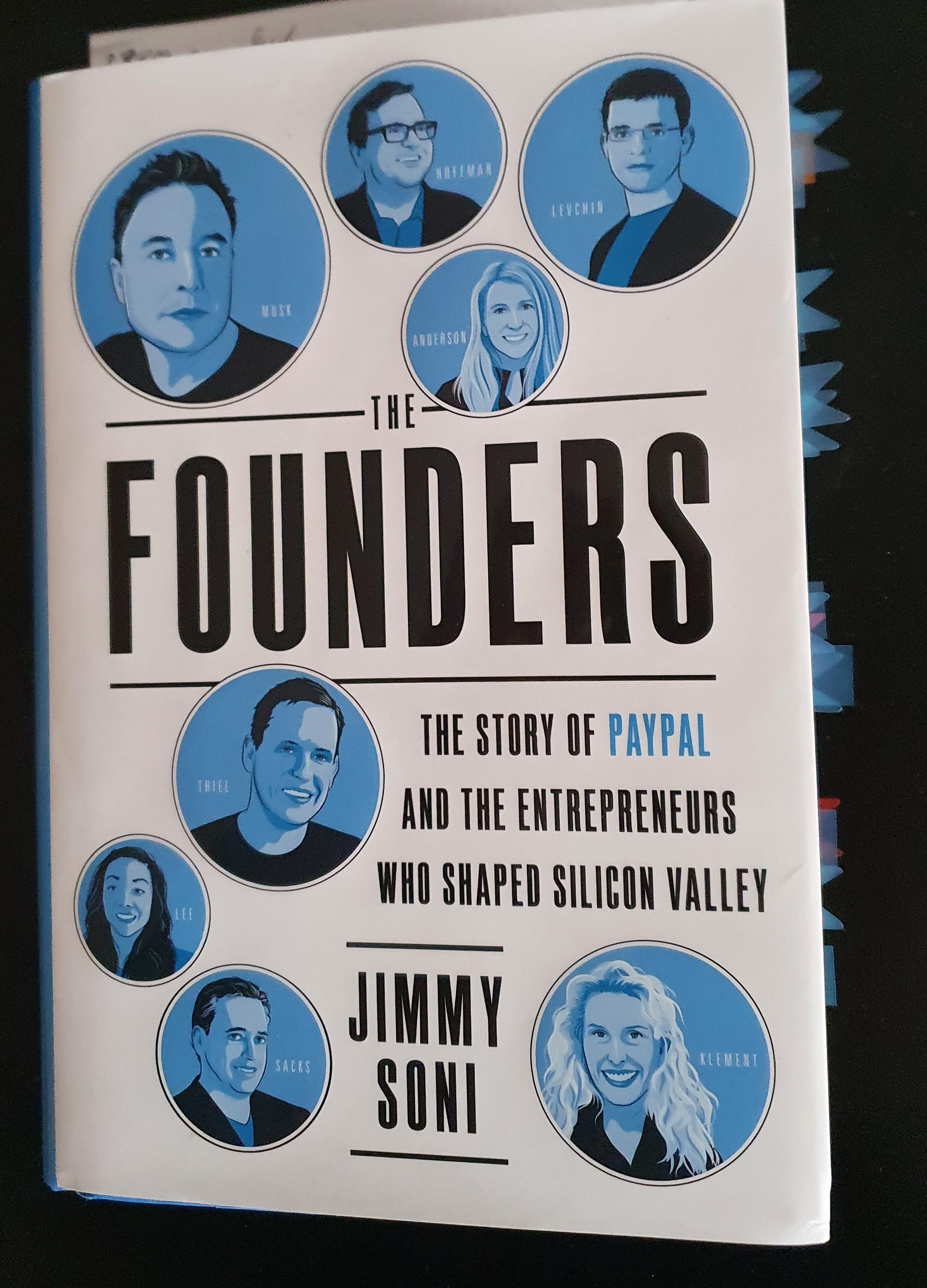

Frederik Journals

58 episodes — Page 1 of 2

Writing Stories Close to Life: Jared Dillian's Night Moves

I talk to author, trader, and DJ Jared Dillian about writing, lives, and his new collection of short stories: Night Moves. This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit www.frederikjournals.com/subscribe

🎙Audio: Searching for True Words

This is a free preview of a paid episode. To hear more, visit www.frederikjournals.comThe Art of Alchemy is a reader-supported publication. Become a paid subscriber to listen to the audio version of this post.

Lyn Alden: Studying the Financial System

My conversation with Lyn Alden, author of Broken Money.Twitter: @LynAldenContactDisclaimer: I write and podcast for entertainment purposes only. This is not investment advice. This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit www.frederikjournals.com/subscribe

Nervous System Mastery with Jonny Miller

I recently had the pleasure of speaking with Jonny Miller, writer, podcaster, and breathwork facilitator. Jonny wrote some of my favorite recent pieces, including the amazing operating manual for the nervous system and How to Pay Off Your Emotional Debt. Jonny also puts together terrific small wikis like this one on emotional resilience, the ‘spiritual MBA’ and Somalist (‘a global directory of somatic practitioners + trauma-aware bodyworkers’).We talked about breathwork and its benefits and risks (including Wim Hof), ‘state over story’ and the ability to change the state of your own nervous system, Jonny’s own journey, the $55,000 he spent exploring various modalities and experiences to find the most impactful ideas (including super interesting stuff like darkness meditation), emotional debt, repressed anger, and men’s work.In the context of a breathwork journey, incomplete reflexes will rise to the surface and they will be felt. The body will move in a certain way, and then there'll be relaxation. It's almost like layers of an onion that keep on unpeeling. The more we become comfortable with feeling the full spectrum of emotions, the more that these deeper pieces start to arise.We tend to focus on the outer journey, the how of success. How to spot opportunities, how to invest, how to build a business. Mastering the inner journey is equally important: both understanding your why and having the tools and practices to master the stress and setbacks along the way. That’s one of the lessons of the maze. Remember: great investors are survivors and experts at cultivating resilience.We have what I think of as this Cartesian hangover, almost going back to Descartes, of this mind-body dualism. I think the rational brain, the intellect, the kind of left-hemispheric way of perceiving the world has been very prioritized and almost worshiped in our culture.Controlling your mind, mastering your mind, mindfulness, all of these things have been really, really emphasized. I think what is starting to happen is the pendulum swinging back to, ‘oh no, there is no actual distinction between the brain and the nervous system.’ This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit www.frederikjournals.com/subscribe

Cultivating the Creative Seventh Sense with William Duggan

I had a chance to interview William Duggan, professor at Columbia Business School and author of Strategic Intuition. He explained how Kendo led him to his big idea, the difference between creative/strategic intuition and expert intuition (with examples including Howard Schultz, Henry Ford, and Elizabeth Holmes), and the roles of memory, passion, and presence of mind.Quotes that stuck with me:There is no now. Everything is history. … There is no other guide to the future.You don't have to have the passion before you have the idea. The idea gives you the passion. Oh great, this is what I'm gonna do.How do you judge an idea when you have it? Is it based on real knowledge and experience? Real pieces of the puzzle. That's how you judge.The moment you step into the battle, you forget everything. Meaning that you let your brain make the correct connections. That's the presence of mind, where your mind is clear. In martial arts, it's very fast, but it's really the same idea. It's to clear your mind and let your brain make its own connections, according to the situation and the circumstances.A lot of people think Henry Ford invented the assembly line. He did not. The assembly line was invented a hundred years before, at the start of the Industrial Revolution. He invented a certain kind of assembly line, meaning he put together the old assembly line with something new. I like to distinguish the natural flash of insight … Steve Jobs was good at it. He'd search and search and search and then something would strike him. I don't know if you know about the origin of Starbucks. Howard Schultz was working for a coffee company, high quality coffee, where you fill up your bag and take the coffee beans home. He goes to Milan for the first time in his life and he sees the coffee bar and he says, oh, okay, well we should clearly convert all our stores into that. This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit www.frederikjournals.com/subscribe

