Could All Debt Actually Just Be Canceled?

Based Camp | Simone & Malcolm Collins · Based Camp | Simone & Malcolm

Audio is streamed directly from the publisher (api.substack.com) as published in their RSS feed. Play Podcasts does not host this file. Rights-holders can request removal through the copyright & takedown page.

Show Notes

Could a “debt jubilee” happen in the US? Malcolm and Simone dive deep into skyrocketing consumer debt, unsustainable government obligations (like Social Security insolvency by 2032-2034), and historical debt cancellations—from ancient Mesopotamia and Biblical jubilees to Japan’s post-WWII wealth confiscation and modern “Abenomics.”

They debate whether America’s record-high credit card debt, buy-now-pay-later defaults, and cultural attitudes toward money could trigger a crisis, hyperinflation, or forced wealth redistribution. Is bankruptcy already America’s soft debt jubilee? What should you invest in (or avoid) if things get weird in the 2030s?

Hilarious tangents include check fraud “hacks,” Caleb Hammer roasts, ramen lifehacks, and why Japan pulled off drastic reforms while Venezuela and Zimbabwe collapsed.

As Simone outlined this episode, the outline (and links) follows! The transcript is at the end of the post. Merry Christmas, you filthy animals!

Episode Outline

* US consumer debt levels are currently at record highs in 2025, both in nominal and inflation-adjusted terms

* Average credit card debt among cardholders with unpaid balances rose to about $7,321 in Q1 2025, up 5.8% from a year earlier

* People are using buy now pay later services like Klarna and Afterpay at record levels and increasingly paying late

* A LendingTree survey found that 41% of BNPL users made a late payment in 2025, up from 34% the prior year

* April 2025, 31% of federal student loan borrowers were 90+ days delinquent on payments,

* This comes at a time when…

* People are beginning to view debt payoff, the concept of capitalism, and even faith in fiat currency with increasing skepticism

* Loan defaults and late payments are on the rise

* democratic socialist political figures like Zohran Mamdani are gaining serious traction and public attention

* Even our governments are spending like someone with zero expectation of paying off their debt

* US social security likely to falter in 2032-2034

* The UK is set to experience a social security crisis in the early 2030s

* And this matters, because something’s gotta give, and in the past, this has involved various forms of debt jubilees

* So we’re going to discuss:

* The situation with consumer debt today

* The situation with government debt today

* How unsustainable debt has been dealt with historically

* How this could go poorly

* How this could go well and how we as individuals might prepare

Banks and Fractional Reserves

* The post:

* Oct 21 trending discussion: https://x.com/i/trending/1980520651816341983

US Consumer Debt

* Credit card balances hit another all-time high, reaching around $1.21 trillion in Q2 2025—matching last year’s record with annualized growth rates of over 9% in mid-2025.

* Credit card interest rates are commonly averaging 22–24% in 2025, compared to around 15% just a few years ago.

* Delinquency rates for credit cards and other non-housing debts have increased to levels well above pre-pandemic norms. In Q2 2025, about 4.4% of all debt was in some phase of delinquency.

* Klarna reported a 17% increase in consumer credit losses in Q1 2025, totaling $136 million, with repayment defaults rising among users.

* Student loan delinquencies are also rising, especially following the resumption of payments after long pandemic-era forbearance, adding further strain to household finances

* In March 2025, just 35% of federal student-loan borrowers had made their most recent payment on time. The rest were at risk of (or already in) serious delinquency or default.

It has actually been worse recently, though:

* US consumer (household) debt has reached nominal record highs in 2025, but when adjusted for economic growth (e.g., as a percentage of GDP), it remains below pre-2008 financial crisis peaks and has even declined slightly in recent quarters.

