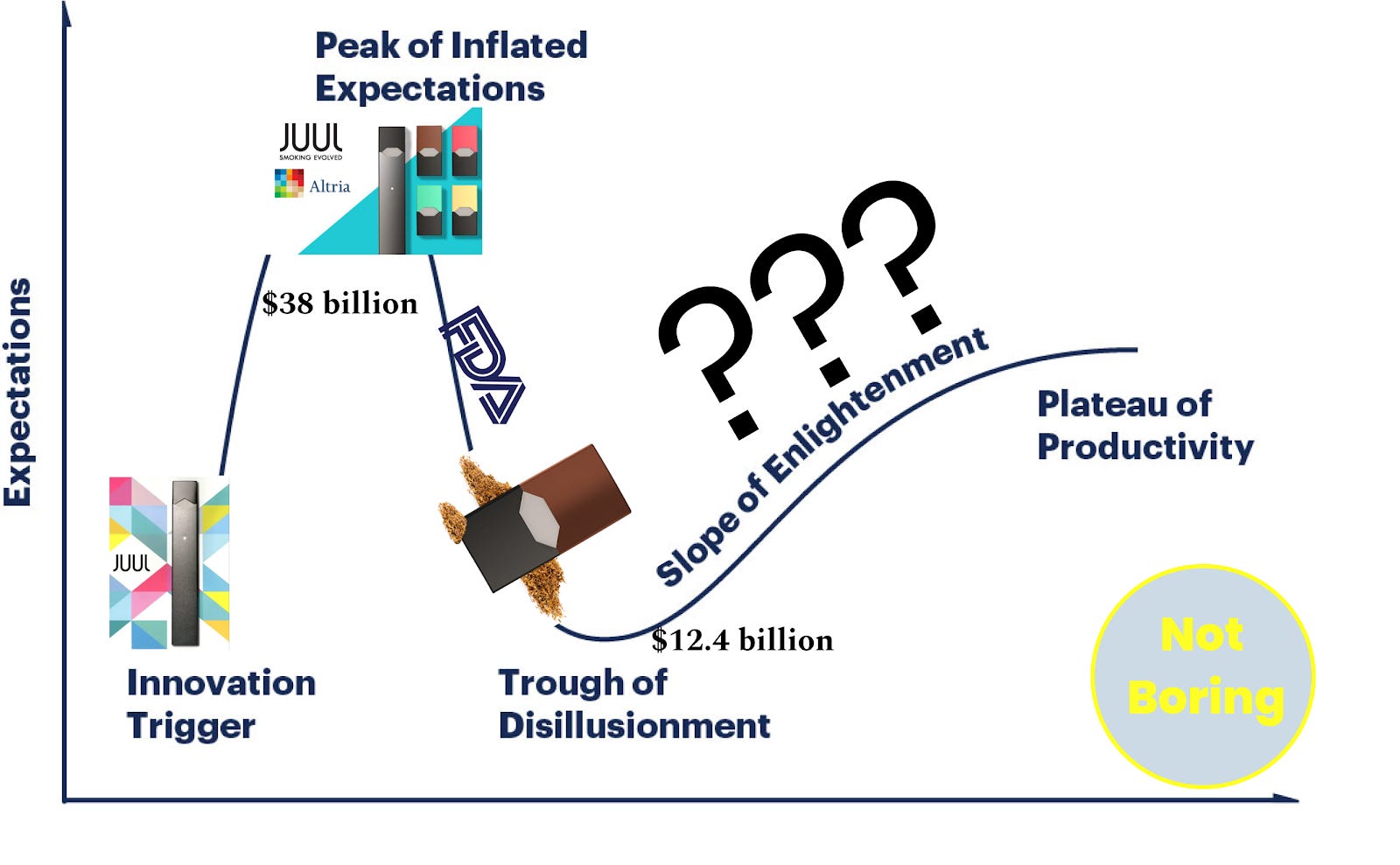

Not Boring by Packy McCormick

83 episodes — Page 2 of 2

Trust the Process (Audio)

Welcome to the 577 newly Not Boring people who have joined us since the last email! If you’re reading this but haven’t subscribed, join 19,190 smart, curious folks by subscribing here!Hi friends 👋,Happy Monday! This is, uhh, an important week here in the United States. With nearly 100 million early votes already in, tomorrow is officially Election Day. If you haven’t voted already, let this serve as one of hundreds of reminders you’ll get today across the internet: VOTE. Find the nearest polling place or early voting locations here: Because it’s not a normal week, I’m not going to write a normal post today. I’ll keep it short(er) and sweet and highlight leadership lessons from my favorite piece of writing: former Philadelphia 76ers GM Sam Hinkie’s Resignation Letter.I’m a huge Sixers fan, so I’m biased, but I promise you don’t even need to know what basketball is to appreciate Sam Hinkie, The Process, and the courage to do the hard thing in the face of ridicule. As one former Sixers colleague told SI, Hinkie’s approach “could be applied to a draft or an apartment search or a dating website.”I’ve been wanting to write about the letter for a while, and this week is right for two reasons. First, last week, the Sixers hired former Rockets GM, Daryl Morey, to become their President of Basketball Operations. Morey made waves last year when he tweeted in solidarity with the Hong Kong protestors, but for our purposes, what’s relevant is that Hinkie was Morey’s protege in Houston before he joined the Sixers. As ESPN’s Pablo Torre put it, “The Philadelphia 76ers kind of just hired their ex-wife’s older sister.” With Morey and new coach Doc Rivers, the post-Process era is officially over, and it’s a great time to revisit The Process.Second, tomorrow, the United States is electing a (hopefully new) President. It’s a good time to reflect on what makes a good leader, and Hinkie’s stoicism and peaceful transition out of the Sixers organization is an example that I hope Trump follows. Of course, I abhor Trump because I think he’s morally bankrupt and is willing to destroy Democracy for personal gain. But even if you’re willing to accept his personal flaws, he’s also an inexcusably short-term thinker, constantly trading what’s popular with his supporters today even for what’s in their best interest tomorrow. He’s the opposite of Sam Hinkie. No complex organization can survive a leader incapable of recognizing the long-term implications of their actions, including the United States. Vote.Today’s Not Boring is brought to you by… MainStreet is free money for startups. You sign up and plug in your payroll, MainStreet finds tax credits and incentives that apply to your business, and then they send you money now. I wrote about MainStreet in September, and maybe you didn’t believe me then. I get it. But since then, MainStreet has found over $1 million for Not Boring readers. That’s $1 million of government money in Not Boring companies’ pockets — an average of $50k — for like 20 minutes of work each.If you run or work for a US business that does anything technical, you need to check out how much money MainStreet can send you today. You don’t owe them anything unless you get paid.Now let’s get to it. Trust The ProcessFor 1,062 painful and glorious days, between May 10, 2013 and April 6, 2016, my hometown, Philadelphia, transformed. Known as the type of people who booed Santa Claus, Philly fans started talking about such highbrow concepts as undervalued assets, probabilities, and compounding. Always the heart of pro sports, Philly became the brain.The reason? Sam Hinkie and The Process.In Two Ways To Predict the Future, I compared two different types of leaders: Worldbuilders and Shotcallers. Shotcallers attack big, obvious markets and use brute force and big budgets to win. Shotcallers are like athletes -- Joe Naimath guaranteed a Super Bowl victory, Babe Ruth literally called his shot, and the Yankees spend their way into contention every year. In the business world, Quibi was a Shotcaller. It thought it could use a $1.75 billion war chest to storm in and own mobile video. Worldbuilders see the way the world should be in the future, lay out a clear vision and unintuitive plan to get there, and patiently execute for years or decades to achieve it, often in the face of vociferous criticism. Jeff Bezos, Elon Musk, Carta’s Henry Ward, and Stripe’s Collison Brothers are Worldbuilders. Hinkie is a Worldbuilder. Hinkie’s Process, his three year term as the Sixers’ GM, is textbook Worldbuilding. He had a vision for an NBA Championship in Philadelphia, charted a probabilistic path to get there, and then did the unconventional, criticism-attracting things required to make it happen. More impressively, he was a Worldbuilder in a league full of Shotcallers. Tech CEOs are supposed to be crazy and future-focused; NBA GMs are supposed to win now. If Hinkie’s Process is textbook Worldbuilding, his Resignation Letter is the Worldbuilding Textbook

