Show overview

Concretum Research has published 9 episodes, alongside 4 trailers or bonus episodes during 2025. That works out to roughly 5 hours of audio in total. Releases follow a roughly quarterly cadence.

Episodes typically run twenty to thirty-five minutes — most land between 16 min and 44 min — with run-times ranging widely across the catalogue. It is catalogued as a EN-language Business show.

There hasn’t been a new episode in the last ninety days; the most recent episode landed 8 months ago. Published by CONCRETUM GROUP.

From the publisher

Be inspired by the audio content from our cutting-edge quantitative trading research, published on SSRN.com and in our website.You can visit us at www.concretumgroup.com or reach us out in X or via email at [email protected]

Latest Episodes

S1 Ep 5Audio-Paper: The Tranching Dilemma A Cost-Aware Approach to Mitigate Rebalance-Timing Luck in Factor Portfolios.

In this episode, the Concretum Research Team breaks down a hidden but powerful force in systematic investing: Rebalance Timing Luck—the idea that two identical factor strategies can produce dramatically different long-term returns simply because they rebalance on different days. Drawing from a new study by Carlo Zarattini and Alberto Pagani, the discussion reveals how a concentrated U.S. equity momentum strategy showed nearly 350 bps of annualized performance dispersion across monthly schedules, and why traditional fixes like tranching—splitting a portfolio into multiple staggered sub-portfolios—are not the free lunch they appear to be. While tranching reduces timing noise, it also increases trading costs, creating what the authors call The Tranching Dilemma, where the optimal number of tranches depends heavily on portfolio size: too few magnifies luck, too many erodes returns. The episode offers a practical, cost-aware framework for determining the right balance, making it essential listening for systematic traders, quant PMs, and anyone curious about why “identical” smart-beta products often behave nothing alike.