Escaping the Caterpillar Pillar with Jared Dillian

Hello everyone,I had the pleasure of chatting with Jared Dillian, author of The Daily Dirtnap and We're Gonna Get Those B******s, about his new book Those B******s. Years ago, I read his book Street Freak and I fondly remembered his wit, candor, depth of introspection, and keen eye for the antics of markets.Those B******s is a collection of Jared’s essays on life, death, meaning, friendship, marriage, luck, ambition, suicide, and much in between (including a few great bits on markets and finance). It’s refreshingly honest and fun and led to a lot of reflection.In our conversation we touched on writing and finding your voice, escaping the caterpillar pillar, how markets are ruled by fear, being the guy who knows a guy, mental health and the power of writing, making meaningful memories, the right temperament for markets, why people don’t change, and why you should ask people if they are lucky.A few highlights from the conversation:A lot of people think that markets sort of oscillate between fear and greed, right? But it really isn't fear and greed. It's fear and fear. It's all fear, right? Greed is fear of not getting something that you want. So working in the markets is, if you have any background in psychology, it's a very depressing place because the markets are filled with fearful people, like acting based on fear. But the thing is that it's very predictable. People behave in very predictable ways. So that's been my thesis about markets all along.I like to know lots and lots of people. Now, having a newsletter has been the perfect way to do that because a lot of times if I have a question about like air conditioning, I can put it in my newsletter and I get 20 responses. I know somebody who owns an HVAC company. I know people in all different kinds of industries and if I ever need help, I can reach out to them. I like to call that having a big world. I like to have a big world. I like to know lots of people. That's just my personal philosophy.I learned that people had similar experiences, they just would never talk about it. There are things you cannot talk about in polite conversation, but you can do it with words, you can do it on the page and you can bring people into this world. And that's the magic of it. My Substack is like a safe space for people to read this stuff and think about these issues, really the only place you can talk about 'em is with a therapist or something like that.The top five memories piece came from the show Lost. There's a character named Charlie and he has a premonition that he's going to die. He knows exactly when it's going to happen. And so he sits down and he starts thinking of his top five memories of all time.And it got me thinking like, that's actually a really good exercise. Like what are your top five memories of all time? I think one of mine was marching band in high school. One of mine was DJing. Really your goal in life should be to make more of those top five memories and keep doing that over and over again.I had a trade that made 15 million bucks. That was a great trade. But it doesn't make my list of top five memories, because top five memories are about relationships and achievement and things like that. Lehman was a great place to work, but ultimately that's not what we're here on earth for. This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit www.frederikjournals.com/subscribe

Escaping the Caterpillar Pillar with Jared Dillian

Hello everyone,I had the pleasure of chatting with Jared Dillian, author of The Daily Dirtnap and We're Gonna Get Those B******s, about his new book Those B******s. Years ago, I read his book Street Freak and I fondly remembered his wit, candor, depth of introspection, and keen eye for the antics of markets.Those B******s is a collection of Jared’s essays on life, death, meaning, friendship, marriage, luck, ambition, suicide, and much in between (including a few great bits on markets and finance). It’s refreshingly honest and fun and led to a lot of reflection. For a taste of Jared’s writing check out his excellent recent essay People Don't Change:People don’t change, until they do. What has to happen is that person has to hit bottom. Bottoms vary for different people—people with a high bottom get to keep their jobs and spouses. People with a low bottom have to lose everything before they learn.In our conversation we touched on writing and finding your voice, escaping the caterpillar pillar, how markets are ruled by fear, being the guy who knows a guy, mental health and the power of writing, making meaningful memories, the right temperament for markets, why people don’t change, and why you should ask people if they are lucky.Enjoy,FrederikYou can listen to our conversation on Spotify, Apple, anchor (and via RSS).A few highlights from the conversation:A lot of people think that markets sort of oscillate between fear and greed, right? But it really isn't fear and greed. It's fear and fear. It's all fear, right? Greed is fear of not getting something that you want. So working in the markets is, if you have any background in psychology, it's a very depressing place because the markets are filled with fearful people, like acting based on fear.But the thing is that it's very predictable. People behave in very predictable ways. So that's been my thesis about markets all along.I like to know lots and lots of people. Now, having a newsletter has been the perfect way to do that because a lot of times if I have a question about like air conditioning, I can put it in my newsletter and I get 20 responses. I know somebody who owns an HVAC company. I know people in all different kinds of industries and if I ever need help, I can reach out to them. I like to call that having a big world. I like to have a big world. I like to know lots of people. That's just my personal philosophy.I learned that people had similar experiences, they just would never talk about it. There are things you cannot talk about in polite conversation, but you can do it with words, you can do it on the page and you can bring people into this world. And that's the magic of it. My Substack is like a safe space for people to read this stuff and think about these issues, really the only place you can talk about 'em is with a therapist or something like that.The ‘top five memories’ piece came from the show Lost. There's a character named Charlie and he has a premonition that he's going to die. He knows exactly when it's going to happen. And so he sits down and he starts thinking of his top five memories of all time.And it got me thinking like, that's actually a really good exercise. Like what are your top five memories of all time? I think one of mine was marching band in high school. One of mine was DJing. Really your goal in life should be to make more of those top five memories and keep doing that over and over again.I had a trade that made 15 million bucks. That was a great trade. But it doesn't make my list of top five memories, because top five memories are about relationships and achievement and things like that. Lehman was a great place to work, but ultimately that's not what we're here on earth for.A few quotes from Those B******s:As a trader you must have the memory of a goldfish. You f**k something up, you clean up the mess, and move onto the next trade. There is always another trade.This is something they teach professional athletes. It was said that Derek Jeter was the best at doing this- he did not dwell in the past. He had absolutely no memory, and was out there hacking at his next time up at the plate. We all have slumps. It's about your ability to shake it off, rub some dirt on it, and get back in the game.If you are to be successful, pray that it happens very slowly. Peaking early isn't just true in high school--it's broadly true throughout life. You see this a lot on Wall Street. Good performance is difficult to sustain over any period of time. Early success leads to hubris which leads to mistakes.After a few successively smaller fund launches, you end up as a CFP in Evanston, Illinois. I was 34 years old at Lehman Brothers and still a vice president. A 34-year-old VP. Many people are surprised to hear that. Well, most of the guys I worked with are now selling insurance.I'm not a snob and I don't look down on people, but I did resent people dumber than me getting paid more for work that required less technical sophistication. But as time

So Far, So Good: Roy Neuberger's Long Walk Down Wall Street

"What first led me to Wall Street was a desire to make money so I could buy great art and support artists. What I didn't know when I started is that working on Wall Street can be a fascinating art in itself and one for which I was almost immediately suited." — Roy NeubergerDISCLAIMER. I write and podcast for entertainment purposes only. None of this is investment advice and any information contained in my work should not be relied on to make investment decisions. Do your own work and seek your own financial, tax, and legal advice before making any investment decisions. This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit www.frederikjournals.com/subscribe

Drew Cohen of Speedwell Research: Deep Research and Business Counterfactuals

Disclaimer: None of this is investment advice. I write and podcast for entertainment purposes only and this conversation reflects our personal opinions. It should not be relied on to make investment decisions. Do your own work and seek your own financial, tax, and legal advice before making any investment decisions. Also see Speedwell’s Disclaimer.Drew and I talked about Meta, Constellation, Floor & Decor, Restoration Hardware, and his research and writing process. I will share excerpts from the conversation and Drew's work on the substack.Drew Cohen writes at Speedwell Research and is a Portfolio Manager at Davidson Kahn Capital Management. Prior to Davidson Kahn, Drew was at Capital Group, where he helped managed $5B+ of AUM. Prior to his role at Capital Group, he worked at Goldman Sachs in New York in their Global Investment Research division. This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit www.frederikjournals.com/subscribe