Pipe: Business-Funding Fit (Audio)

Welcome to the 389 newly Not Boring people who have joined us since Monday! If you’re reading this but haven’t subscribed, join 18,850 smart, curious folks by subscribing here!Today’s Not Boring is brought to you by… Read on and I’ll tell you how Pipe is the smartest way to finance subscription businesses.Hi friends 👋 ,Happy Thursday! I love my job. * In February, when Pipe announced its seed round, I knew that the company was going to be special. It solves a problem I’d been thinking a lot about and elegantly marries tech and finance. I was jealous I hadn’t thought of the solution! * In July, when Alex Danco interviewed founder and co-CEO Harry Hurst and Pipe raised another $60 million, I knew my initial hunch was right. * Last week, VC Guide included Pipe on its Wishlist of “companies we'd ‘quit our jobs for’ and ‘leave our 4-year vesting schedules early for’” alongside Not Boring favorites Stripe, DoNotPay, Figma, Mercury, Discord, and Webflow. * On Monday, I included Pipe in my essay on software that’s eating the financial markets.* Then on Tuesday, Harry and I decided to do a Not Boring deep dive on Pipe.This is a company that I’ve admired from afar, and it’s surreal that I got to go behind the scenes. I’ve come away even more impressed. I can’t believe I get paid for this. Speaking of which… I told you that when I write company deep dives, I would tell you whether I’m making money via CPA (I get paid when someone signs up for the product) or CPM (I get paid upfront no matter what happens). I had a choice on this one and I chose a CPA deal, because I think that any reader involved with a subscription business should work with Pipe. Now let’s get to it. Pipe: Business-Funding FitI know, I know… I’m getting paid to write this essay. But my reputation is more important to me than any one deal, and I’m willing to stake it on this: for any recurring revenue business, checking to see how much your recurring revenues are worth today on Pipe is a no-brainer. Not comparing Pipe to other forms of financing or discounting is a disservice to your shareholders, including yourself and your employees. Pipe is building an entirely new asset class based on recurring revenue contracts. It’s not equity and it’s not a loan. Pipe lets businesses raise money today by selling their monthly or quarterly subscription cash flows directly through its platform. It’s as if you could convince all of your customers to pay you upfront, immediately in exchange for a small discount. We’re going to go deep on the business, but I love making Not Boring readers money, so I’m going to tell you how to do that first. Here’s how it works: * Sign up for Pipe and connect your banking, payment processing, and accounting software.* Pipe instantly assigns your subscription revenue a rating.* Once approved, you access the Pipe Trading Platform and can see how much investors are willing to pay for your subscription revenue right now. On average, investors pay $0.90 - $0.95 for every dollar of revenue they buy on Pipe.* Choose how much or which of your contracts you want to trade from an auto-populated list.* Click “Payout” and receive the money within a day. * Pipe makes money like an exchange, charging a one-time maximum 1% fee to companies and another fee to investors.From sign up to cash in bank in 24 hours:That’s it. In less time than it takes to set up a Slack group, your company can raise as much money as it might in a months-long, dilutive venture capital fundraising process or in an equally painful venture debt raise that leaves you with liens on your business and warrants outstanding. If you run or work for a recurring revenue business, you should see how much your monthly or quarterly cash flows are worth today. At the very least, it’s free and fun to check; at best, you might be able to fund your company’s growth without raising another round. Who is Pipe for? Pipe works with companies that make recurring revenue - from SaaS to subscription content businesses, and everything in between. Pipe’s clients are small businesses with as little as $100k in ARR all the way up to publicly traded companies that make hundreds of millions in ARR. If your business makes recurring revenue, whether it’s venture-backed, bootstrapped, or public - chances are, Pipe can help you raise cheaper capital faster.If that sounds like your business and you want to give it a try: I only write deep dives about companies that I think can help your business. MainStreet, for example, has gotten Not Boring readers nearly $1 million back from the government already. But I also only write about companies that I think are fascinating to learn about. I’ve been excited about Pipe since long before Harry approached me about working together because of its potential to solve one of the biggest problems facing startups. Business-Funding FitFor such an innovative, smart group of people, startup founders all fund their businesses pretty much the same way they’ve been funding them

Software is Eating the Markets (Audio)

Welcome to the 574 newly Not Boring people who have joined us since the last email! If you’re reading this but haven’t subscribed, join 18,613 smart, curious folks by subscribing here!Hi friends 👋 ,Happy Monday!Not Boring straddles two worlds - technology and finance. I try to bring pro-level insights to a consumer audience. Today’s essay is about what happens when those things start to blur, when technology alters finance and consumers play a larger role in shaping the markets.It’s an early exploration of a topic that I’ll be writing a lot more about in the months and years ahead, putting thoughts down on paper so that we can debate and stress-test them together. I’d love to hear your thoughts in the comments.But first, a word from our sponsor:Today's Not Boring is brought to you by…Seemingly everyone is talking about how next week’s elections will impact the markets and their investments. The fear makes sense -- historical data shows US presidential elections tend to make investors more conservative. Even my most risk-seeking, SPAC-loving friend told me that he’s going to cash until after the election. But knowledge is better than fear: do markets perform better in Democratic or Republican administrations? And most importantly, is there an ideal investment strategy during an election season?Weathering financial uncertainty during this election is crucial for long-term financial success. Yet, it can be challenging to find a go-to source for trustworthy and unbiased insights. That’s where Zoe Financial comes in.Read Zoe Financial’s Top 5 Investment Impacts of US Presidential Elections Here:Software is Eating the MarketsIn 2011, Netscape and a16z founder, Marc Andreesen, wrote a guest post in the WSJ titled Why Software Is Eating the World. With nine years of hindsight, he was so obviously right that it’s cliché to cite it today. I’m kind of mad at myself for typing these words right now. Software has fundamentally altered nearly every industry. Netflix put a dent in cable’s long standing dominance, and already TikTok and Fortnite threaten Netflix. Newspapers are dying. Millions of people now earn livings in the Gig Economy or the Passion Economy. A private company, SpaceX, is doing things that NASA can’t. The list goes on. But despite that, we operate under the assumption that financial markets are somehow different, impervious. Of course, technology has impacted finance. High-speed trading accounts for an increasingly large percentage of activity, and institutional investors will spend millions or billions on any tech that gets them a slight advantage. But if recent tech history is a guide, technology’s ultimate impact on finance will be less about further entrenching incumbents; it will empower consumers. Consumers are participating directly in the market in greater numbers than ever before, but every analysis I’ve read treats increased retail participation as a temporary COVID-induced blip, and retail traders as irresponsible and irrational gamblers just looking to have a good time. Soon, serious people argue, things will go back to the way they were.They may be right. But what if they’re not? Investing in Social StatusIn November, back when San Francisco was still more physical place than state of mind and most people associated Corona with lime, Alex Danco wrote an excellent post called The Social Subsidy of Angel Investing. In it, he argued three main points: * Angel Investors in the Bay Area don’t just invest for the financial returns; they also invest for the social returns. * The social rewards of angel investing solve an important chicken-and-egg problem in early stage fundraising that financial rewards do not.* The social returns to angel investing have a strong geographical network effect, because they require a threshold density in order to kick in.In San Francisco, owning a Ferrari wasn’t nearly as cool as owning pre-seed shares in Stripe or Uber. In some ways, startup equity behaved more like a Veblen Good -- one that paradoxically sees more demand as the price goes up -- than like an investment. How else to explain the mad dash to invest in Clubhouse at any price? A high price signaled a more competitive round, which meant more social status for getting in.To an outsider, this might seem crazy. Why invest your hard-earned money in something that doesn’t provide the best risk-adjusted returns? When angel investors wrote checks into startups, they were really buying two things: an asset with a potential financial return and a status symbol. As usual, Danco was prescient, but he couldn’t have predicted what happened in the year since his post. Since the beginning of the COVID pandemic in the US in March, the economy is struggling, consumers are buying fewer things, and millions are unemployed. And yet, the stock market hovers near all-time highs. People are spending less on services and luxury items, and investing more.There is no one way to explain everything that’s been going on, but there a

Reliance's Next Act (Audio)

