Anticipating the Unintended

152 episodes — Page 1 of 4

#240 Peering Into the Future

Prediction Time—RSJIn a year when countries as diverse as India, the United States, the United Kingdom, Russia, Taiwan, Pakistan and Palau go for their elections, it is tempting to go for an overarching theme for the year while looking ahead. Unfortunately, like these aforementioned elections and the many others that will see about 50 per cent of the human population exercise their democratic choice, there seems to be only a messy mix of political signals emerging from them. Illiberal forces are rising in some places, and autocrats are rubber-stamping their authority in others. Democracy is blooming afresh in a few, while the trends of deglobalisation and closed borders are resonating among others. Of course, there are the wars old and new and, maybe, a few more round the corner to complicate any attempt at a broad narrative for the world. To add to the woes of anyone trying to write a piece like this, the economic macros globally look volatile and inchoate. There is increasing talk of a soft landing of the US economy while the EU and the UK stare at another lost year. Depending on who you speak to, China has either put its economic issues behind it and is ready to charge back with its investment in future technologies like AI, EVs and hi-tech manufacturing, or it is at the “Japan moment” of the late 80s. Japan, on the other hand, is itself having a brief moment of revival, and no one knows if it will have legs or if it is yet another false dawn.It is foolhardy to purvey macro forecasts in this environment. But then this newsletter won’t write itself. No? So, I guess the best course then is to make more specific predictions instead of taking big swings and hoping those come true while the macros swing wildly. This will also satisfy Pranay’s pet peeve about generic predictions that I mentioned in the last newsletter. So, let me get going with 10 somewhat specific predictions for next year.* President Biden will decide sometime in early February that he cannot lead the Democratic Party to power in the 2024 elections. He will opt out of the race and give possibly the most well-backed Democrat, financially and otherwise, a really short window of four months to clinch the nomination. In a way, this will be the best option for his party. If he continued to run for the 2024 elections, it would have been apparent to many in the electorate that they are risking a President who won’t last the full term. If he had opted out earlier, the long-drawn primary process would have led to intense infighting among the many factions of the party, eventually leading to fratricide or a Trump-like populist to emerge perhaps. A narrow window will allow the Party to back an establishment figure and reduce the fraternal bloodletting. Who will emerge from this is anyone’s guess. But whoever it might be, if (and it is a big if) they have to come up against Trump, they will lose. To me, the only way Trump doesn’t become the next President is if he isn’t on the ballot. And the only way that looks possible is if he loses his legal battles. Otherwise, you will see a second Trump term which will be worse than the first one. * There’s way too much confidence about the Fed having piloted a ‘safe landing’ for the US economy despite the many odds that were stacked against it. I think this is fundamentally misplaced. The fiscal deficit is unsustainable, and much of the soft landing is thanks to it. The GDP growth has been supported by an almost doubling of the federal fiscal deficit. This won’t last. The higher rates that haven’t yet led to any real string of bankruptcies or asset bubble collapses will begin to make an impact. The geopolitical risks that have only been aggravated in the last 12 months and the increasing protectionism worldwide will make it difficult to sustain growth at 2023 levels. My view is that the real landing will be in 2024, and it won’t be soft.* China will get more adventurous geopolitically as it weakens economically. Look, the property market crisis is real in China and given the influence it wields on its economy, it is difficult to see any return to the ‘normal’ 8 per cent growth anytime soon. The local government finances will worsen, and there is a real possibility of a few of them defaulting. There will be more fiscal support to prop up the numbers and more packages for sectors in stress. Foreign inflow will continue to be anaemic, though it won’t be negative, as it turned out late last year. The Chinese customers' long-awaited consumption spree isn’t coming in 2024. All in all, China will stutter while still wowing the world with its progress in tech.* BJP will come back to power, but it will fall a bit short of 300 seats. This will surprise many, considering the continued electoral success of its machinery and all the Ram Mandir ballast it plans for itself from this month onwards. There are a couple of reasons for it, largely driven by electoral arithmetic across the states where it did very well in 2019 and wh

#239 Of Screws and Racquets

Happy New Year— RSJHappy 2024, dear readers! We hope 2023 was good for all of you. If it wasn’t, we are glad that it’s behind you. We didn’t have too bad a 2023 ourselves. This newsletter went along swimmingly (or so we think) and we had our book ‘Missing in Action: Why You Should Care About Public Policy’ published on 23 January 2023. Why haven’t you bought it yet? Anyway, it seems to be doing well based on the modest expectations we had of it. I’m yet to see the pirated versions of it peddled at traffic signals. Heh, that will be the day. But then I see it on shelves of all decent bookstores and that’s quite reassuring. That apart, Pranay had another book (one productive chap, I tell you), When The Chips Are Down on semiconductor geopolitics which is an area that’s going to get more interesting and contentious in this decade. All in all, we ended up writing 44 editions during the year totaling up to over a hundred thousand words. A good year, I guess.On to 2024 then. Like in the past, we will indulge ourselves a bit in the first edition of the year. First, looking back at our predictions for 2023 and seeing how badly off we were and then next week, I will be doing a bit of crystal ball gazing for 2024.Before I bore you with that, let me share with you this wonderful excerpt from a paper I read recently. Titled ‘Enlightenment Ideals and Belief in Progress in the Run-up to the Industrial Revolution: A Textual Analysis’, it covers an area of eternal fascination for me - Enlightenment and its impact on Western Europe. Interesting conclusions and a must-read:“The role of cultural attitudes—specifically, of Enlightenment ideals that had a progress oriented view of scientific and industrial pursuits—in Britain’s economic takeoff and industrialization has been emphasized by leading economic historians. Foremost amongst them is Joel Mokyr (2016), who states that the progress-oriented view of science promoted by great Enlightenment thinkers, such as Francis Bacon and Isaac Newton, among many others, was central to what would become the “Industrial Enlightenment,” and ultimately Britain’s Industrial Revolution. In this paper, we test these claims using quantitative data from 173,031 works printed in England in English between 1500 and 1900. A textual analysis resulted in three salient findings. First, there is little overlap in scientific and religious works in the period under study. This indicates that the “secularization” of science was entrenched from the beginning of the Enlightenment. Second, while scientific works did become more progress-oriented during the Enlightenment, this sentiment was mainly concentrated in the nexus of science and political economy. We interpret this to mean that it was the more pragmatic works of science—those that spoke to a broader political and economic audience, especially those literate artisans and craftsmen at the heart of Britain’s industrialization—that contained the cultural values cited as important for Britain’s economic rise. Third, while volumes at the science-political economy nexus were progress-oriented for the entire time period, this was especially true of volumes related to industrialization. Thus, we have unearthed some inaugural quantitative support for the idea that a cultural evolution in the attitudes towards the potential of science accounts in some part for the British Industrial Revolution and its economic takeoff.”2023 Predictions ScorecardI had 8 predictions across the global economy, Indian economy and Indian social and political order. So, this is how does the 2023 report card looks like.Global EconomyThis is what I had written:#1 The trend of securing your supply chain for critical products will get stronger.….but it is clear to most large economies that on issues that concern national security, it will be foolhardy to not plan for worst-case scenarios any longer. And national security could mean anything, really, but I can see on energy and key technology, nations will opt for more secure supply chains with watertight bilateral partnerships than be at the mercy of distributed, multilateral chains. I won’t go as far as calling it ‘de-globalisation’ yet, but this ‘gated globalisation’ is a trend that’s here to stay.This is playing out but a bit slower than what I expected. Disentangling and building domestic capabilities isn’t easy. And it is costly. But through the year we had increasing curbs on what hi-tech (GPU chips, AI research) and defence companies domiciled in the West could export to China. At home, we continued the push on PLI on electronics and tech equipment with debates on how much value-added manufacturing is really coming through in these schemes. Also, interestingly, we are continuing down the path of decoupling from global ‘default platforms’ especially in financial services. The Rupay platform is continuing to get bigger with a specific push from the government to derisk payment infrastructure from global networks like Visa and Maste

