Embrace Any Future

The corporate mentorship I wish I had. Real-world insights and long-form strategies for rising leaders who value depth over soundbites. Moving beyond the basics to help you build financial strength, career power, and a future you own.

Rachel C. Ybarra, CPA CGMA

Show overview

Embrace Any Future has been publishing since 2022, and across the 2 years since has built a catalogue of 9 episodes. That works out to roughly 3 hours of audio in total. Releases follow a roughly quarterly cadence.

Episodes typically run ten to twenty minutes — most land between 18 min and 23 min — and the run-time is fairly consistent across the catalogue. It is catalogued as a EN-language Business show.

The catalogue appears to be on hiatus or wound down — the most recent episode landed 1.6 years ago, with no new episodes in over a year. The busiest year was 2024, with 8 episodes published. Published by Rachel C. Ybarra, CPA CGMA.

From the publisher

A financial education podcast for corporate, entrepreneurial, and non-profit leaders seeking greater business knowledge, financial strategies, and wealth-building solutions. embraceanyfuture.substack.com

Latest Episodes

S1 E10: Personal Power vs Positional Power

Welcome to this special episode of our AI-powered podcast! Today, we're diving into one of our most frequently read articles: Personal Power vs. Positional Power. If you haven't already, you can find the full article on my Substack listed below.This week, I’m embracing a family tradition by taking my nephew on his first-ever trip to New York City—a meaningful adventure to share new experiences with the next generation. While I’m offline, I hope you enjoy this podcast, which uses AI to share key highlights from the article.Understanding the balance between personal and positional power is essential for anyone striving to grow their skills and their financial wealth. If you stay too long in any position, it will be difficult to build your skills and capabilities and ultimately your wealth.Enjoy!Article Below:DisclaimerThis newsletter and podcast are not financial or investment advice. Rather, this is educational information as you build your financial skills to be a better sovereign of your own finances.Share With OthersIf you are a business leader or mentor working with your mentees to improve their career possibilities, having financial strength is key. Understanding how to manage your career is one way your mentees can set themselves up for success. Feel free to share this so others can know and grow.Note: Thanks to AI for helping scribe and edit my dictation on this subject, which is based on my research, observations, experience, and perspectives over the last 30+ years. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit embraceanyfuture.substack.com

S1 E9: First Find the Company, Then Find the Job

The holiday season is here, and I hope you’re taking time to step away from work and enjoy moments with family and friends. It’s a time to reflect, recharge, and maybe even explore something new.While we’re all embracing this festive break, we decided to create a few AI Podcasts inspired by some of the most popular articles I’ve written over the past three years. One of these, First Find the Company, Then Find the Job, resonated deeply with readers—thank you for all the thoughtful emails and words of encouragement. It’s always rewarding to hear how these insights have helped!For me, podcasts have been a go-to for over a decade. What I love most is how they let me multitask—whether I’m walking, making dinner, or waiting at the doctor’s office, I can feed my curiosity and learn on the go.So, if you’re in the U.S. and planning to walk off your Thanksgiving feast—or simply looking for something engaging to listen to—this podcast is for you. Whether you’re job hunting, thinking about advancing your career, or considering a complete shift, this article offers valuable guidance on where to start.As an investor, I firmly believe in the idea of finding the right company first, then identifying the job. It’s a perspective I believe can pay dividends or at a minimum it’s worth considering.In this episode, our AI Podcasters break down the key ideas from the article. If it piques your interest, you’ll find the full piece linked below. Give it a listen, and let me know what you think!Happy Holidays and we will see you next week!DisclaimerThis newsletter and podcast are not financial or investment advice. Rather, this is educational information as you build your financial skills to be a better sovereign of your own finances.My comments and thoughts are based on my observations over the last 30+ years as a hiring manager and investor.Share With OthersIf you're a business leader or mentor guiding your mentees to enhance their career prospects, building financial strength is crucial.Helping your mentees understand which companies are creating value, experiencing growth, and demonstrating strong earning power can be transformative. Employees who grasp these concepts not only improve their engagement but also contribute to the economic value and long-term success of the companies they serve. By learning which companies create value—and how investors evaluate that value—your mentees can position themselves for greater career success as they search for their next career opportunity.Feel free to share this insight with others to inspire growth and understanding.Note: Special thanks to AI for assisting with the scribing and editing of this piece, which reflects my research, observations, experiences, and perspectives. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit embraceanyfuture.substack.com