Welcome to the 805 newly Not Boring people who have joined us since the last email! If you’re reading this but haven’t subscribed, join 18,038 smart, curious folks by subscribing here!💙 Hit the heart at the top to like today’s essay, and if you really love it, share it!Hi friends 👋 ,Happy Monday! I suspect that most of the people reading this newsletter could recite the Facebook, Apple, Amazon, Microsoft, and Google (FAAMG) stories by heart. The American tech giants are widely covered, and rightfully so: they’re the biggest companies in the world, and they’re growing really fast. These companies do everything, vertically integrating and acquiring competitive threats on the path to market dominance.But there’s a new breed of tech leader emerging in Asia, led by Tencent, Alibaba, and SoftBank, that turn their first acts as product-first companies into second acts as investors. By spreading out their bets, Tencent and Alibaba have made themselves future-proof: they have upside whether customers choose their products or new entrants’, because they own large stakes in the most promising startups. (SoftBank… we’ll see, but I’m bullish.)Currently, Reliance is taking the western approach, but I think it would do well to follow its Asian neighbors’ lead. The opportunity is just too large for anyone, even Mukesh Ambani, to take on all by themself. I’ll explain. But first, a word from our sponsor:This week's Not Boring is brought to you by… Every Monday after I hit send, Public is the first place I go. Public makes investing social, which means different things for different people. For me, as an eternal optimist, I value having a positive environment in which people smarter than me can challenge my thinking and point out bear cases that my mind just chooses not to see. After two weeks of writing about Reliance, I couldn't be more bullish on India or on Reliance itself, so it's the perfect time for some friendly pushback and thought-sharpening. I’ll be discussing today’s essay - including my thoughts on Tencent and SoftBank - and asking people for the bear case on India and Reliance. Join me. *This is not investment advice. See Public.com/disclosures/.Reliance’s Next Act The Cricket Proxy WarOutside of Philly and Duke sports, my favorite sports team in the world is the Mumbai Indians, the Indian Premier League cricket team owned by the Ambani family. If you don’t follow cricket, I highly recommend the Netflix series, Cricket Fever: Mumbai Indians as your gateway. After watching the Indian team in the Cricket World Cup every four years, last year was the first year that Puja and I watched the Indians religiously. We got a Willow subscription and woke up at odd hours to lock in for four hours of high-paced T20 cricket. Every match, in the corner of the screen, we saw this logo: The Indian Premier League’s logo looks a lot like the league logos westerners are used to seeing -- a silhouette of someone playing the sport with three letters -- with one difference: a title sponsor. In 2019, that title sponsor was Vivo, a Chinese smartphone company. This year, when the crowdless 2020 IPL season started in Dubai, we noticed a different logo. Vivo signed a deal to sponsor the IPL through 2022, but amidst the China-India conflicts, India’s cricket board dropped it in favor of a homegrown sponsor. Dream11, the $2.5 billion Indian fantasy cricket startup, took its place. China was out. India was in. Atmanirbhar Bharat. Uncharacteristically, Reliance took a backseat on the title sponsorship, but its influence is there, just spread out. Jio is the only company that sponsors all eight IPL teams. Its patch sits prominently on six teams’ jerseys. It’s just cricket, but when I look at that chain of events, I see Reliance’s future. China’s disappearance from the IPL and Jio’s multiple bets point to Reliance’s opportunity and the approach it should take in the Indian startup ecosystem. Reliance’s FutureReliance has a history of vertically integrating, but paradoxically, to capture the most value from the internet, it needs to loosen its grip. Instead of doing everything itself, Reliance should become India’s biggest growth stage investor. Last Monday, in Reliance: Gateway of India, we covered Reliance’s history and present. Reliance is a sprawling giant that spins cash flow from its legacy businesses into a tech-forward future:* India’s Biggest Company. $202 billion market cap on revenues of $105 billion* New Focus. Reliance Retail and Jio, make up 30% of revenue ($31 billion) but took up the lion’s share of the screen time at the company’s most recent AGM (84%).* Reliance Playbook. Undertake projects with high upfront costs, building complex businesses around them, wrangling Indian supply and demand, spreading out the costs over hundreds of millions of users, leveraging its favorable position with the government, and selling stakes to foreign companies and investors. * Gateway of India. Foreign companies and investors poured $20.4 billi

Reliance: Gateway of India (Audio)

Welcome to the 1,034 newly Not Boring people who have joined us since the last email! If you’re reading this but haven’t subscribed, join 17,234 smart, curious folks by subscribing here!Hi friends 👋 ,Happy Monday! This is my first Not Boring as a dad, and we are absolutely loving it (although please forgive me if there are sections in which it seems like my brain is mush — it is.)The timing worked out perfectly for this week’s topic. A couple of weeks ago, I asked people on Twitter for their favorite international companies that not enough people know about. The topic of today’s Not Boring, Reliance, was among the most popular answers. So for my first essay as a father to a half-Indian son, I get to tell the story of India’s most important company. But first, a word from our sponsor: This week's Not Boring is brought to you by… As we'll discuss today, Reliance democratized investing in India back in 1977 when it went public at ₹10/share. The low price gave everyone a chance to own a little piece of a public company, and its strong performance since has generated huge returns for regular investors. Today, Public is democratizing investing by making the stock market social. It's the place where newcomers and experienced investors alike come to discuss their favorite companies and market trends. And it keeps getting better. Just last week, my favorite pseudonymous FinTwit account, Ramp Capital, joined Public.I’ll be discussing today’s essay over on Public, and can't wait to talk about the surge of Indian IPOs on US exchanges over the next year on there. Join me. *This is not investment advice. See Public.com/disclosures/. So throw on some A.R. Rahman…and chalo! Reliance: Gateway of IndiaIn Mumbai, a short walk from Leopold Cafe and across the street from the Taj Hotel, where Puja’s parents were married, a large stone arch-monument called Gateway of India sits between the city and the Arabian Sea. The British commissioned Gateway of India in 1911 to commemorate the landing of King-Emperor George V and Queen-Empress Mary, the first British monarchs to visit India. After Indian Independence from Britain in 1947, the last British soldiers left India through the very same gate. Today, that structure is largely a tourist destination. The real Gateway of India, as far as foreign companies and investors are concerned, is Reliance Industries.Atmanirbhar BharatSince I started writing Not Boring, one type of company has fascinated me more than any other: the Asian tech conglomerate.Japan’s SoftBank, led by Masayoshi Son, distorted both the private and public markets through its Vision Fund and 555 Fund investments. Masa has been reinventing his company since the ‘80s; today, it’s more investor than operator. The 2010s were China’s decade. Tencent and Alibaba, with a combined market cap of $1.4 trillion, are now household names in the kinds of households that read Not Boring. They’ve parlayed strong core businesses into unparalleled global equity portfolios.The 2020s will be India’s decade. And unlike China, which features a fierce competition at the top between Tencent and Alibaba, in India, Reliance is the main game in town. Reliance Industries Ltd (“Reliance” or “RIL”) is like an India-focused Exxon, Dow Chemical, Walmart, AT&T, and Comcast all rolled into one. If it fulfills its Jio vision, it will add Shopify, DoorDash, Zoom, WeChat, Square, AWS, and more to that roll. Its $200 billion market cap is the largest in India, where its backstory, leaders, products, and dramas are well-known. But when I asked a bunch of smart non-Indian friends what they knew about Reliance, they replied, “Who?” I salivated. Nothing gets me jazzed like an under-discussed Asian tech conglomerate. At RIL’s helm is Mukesh Ambani, one of company founder Dhirubhai Ambani’s two sons. Mukesh is the richest person in Asia and the sixth richest person in the world, with a net worth of $85 billion. His house is worth more than whole small cap companies.Under Dhirubhai, the company was a dominant force in domestic Indian business and politics for nearly thirty years. Under Mukesh, particularly since the start of Coronavirus, it is making a dramatic push into the western consciousness.This summer, Reliance made waves by selling 33% of its Jio Platforms business for $20.4 billion to a who’s who of international strategic and financial investors, from Facebook to KKR to Mubadala. Over the past three weeks, Reliance has been at it again, selling stakes in its Reliance Retail business to many of Jio’s financial investors, with a potential Amazon investment waiting in the wings. It’s no surprise that the world’s largest companies, investors, and sovereigns want a piece. India is the world’s most important growth story, and Reliance is its gateway.Now, I might be biased on the India front. Last week, I became a dad to a half-Indian son, and this is a picture of me at my wedding: So caveat emptor. But I’m in good company. When many of the world’s smartest i

Fundrise (Audio)