#238 Everything's Connected

India Policy Watch #1: Like a Kid in a Candy StoreInsights on current policy issues in India— Pranay KotasthaneIn the previous edition, I asked you to name your favourite sports policy to date. I don’t have a great answer myself. Nevertheless, my candidate would be liberalising FDI in retail.When posed with such questions, we often get anchored to the way governments are organised. The best sports policy can only be made by the sports ministry; the best education policy can only be made by the education ministry, and so on. These answers assume that the public policy system is a linear, deterministic system with a small number of variables and negligible overlap across ministries.But as we discussed in edition #213, it is useful to characterise public policy as a complex system. Such a system is greater than the sum of its parts and these parts interact and share information with each other. Complex systems display non-linear behaviour as small actions can have large effects while large actions can have small effects. As a result, decomposing the system into its constituent parts, and analysing them separately often results in inaccurate analysis.Deploying the complexity lens makes us think beyond narrow sectoral policies. In the case of sports, it means we can think beyond the obvious candidates such as Target Olympic Podium Scheme (TOPS), Fit India, or Khelo India. As an amateur sports enthusiast, I contend that liberalising FDI in retail had a disproportionately positive impact on sports in India because that policy led to the world’s largest sporting retailer setting up shop in India.Until fifteen years ago, buying sports equipment was not very different from purchasing soap at a kirana store. The options were limited and the buying experience was consistently disappointing. Moreover, equipment of only the most popular sports found space in the retail storefront.All that changed with the entry of the French sports retailer, Decathlon; first in the cash-and-carry segment starting in 2009 and as a single-brand retailer in 2013 after the FDI policy allowed 100% FDI in single-brand retail. Decathlon has given the Indian sports enthusiast a choice and a range of sporting equipment that my 20-year-old self would find unimaginable. Allowing FDI in e-commerce was the next step jump, making these sports equipment accessible to people outside Tier-I cities.I wish we had a real study of the consumer surplus generated by FDI liberalisation. Nevertheless, this example shows how sector-agnostic liberalisation can have a major impact. Ten years after the entry of Decathlon, further liberalisation of multi-brand retail is needed to bring more competitors into the sector, benefiting Indians at large.Of course, no one policy can solve all problems. All success is multi-causal, especially in a complex system like public policy. But my aim here was to make you think beyond ministry turfs when approaching questions of this nature.India Policy Watch #2: Holiday ReadingInsights on current policy issues in India— Pranay KotasthaneThe year-end holidays are approaching. So what’s the best way to spend the holidays? Reading, of course. This time around, I want to recommend some classic reports that tried to diagnose India’s condition. Initial conditions matter a lot in a complex system, hence I’ve picked out reports that give a fair account of the problems that India inherited in various domains around the time of independence.* Economy: Milton Friedman visited India twice in the 1950s and wrote two stunning articles on “Indian Economic Planning” and “A Memorandum to the Government of India 1955”. His diagnosis rings true even today. Centre for Civil Society has compiled the essays into a book.* Public Policy and Administration: Paul Appleby’s Public Administration in India-Report of a Survey was an important report where the American consultant tries to diagnose problems with India’s public administration. The report is available on the Internet Archive.* Science Policy: AV Hill was called by the British government in 1943 to advise on the organisation of scientific and industrial research in India. Some of our over-centralised scientific establishment cut off from the university ecosystem can be traced back to this influential report.* Politics: It’s amazing how Ambedkar’s diagnosis is accurate in so many areas simultaneously. In Thoughts on Linguistic States, he identifies “one language, one state” and “one state, one language” as the two different approaches for state creation. His election manifesto for the Scheduled Castes Federation from 1951 identifies problems with India’s economy, foreign policy, and society. On the emotional issue of partition, he displays an amazing clarity of thought and analysis. With the benefit of hindsight, we can say that his analysis foresaw events and phenomena other leaders of his generation couldn’t.Enjoy reading! And share your thoughts on these reports with us.HomeWorkReading and listening

#237 Looking Under the Hood

Course Advertisement: Admission to Takshashila’s Graduate Certificate in Public Policy (GCPP) programme is now open. Start your 2024 with a course that will equip you with the tools to understand the world of public policy. Check all details here. India Policy Watch: In Search Of GrowthCurrent policy issues in India— RSJA quick macro update. The RBI’s Monetary Policy Committee (MPC) met this week and, as was widely expected, kept the repo rate unchanged at 6.5 per cent for the fifth consecutive time. The Governor gave the usual explanation of global political risk, higher volatility in global financial markets, and continued inflationary expectations as the reason for keeping the policy stance unchanged as ‘withdrawal of accommodation’. And the Governor was quite clear that there is no ‘inadvertent’ signalling to the market that it has actually moved to a ‘neutral’ stance with its prolonged pause on rate hikes:“Reaching 4 per cent (inflation target) should not just be a one-off event. It has to be durably 4 per cent and the MPC should have confidence that 4 per cent has now become durable.We are very careful in our communication. There is no inadvertence in any of our communication. So, if somebody is assuming that it is a signal to move towards a neutral stance, I think it would be incorrect.”Well, that takes care of any possibility of a rate cut before next year's elections. And what’s the need, really? Between now and the elections, there’s always an inflation risk on vegetable and food prices. Also, while crude oil price has been on a downward trend during this year which has helped on the inflation front, there’s no guarantee how that will trend given the global geopolitical situation remains uncertain. Most importantly, what’s the need to signal any rate cut when the GDP growth numbers are coming in significantly above even RBI’s somewhat optimistic forecasts at the start of the year? Q2 GDP grew at 7.6 percent, almost a full percentage point above estimates, leading the central bank to up its full-year forecast to 7 per cent. All good news so far. Further, the RBI note had this optimistic comment for the near term:“The healthy twin balance sheets of banks and corporates, high capacity utilisation, continuing business optimism and the government’s thrust on infrastructure spending should propel private sector capex.” Well, you can go back to the past six quarters, and you will find similar sentiments about an impending private sector capex boom from both the government and the private sector. But it is turning out to be a bit of a mirage. While both the corporate and bank balance sheets are the healthiest they have been in the past two decades, there is a continued ‘wait and watch’ approach on capex, which has mystified most observers. While the consumption growth remains robust, there are early signs that this lag in private capex is beginning to slow down corporate revenue growth. From the Business Standard:“.... the slowdown in corporate revenue growth over the last one year has begun to reflect in India Inc’s capital expenditure as there is a close correlation between growth in net sales and investment in fixed assets. The net sales of 725 companies, excluding BFSI and state-run oil & gas firms, were up 4.2 per cent year-on-year (Y-o-Y) in H1FY24 – the lowest half-yearly increase in the last three years and down sharply from 12.2 per cent growth in the second half of FY23 and 31.3 per cent growth in the first half of FY23.”As if on cue, the Chief Economic Advisor (CEA), picked the issue of sluggish private capex at a CII event this week. Instead of the expected anodyne address at events of this nature, he made some very insightful points. First, he correctly pointed out that to expect consumption to continue to drive GDP growth while private capex sits out for as long as it has defies logic. Consumption, as we have pointed out more than a few times here, is the residual factor. And that’s exactly the point the CEA made (again quoting the Business Standard):“Waiting for demand to arise before they start investing will actually delay the onset of such demand conditions happening, because usually consumption has to be the residual. Investment leads to employment, which leads to income generation and which in turn creates consumption and then the savings are recycled back into the investment. So the more the corporate sector delays its investment, this virtuous cycle will not materialise.”Then he mused on what might be holding the private sector back despite strong balance sheets, robust GDP growth and a general sense of global optimism about India’s prospects:“So what is holding it (corporates) back? It is easy to say that there is general demand uncertainty. Post Covid, recovery has started. But one thing we have to remember is that this decade is going to be the decade of uncertainty, whether we like it or not. So for us to wait for the uncertainties to abate or recede, [its] like waiting for the w

#235 Right Diagnosis, Wrong Prescription

Read the full text here. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit publicpolicy.substack.com

#221 The Good, the Bad and the Ugly

This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit publicpolicy.substack.com

#220 (China+1) Or (1-China)?