S1 E8: How Stocks and Companies Compounds - AI Podcast and Study Guide

A few weeks ago, I published a 30+ minute episode, S1 E6: Key Drivers of Stock Market Compounding. After some reflection, I decided to take it down. It felt too long-winded and not as organized as I’d like—I simply didn’t have enough time that week to refine it.This new episode replaces it. Thanks to technology, I’m introducing an AI-driven podcast featuring two AI hosts who dive into the subject of stock market compounding. At half the length, this episode is concise and enhanced with relevant examples drawn from the educational materials I provided. It’s an engaging primer that delivers valuable insights in a fraction of the time.Want to Read the Full Article? See the below:DisclaimerThis newsletter and podcast are not financial or investment advice. Rather, this is educational information as you build your financial skills to be a better sovereign of your own finances.My comments and thoughts are based on my observations over the last 30+ years. At present, the financial markets look highly valued as measured by the Shiller PE Ratio.Share With OthersIf you are a business leader or mentor working with your mentees to improve their career possibilities, having financial strength is key. Understanding how company value is created and how investors view that creation is one way your mentees can set themselves up for success. Feel free to share this so others can know and grow.Note: Thanks to AI for helping scribe and edit my dictation on this subject, which is based on my research, observations, experience, and perspectives. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit embraceanyfuture.substack.com

S1 E7 Leadership in the Modern Era

[00:00–00:12] Introduction: Leadership and Hall of Fame Insights* Overview: Lessons from attending the Hall of Fame dinner at UT Austin. Leadership is not just about professional success but inspiring and empowering others.[00:12–01:12] Lessons from the Hall of Fame: Leadership as a Conductor of Change* Key Idea: Leadership transcends professional and financial success, focusing on empowering others.* Core Principles:* Treat people with dignity and respect to achieve collective goals.* Leverage financial capital, technology, and people effectively.* Set clear visions, influence stakeholders, and build systems for scalability.[01:12–04:01] Leadership Requires Velocity: Case Study* Scenario:* A turnaround CEO took over a year to announce a strategic plan, resulting in a key investor exiting early.* Key Events:* Month 0: New CEO hired.* Month 3: Activist investor joins.* Month 9: New board members added.* Month 12: Investor exits due to lack of progress.* Month 15: Strategic plan finally announced.* Takeaways:* Leaders must seize opportunities swiftly and demonstrate quick wins.* Early progress builds momentum, inspires belief, and ensures stakeholder alignment.[04:01–06:06] The Power of Leverage in Leadership* Components of Leverage:* Financial Resources: Allocate strategically.* Technology: Drive innovation and efficiency.* People: Harness specialized expertise and foster team alignment.* Key Insight: Trust and respect amplify leverage, enabling teams to reach their full potential.[06:06–07:36] Hall of Fame Leaders and the Leadership Imperative* Defining Characteristics:* Agility: Identifying opportunities and challenges rapidly.* Focus: Prioritizing impactful strategies.* Ethics: Maintaining high trust and integrity.* Velocity: Acting decisively to capture fleeting opportunities.* Observation: Slow or bad leadership is incompatible with the rapid pace of modern markets.[07:36–09:12] Building for 2025 and Beyond* Reflection Questions:* Are you leading with velocity?* Are you fostering trust and momentum within your team?* Are you capturing opportunities before they vanish?* Conclusion: Effective leadership today demands focus, agility, and urgency, coupled with respect and dignity. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit embraceanyfuture.substack.com

Podcast: S1 E5: Be Prepared When You Show Up to Investors:

In this episode, we dive into the critical steps for raising capital, whether for real estate or any other capital-intensive business. I recently received a question from a former client about raising capital for their real estate venture, which inspired me to share the essential tools and strategies that apply to any entrepreneur looking to take on investors instead of securing a loan.We’ll cover:The key legal documents required to raise capital, including the Operating Agreement, Subscription Agreement, and Private Placement Memorandum (PPM).How to build a strong business plan that highlights market opportunities and your competitive advantage.Why having the right team, such as a fractional CFO and a certified bookkeeper, is critical for gaining investor confidence.Tips on managing investor relations and exit strategies, so you can ensure long-term success for your business.Takeaways:Understanding the fundamental legal documents you need to raise capital.How to craft a business plan that sets you apart in a competitive market.The importance of financial infrastructure and team selection when bringing on investors.Whether you're looking to raise capital for real estate or another capital-intensive business, this episode will give you the roadmap to do it successfully.Resources Mentioned:Blog Post: https://open.substack.com/pub/embraceanyfuture/p/be-prepared-when-you-show-up-to-investorsLegal Documents Overview: Operating Agreement, Subscription Agreement, and PPM.Listen Now:Tune in to learn how to prepare when you show up to investors and set your business up for success! This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit embraceanyfuture.substack.com