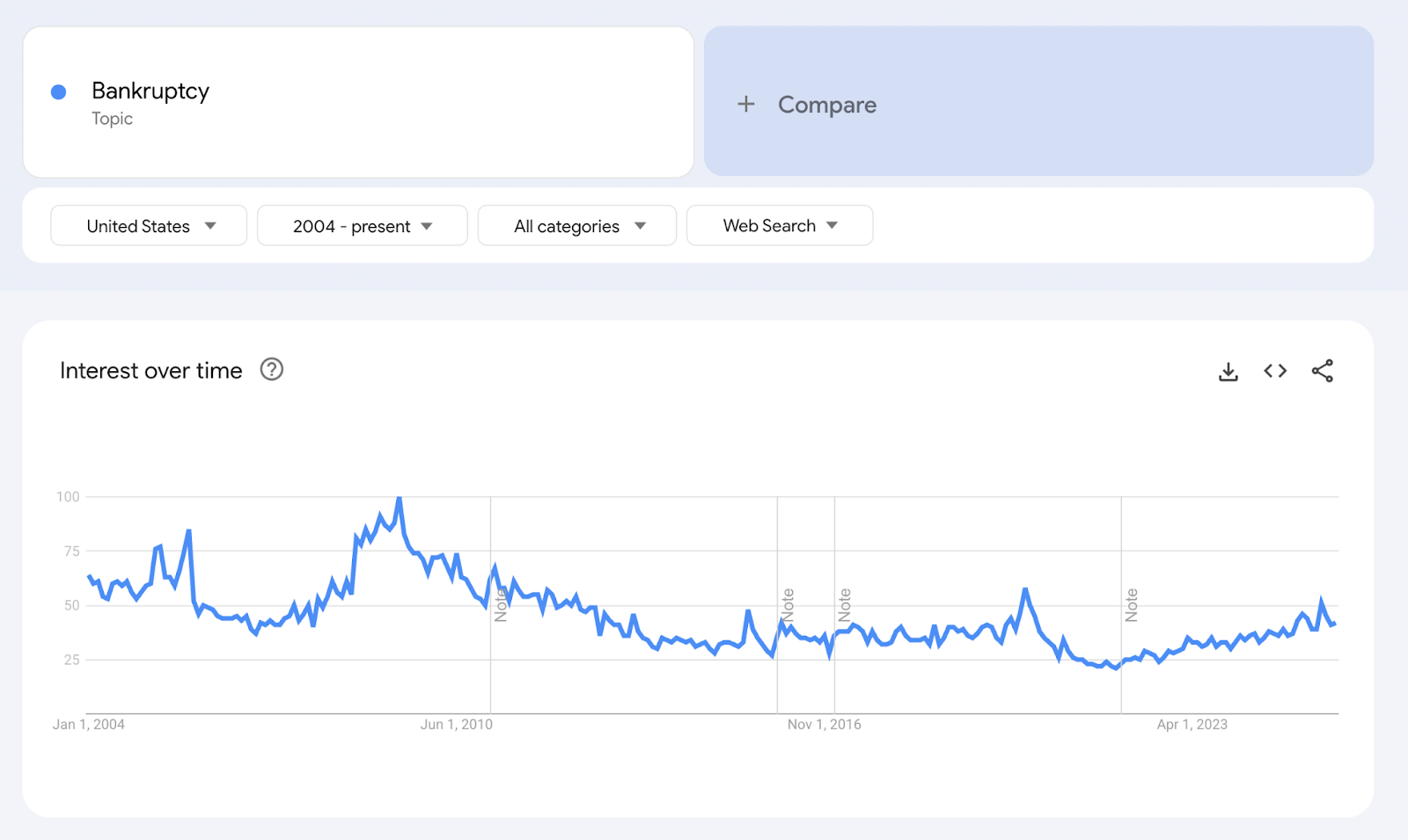

* This tracks with bankruptcy search trends (https://trends.google.com/trends/explore?date=all&geo=US&q=%2Fm%2F01hhz&hl=en)

* After adjusting for inflation, average household debt in 2025 is about 2.9% ($1,800) higher than in 2013 but 17.2% ($13,100) lower than the 2008 peak.

* Also, bankruptcy is pretty soft on people

* Basically bad credit for 10 years and non-essential assets can be frozen, but many don’t have much to lose in the face of that.

* What has me worried more is the mindset

* The surging skepticism around communism

* The employment threat of rising AI

* The increasingly absurdist interpretation of money and normalization of putting off money problems

* E.g. BNPL usage is surging, with monthly spending up 21% year-over-year to $243.90 per user in June 2025.

* 41% of users paid late in the past year (up from 34%), 24% faced late payments in 2025, and nearly 40% regret usage due to hidden costs.

The gist:

* Consumer debt is a problem

* Government debt is a bigger problem

Government Inability to Pay Obligations

Social Security Set to Falter

* The U.S. Social Security retirement trust fund is now projected to be insolvent by late 2032; if the disability fund is combined, around 2034. Benefits would be cut about 24% automatically if nothing is done

* UK state pension is pay-as-you-go and generally funded from current taxes, but there are major concerns about the sustainability of defined benefit (private and public) pension plans and the adequacy of future benefits. A liquidity and solvency crisis in 2022 exposed the vulnerability of the system, and ongoing warnings suggest potential crisis if reforms aren’t enacted as liabilities grow

* Other Western nations face sustainability crises from the 2030s, mostly driven by aging populations and shrinking worker/retiree ratios.

* Canada is currently better positioned due to earlier reforms, but is still monitoring demographic risks.

* All systems will require some combination of benefit reduction, tax increases, or later retirement ages to remain sustainable.

Historical Jubilees

TL:DR: Rules repeatedly cancelled debts (without consent from creditors) to end, evade, or calm rebellion, turmoil, class conflict, revolution, or societal breakdown.

Misc

* Ancient Mesopotamia: Kings of Sumer, Babylon, and neighboring regions periodically canceled debts for peasants and small landholders, often at the start of their reigns or during crises.

* Athens, Greece – Solon’s Seisachtheia “sigh-SAK-thee-uh” (594 BCE): Solon forgave personal debts, banned debt slavery, and wiped out mortgage debts in Athens.

* Initially controversial but eventually credited with preventing revolution and laying foundations for Athenian democracy. Credit eventually resumed as societal structures stabilized.

Medieval Japan

In medieval Japan, particularly during the Kamakura (1185–1333) and Muromachi (1336–1573) periods, the shogunate issued edicts known as tokusei (literally “virtuous government” or “benevolent rule”), which effectively functioned as debt jubilees. These were decrees that canceled debts, often in response to peasant uprisings (tokusei ikki) driven by famines, high taxes, epidemics, or exploitative lending practices. The concept dated back even earlier, with roots in the Nara and Heian periods (710–1185), but became prominent in the 13th–15th centuries.

* The most famous early example is the Einin Tokuseirei of 1297, issued by the Kamakura shogunate. It annulled all debts contracted before that year, allowed vassals (gokenin, or samurai retainers) to reclaim pawned lands without repaying loans, and canceled interest on older debts. This was motivated by the need to bolster military strength against potential Mongol invasions (following attempts in 1274 and 1281) and to address widespread debt burdens among the warrior class.