This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit publicpolicy.substack.com

#219 Of Sins, Bets, and Bluffs

Full text here. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit publicpolicy.substack.com

#218 TechTalk

The full text is here. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit publicpolicy.substack.com

#217 False Hopes and Weak Promises

The full text is here. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit publicpolicy.substack.com

#216 Thick and Fast

Read the edition here. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit publicpolicy.substack.com

#215 Of Openings and Possibilities

Read the edition here. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit publicpolicy.substack.com

#214 The Stakes are High

Financial Regulation of Private Firms + Emigration of Indian Talent This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit publicpolicy.substack.com

#213 The Mind Plays Tricks

India Watch #1: Of Protests and Perfect TricksInsights on issues relevant to India— RSJFor nearly a month now, some of India's top wrestlers, who between them have earned over 25 medals in various global competitions, have been protesting against the conduct of the Wrestling Federation of India (WFI) chief and BJP MP Brij Bhushan Singh. This is not an ordinary protest. The allegations in the FIR against Singh are quite serious, including a couple of instances of demanding sexual favours as a quid pro quo for professional assistance, about 15 incidents of sexual harassment and stories of inappropriate touching, and molestation of minor girls. You would imagine this would be some kind of an open-and-shut case. I mean, here are a few women wrestlers who have everything to lose here by taking a stand against their own federation and the government. They aren’t superstar cricketers with financial security and access to media. They don’t have multi-million and multi-year sponsorship deals or lucrative post-retirement commentary gigs waiting for them. Their sport is everything to them, and they are willing to risk that one thing they have loved doing all their lives. These are girls who have come up the hard way in a society that doesn’t prize either women or sports and especially women in sports. They have persevered despite the odds against them because that’s what athletes do. So, the least you would have thought is that while the police investigations and the judicial process is going on, or, as we like to say in India, as the law takes its own course, the government should ask the WFI chief to step down temporarily. Surprisingly though, this doesn't seem to be a priority for the government. Instead, it appears they would rather suppress these voices than address their concerns. So, last week while you had saturation coverage on various channels about the inauguration of the new parliament building, these athletes were being roughed up and assaulted at the site of protest. There was barely any TV media there. As they say, there are always two Indias at work. It is tempting to zoom out a bit and say that this story, in many ways, reflects the current state of Indian politics and society. It is not there yet. But there is a pattern in how we are dealing with protests and dissent that merits a deeper look. Before I go there, let me count the number of ways we have got this thing wrong. Firstly, for decades, we have managed sports and their governing bodies in India in the most unprofessional way possible. These positions have often been given to politicians as small consolation prizes to run their minor fiefdoms. Corruption, nepotism and high-handedness of officials have come along with this. Read any autobiography of an athlete in India and you will be struck by the remarkable apathy and neglect they had to overcome from their own sporting federation to succeed. As major sports events like the Olympics or Asian Games approach, there's often a question of why our sporting performance doesn't reflect our population size and recent prosperity. This story never gets old. While we have seen some improvement in the last decade, we remain an underperforming nation in sports. One fundamental issue to address is improving sports administration by involving experts with experience in either playing the sport, managing large organizations, or possessing a proven visionary track record. Indian tennis is a prime example where one family has presided over its administration for over half a century. We have only gotten worse in tennis, with almost no one ranked anywhere in the top 1000 in the world. Similar fiefdoms exist in other sports like boxing, shooting and even cricket. Despite the efforts of some public-spirited lawyers and a few interventions by the Supreme Court to set things right, things have remained the same. There was some hope when this government came to power that there would be much-needed reforms in sports administration, especially in those early days. However, once you have the keys to the power of the state, it is difficult to resist its benefits. The result is a disheartening situation where politicians with limited understanding or passion for sports lead the federations. We are back to the bad old days now. Secondly, we seem to be undoing all the progress we have made in addressing sexual harassment allegations in the workplace. There are POSH committees that are legally mandated in organisations and a framework that allows for a safe and secure environment for women at work. In India, the foundation for this framework was based on the Vishaka guidelines set nearly 25 years ago. In cases like this, the employer (in this case, the sports ministry) should form a committee with an independent chair who investigate these allegations and arrive at their conclusions. And it is usual that during such an investigation, it would be appropriate for the accused to step aside for a free and fair process. However,

#212 Myths & Misconceptions

Being Pragmatic about ESG Norms, Lessons for India's Semiconductor Strategy, and Challenging Common Wisdom about India's Constitution-making. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit publicpolicy.substack.com

#211 Of Motives and Presumptions

India Policy Watch #1: Silly Season Is Upon UsInsights on issues relevant to India— RSJLate on Friday this week, the RBI issued a circular withdrawing the circulation of ₹2000 denomination banknotes. The RBI clarified that these notes would continue to serve as legal tender, so this isn’t another demonetisation. Here’s the Indian Express reporting:THE RESERVE Bank of India (RBI) Friday announced the withdrawal of its highest value currency note, Rs 2,000, from circulation, adding that the notes will continue to be legal tender. It said the existing Rs 2,000 notes can be deposited or exchanged in banks until September 30, but set a limit of “Rs 20,000 at a time”.“In order to ensure operational convenience and to avoid disruption of regular activities of bank branches, exchange of Rs 2,000 banknotes can be made up to a limit of Rs 20,000 at a time, at any bank starting from May 23,” it said.“To complete the exercise in a time-bound manner and to provide adequate time to the members of the public, all banks shall provide deposit and/ or exchange facility for Rs 2,000 banknotes until September 30, 2023,” the RBI said.The RBI circular and the press note also attempt to make a convincing, logical case for this decision. There appear to be three reasons for doing this.Thanks for reading Anticipating the Unintended! Subscribe for free to receive new posts and support my work.One, the ₹2000 denomination notes seem to have served their useful purpose. They were introduced in November 2016 when the legal tender status of existing ₹500 and ₹1000 banknotes in circulation were withdrawn. Looking back, it appears these were introduced to help re-monetise the economy really quickly, which was under the stress of not having adequate new legal tender banknotes. According to the RBI, after this task of re-monetising was completed, the printing of new ₹2000 banknotes was stopped in 2018-19. Therefore, after 5 years of not printing any new notes, this looks like the right time to take them out of circulation completely.Two, since most of the ₹2000 denomination notes were issued prior to 2017, they have apparently completed the typical lifespan of a banknote which is between 4-5 years. In an ideal system, most of these old notes should have come back to the RBI by now. Further, these notes are not seen to be used for transactions anymore. They seem to be just sitting somewhere out there. So, in pursuance of the ‘clean note policy’, the best course of action is to withdraw them from circulation. Lastly, there was also an allusion to the ₹2000 notes being often found by various investigative agencies in their haul of black money or frauds. So, somewhere there is a view that withdrawing these notes would smoke these fraudsters out, who are sitting on piles of this unaccounted-for cash.Now, as students of public policy, we must assess this measure based on its intended objectives, the likely costs of doing it and the unintended consequences that are likely to arise. The first reason—that the ₹2000 banknotes have served their purpose, so it is time we take them out—can be scrutinised further. I don’t think it was made clear when they were introduced back in November 2016 that the only reason for doing it was to re-monetise the economy quickly. There’s a bit of retrofitting of logic here. Also, the decision to stop printing new ₹2000 notes in 2018-19 has meant the total circulation of these notes has been on a decline. In the last four years, the total value of the ₹2000 notes in circulation has gone down from ₹6.5 trillion (over 30 per cent of notes in circulation by value) to about ₹3.6 trillion (about 10 per cent of total circulation by value). I guess, left to itself, we might have had this number slide to a smaller number, say below, ₹1 trillion in the next 3 years. The same point is relevant for the ‘clean note policy’ since these notes would have eventually come back if they were not being used for transactions and were already at the end of their lifetime. So, the question is, did we need to accelerate something that would have followed a natural path to the policy objective that’s desired? Would another three years of these notes in circulation have been detrimental to some policy objective? It is not clear. What’s clear is there will be another season of ordinary citizens queuing up in front of bank branches that will begin on Monday. It might be argued that there won’t be any panic because the regulator has made it clear that these notes will continue to be legal tender. But who will receive these notes for any transactions starting today? These notes are as good as useless, and for anyone who uses them for transactions or has stored them for any legal purpose, the only way is to get them exchanged for those notes that are both legal and usable. There’s always a sense of schadenfreude among the middle class that it is the rich who will suffer. As was seen during the demonetisation exercise, the poor suffer equally, if not m