If you’re listening but haven’t subscribed, join 16,497 smart, curious folks by subscribing!Hi friends 👋,Happy Thursday! As I’ve started to monetize Not Boring, I’ve been very pleasantly surprised by the companies that want to tell you their stories. I thought I was going to need to take bold stands and say no to advertisers whose products I don’t believe in, but I’ve noticed something cool happening. All of the sponsors that I’ve worked with are Not Boring readers, they understand the things that I’m excited about, and they realize that if you’re reading Not Boring, you’ll probably be excited about them too. They see their products in the trends and ideas we discuss, and reach out because they recognize the alignment. These are companies I’m genuinely bullish on, and I can’t believe they pay me to tell you about them. A couple of weeks ago, I told you about MainStreet, a company that literally gives startups free money. As a result of that post, Not Boring readers are getting over $900k back from the government this year. Today, I’m writing about Fundrise, a pioneer in the “everyone is an investor” space and one of the smartest, easiest ways to add real estate to your portfolio. When I wrote about MainStreet, I mentioned that it was a CPA deal, meaning that I got paid when people signed up and saved money, and that I would call out when I was doing which type of deal. Fundrise is paying me a flat fee and I don't receive any additional compensation from you signing up for the platform.Let’s get to it. Fundrise & the Magic of DiversificationLast week, I ended my piece on Opendoor talking about my desire for new ways to invest in real estate and make the asset class more liquid and accessible. It’s been under my nose this whole time: Fundrise. Fundrise gives retail investors access to institutional quality real estate investments without high fees and with transparency around the performance of your investments. Having worked in real estate tech, I’ve known about Fundrise for a while, but my conception of the company was based on its earliest model in which Fundrise crowdsourced investments on a property-by-property basis. It was one of the first companies to use crowdfunding for real estate, but it’s evolved since then. Over the past few years, Fundrise has overhauled the model to run more like a traditional real estate private equity fund, but funded entirely by its individual investors, who invest around $8,000 on average. But that doesn’t mean Fundrise itself is small. To date, since its founding in 2012, Fundrise has invested in $4.9 billion worth of real estate, to great success. Since 2014, its platform’s average annualized returns ranged from 8.76% in 2016 to as high as 12.42% in 2015. Last year, it returned 9.47%. What’s really fascinating is that not only are the real estate funds backed largely by individual investors; the majority of the company itself is funded by those same investors. That means that Fundrise can play the long game, and avoid the trade-off between growing quickly and charging high fees to make venture investors happy, and investing patiently with low fees to make its fund investors, who also back the company, happy. So how does it do it? Fundrise is one of a growing list of companies that takes advantage of Reg A+ to democratize investment in asset classes that were previously unavailable to all but the wealthiest few. As I wrote about in Secure the BaaG on Monday, companies like Fundrise give everyone access to similar investment opportunities that professional investors and the ultra-wealthy have access to, and allow us to build diversified portfolios that generate better risk-adjusted returns than going all in on NKLA calls. If you’ve been wanting to invest in real estate but didn’t want to buy and manage a portfolio yourself, or pay the high fees associated with real estate private equity, you can check out Fundrise now:But, as always, this is all about learning, so we’ll cover: * The importance of diversification into alternative assets like real estate* What makes Fundrise different than traditional approachesWhy Invest in Real Estate? DiversificationTwitter is the best. A few days after my Opendoor piece, I was scrolling the tweets and came across this one from the SPAC King, Chamath Palihapitiya, the same guy who took Opendoor public: Chamath pointed out that in a low interest rate environment, the traditionally suggested 60/40 Stocks/Bonds mix no longer makes sense. While many in his replies pointed out that because of the way bonds trade, you can still generate strong returns on bonds if you know what you’re doing, his larger point stands. The traditional way of building a portfolio doesn’t make as much sense as it used to. Today, retail investors have access to a larger universe of options than we did before, and investing in uncorrelated assets creates better risk-adjusted returns than investing only in stocks. In his seminal paper on the topic, “Engineering Targete

Secure the BaaG (Audio)

Welcome to the 1,018 newly Not Boring people who have joined us since last Monday! If you’re reading this but haven’t subscribed, join 16,200 smart, curious folks by subscribing here!This week’s Not Boring is brought to you by…As you’ll read today, one of my most strongly-held beliefs is that we are in the earliest innings of a movement towards more accessible, democratized investing across all asset classes. The lines between finance, gaming, media, and social are only going to get blurrier from here. Saying “I don’t really follow the markets” is no longer an option. But it can also be hard to understand where to start, and to build up a portfolio in a responsible way. That’s where Public comes in. Public makes the stock market social by letting you buy and discuss stocks and the companies behind them with thousands of smart, curious people. I’ll be discussing today’s essay and the companies behind the trend over on Public. Join me. Hi friends 👋,Happy Monday! I read a lot -- from sci-fi to 10-Ks to Twitter -- and a bunch of seemingly disconnected ideas float around in my head and interact with each other and sometimes form the fuzzy outline of something that I can’t quite clearly articulate but that feels important to explore. Occasionally, I’ll try to put some of these concepts into words. Today is one of those days. Today’s essay isn’t meant to be the final or complete picture, but a starting point and a way to shake up our collective brains and see what insights fall out. So throw on some Daft Punk… … and let’s get weird. Secure the BaaGLife Imitates Sci-FiWould it be possible to run a real business in a way that feels like playing a video game?This question has been swimming around in my head for the past few weeks, probably because I’ve been reading too much sci-fi.Before it was a terrible movie, Ender’s Game was one of my favorite books. You should read it, but here’s the plot: A talented six-year-old kid and two-time murderer named Ender goes to Battle School to train to fight an alien enemy known as “Buggers.” He excels and advances through the tests rapidly. For his final test, a war hero named Mazer Rackham puts Ender through a simulation, first solo and then in command of his classmates, in which his fleet is surrounded by Buggers protecting their Queen’s planet. Ender decides to blow up the planet and wins the simulation, only to find out that he was fighting the real war all along. That stuck with me since I first read the book twenty years ago. Imagine thinking you were playing a game only to discover that you were commanding armies of real people. Treating war as a video game abstracted away a lot of things -- pressure, moral complexity, fear, individual people -- and turned it into a game that a ten-year-old could win.Orson Scott Card wrote Ender’s Game in 1985, the same year that Nintendo released Super Mario Bros. on the original Nintendo Entertainment System. When the most advanced video game system was 8-bit, single-player, and 2D, it wasn’t obvious that video game skills would translate to battlefield success. But thirty-four years later, in 2019, the US Army began actively recruiting video gamers. It even put together an all-Army esports team to compete in Call of Duty, Fortnite, and League of Legends tournaments across the country. As war-based Massively Multiplayer Online Games (MMOGs) become more realistic and war is increasingly fought via drones, the skills required to be good at each are converging. Business has a history of following defense. Many of the once-advanced technologies that underpin the economy today, from the internet to GPS, computers to digital cameras, were first developed for the military before being commercialized by private industry. Just as Ender’s Game predicted video games’ growing importance in war way back in 1985, Daniel Suarez’s Daemon novels described a future in which an artificial intelligence runs the economy by controlling humans like video game characters. You should read that one, too, but here’s the PacksNotes: When video game developer Matthew Sobol dies, he unleashes a computer program, the Daemon, on the world. It infiltrates the computer systems of major corporations and governments, crippling them, while simultaneously coordinating the actions of Daemon-sympathetic humans on the Darknet, an Augmented Reality layer that turns the physical world into a video game. By incentivizing humans with points, status, and credits, the Daemon turns civilization into a video game and rebuilds a new economy from the ground up. Today, three trends are converging to make a version of Suarez’s predictions possible: * Video Games are Eating the World. Video games are worth more than the film industry already, and games are spawning thriving virtual economies.* Business-in-a-Box (BiaB). Software is replacing more pieces of every industry’s value chain, and making it easier to operate businesses at higher levels of abstraction.* Everyone is an Investor. As m

Opendoor: The Amazon of Housing (Audio)