* Later examples include uprisings that forced similar measures, such as the Shōchō uprising in 1428 during the Muromachi period. Peasants in the Kinai region (around Kyoto) rebelled amid famine, high rice prices, disease, and heavy taxes. They looted moneylenders, sake merchants, pawnshops, and temples, destroying debt records to achieve “independent debt relief.” The shogunate did not issue a nationwide order, but local authorities like the Kōfuku-ji temple in Yamato Province responded with a formal tokusei law: pawned items could be redeemed for one-third of their value, and loans over five years old were annulled. A stone inscription (Yagyū no Tokusei Hibun) commemorates the full cancellation of pre-1428 debts in specific villages.

Scary Post-WWII Currency Reform and Debt Resolution (1946)

After Japan’s defeat in World War II, the government faced massive sovereign debt (about 267% of national income by March 1945), hyperinflation, and economic ruin. While not explicitly called a “jubilee,” the 1946 Financial Emergency Measures effectively wiped out much of the real value of debts through currency reform and wealth confiscation.

What Exactly Happened

* On February 16, 1946, the government announced surprise measures: All bank accounts were frozen, old yen notes were invalidated unless deposited, and a “new yen” was introduced at a 1:1 exchange rate. Withdrawals were severely limited (initially 300 yen per household head plus 100 yen per member, later 100 yen per month per person—barely enough for survival).

* This was followed by a massive one-time property tax in autumn 1946, levying up to 90% on assets (including blocked deposits) held as of February 16. Tax revenues were used to repay government bonds and interest. War-related compensations to companies and citizens were offset by special taxes, amounting to a partial default.

* Hyperinflation (prices rising over 500% annually in 1945–1946) had already eroded the real value of debts before the reform.

Effects

* Government debt was drastically reduced (from 446 billion yen in 1948 to 316 billion yen in 1950), taming hyperinflation and enabling postwar reconstruction. It paved the way for the “Japanese economic miracle” of rapid growth in the 1950s–1980s.

* The public suffered massive wealth loss (savings wiped out), exacerbating poverty initially but stabilizing the economy long-term. It was a form of forced wealth redistribution, seen as a domestic default, and provided lessons for modern fiscal policy. No significant inflation spike followed due to the controls, but it eroded trust in financial institutions temporarily

How This Could Go Poorly

Zimbabwe and Venezuela

TL:DR: Both governments saw drops in revenue (caused by different things) but were politically unable to cut spending so they printed more money to pay for things and caused hyperinflation.

* Venezuela

* Experienced a drop in income but had huge social spending programs it felt it couldn’t stop funding

* Venezuela’s government depended on oil for about 95% of its foreign currency earnings. When global oil prices crashed (especially post-2014), government income collapsed.

* To cover these budget gaps, the government printed more bolivars rather than cutting spending or raising taxes. This inflated the money supply massively

* These led to shortages of basic goods, discouraged local production, encouraged black markets, and eroded business/investor confidence.

* Zimbabwe

* Following popular but economically disastrous land redistribution, food and export revenues collapsed. Government, unwilling to reverse course or lose power, financed itself by printing currency

How This Could Go Well & How We Should Prepare

Forms of Jubilee That Worked in the Past

Jubilees in Ancient Israel

* Ancient Israel (Biblical Jubilee): Every 50 years, debts were canceled, slaves set free, and lands restored to original owners.

* Practiced from around 1400 to 500 BC

* Whereby debt forgiveness was granted to Fellow Israelites in debt or servitude; families who lost land or freedom due to loans.

* It was limited only to Israelites

* I think debt forgiveness makes sense within tight-knit, cohesive communities

* Like how family members make loans understanding that the loans may never be repaid

Japan’s Case

In recent decades, Japan has managed its enormous public debt (over 250% of GDP) through a quasi-jubilee mechanism without formal cancellation.

In short, Japan’s debt buybacks are a way to prevent market collapse and maintain low borrowing costs for the government. Most countries avoid this because of the risk of inflation, devaluation, and loss of investor confidence, which can destabilize their economies.

Japan’s problem

* Japan did not have a traditional “debt jubilee” where debts were outright forgiven at a large scale for private individuals or companies. Instead, what Japan has done, particularly over the last few decades since its economic bubble burst in the early 1990s, is a form of government debt management that mimics a debt jubilee through central bank policies.

* The Bank of Japan (BoJ), the country’s central bank, has been buying large amounts of Japanese government debt, currently owning around 40% of it. By purchasing government bonds and holding them, effectively the government owes this debt to itself.

* Why Did Japan Need to Buy Back Debt?

* Prevent Market Turmoil: Japan’s government bond market has experienced surges in yields (interest rates) due to a lack of private investor demand for long-term bonds, government calls for more spending, and worries about its huge debt-to-GDP ratio. Higher yields mean higher costs for the government to service its debt. The Bank of Japan stepped in to stabilize these yields and prevent borrowing costs from spiraling out of control.

* Without intervention, yields on government bonds would likely have kept rising. This would force the government to pay much more to finance its deficit, risking a “debt spiral” where interest payments consume more of the public budget.

* Support Public Spending: With an aging population and slow-growing economy, Japan relies on fiscal stimulus (public spending) to maintain stability. High borrowing costs could threaten necessary government programs and pensions.

* Confidence and Liquidity: Aggressive buying by the central bank (quantitative easing, and debt buybacks) helps reassure investors that the government debt will be serviced, supporting confidence in markets and maintaining economic liquidity.

* The interest paid on this debt by the government is funneled back to the government. This means the government is not burdened by the debt servicing costs in a meaningful economic way.