🎙Podcast: Paul Podolsky and The Paradox of Financial Fiction

Hello everyone,I’m usually skeptical of fiction involving financial markets. To make it thrilling and get life and death stakes, the genre typically blends with crime or conspiracy. Which means you need an engaging writer who knows both worlds well enough and doesn’t turn the financial combatants into caricatures.But there are surprises. During my recent trip, I churned through Master, Minion by Paul Podolsky who also writes the Things I Didn’t Learn in School Substack. Master, Minion is a fast-paced and thought-provoking thriller at the intersection of financial markets, geopolitics, and intelligence agencies. Paul started his career in Russia, worked on Wall Street for 20+ years, most of that time at Bridgewater, and spent a lot of time in China as well. He brought all of that to bear in the book.The story weaves together hot spots from Moscow to Hong Kong and, yes, Boston, with a wonderful depth of detail and cultural observation. Paul’s depiction of the “verbal kung fu” and politics in his fictional hedge fund is priceless. But his real strength is to paint compelling characters ensnared in their respective systems of money and power.After reading his book and Substack, I reached out to Paul and am excited to share our conversation.If you can just take one thought with you this Sunday, consider his metaphor for life, the flow and the eddies. The eddies being the loops in which can get stuck in without being aware of it. When I asked him about it, I realized he was the living embodiment of the lessons from Tim Urban’s The Tail End:One of the reasons I left Bridgewater when I was 52, I calculated how many months I was gonna live. I literally looked at an actuarial table. I think when I left Bridgewater, I had 384 months to live, statistically speaking. And there's a pretty wide range around that, if it's an individual.I thought about that. These 384 months are gonna come. There's nothing I can do. That is just the flow. How do I stay in that for myself? It's very hard to see, at least it was very hard for me when I was young. You have to listen carefully. What is that real thing that works for you?There's a period of time where I had no money and I had a young family. Money really, really made a difference, to try to make a comfortable tent, if you will, to sort of shelter them. But a little bit like you, I was thinking inside, this isn't the primary thing that motivates me. If I've got a million bucks now, if next year I have a million dollars and a hundred thousand, and the year after that I have a million dollars and two hundred thousand, that does not actually motivate me. And those months are going by. It's going 383 and 382 and 381… There are eddies that you could get stuck at in life.We talked about Paul’s journey to writing, his book, intrigue and investing in emerging markets, understanding Russia, and much more. You can find a few quotes below. I hope you’ll enjoy the conversation. I certainly did and look forward to reading more of Paul’s work in the future.You can listen to this conversation on Spotify, Apple, YouTube, anchor, and via RSS.The information in these posts and on this website is not and should not be construed as investment advice.The paradox of writing fictionThe strange thing about fiction is, there's a weird paradox. On the one hand, you're making stuff up. On the other hand, it's sometimes easier to say something true by making something up.In the real world, you never quite know what other people are thinking. You have a hypothesis. Fiction allows you to create a bunch of characters and imagine their interior world, which is where so much of the mystery and the richness of life is.A few quotes that stuck from the book (no spoilers):Working at a hedge fund:Everyone understood the Boss had money, they, the hangers-on, me included, wanted that money and we all tried to destroy each other to get it. If [the CIA] was a team, this was Lord of the Flies.The Boss said he liked disagreement, but almost everybody was too scared to disagree.Understanding certain emerging markets:The idea that the state itself was criminal was something Americans had trouble getting their mind around. But the Boss might understand. In the Boss’s mind, there were predators and prey, and he had dedicated his life to joining the ranks of the predators. Wealth was a precondition.Institutions are people:But the Fed is people and people are wired the same everywhere—ambitious, striving for greatness, prone to error, guilt-ridden.Great investors understand impermanence:Most people tend to look at what they are growing up in and think that it is normal, he said. To them it is normal that the US is the richest country. Normal that China is poor. Normal that Black people are poor and white people are rich. But the reality is, things change. Nothing is stable.Magic in markets:The signaling felt like primates establishing hierarchy. While the central bankers had the magical power to make the economy expand or contra

Paul Podolsky and The Paradox of Financial Fiction

My conversation with Paul Podolsky author of Master, Minion and the Things I Didn’t Learn in School Substack. This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit www.frederikjournals.com/subscribe

🎙Audio Repost: Watching Game Tapes of History’s Best Entrepreneurs with David Senra

Hello everyone,A few months ago, I had the pleasure of interviewing David Senra, host of the Founders podcast. David is incredibly high energy and authentic about what he does. You think Mohnish Pabrai takes the idea of cloning seriously? Here’s David:I can live the rest of my entire life never having one original idea. As long as I’ve mastered the handful of ideas that I see as recurring themes in the history of entrepreneurship, I will live a fantastic life. Because it's not only knowing this stuff, but also actually applying them.To paraphrase Bruce Lee, fear not the man who has read 10,000 books once but rather the man who has re-read the best ones over and over. Or, in David’s case, the man who does both.David sticks to Munger’s maxim of taking a simple idea and taking it seriously:The greatest entrepreneurs had one idea. They built everything around that one idea. There might be things that spawn off of that idea later on. There are other businesses that can grow out of that, other business lines, other products. But fundamentally, they start with an idea.In David’s case it’s podcasting and a vein of high quality information that he mines and converts into an attractive product. Actually, it’s a combination of two big ideas: a big wave to surf (podcasting) and a big insight about David himself (love of reading and learning, ability to go deep in one area without burning out).I hope you enjoy the conversation and pick up some valuable ideas from his entrepreneurial heroes (and villains…).Reading a book is a movie for the mind. It's impossible to read a life story of an interesting person and not be involved emotionally. You're with them in their ups and downs. It's a predictable human reaction that you put yourself in their shoes.You can listen to this conversation on Spotify, Apple, anchor (and via RSS) or find a full transcript at Compound.If you’re looking for an all-in-one solution to manage your personal finances, Compound can help (disclosures).A few things I learned from David:Building a company can require an illogical amount of persistence.James Dyson "has 14 years of struggle. He builds 5,127 prototypes. He mortgaged his house. Some days, after doing all these experiments, he's climbing into bed at night covered in dust, crying at how painful what he's trying to do. It's 14 years and 5,127 prototypes before he has a vacuum of his own design, that he owns completely, that he could start selling to the public.We know at year 14 he's going to have success. What about year three? What if he stopped right here? That makes perfect sense. This is why it's so difficult. It is the logical decision. He should have stopped there, but he didn't. The founder is the guardian of the company's soul.I covered the biography of this guy named Sidney Harman. If you ever get into a luxury car, you'll see speakers that say Harman Kardon. He winds up writing this fantastic autobiography. He's 80 or 90 years old when he's writing it. It's called Mind Your Own Business. In that biography he's distilling 50 years. We haven't even been alive for 50 years. This dude had been trying to build companies, successful and unsuccessful for 50 years. Imagine what he knows.He gave the best description of what I feel is the founder’s role. The founder is the guardian of the company's soul.You cannot be the guardian of your company unless you love it. Edwin Land, Enzo Ferrari, and Steve Jobs, they talk about their products the way you would describe your lover. It's not the same as, I made a toaster, here's the toaster. No, they describe it like they're in love with what they've done.No one would have known Walt Disney's name if he’d started Disney and sold it five years later.There is this weird mind virus. I have an idea, I'm going to start up, I'm going to scale up, I'm going to sell, and then I'm going to do that over and over again. Inevitably, the question is who are the entrepreneurs you look up to? Who are your entrepreneur heroes? And they start listing off people that literally worked in the same company forever. I don't understand. Are you learning from these people or not? Because no one would have known Walt Disney's name if he started Disney and sold it five years later. No one would know Job’s name if he just got kicked out of Apple and then disappeared.The value of compounding knowledge.An investor understands the power of compounding. Knowledge compounds, too. Imagine going back and trying to talk to Warren Buffett about everything he knew at 35 compared to what Warren Buffett knew at 80. That's not the same person. I've read 272 biographies of entrepreneurs so far. I have a unique set of knowledge there. It's going to pale in comparison to what I will know two decades from now or three decades from now.Studying the birth of industries.Henry Ford had an idea. I want to build an easy, reliable car that the average person working at Ford can actually afford. That was unheard of. … Edison says something that changes

Watching Game Tapes of History’s Best Entrepreneurs with David Senra of Founders Podcast

This conversation was originally published at Compound. This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit www.frederikjournals.com/subscribe

🎙Audio Repost: Josh Wolfe. Using Doubt as Fuel and Bootstrapping an Enduring Partnership