#210 Metastability

Global Policy Watch: Much Ado About De-dollarisationReflections on global policy issues— RSJThis week, Donald Trump urged Republican lawmakers to let the U.S. default on its debt if the Democrats don’t agree on massive budget cuts. Trump likened the people running the U.S. treasury to ‘drunken sailors’, an epithet I can get behind. Default is not something Janet Yellen, the U.S. Treasury Secretary, can even begin to imagine. As CNBC reported, Yellen chose strong words to express her views if the debt ceiling was not raised by the House:“The notion of defaulting on our debt is something that would so badly undermine the U.S. and global economy that I think it should be regarded by everyone as unthinkable,” she told reporters. “America should never default.”When asked about steps the Biden administration could take in the wake of a default, Yellen emphasized that lawmakers must raise the debt ceiling.“There is no good alternative that will save us from catastrophe. I don’t want to get into ranking which bad alternative is better than others, but the only reasonable thing is to raise the debt ceiling and to avoid the dreadful consequences that will come,” she told reporters, noting that defaulting on debt can be prevented.There is more than a grain of truth there in some of her apparent hyperbole. The U.S. hegemony in the global financial system runs on trust that they won’t default on their debt. Take that trust out of the equation, and what have you got left? This is somewhat more salient in these times when there’s a talk of de-dollarisation going around. Russia and China have been keen to trade in their own currencies between themselves and other partners who are amenable to this idea. And they have found some traction in this idea from other countries who aren’t exactly bit players in the global economy. In March this year, the yuan overtook the dollar in being the predominant currency used for cross-border transactions in China. Here’s a quick run-through of what different countries have been doing to reduce their dollar dependence. Russia and Saudi Arabia are using yuan to settle payments for gas and oil trade. Russia offloaded a lot of US dollars in its foreign reserves before the start of the war and replaced it with gold and yuan. It will possibly continue building yuan reserves in future. Brazil is already doing trade settlements in yuan and is also using the CIPS (China’s response to US-dominated SWIFT) for international financial messaging services. Argentina and Thailand seem to be also doing more of their trade with China in yuan. And I’m not including the likes of Pakistan, Bangladesh and other smaller economies that have politically or economically tied themselves up with China and are following suit. And a few weeks back, the French President, Emmanuel Macron, also raised the issue of strategic autonomy of the EU after his visit to Beijing. As Politico reported:Macron also argued that Europe had increased its dependency on the U.S. for weapons and energy and must now focus on boosting European defense industries. He also suggested Europe should reduce its dependence on the “extraterritoriality of the U.S. dollar,” a key policy objective of both Moscow and Beijing. “If the tensions between the two superpowers heat up … we won’t have the time nor the resources to finance our strategic autonomy and we will become vassals,” he said.You get the picture. This idea of de-dollarisation seems to be gaining traction. How real is this possibility? There are possibly three lenses to look at this issue, and we will cover them in this edition.Why the recent hate for the dollar?A useful area to start with is to understand where this desire to find alternatives to the dollar is emerging. I mean, it is obvious why Russia and China are doing it and the way the U.S. used its dominance over the financial system to shut out Russia. Companies were barred from trading with Russia, Russian banks couldn’t access SWIFT and networks like Visa and Mastercard stopped their operations. Russia got the message but so did other large economies that didn’t think of themselves firmly in the U.S. camp. ‘What if’ questions began circulating among policymakers there. What if, in future, a somewhat unpredictable U.S. president decides to do this to us? And once you start building these scenarios, you soon realise the extent of dependence the global financial system has on not just the dollar but, beyond it, to the infrastructure and rules of the game developed by the U.S. corporations. There’s been a measured retreat ever since. In India, a visible example of this has been the push toward Rupay by the regulator and the government in lieu of Visa and Mastercard. But merely looking at the U.S. response to Russia as the reason would be missing the longer-term trend. In his book ‘Bucking the Buck’, Daniel McDowell shows data on the annual number of executive orders that instruct the US Treasury to enforce financial sanctions against s

#209 Of New Beginnings and Old Grouses

Global Policy Watch: Chronicle Of A Crisis Foretold Reflections on global policy issues — RSJA major state election (Karnataka) is coming up this week. But there’s hardly anything worth analysing. The Congress seemed to have a slight edge in the early opinion polls, but that’s wearing thin. The BJP, always with its ears to the ground, has cranked up its poll machinery in the last couple of weeks drawing upon the star power of the PM in the urban areas of the state. The friendly media houses have been mobilised to pick up ‘emotive’ issues that would tilt the scale in favour of the party in power. It is not too difficult to figure out what the average voter wants if you go by the opinion polls and surveys. But those substantive issues just don’t feature in the public discourse. If you read the papers or media reports on what’s being debated among parties in Karnataka, it is about who is a Hindu hater, who prostrates more often before deities and how going back to the OPS (old pension scheme) is such a wonderful idea. In the classical model of how representative democracy ought to work, the voters would have a limited view of how the world works, and it is the representative who owes the voters not only his labour but also his judgment on issues (to riff on Burke). That seems to be inverted here. One set of representatives has, over the last few years, instituted all kinds of targeted laws - hijaab ban, anti-conversion laws, scrapping minority quotas and cow slaughter ban - in the hope that they will yield electoral gains. The other set is talking of another set of bans convenient to them and some really bad economic policies. We often say that this newsletter attempts to change the demand side of the political equation by making people more aware of public policies and demanding better from their representatives. What we have here is the public demanding the right kind of things (if opinion polls are to go by), but their representatives are keen on dragging them back to divisive emotive issues. The Karnataka election will be a good test of what prevails eventually. I can almost see the straight line from these polls to the general elections due almost exactly 12 months from now. We will all be debating similar trivial issues than what really should matter to India. For some reason, that doesn’t make for a good topic of debate. It makes any election analysis a waste of time, really. Switching gears, as I finished writing my last week’s edition on what the US Fed refuses to learn from the SVB collapse, another mid-sized US bank, the First Republic Bank (FRB), went down and was sold to J.P. Morgan, the ultimate backstop in the US financial system. No amount of assurance from FDIC to the depositors of the bank nor the combined infusion of capital about a month back from a consortium of big banks into FRB was enough to stanch the outflow of deposits. Soon the bank was insolvent, the shareholders and bondholders lost everything, and J.P. Morgan was given enough of a sweet deal to pick up the pieces. I’m sure the Fed will come out with another report on the FRB collapse where it will blame the management for not hedging its treasury risks and being lax in its risk practices. There will be a light rap to the supervisors and staff from Fed who monitored FRB, and that will be that. I hope there’s some more introspection by the Fed than that. Because as the shares of PacWest and Western Alliance have sunk over the last two days, it is clear that a number of mid-sized banks are going to collapse in slow-motion and end up in the lap of J.P. Morgan or FDIC very soon. The feeble Fed response was a 25 bps hike in rates last week with a strong indication that it will hit the pause button on hikes now. The question is if that’s enough to structurally save many of these banks.I have argued for the past couple of months (just after the SVB collapse) that there are three problems for the Fed to contend with, and there are no real answers for them. It is Hail Mary time. Choose the best among the worst options and brace for the impact. I will lay out the three problems it faces before suggesting what looks like the best of the worst option that the Fed has chosen. First, the Fed continued raising interest rates to fight inflation without thinking through its impact on the banking system. This much is clear now. The surprises that have come up in the shape of SVB, Signature and FRB weren’t anticipated at all. As the interest rates rose, the value of the long-term assets held by banks has fallen while their liabilities, in the form of deposits, which tend to be shorter in term, haven’t fallen as much. The slowdown in the economy has meant there’s not enough demand for credit at elevated rates, which means banks continue to invest in long-term US treasury bills. Every time the rates go up, these held-to-maturity (HTM) assets take a notional mark-to-market loss. A recent report by the Hoover Institution suggests that at this moment, th