* The policy prevented a conventional debt crisis but also meant Japan experienced very slow economic growth and deflationary pressures for decades.

* THE RISK: INFLATION & STAGNATION

* Inflation: If a country’s central bank buys back large amounts of government debt (”monetizes the debt”), it effectively prints new money. Unless managed carefully, this can fuel runaway inflation or hyperinflation, as seen in places like Zimbabwe and Venezuela.

* Japan has relatively low inflation, a high domestic savings rate, and cultural/political stability, allowing its central bank to take these actions without the disaster seen elsewhere. Most countries risk much greater instability if they try the same approach.

* Stagnation: Allows Japan to sustain high debt without default or inflation (unlike hyperinflation scenarios). It supports low interest rates and economic stability but risks long-term stagnation if not paired with reforms. Critics argue it’s a stealth jubilee, while proponents see it as innovative debt management.

How to Prepare

Primary risks to prepare for:

* Dangerous investments

* Insane taxes

* Inflation

Actions to Take

* Investments to Avoid

* Key Sectors to Avoid: Those which hold or rely on consumer debt, making them susceptible to defaults/jubilees:

* Financial Services (Banks and Lenders): Directly impacted by loan write-offs and higher provisions for bad debts. Regional banks with subprime exposure are especially at risk.

* Consumer Finance and Fintech: Firms issuing personal loans, credit cards, or BNPL services face elevated credit risks.

* Consumer Discretionary: Reduced spending from indebted consumers hurts retail, auto, and travel firms.

* High-Yield Debt Issuers: Companies with speculative bonds could default more readily in a downturn.

* Stocks and ETFs to avoid in appendix

* Safer Investments

* Safer Sectors During Consumer Debt Crises:

* Defensive sectors (utilities, healthcare, consumer staples).

* Companies with minimal debt exposure and strong cash flow.

* International funds less exposed to US consumer credit.

* The Ron Swanson Approach

* Crypto

* BTC price over time: https://www.coinbase.com/price/bitcoin

* ETH Price Over Time: https://www.coinbase.com/price/ethereum

* As much self reliance as possible to hedge against hyperinflation risk

* Food

* Shelter

* Medicine

* Defense

Episode Transcript

Simone Collins: [00:00:00] Hello Malcolm. I’m so excited to be speaking with you today because we are gonna be talking about debt, jubilees and debt in general because we live in CL world timeline where debt is getting really weird US consumer debt levels. They’re currently at record highs. I mean, it’s no surprise to anyone, right?

Both in nominal and in inflation adjusted terms.

Malcolm Collins: Hold on. Our fans may not know what a debt jubilee is. Mm-hmm. So Simone and I have a ongoing sort of debate on the show where she believes that eventually debt levels was in the general populace or within the government, are going to get so high that they’re just going to declare sort of bankruptcy either society wide or government wide.

And if you are like, that could never happen, which is my general take on this. Mm-hmm. Simone points out, actually a number of countries have already done this. Yeah. Malcolm, not

Simone Collins: us, Simone. Yeah. Ha. And I’m gonna get into it. So this

Malcolm Collins: happened a bunch of times historically. Mm-hmm. And so we’re gonna investigate when it’s happened historically, what triggered that.

Mm-hmm. And what does that [00:01:00] mean? Is the probability of it happening here and what does that mean for society that this is even like hanging around as an option.

Simone Collins: Yeah. And we’re gonna look at consumer debt and we’re gonna look at national debt because both are really important and both affect everyone in terms of like.

What should your savings strategy be? What should you be investing in? What should you not, if you have money, should you bother? Like, should you just max out your debt? And this is coming from the woman who

Malcolm Collins: purposely makes us have no debt even on our houses. How, how, how do you I’m allergic

Simone Collins: to debt. I, I, I can’t be owed anything.

If someone pays me a compliment, I have to pay it back right away because I can’t even deal with that. You understand? Like, I am, I’ve, I’m phobic. I’m sure there’s some Latin word for it. But yeah. Anyway, I, I learned that there was some like Latin word for mirror divination this morning. So I gotta find the one for, for ness of de of debts.

But anyway, like speaking of debt like just bad toxic consumer debt is insane right now. The average credit card debt among cardholders in the [00:02:00] United States, this is like their unpaid balances. It was true around 7,321 in the beginning of 2025. That’s, that’s up almost 6% from 24.

Malcolm Collins: No, wait. What showed me that our relationship was debt, it’s completely unraveling is, I don’t know if you guys remember, ‘cause we covered it on the show, but there was this thing where like dumb people in America thought there was a free money hack.

Yes. The check fraud hack. What Free Money Hack was is they would put in bad checks, like just write checks that were bad. Yeah. And then put them in their banks like auto cash thing and it would give them cash and they thought they had just gotten free money. Yeah. And now, and then they all found out like, oh wait, like the bank recorded that transaction.

I just now owe this much money.

Speaker 3: Some glitch in the Chase banking app where you can deposit a large check. That is bad. Yeah. And then you have a short time limit to actually withdraw the money in cash from the ATM before the check is cleared. And I guess absolute idiots. They’re doing this on their own [00:03:00] accounts. And then you have other people who are doing this on their own accounts.

Speaker 4: It has their first and last name, their phone number, their social security number, their place of work. Why do I have 11,000 missing from my bank account? Damn. Is this like humorous to you guys? Like do you, yeah. Is this, is it? Yes.

Speaker 6: They will use these. There’s no way.