S1 E 4: Personal Finance Education Q&A

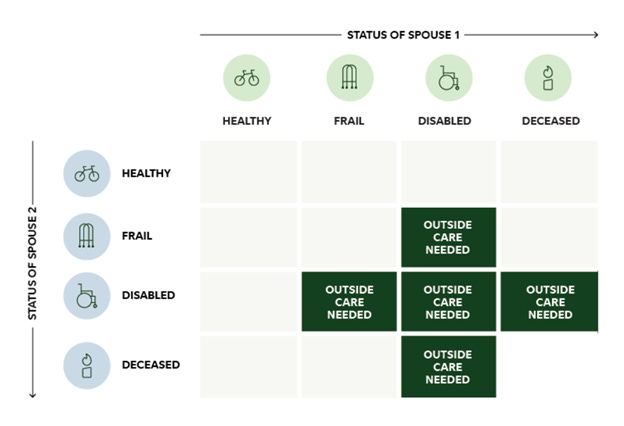

Hi, welcome! As part of Hispanic Heritage Month, we’ve put together a Q&A based on questions submitted by our community. Our hope, aligned with our mission, is to help advance financial education and knowledge so that you feel not only more empowered but also financially savvy in making decisions that best suit you and your family.Thank you to everyone who submitted their questions. They are quite in-depth! I’ve got eight pages of notes, so we’ll try to go through them as quickly as possible. Let’s jump in and get started!Questions from the CommunityQ: At what age do you start allocating for long term care? What options are available for this?A: Navigating Long-Term Care Insurance: Strategic Planning for Future NeedsLong-term care insurance is a crucial consideration for anyone planning for their future healthcare needs. Statistics show that more than half of individuals over the age of 65 will require long-term care. It's vital to understand all available options for funding such care to ensure peace of mind and financial stability.Optimal Timing for Purchasing Long-Term Care InsuranceWhile the mid-50s is generally recommended as the optimal time to secure long-term care insurance, certain circumstances might necessitate earlier consideration:* Health Considerations: Your current health and any medications you take play significant roles in your eligibility for long-term care insurance. Certain medications, especially those affecting cognitive functions or diseases like multiple sclerosis, a history of strokes, or diabetes requiring insulin shots, can preclude you from obtaining coverage. It's crucial to apply before such issues arise.* Early Planning Benefits: Purchasing insurance earlier can lead to lower premiums and a higher likelihood of acceptance, safeguarding your future while also protecting your loved ones.* Considering Others: Let's talk about others—this includes your spouse, partner, adult children, and grandchildren. Planning early can protect them from potential financial burdens or the responsibility of caring for you themselves, which could delay their ability to work or attend school. In some cases, they might not be physically capable of providing the necessary care, such as lifting another human being or relocating from another part of the country to assist. If you find yourself suddenly single and subsequently have a stroke or other health issue requiring long-term care, you would want to be self-sufficient through the assistance of long-term care providers. In all these cases, think of others.Understanding Funding Options for Long-Term CareThere are several strategies to fund long-term care, each with its own set of benefits and considerations:* Government Assistance: Programs like Medicare typically cover limited, short-term long-term care needs, mostly after hospitalization. Medicaid may cover long-term care but only if you meet stringent financial eligibility requirements. Research your state's Medicaid program, particularly for long-term care. Your financial situation will have to be quite dire, and there should be no attempts at "gaming the system" (which we know our readers would not do), among some of the basics.* Hybrid Policies: These policies combine life insurance with long-term care insurance, offering a death benefit if the long-term care benefit is not used. This option provides flexibility and ensures that the premiums paid will not be lost.* Traditional Long-Term Care Insurance: This offers the most comprehensive coverage for long-term care services, from in-home care to full-time nursing home care. These policies can often include benefits like spousal sharing, inflation protection, and return-of-premium features. Benefits usually have a set term of 2 to 6 years once a physician certifies you can’t perform 2 to 3 activities of daily living (ADLs), such as bathing, dressing, eating, and personal hygiene among others.* Self-Funding: For those with sufficient resources, paying out of pocket may be an option. This requires substantial financial planning to ensure that personal assets can cover potential care costs without compromising other financial goals.Estimated FundingAging is a fact of life, and in the United States, our healthcare system places a large financial burden on individuals. There are two pieces to consider when funding for your future age-related needs:* Healthcare Expenses in Retirement: Plan to have approximately $157,000 saved (after-tax)/ per person to cover healthcare-related expenses in retirement. You may need more if you have larger incomes and are subject to Income-Related Monthly Adjustment Amount (IRMAA) Medicare surcharges for those whose incomes are over certain thresholds.* Long-Term Care Needs: Separate from regular healthcare-related expenses noted above, Fidelity estimates that 7 out of 10 people will need long-term care in their lifetime. This includes services in your home, a day program in your community, or a residential facility lik