#208 Go Shape the Molten Metal Now*

India Policy Watch #1: How Not to Let the Opportunity Slip AwayInsights on issues relevant to India — RSJA strange thing happens when you are away on a break. One week you are sitting and wondering how many different things you can write about because of the flurry of events around you. US banks getting into trouble, Rahul Gandhi being denied bail, more curbs on US companies doing business in China, frenetic moves in semiconductor politics - you get the picture. And then you take a break. And everything slows down. First Republic Bank doesn’t implode in a matter of hours like SVB. Instead, it drags its feet in a slow-motion death spiral. RBI pauses on its rate increases. Janet Yellen pulls back on US hostility towards China while cooing about how the two economies need one another. Things go to a standstill when you stop looking at the world with a weekly columnist’s gaze. It is like the vibe of a still summer day in India takes over everything. Nothing moves. Once back, what does one write about? Well, thematically, there isn’t any one thing that will do right now. So, I guess I will cover a few areas that could be of interest.The big story out of India last week was that we might have overtaken China in the population sweepstakes. This was kind of inevitable, and a million people here or there doesn’t make a difference in the larger scheme of things. Yet, it is as good a moment as any to reflect on that elusive thing called the India opportunity. Now, we have devoted multiple editions to why having more people is a good thing. Somewhat to my relief, a lot of commentary in the last week has echoed this sentiment. There’s the usual comparison of the relatively younger demographics in India with that of China and the advantage of being more aligned geopolitically with the West. And, of course, the governments in India don’t do terribly arbitrary things like China did in the past couple of years to the tech sector. On this last point, I have my views, but we are using a really broad brush here, so I will let it pass. The general tone of these articles is that this is India’s opportunity to lose—a far cry from my school days when the population was seen as a problem. I have three points to make in this context which are a bit different from the usual view of what India should do not to let this opportunity slip.First, there’s the usual prescription that India should industrialise faster to take advantage of this dividend and avoid the middle-income trap. My usual take on this is how well do we know why India couldn’t industrialise faster in the last 20 years when China took off. It is not like this is a fresh insight that wasn’t known to policymakers then. So, what gets in the way of India to industrialise? My short answer will always be the state. Despite all the hype around Make in India and the rising ease of doing business rankings, it is still quite difficult to start and run a business in India. The state is deeply entrenched in controlling capital in India, and it enjoys the arbitrary power that it has over them that it is impossible to change this with just better optics of ‘single window’, tax holidays or investment roadshows. In the last two decades, the state has retreated a bit in some areas, but paradoxically, with greater digitisation, it has more information and, therefore, greater power over industry. My general contention is that the state can continue with its welfarism (or whatever else you may call it) on the social and political front, but for India to industrialise, the state has to retreat on the economic control it wields. This looks very difficult today because the state’s first goal is to perpetuate itself. It will require the PM to go back to some of his campaign promises of pre-2014 with real conviction. All Indian politicians of a certain vintage are instinctively socialist. And as the farm reforms saga showed, even a small vocal minority can derail a progressive reform. The other challenge has been the availability of capital for MSMEs to build their business and compete for global orders. For the most part, since 2009, we have had a twin balance sheet problem, and that has meant banks have been very choosy about whom to lend. Add to that the shallowness of the corporate bond market, and we end up having a manufacturing sector low on its ambitions. On this, we might be on a better footing now. Bank and corporate balance sheets are at their robust best, and the public digital infrastructure and GST network make it possible for better underwriting decisions using informational collateral. This is evident in the robust credit offtake reported in the MSME segment across the banking sector in the past year. My view is we will industrialise a bit faster than in the past, but we are going to fall short of the expectations of the kind of industrialisation that’s expected for us to increase our per capita income from $2000 to $10,000 in the next 15 years. China traversed that exact journey

#207 The Rise and Rise of Conglomerates

India Policy Watch #1: Don’t Concentrate Insights on issues relevant to India— RSJIn one of the recent editions on the Hindenburg short-selling saga, I had written about how easily the Adani group had spread itself into a diverse range of sectors. The group was highly leveraged because it was so keen on getting into newer sectors and then winning bids in them with metronomic efficiency. Generally speaking, it is difficult to run a conglomerate of different businesses. You might argue that each business can be handled by a competent management team who will use the brand name and deep pockets of the parent group to build a solid business. But it is easier said than done. Capital allocation decisions, which lie at the heart of executing a business strategy, are difficult within a single line of business. They become hugely complicated within a conglomerate of businesses. Misallocation of capital, lack of focus and inability to stay competitive against smaller, nimbler players eventually follow. Soon, the businesses need to be hived off, and you find companies convincing would-be investors on how they are doing fewer things and doing them well instead of spreading themselves too thin. This is the usual cycle. Yet, you see conglomerates appearing on the business landscape across countries. In some cases, these are businesses integrating vertically or finding interesting adjacencies in their business. This kind of makes sense in the Coase-ian “Nature of Firm” way. I mean, if the transaction costs of finding someone to do a particular work are higher than you doing it yourself, sure, go ahead and do it yourself. But beyond that, there should be no economic reason for having conglomerates. Unless you have one of these conditions in the economy: a) Cost of capital is high, and access to it is difficult. Newer players find it difficult to access capital to start new businesses while older, established players with free cash flow can muscle their way into unrelated but lucrative new sectors only because they have access to capital at a lower rate. b) The playing field isn’t level for newer players to make a dent. Through a mix of friendly regulations, ‘working’ the networks and M&A activities, the bigger players continue to have an advantage going into a new sector over smaller players who might have expertise in cracking those sectors open.c) There’s relatively little ease of doing business in those sectors or in the evening overall. The established conglomerates with an army of people, lawyers and consultants can get started relatively faster and capture the market than new entrants. You don’t have to be a genius to see where the Indian policy-making framework is on the above conditions. There’s common and easy access to capital through a large number of PEs and VC funds but only for a particular kind of ‘flavour of the season’ variety. This also is getting difficult to access. The market for other forms of capital isn’t deep enough. In the same vein, long-term capital for greenfield projects where the credit risk has to be borne by the issuer isn’t available. There is always a whiff of regulatory capture especially in sectors where the government is closely involved bin decision making. Lastly, we might have moved up in the ‘ease of doing business’ rankings, but it isn’t clear yet how this has changed things on the ground. New businesses still find going tough for them. All of the above means that in the past five years, we are reversing a trend seen since the ‘91 reforms. That of increasing salience of conglomerates in India. You don’t have to research too hard. Just take a look at any sector - already big or one that is emerging - you will have the same spectacle of a few large corporate groups getting themselves into all sorts of businesses, from defence to semiconductors or from airlines to carbonated soft drinks only because they believe they can take advantage of market distortions.As if to illustrate this point further, here's news that’s only a day old. Here’s Moneycontrol reporting:“The shares of Mukesh Ambani-led Reliance Industries Ltd (RIL) rallied 3.5 percent in the morning trade on March 31 after the company said secured creditors, unsecured creditors and shareholders would meet on May 2 to approve the proposed demerger of Reliance Strategic Ventures.After the approval, the unit, which is the financial services subsidiary of the oil-to-telecom conglomerate, would be renamed Jio Financial Services.Benefits that shall accrue on the demerger of the financial services business will be the creation of an independent company focusing exclusively on financial services and exploring opportunities in the sector, the independent company can attract different sets of investors, strategic partners, lenders and other stakeholders having a specific interest in the financial services business, a financial services company can have a higher leverage (as compared to the Demerged Company) for its growth and, unlocking