Hello everyone,A few months ago, I finally had the chance to record a conversation with Josh Wolfe of Lux Capital. This was published at Compound (I also previously profiled Josh).Josh has been a frequent podcast guest and I did a lot of prep work to find questions he hadn’t tackled yet. As a result, I think it’s a timeless conversation with the exception of a brief discussion of the macro cycle (Josh and Lux were bearish and cautious before markets turned down).Josh and his partners were young with an unconventional background when they bootstrapped Lux. With little capital under management they earned additional cash flow through a research business.We sold [the report] for $4,750 bucks a copy, sold a few 100 of them and helped keep our little business alive. I got access to all these famous CEOs and VCs. Vinod Khosla was one of the first VCs to buy it. And I was like, Okay, I'll sell it to you, but only if I can come and meet you. So I went out to Sand Hill Road and I remember his office, I remember viscerally what it looked like, it was the first major billionaire VC I met.I absolutely loved his comments about using doubt as motivation and fuel.Anybody that doesn't believe in you, either you let that bring you down, or it becomes fuel. To this day, we like to say that we believe before others understand. Because there really is something powerful, just psychologically, of believing in somebody.I would be on a run on a treadmill, and I'd be getting tired. And I would imagine some of these heroes cheering me on. ‘You can do it, come on.’ I have ghost images of these individuals to cheer me on. Peter and I would find strength in the people that didn't think we were going to make it and felt really motivated to prove correct the people who did.It’s also a framework he uses to assess founders. Chips on shoulders put chips in pockets as he likes to say.The best entrepreneurs we see are the ones who are so obsessed to prove other people wrong who don't think this is possible. That to me feels honest.It feels petty, but it's real.I also admired Josh’s focus on his family. It’s easy to neglect that if you’re highly competitive.Being with my kids is just the great salve. … Family stuff for me is very cathartic. Whatever is going on, I could be negotiating a big financing. And my little guy who's six is like, Dad, I can't get the screw into this thing and that is more important. Getting the screw into the little toy is more important at that moment. That to me is a big thing.Thank you for listening and happy holidays🎄🕎You can listen to this conversation on Spotify, Apple, anchor (and via RSS) or find a full transcript at Compound.If you’re looking for an all-in-one solution to manage your personal finances, Compound can help (disclosures).A few things I learned from Josh:Why does a VC spend so much time on macro?Ignorance of the macro is no virtue. … We're trying to get a palpable sense for what massive currents are shaping the environment. … The number one determinant of future returns is never the hockey stick curve that some consultant or bank or optimistic entrepreneur shows. It's how much capital is going into a sector when capital is abundant.Lessons from living through two cycles.There are lots of differences, but the market sentiment similarities make me think that we're in Q3 of 2000. You're going through the Kubler-Ross five stages of grief … Markets have to go through that, both individually as investors, and then collectively. That's our guiding playbook at the moment.Use your struggles to grow and build intrinsic motivation.Almost every step of the way, there was some moment when we were running out of cash. I still remember the people that told me no for $250,000 checks or dragged me for six months doing diligence on data that didn't even exist to tell us that they were writing a $100k check. That was a formative thing because it shaped the kind of people that we want it to be when we pay it forward. You need struggle and you need people that doubt you so that you can prove them wrong.Networking at the beginning of your career.I remember I wanted to get in touch with some famous investor. I was like, You'd be doing me the biggest favor if you can introduce me to him. And he was like, stop, right there, stop. I thought I insulted him. Maybe this ask crossed the line?And he's like, Do you believe in yourself and what you're doing? And I was like, Yeah. And he's like, Do you think anybody else knows what you know in this particular field? I'm, like, No, I feel like I'm one of the best. He's like, so who's doing who the favor? It was a little bit of a mindset switch, even if you're slightly deceiving yourself to get over that absence of confidence.And the same way that when there's a task that you don't want to do, thinking, I get to do this, because you could be dying tomorrow, versus I have to do it. That was a real confidence booster. Not arrogance but, I'm doing these people a favor by both showin

Josh Wolfe, Lux Capital: Macro, Mentors, Motivation

You can find a full transcript of this conversation at Compound. This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit www.frederikjournals.com/subscribe

🎙 Audio Repost: Patrick O'Shaughnessy. World Building with the Most Interesting People

Hello everyone,A few months ago I had the pleasure of interviewing Patrick O’Shaughnesssy, the prolific host of Invest Like The Best, as part of my work for Compound.We started our conversation on the topic of David Senra, host of the amazing Founders podcast, who had just joined Patrick’s Colossus podcasting platform. David is one of the most focused people I know. Patrick one other hand is prolific but involved in a variety of efforts. Aside from podcasting, there is his venture capital firm Positive Sum, he is the CEO of O’Shaugnessy Asset Management, and he co-hosts Capital Camp. “Having a singular goal that's far in the future, that kind of crowds out serendipity and discovery along the way, is just not my style.”I was very interested in finding the unifying themes and the philosophy behind his work. Curiosity is a big driver for Patrick.“The reason I started my podcast was that I was frustrated by how imprecise even the best book on a topic was, as it related to my specific questions and curiosities. When I went to the world's best expert on whatever, I got exactly what I wanted quickly, with higher impact. I think if you wanted to learn about anything in the world, you'd be far better off, if you could get access to them, spending time with the world's leading thinkers on it and asking them questions directly, than by reading the five or 10 best books on that topic.”If Patrick is a fox, his mission is to find hedgehogs whose knowledge he can tap into.“It turns out that a podcast (a media business) and an investing firm are two really great things to have when your game is people-centric. Your game is effectively searching for interesting people. Being able to interview them and or invest in them are kind of the two most fun things to be honest with you. It's a great way for me to have a world around my interests. And in our investing activity, this is something we explicitly look for, we call it world building.”On the topic of David and Founders, Patrick hit the nail on the head. It’s electrifying to meet someone on a mission.“You find these people that are on one of these scent trails and will stop at nothing to stay on the trail. It's infectious. You finish a conversation with him, and you want to run harder at whatever it is you're running at.”You can listen to our conversation on Spotify, Apple, anchor (and via RSS) or find a full transcript at Compound (part I, part II).If you’re looking for an all-in-one solution to manage your personal finances, Compound can help (disclosures).A few things I learned from Patrick:Follow authentic curiosity and joy.“I don't know if there's a trick here. What you get on my podcast is just me. It's not a character I'm playing, it's just me, and that's a very sustainable strategy.”“I expect to do very well in the things that I do, not because I want some achievement badge, but because the process of doing that is joyful to me.”Conversation as a game.“To me, conversation is kind of like a game. I'm always interested in how much more interesting I can make a conversation that I'm in. I don't do small talk well. If I'm at a party, I'm always interested in how interesting something could get relative to the baseline.”Eastern philosophy as an operating system for life.“If you put a lot out there for others, with no expectation of a selfish return, you end up actually getting more than if you didn't do that. It's a strange worldview, because it's not a business school case study. The inputs and the outputs don't connect via some formula. You have no idea how it's going to come back to you.It is my form of faith. If I do this, it will come back. I have no idea how, but it will, and that's been my experience too. But if you were just trying to approach something strategically, irrationally, you would never behave this way because you can never tie the input to the output.” On working with founders.“Investors, I think, mistake a founder's desire for their capital for a founder’s desire for them, and all the things that come with them."“My experience is that founders want the capital to fuel their business, and they want someone that they can have as a confidant, that they can trust, that they can call when needed. But they don't want a steady stream of ideas and advice. The classic one is, have you seen this competitor yet? Some large percent of texts from VCs to founders is like the website of a competitor. What I think we can do is ask really good questions, the theme in my life, and not mistake what a customer actually wants from us for what we think they want.”The good life.“I optimize for learning, I optimize for freedom of time, to be with my family, especially. Learning, reading, talking to people, spending time with people, moving in the woods, ideally, or outside somewhere on the water somewhere with my family and my friends.Everyone has something they love, or a set of things they love, but very few people really work to protect those things. And to structure the

World Building with the Most Interesting People with Patrick O'Shaughnessy

You can find a full transcript of this conversation Compound (part I, part II). This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit www.frederikjournals.com/subscribe