Simone Collins: Yeah, yeah, yeah. No. Like, and that, that is, that is the culture we live in today. Yeah. Social media really doesn’t help that. And there’s some great viral Caleb Hammer clips where. People are like, oh, well I’m gonna, you know, retire early and travel a ton. And you know, he, at that point, this is for the show financial audit on YouTube, has gone through all their finances.

He knows how much their debt, he knows how much they’ve saved. And he’s like, dude, you. You have no money saved, like, how do you think this is gonna work? How much money do you think they need? And they’re like, oh, I’m just gonna, [00:04:00] like, you know, house hacking something, something. And they just start using a bunch of buzzwords and it’s just clear that like their entire financial strategy is based on tiktoks that are not even like well-founded.

It’s really disturbing. I’ll, I’ll send you a clip. Oh

Malcolm Collins: my God, I love this. A house hacking, of course.

Simone Collins: Yeah. But like, and like literally even the way that they, they use the language implies that, that like they’re just putting in buzzwords and they don’t actually understand the fundamentals of any of this.

They don’t understand what fire means. They don’t understand really what house hacking means. They, they have no understanding if how much anything. Like, it’s weird ‘cause it’s the poor man version of that meme where I can’t, I don’t even know the TV show, but that woman’s like, I don’t know, how much can a banana be $10?

I don’t have time for this.

Speaker: I mean, it’s one banana. Michael, what could it cost? $10. You’ve never actually set foot in a supermarket, have you? I don’t have time for this.

Simone Collins: But it’s like, this is on both ends of the spectrum, you know? Like, I don’t know how much could it be to travel around the, the world all the year, like $30,000.

Malcolm Collins: We did this because we have [00:05:00] friends who live off of welfare who are are close friends of ours and help, help take care of our kids partially.

And they get way more expensive stuff than we get. Like, like pretty much, much. Oh my god. Wherever we are buying something and they are buying something, what they buy is dramatically more expensive than what we buy. Like they buy. Oh yeah, no, we

Simone Collins: get the bargain basement, BJ’s diapers, and they, they get fricking pampers.

That’s like the, that’s the diapers. Like

Malcolm Collins: they have subscriptions to like multiple streaming services, which I just find like obscenely luxurious. Yeah. Like literally

Simone Collins: when we want to watch, when we wanted to watch K-Pop Demon Hunters on Netflix. We, we, we had to log into my dad’s account and then get him to like, call in and give us a code because he was maxed out on all his shares of shared accounts.

We have bought

Malcolm Collins: more cars since we have known them in like the two years we have known them than we have bought in our entire lives by like a factor of two.

I know, I know, I know,

Simone Collins: I know what you gonna do. But again, like that’s, that’s why we need to have these conversations about money [00:06:00] and figure out what we’re doing because again, like while they’re able to do that, also assistance that they receive from the government is not gonna last.

Like, this money is going to run out or. Technically it may not run out, but its purchasing power is going to erode so much that it is not going to matter anymore. So again, let’s get back to it. So credit card debt obviously really high and credit card debt is, is a key thing to look at because of the high interest rates where it sort of balloons to this point where basically you’re never gonna repay it.

You know, when your interest rates like 30%, you’re never gonna repay that debt. It’s just gonna be there with you forever. Mm-hmm. And people are using buy now pay later services like Klarna and Afterpay at record levels and increasingly they’re paying late, which is also telling one lending tree study.

Found that our survey found that 41% of buy now pay later users made a late payment in 2025, up from 34% the prior year. So we’re going from a third, 45%

Malcolm Collins: of buy now, pay later

Simone Collins: 41% made a late payment this year. Oh. And that was, oh my God.

Malcolm Collins: I remember back when, when I, like early in my [00:07:00] finances days when I was building up my credit.

Yeah. I used to have this like existential fear of ever missing a payment. I was, I was, I’ve always had

Simone Collins: automatic payments, always on every card you’ve, you’ve ever had. And I, I, I haven’t even until very recently, been able to stomach the idea of an automatic payment. I would just, every single week pay the card off.

‘cause I was like, I’m not waiting. How could I have No,

Malcolm Collins: but recently, I don’t know, automatic payment has gotten better or something like that. But I don’t, I I remember there was a couple cases in the past where I actually did miss payments and it freaked me out.

Oh my God.

Yeah. But this is years ago. I have a, a near perfect score right now.

Simone Collins: No. Yeah. Our scores I don’t think have ever been higher. Which is weird because I thought that when we, we completely paid off our mortgage. That, that no, that, that

Malcolm Collins: has dinged me. I’m, I, my score has gone down for a tie because we paid off our mortgage, which means we don’t have as many length of credit.

Simone Collins: Yeah. But that also, I mean, like you only need a really good credit score if you’re, you expect to take on a ton of debt,

Malcolm Collins: but get to the juicy stuff. Come on. Right.

Simone Collins: Anyway, so I’m just, I’m, I’m framing this a little bit. And, and, and I’m just pointing out that [00:08:00] people are beginning to view debt payoff and the concept of capitalism and even just faith and fiat currency with increasing skepticism, loan defaults and late payments are on the rise.

Democratic socialist political figures like Zoran, mom, Donny, are gaining serious traction. The betting odds have him at about 95 to 96% now. He’s even citing them in his speeches now ‘cause he is just like, I. Don’t ask me, ask the, ask the people putting money on this. And even our governments are spending like someone with zero expectation of, of paying off their debt.

