2023 isn’t 2019 – for many macro reasons we are going to touch upon.First, let’s picture the current market regime.The chart above shows the TMC’s Market Regime Scrutinizer.It measures the market-implied odds assigned to a US recession, soft landing or strong growth regime ahead.It is derived by scrutinizing option markets in fixed income, equity, and currencies and blending the resulting market-implied probabilities in this flagship TMC indicator.Markets are currently pricing a US soft landing as the dominant probabilistic regime (~65% probability), and in recent weeks the left recessionary tail has been aggressively priced out (now ~15%) while the chance of a strong growth regime ahead has been bumped up to ~20%.Even after the apparently very hot labor market data and ISM services, the bond market keeps screaming immaculate disinflation/soft landing as the main regime ahead.* Inflation is priced to drop to 2.5% by year-end, and stay close to 2% in the long run;* Fed ‘’soft landing’’ cuts are priced in: as inflation slows down but without a recession, the Fed can gently cut rates to neutral levels (2.50-2.75%) without resorting to recessionary cuts or being forced to keep rates higher for longer.Bond markets assign only a ~15% probability to recessionary cuts, and a ~30% chance to Higher-For-Longer Fed Funds amidst strong growth and sticky inflation.As a result, the option-implied market points to a ~55% probability of a disinflationary soft landing.When a disinflationary, immaculate soft landing becomes the dominant market regime it’s all about selling insurance and getting paid while…well, not much happens and the Fed is on a very predictable path.And indeed, as the Fed is assumed to be on a more predictable path ahead bond volatility is getting crushed.Lower bond volatility is leading to a much better risk sentiment in equity markets.Now, to the key questions.Are macro data really validating the soft landing base case priced in by markets?Are Central Banks really on a predictable path ahead?And finally: is 2023 going to look like 2019, a year when the S&P rallied 30%+ with minimal volatility?Let’s find out…Getting access to The Macro Compass full-length pieces requires a paid subscription.On the new TMC platform, you’ll find not only deep and unique macro insights but also ETF Portfolios, tactical trade ideas, interactive tools, and much more.Come join this vibrant community of macro investors - check out which subscription tier suits you the most using the link below.For more information, here is the website. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit themacrocompass.substack.com

Markets Don't Believe You, J-POW

Hi everybody, and welcome back to The Macro Compass!Powell didn’t push back enough, and so markets are now rallying hard in his face.And given J-Pow’s lack of real pushback, markets won’t stop unless data comes in very hot (or recessionary). The window for the soft landing narrative is now extended.With one caveat: the narrative is very misplaced.In this piece, we will:* Dissect the Fed meeting, focusing on Powell’s important comments about inflation and the labor market;* Scrutinize markets’ reaction, with a particular focus on the bond market;* Conclude by refreshing our actionable tactical trades and ETF PortfolioPowell didn’t nearly push back enough, and so markets are now rallying hard in his face. And given J-Pow’s lack of real pushback, markets won’t stop unless data comes in very hot (or recessionary). The window for the misplaced soft landing narrative is now extended. Picture this. The first innings of a recession always look like a soft landing, as growth and inflation come down but not to alarming levels yet – exactly like today. And as markets myopically embrace this soft landing narrative, Powell’s lack of pushback against easier financial conditions adds fuel to the fire.Taking a deeper look at what Powell actually said, it becomes increasingly clear markets don’t believe him. At all. #1: On Inflation ‘’We need substantial more evidence to be confident about inflation returning to 2%, in particular as we see core non-housing services inflation still running at 4% annualized with no progress there’’ ‘’We need to be honest with ourselves: inflation might be more persistent in this sticky category, and that means we have to do more’’The 6-month (annualized) rate of change in core services ex-housing CPI is down to 4% - and despite the clear downward trend, Powell told us he is not happy about it.The composition of this downward move (right chart) is indeed a bit messy: medical care deflation accounted for a large portion of it. Despite the progress on inflation, Powell didn’t remotely sound the all-clear yet. The bar for a proper Fed pivot remains high.But then, why did the market rally like if a new round of QE was announced?What’s the bond market trying to tell us here?And most importantly, how to tactically position portfolios now?Let’s dig in…This timely, premium article on the Fed meeting is reserved to paid subscribers to the All-Round and Pro tiers of The Macro Compass.A subscription gets you deep and unique macro insights but also ETF Portfolios, tactical trade ideas, interactive tools, courses and much more!Come join this vibrant community of macro investors to continue reading this piece on the Fed and get access to The Macro Compass platform.For more information, here is the website. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit themacrocompass.substack.com

''Liquidity''