Welcome to the 805 newly Not Boring people who have joined us since last Monday! If you’re reading this but haven’t subscribed, join 15,182 smart, curious folks by subscribing here!Hi friends 👋,Happy Monday! It’s hard to avoid SPACs. Everyone has one, Nikola is looking more and more like a fraud, and Chamath just launched three more. It’s easy to dismiss SPACs as a fad and the companies that they take public as immature, risky, and dangerous. But great companies can go public via SPAC, too, and they increasingly will. When we find one of those, it’s worth doing our homework, which is what today is all about.But first, a word from our Sponsor.Today’s Not Boring is brought to you by… In early June, I wrote: A startup called Public, backed by top VCs like Accel and Greycroft and celebrities and athletes including Will Smith and JJ Watt, built a product that makes investing social and community-forward, allowing people to build followings based on their investing acumen.I don’t know about my investing acumen, time will tell, but I know that we’ll make smarter decisions if we’re able to sharpen our ideas on each other. Like today, for example. Whether you’re bullish on $IPOB, bearish on it, or still figuring it out, I want to hear your opinion, so I’ll be posting and discussing on Public and would love to hear your thoughts over there. You can join the conversation whether or not you buy a single share… although everything is more fun with some skin in the game. (This is NOT investment advice, just an observation 😎) Now let’s get to it… Knock Knock. Who’s There? Opendoor.Home is Where the Startups Aren’tHomes are emotional. Puja and I are having our first kid, a son, in less than a month. We spent this Saturday cleaning up my parents’ house and getting rid of old junk that we hadn’t used for years to make space for all of the new stuff the little guy will need whenever we come visit. As with any cleaning project, we started by emptying one closet and decided to throw out twenty-plus years’ worth of trash and memories from around the house. As we emptied closets we hadn’t opened in years, my mom came up with reasons we should keep that old empty picture frame or half-used can of WD-40, told us that we should just dry clean the sleeping bag we bought in 1998 in case we might want to use it at some point in the future. None of it is rational, but it’s not unique either. Mari Kondo has made a fortune convincing people to let go of things that once held importance but no longer do. And that’s just the stuff. You would have to pry us out of the house itself. Maybe that’s why housing is one of the last major categories that technology has left alone. Sure, companies have tried. Tons of them. The startup graveyard is filled with companies led by entrepreneurs who realized that the way we buy and sell homes sucks, but couldn’t ultimately figure out how to change it. They weren’t thinking big or long-term enough. The companies that have made the biggest impact, like Zillow and Redfin, make it easier to search for houses, but then kick buyers over to agents to go through the offline process, the same way it’s always been done. There’s this Startup Lindy Effect at play in real estate. If the future life expectancy of something is proportional to its current age, and real estate has survived practically unchanged by technology longer than any other industry, then maybe the way it is is the best we can do. That’s why most people’s reaction to a company like Opendoor is, “Cool idea. Won’t actually work.” Opendoor, founded in 2013, lets people transact real estate at the click of a button. It promises to transform a process that has traditionally been “Complex, Uncertain, and Slow” into one that is “Simple, Certain, and Fast” by using technology to make instant offers on homes. At least one person sees the vision. Last Tuesday, Chamath Palihapitiya announced that his SPAC, Social Capital Hedosophia II (IPOB) is merging with Opendoor to take it public at a $4.8 billion valuation.(For a refresher on how SPACs work, check out Juul: The SPAC 2020 Deserves.)So now, without the months of preparation and detailed S-1 that the traditional IPO offers, the question shifts from, “Could Opendoor work?” to “Should I invest in Opendoor?”My gut reaction to that question was a resounding “NO.” There are three things that companies say that make me want to run away as fast as I can:* The Shark Tank Market Sizing. “X thing is a $y billion market! If we get just z%, we’ll be a multi-billion dollar business!” Stop. If anyone in a given industry can say something, it’s not an advantage. * Capital as a Moat. We talked about this in Masa Madness, but the idea of capital as a moat -- raising more money than competitors and spending it to achieve a dominant position -- has been disproven multiple times in SoftBank’s portfolio alone. * “We’re Like Amazon.” This is my favorite. If there’s a business out there that’s losing money, chances are, they’ve s

MainStreet (Audio)

Welcome to the 886 newly Not Boring people who have joined us since Thursday! If you’re reading this but haven’t subscribed, join 14,729 smart, curious folks by subscribing here!Today’s Not Boring is brought to you by…Read on and I’ll tell you how they can send your startup $50k tomorrow.Hi friends 👋,Happy Thursday! This little newsletter and our band of smart, curious people just keeps growing. There are a lot of new folks joining Not Boring every week, which has not yet ceased to be exhilarating. I don’t think it will. Because there are so many new faces, I want to give a quick reminder of what the weekly schedule looks like, specifically what I’m doing with Thursdays.Every Monday, I write a deep dive on a large (and typically public) company. The past few weeks, I’ve written about Twitter, Tencent (x2), Stripe, SoftBank, and Zoom. This upcoming Monday, I’m writing about… 🤫Thursdays are more experimental, and typically focused on smaller companies. Recently, I’ve written Not Boring Investment Memos on OZE and Swaypay, and I plan to do about one deal per month through the Not Boring Syndicate. Sometimes, I have guests come on to teach us about something I don’t know much about, like the Magnolia empire or Ringtones. And sometimes, I go behind the scenes to write about how I’m growing and monetizing Not Boring. Thursdays are Wild Cards. And today, I’m trying something new: a Sponsored Writeup. I want to tell you a little bit about how it works for a couple reasons:* In case other people are figuring out how to monetize their small media business or creative project.* So that we go into this eyes wide open. I need to make money to keep Not Boring going as my full-time thing, and I want to do it as transparently as possible. A few weeks ago, I sent you all an email asking me to tell me about yourselves so that I could figure out how to make money with Not Boring and let potential sponsors know who reads it. The results are in, and you’re an impressive bunch. I put together a Sponsor Deck with some of the stats and rates. You can check it out here.I decided to go the sponsored route so that I can:* Keep it free for everyone. I think newsletters are an incredible way to democratize knowledge. * Keep growing. I put too much damn time into writing each of these to only send to a small group of people. There are broadly two ways that I can make money from sponsorships: * Cost Per Impression (CPM): A company pays me to get its message in front of this group of smart, curious people based on how many people read it, and regardless of whether anyone clicks the button to learn more or sign up or buy. Most of the sponsorships will be CPM. * Cost Per Acquisition (CPA): A company pays me a certain amount for each person who signs up, subscribes to, or buys its product. For example, if I did a deal with Fictional Shirt Company at $100 CPA, and 90 of you bought shirts after clicking my link, Fictional Shirt Company would pay me $9,000. I’ll do these less often. Typically, CPM deals make more sense because there’s value to a company in getting in front of you even if you don’t buy immediately. There’s an idea in marketing that someone needs to see a product seven times before buying, and while the number might not be exactly seven, it’s rarely one. I’m certainly not going to put on a hard enough sell to bring that number down. I’d rather just expose you to products and companies I like (and often use myself), and if you’re interested, great! Sometimes, though, CPA deals just make sense. After I sent the survey out, and before I made the deck, Nick Abouzeid reached out to me. Nick worked at Product Hunt, AngelList, and was most recently a VC at Shrug Capital. He told me that he was leaving Shrug -- a dream job -- to go work for one of their portfolio companies, that he was interested in sponsoring Not Boring, and that we should chat. When we talked, Nick said that he was going to MainStreet because as one of their investors, he had so much fun telling the people about the product that he wanted to go do it full-time. He offered me a choice: CPM (at the rate I was asking for) or CPA. I chose CPA, because I agree with Nick. In telling you about MainStreet, I’m making money by giving you free money.MainStreet is relevant for both startups and investors: * Startups: MainStreet will get you a bunch of money the government owes you.* Investors: MainStreet is the type of unsexy but practical AI application that will create investment opportunities for years before the machines start turning us into paperclips. Main Street: Free Money for StartupsI’m not going to bury the lede. If you’re a startup, MainStreet will make you money. Here’s how:* You sign up and connect your payroll system. * MainStreet finds tax credits and incentives that apply to your business.* MainStreet sends you money now. You don’t need to wait until April. * MainStreet makes money by keeping 20% of the money the government pays you. If you don’t get anything,

Zoom's Blank Check (Audio)