So US Social Security is likely to falter in 2032 to 2034. That’s in less than 10 years. The UK is, is set to experience a social security crisis in the early 2030s as well. And this matters because something’s gotta give. And in the past this has involved various forms of debt. Jubilee, even though you say that this just doesn’t happen.

So what we’re gonna discuss and what I’ve, what I’ve researched is this situation with consumer debt today, this situation with government debt today, because I think people don’t really realize it or they need to be reminded [00:09:00] how unsustainable debt has been dealt with historically, how this could go poorly.

Because there are times when people tried to. Sweep it under the rug and it doesn’t go well. And then how this could go well and how individuals might prepare, like how maybe we should rethink our investing strategies based on all this. Okay. So yeah, this is, this is important. So US consumer debt is.

Really high. We’re at an all time high reaching 1.21 trillion in Q2. That’s, that’s just, it’s, it’s, it’s getting, people are using a lot of debt. Credit card interest rates are 22 to 24% this year. And that’s, that’s compared to around 15% last year. So not only do people have tons more debt than before, or a lot more debt than before, but like the interest rates are higher, meaning they’re way less likely to be able to pay it off.

Right. So we’re, we’re getting sort of, we’re reaching terminal velocity here. Delinquency rates for credit cards and other non in-housing debts have increased to levels well above the pre pandemic norms. In Q2 of this year, about 4.4% of all debt was in some phase [00:10:00] of delinquency, which just is quite high, you know, it seems like, oh, just 4%.

But like, that’s, that’s pretty high. And Klarna, that’s the buy now pay later company reported a 17% increase in consumer credit losses in Q1. That’s about $1.36 million. So. It’s, it’s, it’s, it’s not good. Student loan delinquencies are also rising, and this is a form of debt in the United States that’s harder to evade using bankruptcy or well, sort of impossible to evade using bankruptcy.

And this is especially after, during the pandemic, there were a lot of like, sort of, we’ll just put this on pause things, and a lot of people thought that it was just gonna be canceled. But yeah no, it’s not gonna be canceled. In March 25, just 35% of federal student loan borrowers made their most recent payments on time.

Mm-hmm. So basically two thirds of people just didn’t make their student debt payments on time, and the rest were at risk or already in serious delin, delinquency or default. So, as much [00:11:00] as I, at first was like, well, this, it’s never been worse. This is, this is actually terrible. Do you think that we’re at an all time low point, or do you think that’s not the case?

Malcolm Collins: I think what do you mean an all time low point?

Simone Collins: Like, are we in more serious debt dodo today than we have been at any other point in our lives?

Malcolm Collins: I, I guess,

Simone Collins: no, it was actually worse before, around the time we graduated from college. So US consumer debt has, has reached nominal record highs in 25, but adjusted for economic growth.

It remains below pre 2008 financial crisis peaks. It’s even declined slightly in recent quarters. So, I, I can sort of show you like, and this also tracked with bankruptcy trends as well. I, I can show you the Google trends for bankruptcy. And it, it peaked around 2008 with that H housing crisis.

So we were actually. You know, as much as things are bad now they’re not at an all time bad. I think things are just a little bit different. Like buy now, pay later [00:12:00] services did not really exist then. People didn’t have the same kind of absurd absurdist to, yeah, these numbers

Malcolm Collins: don’t look high now at all.

Come on, Simone. This looks relatively normal.

Simone Collins: Ah,

If anything we’re at like a low point. The we’re Yeah, it’s, it’s, it’s interesting. Yeah. I mean, like this, I’m, I’m putting this here because I thought that we were at an all time bad point and, and this surprised me. So I do wanna point it out here, but I also at the same time think that the, the mental attitude toward debt combined with our collective pessimism around capitalism and the ability to get jobs at all at this point.

Still makes it different and more dangerous than it was in the past. Mm-hmm. And we’re gonna get into it, but in the past, every time there have been debt jubilees with consumer debt or what you could call consumer debt, like with average people, it hasn’t been because technically they’re in more debt and they can’t pay it back.

It’s because technically they’re showing extreme signs of unrest. [00:13:00] And that’s what I’m feeling. That’s the, that’s the sentiment and the, the zeitgeist right now. Okay. Okay. So, so that matters more.

Malcolm Collins: Explain to me how this has happened before, because right now I’m still thinking, okay, people took out dumb debt, but my thought is still, but companies own this tech debt, pension plans, own this debt.

Nobody’s going to, like, how can you convince them? How can you just take that money from them? Right. Like, well, and I mean, yeah.

Simone Collins: So another, another argument against my point in, in favor of yours is that GR in the US is. I don’t know how this, it’s incredibly soft on people. Basically, you have bad credit for 10 years and non-essential assets can be frozen, but you’re still, like, you can have a car.

You’re allowed to keep, like most of your stuff, like, not luxuries, but like, you actually don’t lose that much. And I think a lot of people, the attitude is just, oh, I’m just gonna declare bankruptcy. It’s fine. No bankruptcy.

Malcolm Collins: The United States actually has an, i, I would say, an incredibly generous and lenient policy [00:14:00] towards bankruptcies, which I think put us in a form of like pseudo communism already.

Yeah. It’s like communism. It’s like capitalism was like gutter rails in Yes. Like you have to keep. Like, like your life is like not, you’re not like an a, a a in debt, in debtor slave or whatever, like used to happen. Right. You know, you don’t even have to go like live in the slums if, if you declare bankruptcy, right?

Mm-hmm. Like, it’s just sort of like, okay, all of the really expensive stuff you own that isn’t part of your, like, daily life that you’re not able to hide well at that, or that you don’t hide well, yes. Yeah. Which, you know, how many people

Simone Collins: are declaring bankruptcy with like a ton of stuff in crypto, cold wallet somewhere.