#206 Those Immutable Laws

India Policy Watch: Those Mind GamesInsights on issues relevant to India— RSJRegular readers might have noticed the absence of posts analysing the political economy and politics in general in our editions of late. This isn’t intentional. There’s not much to write about. There is a strange sense of stasis all around. Every move, every act is a chronicle of a future foretold. This inertness stems from a complete absence of ferment in the political landscape. The external factors that could impact politics, like the economy or national security, appear stable. And those directly in the fray have to contend with a political juggernaut backed by a fawning media that takes no prisoners. It is a complete mismatch. So, what can one write about except rallies, speeches and opinion pollsInto this state of ennui, this week walked the Court of chief judicial magistrate HH Verma, Surat. Here’s the Mint reporting on this:“The Surat District Court sentenced Congress MP Rahul Gandhi to two years of imprisonment in the criminal defamation case filed against him over his alleged 'Modi surname' remark. The Congress leader was later granted bail by the court.The court of Chief Judicial Magistrate HH Varma, which held Gandhi guilty under Indian Penal Code sections 499 and 500, also granted him bail and suspended the sentence for 30 days to allow him to appeal in a higher court, the Congress leader's lawyer Babu Mangukiya said.The case was filed against Rahul Gandhi for his alleged “how come all the thieves have Modi as the common surname?" remarks on a complaint lodged by BJP MLA and former Gujarat minister Purnesh Modi. The Lok Sabha MP from Wayanad made the alleged remarks while addressing a rally at Kolar in Karnataka ahead of the 2019 Lok Sabha elections.”In a remarkable feat of speed and agility, the Lok Sabha Secretariat disqualified Rahul Gandhi as a member of Lok Sabha the next day. As the Hindustan Times reported:“Congress leader Rahul Gandhi has been disqualified as a member of Lok Sabha a day after the Surat court convicted him for two years in a defamation case. However, he was granted a 30-day bail in the case to allow him appeal in a higher court. The Lok Sabha secretariat said in a notification that he has been disqualified from the day of the conviction under the Constitution’s Article 102(1)(e) read with Section 8 of the Representation of the People Act.As a next step, the Wayanad MP will have to appeal to the higher court seeking a stay on the conviction, in order to prevent the disqualification and the Congress said it will follow the procedure to move to a higher court.”Look, there’s a tired old way of looking at all of this. And that’s what the discourse has been about this over the past few days. The opposition reminds us how there’s an undeclared emergency at this moment in India. Dissent is being suppressed, the slightest criticism of the PM or his party is seen as an affront to the nation, and the state machinery is fairly quick in settling scores on those not falling in line. There is also the eternal optimism of a certain section of the commentariat that suggests that Rahul Gandhi has rattled the BJP with his Bharat Jodo yatra. And this is the response to keep him in check. I’m sure there is an alternate universe where this is all true. But none among us is turning into Michelle Yeoh anytime soon to enter that multiverse. As I have mentioned earlier, there’s still space for the opposition, as the response to the yatra shows. But Rahul Gandhi neither has the enterprise nor the ideas to turn that into electoral success. On the other hand, the BJP and its supporters initially argued that a sitting MP cannot make disrespectful remarks about the PM. Apparently, it is not done, especially when the PM is feted the world over for his leadership. Soon old videos popped up that showed we have a hoary tradition of calling our past PMs names. I’m old enough to remember the memorable rhyming metre of ‘gali gali mein shor hai, Rajiv Gandhi chor hai’ that rented the air in 1989 when I first followed a general election in my life. The tack changed. So, now you have the charge that Rahul Gandhi was denigrating an entire OBC community with that statement and triggering possible social unrest. This is a failure to understand syllogism 101. Even if one were to accept the dubious statement that ‘all thieves have Modi surnames’, it doesn’t follow that ‘all with Modi surnames are thieves’. The more nuanced lot is taking the line that it is the courts that are letting the law take its own course, and we shouldn’t read anything more into this. It is possible this is true, but we might again be talking of the multiverse here. Leaving that aside, we now have WhatsApp experts who look for a masterstroke in every decision of the ruling party now suggesting that this is a convoluted plan to give Rahul Gandhi a convenient leg up to be the face of the opposition in 2024 and then decimate him in the elections. If only there were a No

#205 Doodh Ka Doodh, Paani Ka Paani

Global Policy Watch: Bailout Pe Bailout Pe BailoutInsights on global policy issues relevant to India— RSJWhere do I start this week? Maybe with a spot of self-promotion. Pranay and I were guests on the popular Hindi podcast Puliyaabazi. I have been a long-time fan, so it was nice to be a guest there. Pranay usually co-hosts this with Saurabh and Khyati, but this time, he was on the other side. I felt a bit like Uday Chopra, who is only in the film because he is the producer’s brother. Anyway, I think a good time was had by all as we covered a wide variety of topics - Enlightenment and why it didn’t happen in India (short answer: there wasn’t any need, really), why we write this newsletter (majboori) and the usual quota of Bastiat, Smith and Rorty (showing off). Do listen if you have time (of course, you do).Moving on. Here is a quick run-through of what’s gone on since my last post. Another US regional bank, Signature Bank, stared into the abyss with depositors making a run to withdraw their money as analysts looked around for large unrealised losses sitting on banks’ balance sheets. Fed officials spent their weekend hawking the other failed bank, Silicon Valley Bank (SVB), to potential buyers. But who in their right mind will buy out a troubled bank in these times? More so after all the trouble that the likes of JP Morgan Chase had buying out such banks during the financial crisis of 2009. Running out of options, the Fed, the Treasury and the Federal Deposit Insurance Corporation (FDIC) announced an unprecedented bailout of all depositors of SVB and any other bank that will be in a similar hole in future. Simply put, FDIC will guarantee all deposits and not just those below $250,000 for which there’s insurance. To be sure, the equity shareholders and those holding unsecured corporate bonds won’t be bailed out. They will lose their shirts. So, this isn’t a repeat of the 2009 bailouts. The Fed then went a step further to address the root cause of the problem. Banks are sitting on huge held-to-maturity (HTM) losses on the securities they hold because the interest rates have moved too far up too quickly. And they have a liquidity issue if there are continued withdrawals from the depositors. If they sell their securities today to meet their commitments to give depositors their money when they ask for it, they will have to sell them at a loss. This substantial loss will mean they will need to raise capital from shareholders to keep themselves solvent as per Fed requirements. But who will give them money in this market? Uninsured depositors who play out this game-theory scenario in their minds will therefore withdraw more of their money. Ideally, if they play the scenario right as a collective, they shouldn’t. But as individuals, they will make a run on the bank. Soon, the bank will be in a death spiral, and this is what happened at SVB and Signature Banks. The last-minute solution devised by Fed was the creation of what’s termed the Bank Term Funding Program (BTFP). Here’s how Fed sees BTFP:“The additional funding will be made available through the creation of a new Bank Term Funding Program (BTFP), offering loans of up to one year in length to banks, savings associations, credit unions, and other eligible depository institutions pledging U.S. Treasuries, agency debt and mortgage-backed securities, and other qualifying assets as collateral. These assets will be valued at par. The BTFP will be an additional source of liquidity against high-quality securities, eliminating an institution's need to quickly sell those securities in times of stress.With approval of the Treasury Secretary, the Department of the Treasury will make available up to $25 billion from the Exchange Stabilization Fund as a backstop for the BTFP. The Federal Reserve does not anticipate that it will be necessary to draw on these backstop funds.”If you didn’t have any background to this situation and just read the above note from the Fed, you’d be forgiven if you thought here was a central bank of a developing world economy figuring out a short-term jugaad to solve a crisis at hand. But the Fed didn’t just stop here. After all, like the Queen in Through The Looking Glass, it can believe in six impossible things before breakfast. Leaving their struggles to find a buyer for Signature Bank behind, they put together a unique Barjatya style “hum saath saath hain” deal and nudged a number of banks to do their bit to shore up confidence in the banking system: (as CNBC reports)“A group of financial institutions has agreed to deposit $30 billion in First Republic in what’s meant to be a sign of confidence in the banking system, the banks announced Thursday afternoon.Bank of America, Wells Fargo, Citigroup and JPMorgan Chase will contribute about $5 billion apiece, while Goldman Sachs and Morgan Stanley will deposit around $2.5 billion, the banks said in a news release. Truist, PNC, U.S. Bancorp, State Street and Bank of New York Mellon will deposit about