Welcome to the 870 newly Not Boring people who have joined us since last Tuesday! If you’re reading this but haven’t subscribed, join 14,377 smart, curious folks by subscribing here!Hi friends 👋,Happy Monday! I hope all of you had a great weekend and got to spend some time away from Zoom. It’s Monday now, though, and Mondays mean Zoom.Because we all live and work on Zoom, everyone talks about it. We talk about Zoom fatigue, sure, but we also talk about how expensive Zoom’s stock is and whether or not it has any moats that will protect the business after COVID passes and competitors catch up. What we don’t talk about as much is what the company should do about it. Today, we’re going to change that with the first Not Boring Case Study. But first, a word from our sponsor. Today’s Not Boring is brought to you by… BarrelLast year, when people still gathered in person, I went to a Write of Passage meetup in NYC. I spent most of the night talking to a couple of people, one of whom was (and still is) Peter Kang. Peter told me that he ran a creative and digital marketing agency called Barrel. Said it was doing well, didn’t brag. Then I got home and looked it up. Peter was being humble. Barrel is a 32-person team of designers, developers, strategists, and producers who have worked with clients like Barry’s, Dr.Jart+, Bare Snacks, ScottsMiracle-Gro, Rowing Blazers and many more to build their Shopify sites and marketing strategies across email, paid, and SEO.You know how I feel about companies forking their dollars straight over to Google and Facebook with shitty creative and unoptimized campaigns. Please don’t do that. Work with Peter and the Barrel team. Now let’s get to it.Zoom’s Blank CheckYou Think You Know ZoomZoom has grown spectacularly during COVID. It is the best video conferencing software on the market and is perfectly designed for viral growth. Its numbers are mind-blowing, and it deserves to be one of the best performing stocks in the world.Having said that… $ZM (the stock) is also incredibly expensive. Worse, many, yours truly included, worry that Zoom has no moat. It me ^^No moat means that Zoom is open to attack from all angles. * Google can increase the size of the Meet button until it takes up the whole calendar.* Microsoft can do the Microsoft thing and bundle video with Teams.* A wave of startups can come in and pick off verticals. At best, the argument goes, Zoom will have to lower prices to retain customers. At worst, it will lose them to free, bundled, or more use case-specific competitors. Easy come, easy go. But I’m coming around on Zoom’s long-term prospects, if it makes the right moves in the coming months, because I think it may have stumbled into a truly brilliant strategy. Before we get there, though, we’re going to start with a case study. Today, you’re Zoom’s CEO, Eric Yuan. * Your company has put up historic numbers because of your single-minded focus on the customer and your product’s quality and virality.* Competitors are coming at you from all sides, and you’re easy to attack because you haven’t built moats around your business. * Your stock is expensive by any measure.I’m going to ask you to give me your ideas after the case study before giving you mine. Here’s the question you need to answer: What do you, as Zoom’s CEO, do to maximize long-term shareholder value? Zoom Case StudyZoom’s Unprecedented AscentYou’re all familiar with Zoom the product at this point in the quarantine, but you might not know as much about Zoom the company. Compared to my recent profiles on Tencent and SoftBank, the Zoom story is dead simple, because the company has focused on customer happiness through product and engineering to the exclusion of almost everything else. In 1995, a Chinese engineer named Eric Yuan went to Japan to see Bill Gates speak. He was so inspired that he decided then and there to move to Silicon Valley. He applied for his H1-B visa and was denied eight times before the US granted him a visa on his ninth attempt. When he arrived in the States, he went to work for an early video conferencing software company, WebEx, where he served as a founding engineer then VP of Engineering for nine years. The company IPO’d in 2000 and Cisco acquired it six years later for $3.2 billion in cash. He stayed on at Cisco in the same role for four years, but became increasingly unhappy. As he explained to Bessemer partner Byron Deeter: Every time I talked to a WebEx customer, I felt very embarrassed, because I did not speak with a single happy WebEx customer.He realized small tweaks wouldn’t fix WebEx, so he pitched the Cisco execs on rebuilding it from the ground up. When he failed to convince his new bosses, he left to start his own thing. After leaving WebEx, according to the Acquired podcast, “a whole cadre or basically anyone who had ever worked with Eric immediately gives him money, just blank check, to back him to work on whatever he’s going to do.” He started building SASB, a consumer applicati

Swaypay: Not Boring Memo (Audio)

Welcome to the 890 newly Not Boring people who have joined us since Monday! If you’re listening to this but haven’t subscribed, join 13,842 smart, curious folks by subscribing here!Hi friends 👋,Happy Thursday! We have a little early Fall treat: the first-ever-back-to-back Not Boring Investment Memo. This one has a little something for everyone: * Angel Investors: A high-potential ecommerce software play that I think can become an important piece of the Modern DTC Value Chain.* Ecommerce People: A better checkout experience that helps your customers share your product, increases conversion, and lowers CAC.* Business Nerds (all of us): A look at an early stage company and an explanation of alternative payments and the Google/Facebook duopoly.They’re longer than a typical investment memo — which you’ve probably come to expect from me at this point. That’s because I want everyone to come away with some new knowledge and a little glimpse into the future courtesy of the stories of the founders who are shaping it. And if you’d like to invest too, great. Today’s Not Boring is brought to you by… TrendsThere are a few things I love more than anything else besides my family and friends: business deep dives and notebooks. Not kidding. Told Sumeet about my obsession here. Of course, Trends went ahead and did a deep dive on all the notebook companies (think Moleskin) this week. They just keep dropping business content that feels like it’s made for me, and they’re giving Not Boring readers a $1 trial to see if it’s made for you, too. No risk, high reward. Plus, when you sign up, you help keep Not Boring free. Try it out:Now let’s get to it.Not Boring Investment Memo: SwaypayMeet SwaypayWhether you like it or not, you’re an influencer. Every time you post a pic in your new kicks or answer the question, “Where’d you buy that dress?!” you’re influencing people’s purchasing decisions. Because it’s historically been hard to wrangle, track, and direct small amounts of influence, until now, you’ve done it out of the kindness of your heart. That’s very nice of you, but it causes a couple problems: * You don’t get any value from your influence other than nebulous social capital. * Brands are forced to pay Facebook and Google to acquire customers. As a result, according to reformed VC Chamath Palihapitiya, “Startups spend almost 40 cents of every VC dollar on Google, Facebook, and Amazon.”Swaypay wants retailers to pay you instead of paying Google, Facebook, and Amazon. Its mission is to bring financial empowerment back to retailers and shoppers alike by rerouting the billions of advertisement dollars back into shoppers' pockets as savings directly at the point of sale. When Swaypay’s CEO, Kaeya Majmundar, first walked me through the deck, I wrote in my notes, “Fucking love this mission.” I also love the investment, for five reasons: * The Product is Already Magical. Swaypay already makes good on its promise of a frictionless experience. I went from homepage to discount to checkout in 15 seconds.* Ecommerce is Growing. This is a recurring theme here at Not Boring, because the shift towards ecommerce is massive. Swaypay is well-positioned to ride the wave.* Strong Early Traction. After a successful beta, Swaypay has 60 retailers on board for its Q4 launch and is targeting 200-300 by end of year.* Swaypay is Ecommerce Robinhood. I believe that anything that takes money from Facebook and Google and gives it to shoppers and retailers will win. * Kaeya and Team. Kaeya has been in ecommerce since going on Shark Tank at 19 (video below, of course) and has been on both the seller and platform sides. She’s building a high-quality team with super relevant experience.Product: Frictionless Savings for SharingSwaypay is the first payment method that plugs into eCommerce storefronts and lets shoppers convert their “sway,” or social influence into currency for online purchases. Swaypay believes that there is tremendous untapped value in bringing influencer marketing downstream to the 99% of people who have small amounts of powerful social capital, or sway, that they have not been able to exercise. To make the long-tail viable requires clear value and a frictionless experience. That’s what Swaypay is building: * Clear Value: Discount on items shoppers are buying anyway based on sway. * Frictionless: Discount applied via Swaypay checkout button in the checkout flow. The product is dead simple. Shoppers shop online like normal and when they get to the checkout page, they’re presented with the Swaypay Checkout button next to the regular checkout button. When a shopper clicks the button, they’re prompted to enter their Instagram handle, and given a discount based on their sway. The shopper checks out, the discount is applied automatically, and they have 30 days to post on Instagram and share the link through Swaypay or they have to pay back the difference. You know what, let me just show you. Let’s say I was planning on having a few too many drinks t

Masa Madness (Audio)