Great Investors Build Networks and Never Stop Learning with Alix Pasquet III

Alix Pasquet III is the Managing Partner and portfolio manager at Prime Macaya Capital.Disclaimer: The information contained in this summary has been prepared solely for informational purposes and is not an offer to sell or purchase or a solicitation of an offer to sell or purchase any interests or shares in any of the funds managed by Prime Macaya Capital Management LP. Any such offer will be made only pursuant to an offering memorandum and the documents relating thereto describing such securities (the “Offering Documents”) and to which prospective investors are referred. This summary is subject to and qualified in its entirety by reference to the Offering Documents. An investment in those funds carries certain risks, including the risk of loss of principal. While all the information prepared in this presentation is believed to be accurate, Prime Macaya Capital Management LP makes no express warranty as to the completeness or accuracy nor can it accept responsibility for errors, appearing in the presentation. Other events which were not taken into account may occur and may significantly affect the returns or performance of the fund. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. This summary is provided to you on a confidential basis and is intended solely for the use of the person to whom it is provided. It may not be modified, reproduced or redistributed in whole or in part without the prior written consent of Prime Macaya Capital Management LP. This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit www.frederikjournals.com/subscribe

🎙Adam Mead, Author of The Complete Financial History of Berkshire Hathaway

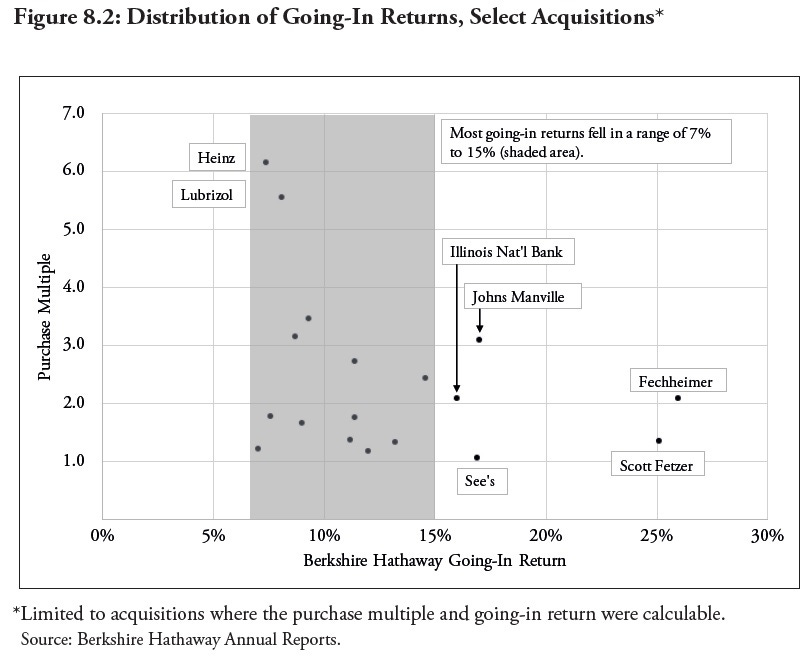

Hi everyone,The following is my conversation with Adam Mead, author of The Complete Financial History of Berkshire Hathaway. We talked about conglomerates, early entrepreneurial experiments at Berkshire, the lean years in the insurance business, managing the company as an informed observer, and returns on his acquisitions.As to finding another Berkshire, Adam was skeptical:“I'll never say never, but it would be highly unlikely to find another [Berkshire Hathaway]. You have a Lollapalooza, to use a Charlie Munger term, starting when they're able to shoot fish in a barrel.”You can listen to this conversation on Spotify, Apple, anchor (and via RSS).Disclaimer: I write and podcast for entertainment purposes only. This commentary reflects the personal opinions of myself and my guest. This is not investment advice. Acquisitions: going-in returns vs. reinvestmentThis is another chart from the book worth highlighting. Berkshire was not built on finding extreme outlier deals. Much depended on how capital was reinvested subsequently (whether in organic growth, further acquisitions, or public markets) and, of course, cheap leverage from insurance float.From the book: “In Berkshire’s early years, good companies were available for bargain prices. It bought the Illinois National Bank & Trust Company and The Buffalo News at book value, and the discarded Scott Fetzer and Fechheimer at premiums that still produced going-in pre-tax returns in the mid-20% range.Generally, the better the business was, the higher its price (as represented by purchase multiple paid compared to the company’s underlying value). The return on capital of the underlying businesses (the company-level return) ranges widely.See’s was one of Berkshire’s earliest purchases and was made when markets were not as efficient. The low Scott Fetzer and Fechheimer purchase multiples reflected that Berkshire could act as a safe port amid the leverage buyout storm of the mid-1980s.By contrast, Lubrizol and Heinz were excellent companies earning great returns on capital, but the price Berkshire paid reflected the market’s correct appraisal of that fact.”(I didn’t see it specified on the page but I think the numbers refer to return on equity and price/book).From the conversation: “You have this dynamic in the early days of finding really good businesses like See’s and having a pretty modest multiple. Good businesses at really good prices. Then you have the later days of buying really good or pretty good businesses at higher multiples because the market's just gotten efficient over time. But you still have the dynamic of reinvestment going on.Let's just use a plain example. If you had a business earning 30% on capital and you paid two times that capital, your going in return would be 30 divided by two, 15%. The important part is, if that business can grow, you don't have to reinvest at 2x the capital, you get to reinvest at 1x. That marginal capital gets, in this example, reinvested at 30%. That drags up your going in return over time. But I think Buffet's very clear in pointing out that you can't pay too much for growth. You can't have a going-in return of 2-3%, even if it grows enormously. The time value of money just destroys any kind of return that you have. I think he always looks for the good business and then he has a secondary analysis of what are the reinvestment opportunities. And he's fine, as long as the purchase price reflects it, he's fine taking the dividends and finding another place for them. And if the business can reinvest that capital, let's do that. That plays out in the extreme case of the energy business, where you're still getting, in many cases, 11-12% regulated return, which is nothing to sneeze at.”Conglomerates before Berkshire“The first sort of real conglomerate was American Home Products in the late 1930s. I do have some of those Moody’s reports on my website.They weren't crooks. I think that can kind of be misconstrued. These guys weren't the Enrons of their day trying to just put something over on investors. But they strayed a little bit in terms of messing around with the accounting or saying, gee, the market's valuing our conglomerate at 20 times earnings or 15 times earnings, and we're gonna buy this other company at five or six times earnings. And I can buy anything that I want as long as it's less than my P/E. And it's gonna magically transform my conglomerate into something better. Now the problem with that is it ignored the underlying economics.”Control vs. delegation“I think this whole idea of extreme delegation comes from the fact that Buffet and Monger started as stock pickers. What is the difference between owning a 5% position and owning a hundred percent position? You have the ability to direct the actions of that company. But should you? Berkshire was being almost agnostic in the sense of ownership level. We're still gonna let that manager run his or her business. We're only attracted to businesses that are good anyways. S

Adam Mead, Author of The Complete Financial History Berkshire Hathaway

My conversation with Adam Mead, author of The Complete Financial History of Berkshire Hathaway. This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit www.frederikjournals.com/subscribe

Julian Robertson: The Tiger Who Was a Wolf

You can find the full essay on Julian Robertson at: neckar.substack.com/p/the-tiger-that-was-a-wolf-lessons This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit www.frederikjournals.com/subscribe