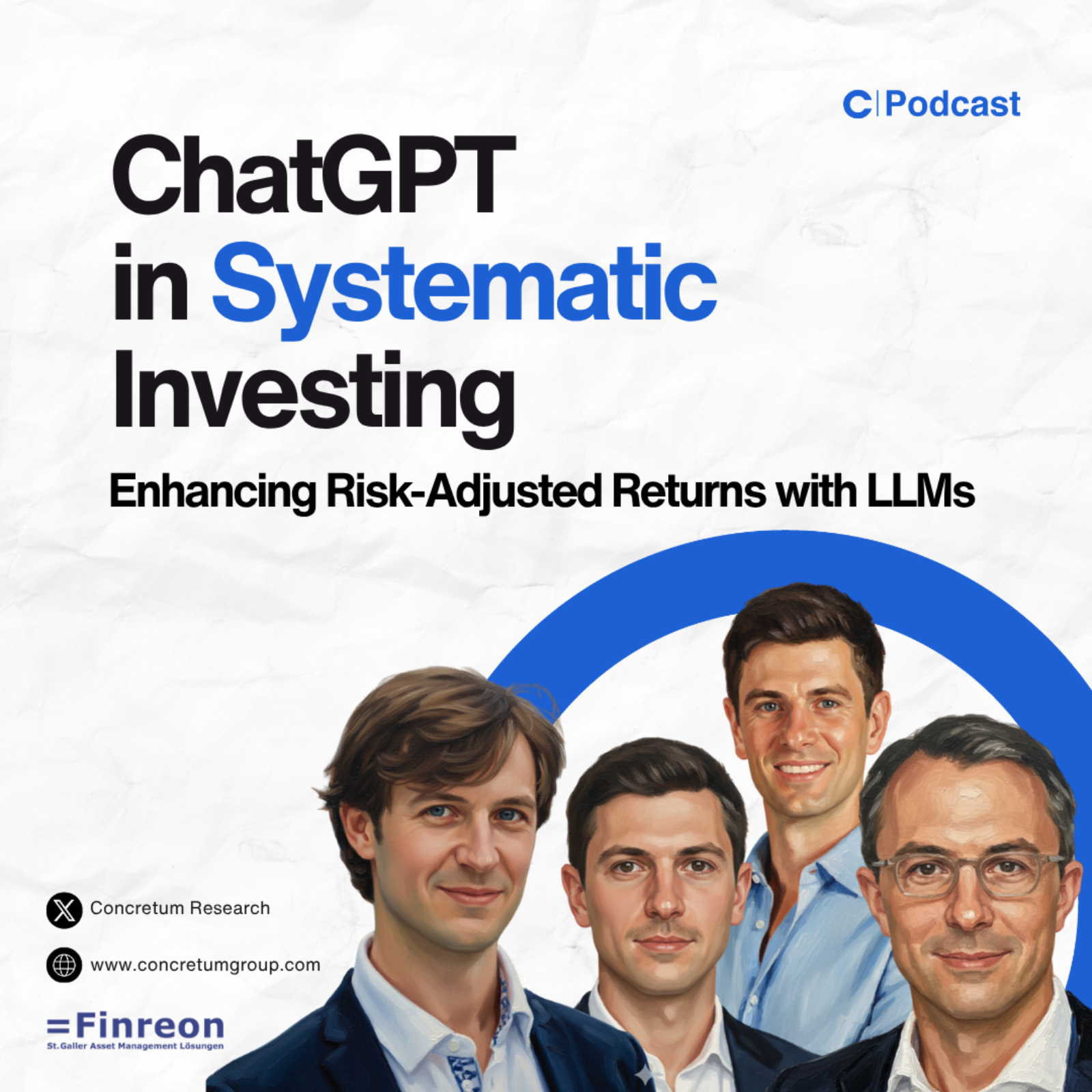

S1 Ep 4Audio-Paper: ChatGPT in Systematic Investing - Enhancing Risk-Adjusted Returns with LLMs

In this episode, the Concretum Research Team discusses a new study at the intersection of artificial intelligence and systematic investing. Conducted with Finreon Asset Management, the research asks a simple but ambitious question: can a large language model like ChatGPT read corporate news and use that information to refine momentum-based investment strategies?Using daily data on S&P 500 stocks, the study combines traditional price-based signals with ChatGPT’s interpretation of firm-specific news. The results show that this AI-assisted approach improves both stock selection and portfolio performance, delivering higher risk-adjusted returns than a standard momentum strategy — even in out-of-sample tests.

Deep Dive: The Volatility Edge: A Dual Approach For VIX ETNs Trading

bonusThis AI-generated NotebookLM-approved episode shows how individual investors can profit from the volatility risk premium using VIX-linked ETNs. A dynamic strategy tested from 2008–2025 yields strong returns with low equity correlation. With proper tools, volatility trading is now accessible—but must be approached cautiously.

S1 Ep 3Audio-Paper: The Volatility Edge: A Dual Approach For VIX ETNs Trading

This Episode shows how individual investors can profit from the volatility risk premium using VIX-linked ETNs. A dynamic strategy tested from 2008–2025 yields strong returns with low equity correlation. With proper tools, volatility trading is now accessible—but must be approached cautiously.

Deep Dive: Catching Crypto Trends A Tactical Approach for Bitcoin and Altcoins

bonusIn this episode, we share an approved Deep Dive by Notebook LM, highlighting a crypto trend-following strategy that blends classic technical tools with digital asset data, as explored in a paper on Donchian channels and volatility-based rotation.

S1 Ep 2Audio-Paper: Catching Crypto Trends A Tactical Approach for Bitcoin and Altcoins

We explore how a classic trend-following strategy using Donchian channels performs in crypto markets. Tested on Bitcoin and a broad altcoin dataset since 2015, this approach delivers strong returns and risk-adjusted performance. We also cover transaction cost management and real-world execution tips.

Deep-Dive: The Power of Price Action Reading

bonusIn this episode, we share an approved Deep Dive by Notebook LM, discussing the experiment conducted by Carlo Zarattini and Marios Stamatoudis, as presented in their fascinating paper titled "The Power of Price Action Reading."

Deep Dive: Does Trend-Following Still Work on Stocks

bonusIn this episode, we share an approved Deep Dive by NotebookLM discussing the key insights from our paper, "Does Trend Following Still Work on Stocks?"

S1 Ep 1Audio-Paper: Does Trend-Following Still Work on Stocks?

This paper explores the performance of trend-following strategies in U.S. stock markets over the past 70 years, addressing practical implementation challenges and techniques to reduce transaction costs.