Welcome to the 1,301 newly Not Boring people who have joined us since last Monday! If you’re reading this but haven’t subscribed, join 13,507 smart, curious folks by subscribing here!Hi friends 👋,Happy Tuesday! I hope you enjoyed the Labor Day Weekend. In case last week seems oh so long ago, a little refresher: tech stocks were on an all-time tear until Thursday, when the music stopped and prices tumbled. The Financial Times did some digging and discovered that an old Not Boring favorite was behind the market’s rise and fall. That’s right… SoftBank is at it again. Brought to you by… Teachable: Share What You Know SummitFun fact: I started this newsletter in May 2019 as an assignment for an online writing course I was taking. That course was built on my favorite Passion Economy platform: Teachable. Smart people have made over $850 million teaching what they know in courses built on Teachable, and in two weeks, the company is hosting a three-day Summit to share everything that successful creators — including Not Boring favorites Li Jin, Tiago Forte, and Ankur Nagpal — have learned about turning their knowledge into money. I’ll be there taking notes.Tickets are $29 this week, and going up to $39 on Friday, so get in now. If you want to start or grow an online or content-based business, this will pay for itself thousands of times over.Now let’s get to it.Masa MadnessBefore I wrote this newsletter, I worked for a company called Breather, where part of my job was running our real estate team. We were responsible for finding and negotiating leases on office spaces that we would design, build, and rent out to clients for shorter time periods. As we moved upmarket (longer rentals in bigger spaces), we increasingly competed with WeWork for both spaces and clients. It sucked.Every space we looked at, WeWork looked at. For a space that would typically cost $65/sf, they would offer $70/sf. When brokers brought WeWork potential customers, they would pay up to 100% of one year’s rent as a commission. If a customer asked for an expensive buildout, they would do it. Different WeWork locations would even compete with each other for the same customer by offering lower prices.We ran our underwriting model to understand if we could do the same things that they could to acquire spaces or customers, and we couldn’t figure out how to make the numbers work. Because they didn’t. And they didn’t have to. Because WeWork was backed by SoftBank. Dunking on SoftBank became de rigueur when the market realized what all of us in the industry already knew - that WeWork’s unit economics were terrible because they were trying to use capital as their moat. And it wasn’t just WeWork. Wag. Brandless. Katerra. Uber. Compass. Bloomberg called SoftBank “the Pied Piper of Unicorns” as it lured startups to giant pools of money in which they drowned.After WeWork’s downfall, the man behind the madness, Softbank CEO Masayoshi Son, or Masa, admitted that maybe he’d made some mistakes. He feigned contrition. Along with the company’s first quarterly earnings loss in 14 years last November, Son told investors, “My investment judgment was poor in many ways and I am reflecting on that.” And it kinda seemed like he meant it. Masa and SoftBank have stayed relatively quiet by their standards. It announced that it would unload more than $50 billion of legacy assets including stakes in T-Mobile US, Alibaba, and its own Japanese telecom business to shore up its balance sheet and buy back shares. Conservative move. Nice. The market bought it. SoftBank shares recovered from the 2,687¥ ($25.25) level post-earnings loss in November to as high as 6,932¥ ($65.16) in late August. Then last Friday, the FT dropped a bomb. Masa and his team of profligate spenders were behind the massive runup and subsequent crash in tech stocks. The Son of a bitch had done it again. Hard Truth About SoftBankAfter I wrote about Stripe last week, one of my favorite anonymous alt accounts on Twitter goaded me:My brain doesn’t normally work like that. I’m an optimist. But when I saw that SoftBank was behind the public market tech pump and dump, I knew I had my target. It’s easy to look at SoftBank’s moves and think, “Fuck these guys,” particularly after my experience competing against WeWork. That was my first reaction when the news dropped. SoftBank distorts the markets it plays in. It has had some spectacular private market blowups. And now, it’s messing up the public markets, too.Because SoftBank is so nakedly ambitious and takes such big swings, it’s extremely polarizing. Most recently, SoftBank’s Vision Fund went from “This is going to change the world” to “They’re ruining venture capital” to “See! This guy is an idiot” in the blink of an eye. As a result, there’s not a lot of nuance in the conversation around the company. That’s what I’ll try to bring today, by covering the three ways to look at SoftBank: * Bullish: Masa has a vision that no one fully appreciates and trades at a discount*

Stripe: The Internet's Most Undervalued Company (Audio)

Welcome to the 936 newly Not Boring people who have joined us since last Monday! If you’re listening to this but haven’t subscribed, join 12,206 smart, curious folks by subscribing here!🎧 To get this essay straight in your ears: Stripe (Audio) or on SpotifyHi friends 👋,Happy Monday! The subject of today’s essay, Stripe, is a company I’ve been wanting to write about for a long time. So many smart people are so bullish on the company that I thought they must be missing something. I came away even more impressed by Stripe and optimistic about its ability to transform money on the internet. Speaking of internet money… my friends at The Hustle are Not Boring’s first ever Sponsor! I’m excited about this one, because I read Trends religiously. Trung Phan’s newsletter report has been critical in thinking through how to turn Not Boring into my real job.Trends is offering Not Boring readers a $1 two-week trial, which gives you access to all of their in-depth industry research reports and an excellent community of entrepreneurs. Show them the love and help keep Not Boring free by signing up for a trial at this link:Let’s get to it. Stripe: The Internet’s Most Undervalued CompanyStripe is a payments company that describes itself using the word “infrastructure.” It doesn’t get more boring than that in tech, and yet, Stripe is fanatically adored. People love the company’s co-founders, the charming, intellectual Irish brothers Patrick and John Collison. Its mission is audacious: to increase the GDP of the internet. Engineers rave about its simple-to-use product that makes something as complex as payments just work.And yet... Stripe is underrated. Because everyone loves Stripe, the company is under analyzed. Ben Thompson hasn’t written a Stripe-centered piece since 2017. Sure, there are plenty of product comparisons: Stripe vs. Adyen, PayPal vs. Stripe, Stripe vs. Braintree vs. Square. CB Insights did an excellent deep dive on its history, funding, and offerings earlier this year. There are interviews and podcasts with the Collison brothers galore. The Information did one with Patrick on Saturday. But there is very little in the way of strategic analysis on the company, because writing good things about Stripe just feels cliché. As a result, most people know that Stripe is an incredible company, but very few know why Stripe is an incredible company. So I dug in, looking to write a balanced take. I searched high and low for a bear case for the company -- so many once-gleaming unicorns have faltered recently that I wondered if Stripe didn’t also have some fool’s gold at the end of its rainbow. But clichés exist for a reason, and I came away even more impressed and excited about its future. Stripe is undervalued. The company’s recent $36 billion valuation was a steal and its strategy is underappreciated.Let’s analyze Stripe.What is Stripe? Stripe’s mission is ambitious: to increase the GDP of the internet. Here’s how it describes itself:Stripe is a technology company that builds economic infrastructure for the internet. Businesses of every size—from new startups to public companies—use our software to accept payments and manage their businesses online.But before it was an “economic infrastructure” company, Stripe was simply an easier way for startups to accept payments online with a few lines of code.Stripe’s founding story is well-documented. In 2010, two prodigious brothers from a small village in Ireland, Patrick and John Collison, dropped out of MIT and Harvard, respectively, to start Stripe. It was their second company. They sold their first, Auctomatic, for $5 million in 2008, when they were 19 and 17. While running Auctomatic, the Collisons realized that, despite PayPal’s success and banks’ participation, accepting payments online was too hard. They felt that with more businesses starting online, engineers would decide which payment tools to use, not finance people, and built a product that engineers loved. To this day, everything from their products to their communications are designed to delight engineers. Stripe’s first product was simple. Copy a few lines of code. Start accepting one-off payments. Since then, Stripe has expanded its payments offering to include: * Connect. Payments for platforms. Booking.com accepts payments from travelers and pays out hotels using Stripe. * Billing. Subscription and invoice payments. Were I to make this newsletter paid, Stripe would handle collecting money each month from those of you kind enough to subscribe.* Terminal. Offline payments for online native brands. Warby Parker uses Stripe for both online and in-store purchases. Unlike Square, Stripe doesn’t have a salesforce knocking on bodegas’ doors. This, like everything else Stripe does, is a product for internet businesses, just the ones who happen to have a physical presence, too. * Stripe Payouts. Payments to service providers, sellers, or freelancers. StyleSeat pays out hair stylists instantly for the jobs they’ve complet

Tencent's Dreams (Audio Edition)