🎙Audio Repost: Reflections on the Investing Process with Michael Mauboussin

You can listen to this conversation on Spotify, Apple, anchor (and via RSS) or find a full transcript at Compound.“This is the nature of what we do. It's the intersection of business and people and psychology and sociology and numbers. There's a lot of stuff that's always going on that makes sure you never have the game beat, never.”This past June I had the opportunity to interview Michael Mauboussin. I tremendously enjoyed this conversation and I believe it captures Michael’s deep curiosity and passion about investing, business, the research process, and being a multi-disciplinary learner.At the time I published a full transcript at Compound. I am happy that I can now share the audio version.I assume many of you are familiar with his work. For an easy introduction check out this 2021 profile. Another excellent piece is his Reflections on the Ten Attributes of Great Investors which incorporates many of his key frameworks. And be sure to check out his new website with a library of his collected writings.If you’re looking for an all-in-one solution to manage your personal finances, Compound can help. The firm can help diversify concentrated stock positions, optimize company equity, plan asset allocation, and more. You can sign up for access here.For more information, please check out further disclosures here.“Most investors act as if their task is to figure out a stock’s value and then to compare that value to the price. Our approach reverses this mindset. We start with the only thing we know for sure — the price — and then assess what has to happen to realize an attractive return. … The most important question in investing is what is discounted, or put slightly differently, what are the expectations embedded in the valuation?”The below are some of my favorite highlights.You can listen to the conversation on Spotify, Apple, at anchor, and via RSS or find a full transcript at Compound.Druckenmiller, Soros, and position sizing* “When you observe very successful people over very long periods of time in these probabilistic fields, they tend to have certain attributes that are worth all of us paying attention to.”* “Here we have George Soros and Stanley Druckenmiller, two legendary investors, who say that [position sizing] is the main thing that drives their returns and results over a long period of time. Whereas we look at the real world, we find that most people don't create a lot of value from sizing and it's all security selection. The question is can we bring those things together to some degree?”Analysts and portfolio managers:* “A very good portfolio manager will be able to focus on the two or three issues that matter most for a particular company. And they're very good at identifying those and honing in on those.”* “There was a letter from Seth Klarman at Baupost to his shareholders. He said, we aspire to the idea that if you lifted the roof off our organization and peered in and saw our investors operating, that they would be doing precisely what you thought they would be doing, given what we've said, we're going to do. It's this idea of congruence.”Holding Amazon for two decades* “I first learned about this company from Bill Gurley who at the time was part of the underwriting team at Deutsche Bank who did the IPO. Bill just said, you should meet these guys because the way they think about things, even though this is a completely nascent industry doing, completely different stuff, the language they're using is the language you're going to be familiar with.* “In the late 1990s, I met Jeff Bezos and Joy Covy, the CFO. … Joy would just say to me, we’re big fans of Warren Buffett and Charlie Munger. We think about return on capital. We think long term. We're making investments that appear to be bad, but when you pencil out the numbers, we think we're going to generate really attractive returns. I bought into that.”* “I was very influenced by a wonderful book by Carlota Perez that came out probably in the early 2000s where she talks about the interplay between technological revolutions and financial capital, one of the points she made was, it's often the case that the hard work happened after the financial bust.”On feedback, learning, and teams of superforecaster (aka investors)* “In every domain elite performers tend to practice. Every sports team practices, every musician practices, every comedian practices. What is practice in investment management? How much time should we be allocating to that?”* “The investment management industry is an industry that draws a lot of really smart people. It's a very competitive, interesting field. It's remarkable in the sense that feedback is very difficult to attain. In the long run it's portfolio performance and so on. But in the short run it's very, very difficult to do.”* “There's a distinction between intelligence quotient and rationality quotient, which is the ability to make good decisions. Along with some of his colleagues he developed a specific test to measure rat

Reflections on the Investing Process with Michael Mauboussin

This conversation was recorded in June 2022. You can find a full transcript at manual.withcompound.com. This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit www.frederikjournals.com/subscribe

Alix Pasquet: Learning for Analysts and Future Portfolio Managers

Alix Pasquet III is the Managing Partner and portfolio manager at Prime Macaya Capital. Notes on substack. Presentation on youtube.Disclaimer: The information contained in this summary has been prepared solely for informational purposes and is not an offer to sell or purchase or a solicitation of an offer to sell or purchase any interests or shares in any of the funds managed by Prime Macaya Capital Management LP. Any such offer will be made only pursuant to an offering memorandum and the documents relating thereto describing such securities (the “Offering Documents”) and to which prospective investors are referred. This summary is subject to and qualified in its entirety by reference to the Offering Documents. An investment in those funds carries certain risks, including the risk of loss of principal. While all the information prepared in this presentation is believed to be accurate, Prime Macaya Capital Management LP makes no express warranty as to the completeness or accuracy nor can it accept responsibility for errors, appearing in the presentation. Other events which were not taken into account may occur and may significantly affect the returns or performance of the fund. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. This summary is provided to you on a confidential basis and is intended solely for the use of the person to whom it is provided. It may not be modified, reproduced or redistributed in whole or in part without the prior written consent of Prime Macaya Capital Management LP. This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit www.frederikjournals.com/subscribe

🎙Marc Rubinstein of Net Interest: Fascinating Financials

You can listen to the conversation on: Spotify, Apple, at anchor, and via RSS.Hi everyone,I am a big fan Marc Rubinstein and his Net Interest substack and was very excited to finally record a conversation with him. Marc previously covered financials and fintech as a research analyst and hedge fund investor and now shares his takes on the sector with his readers on a weekly basis. It’s a very well written and insightful lens on a fascinating corner of the market.I spent the first couple of years of my career as an analyst at Macquarie Group dealing with financials - with leasing and lending companies which we acquired for my employer’s balance sheet. My view has been shaped by this early period of bargain hunting and I later struggled with fintech companies and their valuations. As Marc explains, financials are a unique sector with its own rules and heuristics where growth can be treacherous and the balance sheet is of supreme importance.It can be especially tricky to tell apart secular change from the credit cycle. As Jim Chanos said last week on Odd Lots, “every down cycle since ‘98 has seen those companies blow up, because it turns out they didn't have a better mousetrap. They just had the credit cycle at their back.”Marc and I talked about banks, fintech, the importance of incentives and culture, payments, the need to watch regulators, private equity and how alternative asset managers have been picking up business from investment banks, and the danger of relying on the view of CEOs too far removed from the risk.I’m going to share a few of my favorite writings by Marc followed by show notes. I hope you enjoy the conversation.Disclaimer: I write and podcast for entertainment purposes only. This commentary reflects a personal opinion, is not investment advice, and should not be relied on to make investment decisions. The views reflected in this commentary are subject to change at any time without notice. Do your own work and seek your own financial, tax, and legal advice before making any investment decisions.Why learn about financials?For a start, there’s something exclusive about them. There are some industries on which everyone has a view. Supermarkets for example, or consumer tech. Financials isn’t one of those industries…Second, financials are everywhere. Even companies that on the face of it aren’t, can be financial companies in disguise.The third aspect of financials that makes them especially compelling is they’re a great metaphor for the world around us. The financial system operates as a complex adaptive system. It consists of a network of banks and other financial institutions each of which operate according to their own incentives.Dotcom 2.0 (online brokers, asset managers, Silicon Valley Bank):I actually remember where I was the day the dot-com bubble burst. It was March 2000 and I was sitting in a newly-opened branch of Starbucks near my home in London, reading a copy of the Financial Times. …Commodities trading. In commodity trading, there are three ways to make money:Geographic arbitrage. Unlike financial markets, where pricing relationships are normally stable across regions, proximity to a product in the physical trading world can have a big impact on pricing. Commodity trading firms can leverage logistical capabilities to source product in one location and deliver in another, taking advantage of pricing differences between the two.Product arbitrage. Pricing differences exist between different blends, grades or types of the same commodity. There are over 160 tradable crude oil products with many different refined products and numerous end-users with highly specific requirements. By changing the form of the commodity, traders can lock in a profit. Time arbitrage. Over the long term, supply and demand tend to find a balance but, on shorter term horizons, they can remain out of sync. Trading firms can take advantage by storing commodities when supply is unusually high and drawing down inventories when demand is unusually high.What Sort of a Business is Investment Banking?For investment banks, risk management is their business. If they take risk, match risk and source risk, they can’t outsource the management of that to a chief risk officer; it’s the job of the frontline staff. How that all hangs together – how the incentives of staff are reconciled with the health of the firm comes down to the culture of the firm. And culture takes a long time to build, longer than most participants in fast-moving markets have the energy to invest.Buffett’s BanksFinancial companies have a tradition of courting disaster, and Buffett’s names are no exceptionThis is not by Marc but a related idea worth keeping in the back of our head: Aswath Damodaran recently discussed how in countries with sustained high inflation “every company becomes a financial service company, because they discover it's easier to run a bank on the side and lend money out short term than it is to build factories or toll roads.”Show notes*

Marc Rubinstein of Net Interest: Fascinating Financials

I am a big fan Marc Rubinstein and his Net Interest substack and was very excited to finally record a conversation with him. Marc previously covered financials and fintech as a research analyst and hedge fund investor and now shares his takes on the sector with his readers on a weekly basis. It’s a very well written and insightful lens on a fascinating corner of the market.We talked about banks, fintech, the importance of incentives and culture, payments, the need to watch regulators, how alternative asset managers have been picking up business from investment banks, and the danger of relying on the view of CEOs too far removed from the risk.You can find show notes on the substack. This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit www.frederikjournals.com/subscribe