#204 The Distant Roll Of Thunder

Global Policy Watch: Accident Ho GayaInsights on global policy issues relevant to India— RSJI must admit there are times when I have made a big deal about writing this newsletter. Not about the content, mind you. I’m not that vain yet. But the regularity of it all. Getting about 4000 words out between the two of us every week isn’t trivial stuff. But then there are weeks I ask myself if it is really a big deal. I mean, there are weeks when there’s so much happening in policy, politics and macro spheres that things just write themselves. I have been in what could be called writing self-help groups where people bemoan their writer’s blocks and the soul-crushing experience of staring at a blank word document with the cursor blinking. To them, I have two pieces of advice. Switch to writing on public policy. And don’t bother much about quality (speaking for me here, not what Pranay produces). Voila! You get something like 50% of this newsletter.Anyway, coming back to this week. Sometime midweek, I thought it might be a good idea to write about the state of opposition in India in the light of Rahul Gandhi’s Bharat Jodo Yatra and his media engagements in Oxford. There’s always space for the opposition in India despite the brutal electoral majority of the party in power, as we have seen in the past. This was evident during the yatra. What is also evident now is that there’s a complete lack of understanding on the part of Rahul Gandhi on issues that can animate the electorate. So, he can only hope for the party in power to hit self-destruct mode to score an electoral victory. What’s worse is he has terrible ideas of his own and a tin ear for good advice. His acolytes defend him saying he’s sincere. I can only say when you combine sincerity with bad ideas, you get demonetisation and instant lockdowns. Back to the point. As I was thinking of writing about this, news came in of Manish Sisodia, the deputy CM of Delhi, being taken into custody by ED for what’s being called the liquor scam. Liquor policy in various Indian states is a gift that keeps giving. We love talking about it. What I also thought was admirable is the agile way the ED functions these days. Like some start-up in Koramangala. It is always hustling. These were the ideas I was toying with till a bank with a balance sheet size of US$ 200 billion (a tad smaller than HDFC Bank) collapsed in the US. And, so, served on a platter was another possible post on what could go wrong in the global economy. I’m afraid Rahul Gandhi, Sisodia, and liquor will have to wait for another day. I would like to discuss the aptly named Silicon Valley Bank (SVB) that has gone from boom to bust in less than two years.Here’s what has happened since Thursday. WSJ reports:“On Wednesday SVB said it had sold a large chunk of its securities, worth $21 billion at the time of sale, at a loss of about $1.8 billion after tax. The bank’s aim was to help it reset its interest earnings at today’s higher yields, and provide it with the balance-sheet flexibility to meet potential outflows and still fund new lending. It also set out to raise about $2.25 billion in capital.Following that announcement on Wednesday evening, things seemed to get even worse for the bank. The share-sale announcement led the stock to crater in price, making it harder to raise capital and leading the bank to scuttle its share-sale plans, The Wall Street Journal has reported. And venture-capital firms reportedly began advising their portfolio companies to withdraw deposits from SVB.On Thursday, customers tried to withdraw $42 billion of deposits—about a quarter of the bank’s total—according to a filing by California regulators. It ran out of cash.”Looks like a good old run on the bank. The regulators had to step in. Again from WSJ:“The Federal Deposit Insurance Corp. said it has taken control of the bank via a new entity it created called the Deposit Insurance National Bank of Santa Clara. All of the bank’s deposits have been transferred to the new bank, the regulator said.Insured depositors will have access to their funds by Monday morning, the FDIC said. Depositors with funds exceeding insurance caps will get receivership certificates for their uninsured balances, meaning businesses with big deposits stuck at the bank are unlikely to get their money out soon.”If you’ve been reading me over the past month, I have made three points. One, it is foolish to assume that the Fed will pause on rate hikes anytime soon. Inflation isn’t transitory in the US. And this was made clear this week when the Fed Chair, in his response to the questions from the Senate Committee on Banking, said that interest rate hikes are “likely to be higher than previously anticipated” and that because of it, the labour market is also likely to weaken in the near term. Like I have said before, it is best that markets, banks and companies plan for scenarios where the rate goes up to 7 per cent to stress test their models. This holds for India too. Two,

#203 Economic Growth and Voter Preferences

India Policy Watch #1: Why We Don’t Care About GrowthInsights on burning policy issues in India— RSJEarlier this week, Pranay and I recorded an episode with Shruti Rajagopalan for her podcast Ideas of India. I have been following Shruti’s columns and the podcast for a while now, and I will recommend you subscribe to both her podcast and her newsletter. She’s always insightful, curious and uses first principles to probe issues. This means you cannot get away with the usual stock answers. One of the questions we discussed at length was why does the Indian electorate not prioritise growth while making their choices at polls. It is an interesting contention whose premise itself can be questioned. How can we conclude that they don’t? And then, if we assume for a moment they don’t, why do they not? I won’t spoil your experience of listening to the episode by going into the details of what we discussed. But I will cover some ground in today’s edition on why it seems that people in India don’t care about economic growth. And as it often happens in life, this discussion happened in the same week when India published its GDP estimates for the quarter Oct-Dec, 2022. So what I will do today is cover the data released by the National Statistical Office (NSO), take a wider view of what’s happening with the economy and round it off with that question that Shruti asked.Here’s the headline news on growth: From the ET:“India’s gross domestic product (GDP) for the October-December quarter moderated to 4.4 per cent from 6.3 per cent in the previous quarter, data shared by the Ministry of Statistics and Programme Implementation showed on Tuesday. The GDP has now moderated from 13.5 per cent in the first quarter of FY23 largely due to pandemic-related statistical distortions.Lower GDP growth can also be attributed to aggressive rate hikes by the Reserve Bank of India in order to tame the high inflation. In addition to these factors, the slowdown in exports and consumer demand has also contributed in bringing down the numbers. The dent in consumer demand can be linked with the bullish rate hikes by the central bank to bring down inflation in the past few months. Meanwhile, slowdown in external demand could be a consequence of the rate hikes by major central banks around the world.”Apart from this, the NSO made revisions to the GDP numbers for FY 22, FY 21, FY 20 and to the first two quarters of this FY. Heh! I’m reminded of that famous quip by a former RBI Governor, ‘In other countries the future is uncertain, but in India even the past is uncertain’. The growth numbers came in as a negative surprise. What’s worse, manufacturing showed a contraction for the second quarter in a row. Not a great sign when the government has been pushing for companies to set up a base in India and eyeing that ‘China+1’ pie. The WSJ had a summary of the key signs of worry in the Indian economy:“Weakness in private consumption stood out the most. India’s private consumer spending, which comprises about 60% of India’s gross domestic product, rose just 2.1% year over year, compared with an 8.8% increase in the September quarter. It was mainly hurt by higher interest rates and elevated inflation. Slower growth in rural spending after some pandemic-era subsidies were cut could have also played a role.A closer look at other numbers in the GDP data also paints a worrisome picture. Import growth fell more sharply than export growth, again signalling weak domestic demand. And while fixed investment growth was a relative bright spot, it still slowed for the second quarter in a row.Nomura economists Sonal Varma and Aurodeep Nandi think markets are still significantly underappreciating the risks to India’s growth. They say the country’s growth cycle has peaked, and a combination of weaker global growth and tight domestic and global financial conditions could spell further trouble for exports, investment and discretionary consumption.”So, what should one make of this data? There’s clearly a moderation of growth. Some of it is expected because of the base effect of the pandemic years and the upward revision to growth done for the previous years. It is also true that global demand is weak, so exports will be sluggish for a while. On the other hand, manufacturing growth remaining weak despite all the PLI and ‘Make in India’ efforts should worry policymakers. Domestic consumption is starting to feel the impact of rate hikes, and the liquidity situation remains tight. Of course, the data can be spun the other way too. The NSO has maintained its 7 per cent growth forecast for the full year, which implies a 5.1 per cent growth in Q4. Inflation is subsiding, and it is likely that after the potential April rate hike, we will have a pause unless global factors come into play. Also, an expected good monsoon and China opening up post its Zero Covid madness will mean domestic and global demand will be back. So, it is all a mixed bag if you just go by quarterly numbers.I thoug