You know what I mean? Yeah. Which is, it’s, it’s, it’s kind of messed up and that’s why, again, I, I’m pointing to the sentiment more than the actual numbers. And it, it, it still really worries me. But what worries me more is government inability to pay debt obligations. So, like I [00:15:00] said, US Social Security projected to be insolvent by late 2032.

That’s really freaking soon. UK State pensions are, it’s, it’s pay as you go and it’s generally funded from current taxes. So there are major concerns about the sustainability of the defined benefit, both private and public pension plans and, and the adequacy of future benefits. And, and remember, like what it, what the per capita GDP in the UK is worse than the, that of the poorest state in the us right?

Malcolm Collins: Yeah. Yeah. For people who don’t know this, the per capita GDP of the uk is, is lower than, I think it’s Mississippi or Alabama. I don’t remember this one.

Simone Collins: Yeah. And, and so that’s, that’s scary. And other western countries also face sustainability crises in, in the early 2030s. So, you know, okay.

We’re maybe like five years away from starting to see. And bad things happen, but it’s, it’s getting there. Canada’s currently better positioned [00:16:00] actually due to earlier reforms ‘cause they had a, a crisis a little earlier on. But I don’t know. They’re also like, oh, you can’t get the medical care you want.

Why don’t you consider maid why don’t you just end your, end your pathetic existence? So, I don’t know. I feel like they solved it, but not in the way that people want by just being like, yeah, you should consider dying. And basically all systems are going to require some form of benefit reduction or tax increases or later retirement ages just to remain sustainable.

So we also just need to be aware of the fact that, okay, while you’re saying yes, Simone, the government’s or the US is already on this like quasi. Communist system where people just kind of fall back. You know, they declare bankruptcy and they go on government assistance and everything’s fine.

And it’s like, yeah, that’s fine right now, but it’s not gonna stay that way. So let’s, let’s just take a break and look at the past for a second and see how this has gone well and see how it’s gone Poorly. Historical [00:17:00] jubilees are, are interesting and they just didn’t know about them. But basically like people, rulers have repeatedly canceled debts without consent from creditors to end evade or calm rebellion, turmoil class, conflict revolution or societal breakdown.

Like any, any sort of form of like, oh my gosh, just will just like, make it disappear. And a ancient Mesopotamia, king, kings of Sumir, Babylon and, and neighboring mm-hmm. Areas regularly or periodically cancel debts for peasants and small landlords often at the start of their reigns. So you like come in as a new king, you’d be like, don’t you love me?

You don’t have to pay your debts anymore. Which doesn’t seem that dissimilar from like campaign promises made by politic. Well, if you’re a king or

Malcolm Collins: something like that, it’s a little different. Yeah. And there’s a lot of reasons you might do this that you wouldn’t if you were a democracy. So when you’re a king, you’re basically being like, what’s less likely to kill me?

You know, the bankers or the, the [00:18:00] citizens. Right. Especially if I’m about to do a paw grom or something like that. The bankers, right? Like they’re, they’re way less of an active danger to me. And especially if I’m canceling debts on like, big, rich people debts too. Right? So like, I, I think that there was less participation in debt marketplaces in that time where now if you cancel debts, it’s granny social, you, you know, retirement pension that you’re actually robbing rather than you know, some, some, you know, secluded minority, ultra wealthy population.

Simone Collins: Yeah. Who is like pretty easy to take out, you know? ‘cause you didn’t care about them. Yeah. So let’s jump forward though to, to ancient Greece. Where Solon, so Solon. Yeah. Solon. He’s like the early democracy guy, right? Yeah, I guess, yeah. So yeah, Solon was one of their pioneers of democracy. If I’m remembering correctly, I’m thinking back to this great courses lecture, but all I can really remember is the cadence and accent of the woman, the female [00:19:00] professor’s voice, and not what Solon actually is famous for, which is really annoying.

But yeah, so Solans CEC Thea in 594 BCE involved forgiving personal debts. He banned debt slavery, and he wiped out mortgage debts in Athens. And this was originally considered really controversial but it was eventually credited with preventing revolution and laying the foundations for Athenian democracy.

So credit eventually did resume as societal structure stabilized. And this is, I think one of the, the earlier examples of both. Democracy being either enabled or protected by this action. But also about how like, well, well this does initially lead to a crisis of like people being willing to, to give debt, which is essential for innovation and growth and capitalism in general.

Malcolm Collins: Yeah. Like debt is very, very important to make democracies and society work.

Simone Collins: Mm-hmm. It basically like greed and opportunity will bring it back with [00:20:00] time. If, if basically the, the, the, the, the Jubilee is executed in the name of creating a stable society instead of just sweeping something under the rug.

And I wanna highlight this as a core. In my view separation point between the success cases and the failure cases, there are the failure cases where people do this out of greed or I just don’t wanna deal with it, or just give me the power or vote me in. Yeah. And it goes really sideways. And then there are the people who are like, guys, this is really gonna suck.

Like I, I, I don’t know how to tell you this, but we have to do it for the good of our future. It goes really well. If, if initially second. So

Malcolm Collins: tell me those cases, when, when has it worked out other than ancient Greece where again, it’s not really analogous ‘cause you’re not taking it from granny.

Simone Collins: Yeah. So the, I, I, this is Japan.

Japan,

Malcolm Collins: okay. Because Japan has

Simone Collins: actually done this a ton.