🎙Nick Maggiulli: Just Keep Buying

Hello everyone,I’m happy to share my conversation with my friend Nick Maggiulli who writes the excellent personal finance blog Of Dollars and Data. Nick just came out with his first book: Just Keep Buying: Proven Ways To Save Money And Build Your Wealth. Nick combines his empirical research with a personal perspective and I really like that he distills the work down into rules that are effective yet pragmatic. His advice is free from some of the guilt-driven personal finance drivel (save on avocado toast to get wealthy..).We talked about the book, his writing process, the optimal level of fame, and why he thinks people should not pick stocks themselves.You can listen to the conversation on your podcast player of choice: Spotify, Apple, at anchor, and via RSS.“Fear has a far greater grasp on human action than the impressive weight of historical evidence.” Jeremy Siegel“You have to keep reminding yourself of that quote. It's my favorite investment quote because it's the only thing that keeps me from letting my behavior take over from my logic.” Nick MaggiulliSome highlights from the conversation:Nick’s argument against stock picking: how do you know whether you’re good at it? It takes too long to establish a track record that is meaningful:“Imagine you're trying to get in shape. … You go to the gym for three months, see no difference. Go to the gym for six months, one year, no difference. Then, all of a sudden, you lose 10 pounds. .. No one would do it. With diet and exercise, you start seeing results within a few months. But with stock picking … after one year, no way. … I think it can take a decade or longer. And this is obviously debated in the literature. … How do you know when a factor is dead? It can take you 20 years. It takes roughly the same amount of time to figure up a manager's really good … Let's just say you did it for 10 years. … My whole life's changed. Five years ago, I just started blogging. I didn't have a book. Imagine I have to do this again and only then would I know if I have skill. After 10 years, oh, actually I shouldn't be doing this.”Income vs. expenses and guilt-free saving and investing:“I do these like simulations and say, Hey, if this person is on a steady state of retirement and they get this raise, if they save at least half of it, they're usually good to go. It's about reducing guilt. It's okay to spend a little bit of money. … Cutting spending is not a way to raise wealth in the long run. You can do it in the short term, but the only sustainable path out is I've seen based on the data is raising our income.Everyone was like, you got to cut your lattes. You're just gonna feel miserable and hate it and guilt yourself. And you're going to end up giving up or you're gonna feel like s**t. I'm saying that the way out is raising her income and there's a way to do it. It just takes a lot of work, but it's the only sustainable path out.”Nick’s writing process:“I used to have a bunch of drafts which you can imagine as different pots sitting on the stove. Some have just ingredients, there's no heat on them. Some are kind of just simmering. Some are ready to take off, ready to serve. Sometimes I have nothing going and I just have to come up with something. It varies every week. Last week I wrote about inflation, why I think people are thinking about inflation incorrectly. I had this epiphany where I thought about it like, is that true?I said, oh, that's actually not true. Let's just write about that and see how it does. I like to reframe common things. A lot of stuff logically makes sense and then you run the numbers and you go, ah, that doesn't make sense as much as I thought it would have. A lot of things we just assume to be true and you ask, is that actually true?”Intuition backed by data:“I think there's a lot of people that have really good intuition, but they can't explain why it's true. So I ran the numbers and was like, Hey, this person who everyone is saying is dumb … yes, some of the things he said were a little silly, but I think his intuition was a lot stronger and more intelligent.” This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit www.frederikjournals.com/subscribe

Nick Maggiulli: Just Keep Buying

“We begin our lives as growth stocks and end our lives as value stocks.”I’m happy to share my conversation with my friend Nick Maggiulli who writes the excellent personal finance blog Of Dollars and Data. Nick just came out with his first book: Just Keep Buying: Proven Ways To Save Money And Build Your Wealth. He uniquely combines his data-driven research with a personal perspective and I really like that he distills the work down into rules that are effective yet pragmatic. His advice is free from some of the guilt-driven personal finance drivel (save on avocado toast to get wealthy..). We talked about the book, his writing process, the optimal level of fame, and why he thinks people should not pick stocks themselves.“Fear has a far greater grasp on human action than the impressive weight of historical evidence.” Jeremy Siegel “You have to keep reminding yourself of that quote. It's my favorite investment quote, because it's the only thing that keeps me from letting my behavior take over from my logic.” Nick Maggiulli This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit www.frederikjournals.com/subscribe

🎙Sebastian Mallaby and the Machine for Manufacturing Courage

Hello everyone,I’m excited to share my second conversation with Sebastian Mallaby. Last time, we discussed his book More Money Than God. A quote from that conversation stuck with me:“The key was to do an unreasonable amount of preparation work. It shows you're serious and not wasting people's time by asking the obvious questions.”This time, we discussed The Power Law (see my write-up) in which he tackled the history of venture capital. The two worlds make for an interesting contrast: venture capitalists, networkers by nature, are more willing to meet and chat. But they’re also natural storytellers which presents a challenge in the search for truth.In his book, Mallaby tried to disentangle luck and skill in venture investing, how to build winning and lasting cultures, and the importance of VCs for Silicon Valley. I had a lot of fun digging into these questions with him. I hope you enjoy the conversation. You can listen to it on your podcast player of choice: Spotify, Apple, at anchor, and via RSS.You can also add the Substack podcast feed to your podcasting player with the link on the bottom-right of the player.While individually “the story of every bet can seem to hinge on serendipity,” he argues that over the long run, “the best venture capitalists consciously create their luck.” The best “work systematically to boost the odds that serendipity will strike repeatedly.” A History of Systematic Serendipity and Grand Slams“The great challenge at venture partnerships is that the principals must refrain from killing each other.” Michael Moritz“When people write about the venture business, they’re always writing about the startups we back. They never write about the most important investment we make, which is in the business.” Michael Moritz."The fast moving of ideas, people and money until they reached their optimal use, that’s what made Silicon Valley worked. That’s what made innovation turbocharged. "But where did that fast circulation come from, and my argument is it comes from venture capitalists."Some highlights from the conversation:* Sequoia:* “It took a year or two of networking to break into the cathedral. But once I was in they are very thoughtful people. … They explained to me how they thought about behavioral biases in decision-making. … For example, we know that we anchor on past decisions. When a VC decides not to invest in a startup at the Series A stage, it's quite difficult to change your mind at the Series B. … it's painful to pay much more … because we were wrong the first time. They kind put that on the table and said, we’re probably anchoring, we're probably turning things down at Series B. From now on anybody who argues against the Series B investment is going to be subjected to cross examination - are you sure you're not anchoring?”* Strategy buckets in venture vs. hedge funds:* “Having written More Money Than God I was keen to put these different companies in buckets. I would see two different venture investors who had invested in the same company. I would try to find out … the contrasting mindsets. … People tend to have a few different stories going on in their head at once when they invest. It's not like you go with one chain of logic but not the other one. In venture capital, the distinctions people make are more around stage. Are you a seed investor, a series A investor, a growth investor. They might make distinctions by geography and they might make distinctions by sector.* But the mental approach, they say things like, some people want to bet on the size of the market and other people really want to bet on the type of founder they are backing. When I stress tested that kind of theory, I found it was normally not true.* Google had a strong position at series A because it had a working product which already had better search results than rivals. [Sequoia and Kleiner Perkins shared the round.] You had a natural experiment. The two were doing the same investment: did they have a different logic? And I came to the view that they had a subtly different logic. Kleiner Perkins was more a believer in technical breakthroughs, a product that was 10x better. I think that reflected the fact that both the dominant partners, John Doerr and Vinod Khosla were engineers by training. When they backed Google, I think they really believed the fact that the product was better was a huge deal. And therefore it justified a high valuation. I think Michael Moritz, who invested for Sequoia, came at it with a slightly different mindset. He also could see the product was much better. But I think he also thought of the Google investment in terms of the media side that he came out of himself. He said he made he invested in Google to look after Yahoo. He'd already invested in Yahoo. Yahoo had a popular web portal at the time. Part of him thought that Google could be the search engine in the top right-hand corner of the Yahoo site, a very valuable utility.”* Identifying founders:* “[At Accel] the idea was that when