#201 Blocking out the Sun

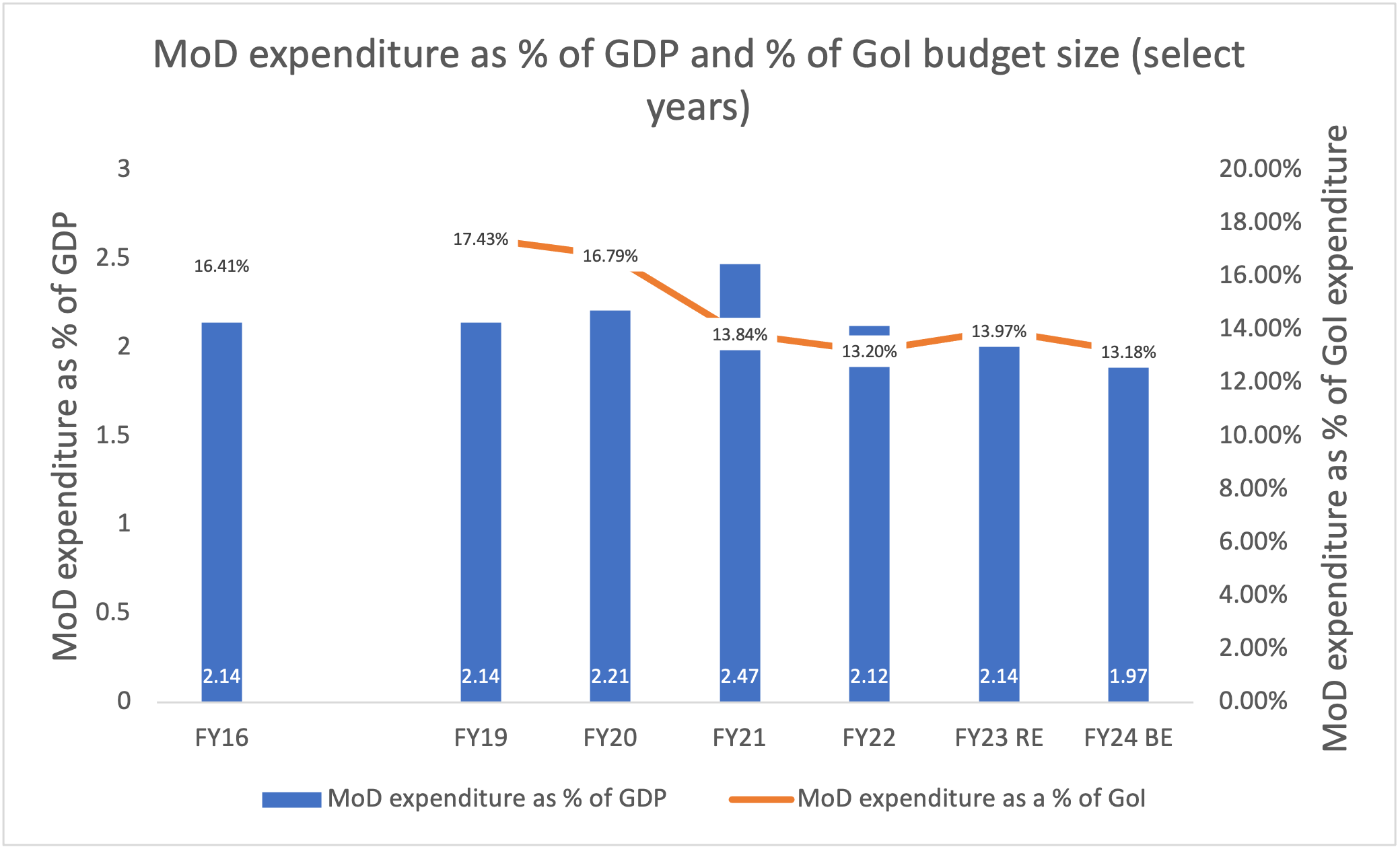

India Policy Watch #1: What Do Successive Defence Budgets Reveal?Insights on burning policy issues in India— Pranay Kotasthane(An edited version of this article was published in Hindustan Times on 13th Feb)Another defence budget zoomed past us on Feb 1. Since then, analyses have focused on how the defence spending for the coming year departs from the last year. Some have waved a red flag as defence spending has fallen below 2 per cent of GDP for the first time in many years. On the other hand, the defence ministry’s post-budget press release emphasised a 44 per cent increase in operational spending, which is expected to “close critical gaps in the combat capabilities and equip the Forces in terms of ammunition, sustenance of weapons & assets, military reserves etc.” The ministry also highlighted that the capital outlay for modernisation and infrastructure development has risen by a seemingly handsome 57 per cent over the last five years. How, then, do we make sense of these conflicting narratives?Comparing allocations with those in the previous year gives us a confusing picture. Every interest group can pull up a number from the budget to suit their pre-formed narrative. Taking a step back from these narratives, this article will show that this was another run-of-the-mill defence budget, just like the previous one was. Nothing in it indicates any significant change in the defence posture. Unlike Japan, which has announced a doubling of its military spending in the next five years, India’s approach is about gradually improving the operational efficiency of the armed forces.Looking under the hoodThis article looks at the defence expenditure over the last six budgets to make sense of the numbers. To put numbers into context, let’s use an earlier year (FY16). FY16 is a useful reference point as it predates two major developments: China’s visibly aggressive posture on the border and the budgetary commitments arising from the One Rank One Pension (OROP) scheme. Three observations follow from such an analysis.One, not only has defence spending fallen as a proportion of GDP, but it has also fallen as a percentage of government expenditure. In other words, defence has slipped in priority relative to non-defence functions (Figure 1). Two, the China challenge hasn’t led to any spectacular change in the composition of defence expenditure. Defence spending can be divided into four major components: salaries, pensions, capital outlay, and others. As Figure 2 shows, capital outlay was being squeezed by rising pension expenditure over the last few years. For two consecutive years (FY19 and FY20), more money was spent on pensions than on capital acquisition and modernisation. The balance has now been marginally restored since FY21, after the Galwan crisis flared up.Crucially, the rises in pension and capital expenditures have come at the cost of operational and maintenance expenditures, including ammunition stores (under the Others category). It is hence not surprising that the latest budget is trying to arrest this decline in combat capabilities.Three, this period has been relatively better for the Indian Navy in terms of capital expenditure. Since the procurement of new platforms happens over multiple years, a temporal view is useful in analysing how capital outlay is split between the three armed forces. Figure 3 suggests that the big change in the last four years is in the capital outlay for the Indian Navy, with the FY24 figure having doubled in absolute terms since FY20.The Big PictureBy connecting these dots over the last five years, the picture that emerges is this: the government seems confident that China can be handled without a substantial rise in defence expenditure. The latest budget serves as a bellwether indicator for this claim. It was the first budget of the post-pandemic period, at a time when the economic prospects for India had improved considerably. The government achieved better-than-expected buoyancy in income taxes and GST in the current financial year, while the cooling of global fertilizer prices has led to a decline in the projected subsidy bill. Consequently, the government, for the first time in many years, had some fiscal room to play with. It has used that space to increase the overall capital outlay to Rs 10 lakh crore, almost three times the outlay in 2019-20. Despite this increase in the overall capital outlay, the defence budget resembles the middle overs of a one-day cricket match.From a financial savings perspective, there have been just two important changes over this period in the defence domain. The first was the announcement of the Agnipath scheme. It might reduce the pension burden, but these savings will reflect only after a decade-and-a-half. Other proposals, such as theatre commands, haven’t come to fruition yet. The proposal to create a non-lapsable fund for modernisation — a proposal the union government gave an in-principle agreement way back in Feb 2021, still hasn’t found a

#202 The Debt of the Future