S1 E3 An Agreement With Yourself

Listen to Rachel as she reads an article she originally wrote in March 2024 about creating your own investment policy statement. In this recording, she expands on the original content to encourage her audience to develop their investing skills. Whether you're opening a savings account at 17 or evaluating your assets as a new retiree, it's never too early or too late to cultivate an investor mindset.Please note that this is not investment advice. It is educational material designed to help listeners grow their understanding of key considerations as they embark on their investment journey.You can find the original article here, along with key highlights of what will be covered: An Agreement With Yourself. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit embraceanyfuture.substack.com

Your Financial Well-being

In this podcast episode, we delve into personal finance reflections and address questions from the community, emphasizing the uniqueness of personal finance journeys and advocating for informed, value-driven decisions. The episode covers several key themes:* Investment Discipline During Economic Stress: Hear some of my experiences with market downturns and the importance of sticking to core values and investment principles. The discussion underscores the significance of balance, support systems, and aligning financial decisions with personal values over purely economic gains.* Learning from Financial Crises: Reflecting on past financial crises, you will hear lessons learned about global debt, economic resilience, and the societal need for overall prosperity. An "investment policy statement" is introduced as a guide for investment decisions, with advocacy for periodic reviews to ensure alignment with long-term goals. If you are interested in learning more about an investment policy statement, start by reading this article.* Relationship with Money and Investment Strategy: Listeners are encouraged to understand their relationship with money and how it influences their investment strategy; highlighting the importance of core values, goal setting, and understanding the time horizon in shaping investment choices.* Paying Off Mortgages Early vs. Investing: Here we address a question about paying off a mortgage early, a balanced view is presented, suggesting there are more solutions than just two options to include a hybrid that might offer both security and financial growth. The discussion advises listeners to consider their core values and financial goals in making such decisions.* Debt Management and Monthly Budgeting: In response to a question from the community, we discuss strategies to manage significant debt. It starts with understanding one’s relationship with money and adopting a kind and understanding approach to yourself is suggested. Practical strategies like prioritizing expenditures, seeking additional income, and embracing creativity to navigate financial recovery are recommended.Throughout the episode, we emphasize personal reflection, the alignment of financial decisions with your personal core values, and the proactive management of finances through education and disciplined strategy. If you are interested in learning more about Your Relationship with Money, Determining Your Core Values, and Your Personal Power, you can now purchase the workbooks and get started on the self-study program.These upcoming materials, including affordable workbooks on financial wellness, will aid you as you start to develop your own personal finance plan and journey with an emphasis on the holistic nature of financial well-being beyond mere numbers.Thank you again for those who submitted in questions. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit embraceanyfuture.substack.com

Investor Mindset Session - Q&A

This is a Q&A from the October 4, 2022 AT&T HACEMOS Webcast. How do you build an investor mindset. Here are few questions asked after the session:1) Is it too late to start in your thirties, forties, or fifties, in terms of creating an investor mindset and ultimately creating wealth? (0:10)2) What is your advice for creating an investor mindset in teenagers or youth? Any recommendations on books or articles to read? (2:11)3) What financial advice would you tell someone who's starting investing? Is there a particular investment strategy type that you'd recommend? And what advice would you tell your younger self? (4:45)4) Many economists say that the global recession is going to be happening within the next year. What are your thoughts and how will impact people's investment strategies? (7:54)5) Have you ever invested in a minority owned business? Any advice or tips when investing in a minority owned business? And why is investing in minority owned businesses important? (9:41)6) Where can one go to get a better understanding of one's 401k fund? (11:22)Are you interested in having a wealth coach from someone who has achieved similar financial success? If so, feel free to reach out: [email protected] or call 210-810-2459. This is a public episode. If you would like to discuss this with other subscribers or get access to bonus episodes, visit embraceanyfuture.substack.com