Sebastian Mallaby and the Machine for Manufacturing Courage

Hello everyone,I’m excited to share my second conversation with Sebastian Mallaby. Last time, we discussed his book More Money Than God. A quote from that conversation stuck with me:“The key was to do an unreasonable amount of preparation work. It shows you're serious and not wasting people's time by asking the obvious questions."This time, we discussed The Power Law (see my write-up) in which he tackled the history of venture capital. The two worlds make for an interesting contrast: venture capitalists, networkers by nature, are more willing to meet and chat. But they’re also natural storytellers which presents a challenge in the search for truth. In his book, Mallaby tried to disentangle luck and skill in venture investing, how to build winning and lasting cultures, and the importance of VCs for silicon valley.And while he admits that individually “the story of every bet can seem to hinge on serendipity,” he argues that over the long run, “the best venture capitalists consciously create their luck.” Individual venture capitalists can “can stumble sideways into fortunes” and at times it seems like luck beats diligence and foresight. The best however, “work systematically to boost the odds that serendipity will strike repeatedly.”“The great challenge at venture partnerships is that the principals must refrain from killing each other.” Michael Moritz“When people write about the venture business, they’re always writing about the startups we back. They never write about the most important investment we make, which is in the business.” Michael Moritz."The fast moving of ideas, people and money until they reached their optimal use, that’s what made Silicon Valley worked. That’s what made innovation turbocharged. "But where did that fast circulation come from, and my argument is it comes from venture capitalists."I had a lot of fun digging into these questions with him. I hope you enjoy the conversation. This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit www.frederikjournals.com/subscribe

🎙Mary Childs and her book The Bond King

Hello everyone,I’m excited to share my conversation with Mary Childs, author of The Bond King (and co-host at Planet Money) on the rise and fall of legendary bond manager Bill Gross.You can listen to this conversation on your podcast player of choice: Spotify, Apple, at anchor, and via RSS.You can also add the Substack podcast feed to your favorite podcasting app via the link on the bottom-right of the player. I didn’t realize this until Liberty showed me🙏 (except Spotify doesn’t allow RSS importing😪).Mary and I talked about Bill’s breakfast habits (did low blood sugars end his career?!), his card counting days, the culture of paranoia at PIMCO, how he combined multiple sources of edge into “structural alpha” for long-term outperformance, the difficulty for a founder to leave their firm, Bill’s desire for fame, and how emotions ultimately got in the way of investing.I really enjoyed the book and was struck by the combination of structural factors that Gross used to build his track record (early in new products and going outside the benchmark, selling volatility, being creative with cash equivalents, figuring out how to use leverage in the mutual fund). His big picture calls are interesting but the record seems mixed.If you’re interested in Bill’s perspective, he recently appeared on this podcast. I liked how he framed what made a great bond manager: "One third mathematician, one third economist, one third horse trader. That certainly worked for me."It seems that at some point after the financial crisis he got stuck in bearish thinking. As his track record and public image took some hits, his behavior became more erratic and even belligerent towards the new generation of portfolio managers at PIMCO. The story illustrates how contentious the transition from founder to institutional money management firm can be.A few notes and quotes:Bill got started card counting in Vegas:"You have to have that gambling instinct. This business, if it's done properly, isn't gambling. But it entails some of the gambler's spirit.Vegas taught me that I could beat the system with a combination of hard work, ideas that no one has thought of yet, and the ability to tolerate a constant routine that to many people seems monotonous. But to me, it's the most exciting thing in the world."Perseverance:“My life’s plan has always been to outlive and outlast ’em. To persist. To persevere. To land on my feet, keep on running, and never stop.Excellence for most of us blossoms and flourishes for only a brief flicker of time. Either because of human frailty, maturation, or simple outright exhaustion, it’s difficult to perform at a crescendo for an extended period. Very few stay at the top for very long.”The culture of anxiety at PIMCO:For a Pimco trader, a day could easily be derailed by accidentally looking up from the screens and—disaster!—making fleeting eye contact with Bill Gross. No matter how well you were doing, it wasn’t good enough. Do more, better. Your ass was always on the line.He tested them constantly. He used to pace the trade floor, quizzing underlings … What mattered was “owning” the risk. It was yours now. Defend it. What did you think and what were your justifications, with fresh data points and prices?On the pain of being early in a trade (in this case bearish too early before 2007/2008):"Every investor has an alarm clock. I wish I could get up at 6 every morning and time things just right. I probably get up at 4:30."Some highlights from the conversation:Opening the door to a story:“If you're staring at a closed door … you just have to come up with a little piece of information to get that person to open that door, to crack it open. A little piece of gossip, a story that everyone's talking about. In and of itself that gossip is useless to you as a journalist, of course. But you can asking somebody, Hey, I keep hearing this ridiculous story. You have a little nugget of truth in there. You don't know what it is yet. … A lot of people want to help you understand and don't want to see the story misrepresented.”Traits of a founder:“The things that make someone capable of achieving the track record that Bill Gross did, building the kind of firm that Bill Gross was a part of, those personality traits are: you're going to be exacting. You're going to be really intense and focused. You're going to be a perfectionist, a micromanager. You're going to keep a really tight grip. These things, generally speaking help contribute to the success of the firm. … For the most part, these are things you see very frequently among founders, and also that toxic culture that can often come along with some of those traits. Those traits also make it very difficult, if not impossible, to have a graceful transition away from that founder. Because the minute they start to loosen their grip, they freak out. … The tight grip is who they are. This firm is who they are.”Being the house: “Bill gross learned from Ed Thorp’s book called Beat the Dealer that yo

Mary Childs and her book The Bond King

I’m excited to share my conversation with Mary Childs, author of The Bond King (and co-host at Planet Money) on the rise and fall of legendary bond manager Bill Gross.Mary and I talked about Bill’s breakfast habits (did low blood sugars end his career?!), his card counting days, the culture of paranoia at PIMCO, how he combined multiple sources of edge into “structural alpha” for long-term outperformance, the difficulty for a founder to leave their firm, Bill’s desire for fame, and how emotions ultimately got in the way of investing.Some highlights from the conversation:Opening the door to a story: “If you're staring at a closed door … you just have to come up with a little piece of information to get that person to open that door, to crack it open. A little piece of gossip, a story that everyone's talking about. In and of itself that gossip is useless to you as a journalist, of course. But you can asking somebody, Hey, I keep hearing this ridiculous story. You have a little nugget of truth in there. You don't know what it is yet. … A lot of people want to help you understand and don't want to see the story misrepresented.”Traits of a founder: “The things that make someone capable of achieving the track record that Bill Gross did, building the kind of firm that Bill Gross was a part of, those personality traits are: you're going to be exacting. You're going to be really intense and focused. You're going to be a perfectionist, a micromanager. You're going to keep a really tight grip. These things, generally speaking help contribute to the success of the firm. … For the most part, these are things you see very frequently among founders, and also that toxic culture that can often come along with some of those traits. Those traits also make it very difficult, if not impossible, to have a graceful transition away from that founder. Because the minute they start to loosen their grip, they freak out. … The tight grip is who they are. This firm is who they are.” Being the house: “Bill gross learned from Ed Thorp’s book called Beat the Dealer that you can count cards. … I think that this sensibility of both understanding the math but also feeling the pace of the table and knowing when you have that edge and when you don't, and also watching all the people around you who have no edge whatsoever and who were just flopping around taking dumb chances. All of that helped to inform how he approached the market and who he saw as his competitors. His competitors, aren't the dumb people doing the dumb stuff. His competitor is the market, is the dealer.This shows up when PIMCO figured out that the US government wasn't going to let certain institutions fail in the financial crisis. That there was going to be a government backstop … If I know that the US government is the house, I'm going to be the house, I'm going to try to align my own interests. … The point was to do what the government's going to do, but do it first: buy what they're going to buy and then sell it to them or ride that wave as the news of their purchase causes the price of those assets to soar. And that's exactly what happened.” This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit www.frederikjournals.com/subscribe

🎙Max Frumes: The Caesar's Palace Coup and Distressed Investing