Welcome to the 1,085 newly Not Boring people who have joined us since last Monday! If you’re reading this but haven’t subscribed, join 11,270 smart, curious folks by subscribing here!Hi friends 👋,Happy Monday! Thanks to all of you for your feedback! I’ve read through all of it, and I’ll be incorporating a lot of your ideas in the coming weeks. One of the biggest pieces of feedback you gave was to either a) shorten the essays or b) give a TL;DR upfront. I’m going to try the latter today with a short summary of the essay in slide form. You can check it out here, and I’d love to hear your thoughts. In Part I, we covered Tencent’s history, its current businesses, and its massive portfolio of investments. Tencent is undervalued based on its current operating businesses and the current value of its portfolio alone. But Tencent’s positioning for the future is even more compelling, and that’s what we’re going to discuss in Part II today. Full Disclosure: I own shares in Tencent after doing research on it for this two-parter.Let’s get to it.Tencent’s DreamsTencent’s critics argue that it gave up on its dreams by focusing on investing instead of product innovation. I disagree. Instead of building any specific product, Tencent is building an organization and ecosystem designed to be massively profitable in the short-term with asymmetric upside.Through its investments, Tencent is in the best position of any company to usher in and profit from the Metaverse, the misunderstood and potentially mega-lucrative evolution of the internet. I’m not the first person to realize that Tencent is in the lead. In his recent Invest Like the Best interview, investor Matthew Ball said, “So if you said ‘who is closest to the Metaverse today?’ the simple answer is not Fortnite or Minecraft, it’s Tencent.” But Tencent’s advantage extends beyond its lead position in gaming, because the Metaverse will be so much more than games. Look closely at Tencent’s portfolio and you’ll find a group of companies across gaming, ecommerce, and social that will bring the Metaverse to fruition and share in its massive upside. Tencent’s structure and strategy -- provide capital and traffic -- is the perfect model to profit from the decentralized, competitive, creator-friendly ecosystem that the Metaverse is likely to be.That’s a big claim, so here’s what we’ll cover to get there:* The Metaverse. What the Metaverse is, which parts of it are here already, and how big the opportunity is.* Tencent’s Strategy. Instead of building everything itself, Tencent invests. Its Capital + Traffic Flywheel is a smart way to bet on the Metaverse because while technologists are nearly certain that it will exist, no one knows exactly what form it will take. * Platform + Content. The Metaverse will comprise the Platforms on top of which it’s built and Content that users interact with for entertainment, socializing, learning, and commerce. Tencent owns leading Platform candidates - Epic’s Unreal Engine (VR), Snap (AR), Spotify (Audio), and WeChat (internet / super app) - plus companies through which people will play, shop, learn, and socialize.* Where Tencent Might Invest Next. Tencent has announced its intention to invest in infrastructure and “Smart Retail,” and it is likely to invest in remote work and collaboration products like Figma and Agora to round out its business offering.* Obstacles. Tencent faces government regulation and well-resourced competitors. This post is fun speculation combined with practical implications. Tencent’s valuation doesn’t properly price the Metaverse opportunity -- it can’t, it’s so early and so speculative -- which means that with Tencent, you get a business that is undervalued today and a free call option on the future. I want you to leave this post with a better understanding of the Metaverse, and an appreciation for the opportunity that Tencent has to make it a reality and profit from its rise. What is the Metaverse?Oh no, not another Metaverse thinkpiece… Hear me out. The term, first introduced by sci-fi author Neal Stevenson in his 1992 Snow Crash, makes the idea sound silly and game-like. It sounds a little like talking about the World Wide Web in the early 1990’s. Like the Web back then, the Metaverse is an important idea in need of a rebrand.So what is it?In The Metaverse, Matthew Ball says the Metaverse will be an always-on, real-time world in which an unlimited number of people can participate at the same time. It will have a fully functioning economy and span the physical and digital worlds. Data, digital items, content, and intellectual property (“IP”) will work across the Metaverse, and many people and companies will create the content, stores, and experiences that populate it.Epic Games CEO Tim Sweeney agrees, adding, “it will be a massively participatory medium of a type that we really haven’t seen yet,” with “ a fair economy in which all creators can participate, make money and be rewarded.”The Metaverse sounds a lot like the r

Tencent: The Ultimate Outsider (Audio)

Welcome to the 928 newly Not Boring people who have joined us since last Monday! If you’re reading this but haven’t subscribed, join 10,185 smart, curious folks by subscribing here!Hi friends 👋,I want to celebrate Ten k subscribers by going deep on the only company with the right name for the occasion, Tencent. Tencent is the Chinese conglomerate behind the recently-banned WeChat, and one of the world’s most successful investment funds. There’s so much to say about this company that I’m breaking it up into two parts: * Part I (today): Tencent’s history, its business, and its portfolio, including a bonus goody for the investing nerds out there: a link to a spreadsheet I made with the current value of 102 of Tencent’s investments. * Part II (Thursday): Where Tencent is headed - it’s building new cities in China, and it’s going to be at the center of building a whole new world. This post isn’t meant to be political or to pass value judgments. It’s just an assessment of a fascinating company that most of us know far too little about. Favor: if you enjoy this post, please click the little heart button to like it - it helps more people discover my writing - or share it with your most Sinocurious friend. Let’s get to it. Tencent: The Ultimate OutsiderTencent is the most important company that many Americans know the least about. When President Trump signed an August 6th Executive Order banning WeChat from the United States, a lot of people said, “What’s WeChat?” Even those who knew about WeChat know very little about the octopoid company behind it. Let’s fix that. You should leave this two-part essay with a better understanding of what Tencent does, what it owns, and why it’s one of the most significant companies in the world.The Chinese pager-based internet service that Pony Ma launched in 1998 is now the world’s seventh most valuable company, right ahead of Berkshire Hathaway and right behind its bitter rival, Alibaba. As of Friday, Tencent is worth $628 billion.In China, Tencent is like Facebook, Nintendo, Shopify, Netflix, Spotify, Slack, and PayPal rolled into one. Its flagship product, WeChat, has 1.2 billion users, and those users spend more time in the app every day than Americans spend on all social media apps combined. People use WeChat to message friends, shop, read the news, play games, pay for things in physical stores… pretty anything you can do on your phone, you can do on WeChat. Tencent turned the profits from its social networking, ecommerce, and gaming cash cows into a global investment portfolio that includes many of the world’s most popular video games, the fastest-growing internet businesses in China, meaningful stakes in Tesla, Spotify, and Snap, and a portfolio of international startup unicorns second only to Sequoia’s. It even financed A Beautiful Day in the Neighborhood. Americans don’t know much about Tencent because, in addition to being Chinese, it’s really fucking complex. It’s both one of the most profitable operating businesses in the world and one of the most ambitious investment funds. Tencent has been dubbed “The SoftBank of China” and “The Berkshire Hathaway of Tech.” Neither description does it justice. While it gets less hype, its performance puts SoftBank’s to shame. It’s going to be one of the most important companies in the world for decades to come. Today, in Part I, I’m going to explain Tencent in four sections: * What is Tencent? An entrepreneurial story just like the ones you hear in the US, with all of the highs, lows, and near-deaths. An improbable journey from pager-based internet service to the giant holding company it is today.* The Outsiders. William N. Thorndike’s 2012 book, The Outsiders, about eight of the most successful CEOs in US history, provides a framework for thinking about Tencent’s business. CEO Pony Ma shares all of the important characteristics with the eight that Thorndike wrote about.* Tencent’s Operating Businesses. Tencent’s core business makes money in six main ways, and each of its business units rivals in, both scope and revenue, massive, standalone public companies.* Tencent’s Investment Portfolio. There’s no great public source for all of Tencent’s 700-800 investments, so I created a database of 103 of its biggest and share insights around where it invests, in which types of companies, and the unfair advantages it has as an investor. The founding stories of Apple, Google, Microsoft, Facebook, and Amazon are canon for the type of people who read Not Boring. They’re part of modern American mythology. It’s time for us to get to know Tencent.What is Tencent?Note: I’ve used Julia Wu’s summary of Wu Xiaobo’s book, Matthew Brennan’s presentations, and the excellent Acquired podcast on Tencent to piece together Tencent’s history. We’ve been conditioned to think of massive Chinese technology companies as shady, government-controlled businesses out to steal your data and try to take over the world. It might surprise you, then, that Tencent started ou

Shopify and the Hard Thing About Easy Things (Audio Edition)