Malcolm Collins: Like oh, a lot. Like how many times has Japan done this? [00:21:00] Why doesn’t anyone lend money in Japan? Like I know, I

Simone Collins: know, I know. Because we, Japanese because they are a, a collectivist culture that takes care of their own. And they’re also, I, I would argue, they’re very future oriented. They’re very responsible and they do care about the collective good in a way that’s like very deep set and cohesive that you just don’t really see in more diverse, competitive and less cohesive cultures. So this first happened in medieval Japan during the comma, kura and achi periods.

The, the shogun issued edicts known as Toku se, like literally virtuous government or beha benevolent rule which effectively functioned as debt jubilee. They, they were decrees that canceled debts often in response to peasant uprising given by like, and this was typically driven not by like irresponsibility, but just bad stuff happening, like famines or epidemics or, or it’s in some cases exploitative lending [00:22:00] practices.

And this, this stated actually even earlier, back to the roots in like the NARA and high-end periods. It’s like seven, 710 to 1185, but it became more prominent in the 13th to 15th century. So again, this is going like way back and they did it a lot. The most famous early example is the inin to, let’s see, to of 1297 issued by the ka kog.

It anul all debts contracted before that year allowed vassals to reclaim pond lands without repaying the loans. And it canceled interest on older debts. And it was motivated by the need to bolster the mi military strength and basically protect Japan against Mongol invasions and to address widespread debt burdens among the Warrior class.

So this wasn’t like, oh, do it because I wanna become, you know, like I wanna be secure as the Shogun, or I wanna like take out this one group that I hate. It was like, oh man, the Mongols are coming and. Our warrior class. [00:23:00] Like they, they’ve lost their lands due to like bad debt.

Malcolm Collins: Due to bad debt.

Simone Collins: Yeah. Like we need to protect our land.

So like, maybe we should rebuild a more stable society so we don’t get totally wiped out by the Mongols like everyone else is. Which is, is really, really interesting. So, so there were more but I’m gonna, I’m gonna skip forward to the one that I think is the most scary. That I’m like, Hmm, I could, I could see this kind of happening, especially given the trends that are happening in our government now.

Or like, not in our government, but like sort of the, the vibe shift taking place with regard to skepticism around capitalism and what politicians are getting popular for. So this is the one I’m like, Ooh. So this is world War, post World War II currency reform and debt resolution in Japan in 1946, after Japan’s defeat in World War ii, the government faced massive sovereign debt about 267% of national income by March, 1945.

And this

Malcolm Collins: was Japan?

Simone Collins: Japan, yeah. Who have their aing

Malcolm Collins: about this [00:24:00] is it happened in part due to demographic collapse.

Mm.

And so we’re looking at a scenario that’s very similar to what the rest of the globe might be going through in the near future.

Simone Collins: Yeah. Well, and, and this is, you’re also gonna see this with the next one that happened more recently.

As, as part of what’s come on. Oh, what’s name? So, when

Malcolm Collins: Japan did this, did they do it for all kinds of debts? Like was No, hold on.

Simone Collins: No. This, this is, no, this is way scarier. This is way scarier than a, a, a debt jubilee. But oh Aon omics. You’re thinking about the abenomics reform. This is, this is different and this is more violent, so, right.

So we had massive sovereign debt. We have hyperinflation, we have economic ruin. You know, they got nuked like it, this was a really bad time for the Japanese people. Yeah. Bad time. They needed to rebuild and they basically had like no ability to do so because like nothing was worth anything.

Everything’s broken, everyone’s starving. Like this is horrible. So while this wasn’t explicitly a jubilee, the 1946 financial emergency measures effectively wiped out much of [00:25:00] the real value of debts through currency reform and wealth confiscation. So this isn’t just currency reform, it’s wealth confiscation, which is.

100% starting to bubble up in various state. Yeah. Non-national legislatures. It

Malcolm Collins: always goes really bad.

Simone Collins: Like, have you, are you familiar with the California bill that was proposed or that’s, that’s gonna be voted on this, this election? No. I can’t remember exactly what percentage of it it, it is, but it’s this bill that’s like, Hey, shall we just, you know, we have some financial troubles, shall we just like, have all billionaires in California pay 5% of their net worth?

And this includes just like the value of, of their stocks. Like, not even like their cash, right? Yeah. To, to help us pay off this debt. It’s just a one time thing and like. Like the guys on the All-In podcast who are all billionaires and like, I think one or two of them is still in California and most of them got out obviously.

And this is, this is effective like beginning 2026 if it’s passed. So, you know, they’re all [00:26:00] just gonna like, move out in a second if this gets passed. And, and they’re all like, well, why would people not vote to pass this? Like the vast majority of people are not billionaires and they don’t care. Yeah.

And you would like the billionaires to just handle a problem. But this is an example of legislation that is already being voted on right now in the United States of just like, Hey, why don’t we just confiscate the wealth of the, of, of wealthy people? And that again, this is part of what this Japanese measure was.

So here’s what exactly happened to Japan in 1946, on February 16th. In 1946, the government announced surprise measures. Surprise measures. Okay. This voted up. Surprise. So you don’t

Malcolm Collins: get a chance to leave first.

Simone Collins: Yeah. They, they, they didn’t get the warning that the all in podcasters got. Mm-hmm. All bank accounts were frozen.

All the Y notes were invalidated unless deposited. So if you’re holding a dollar, it doesn’t work anymore. And a new yen was introduced at a one-to-one exchange rate. Withdrawals were severely limited initially. 300 yen per household [00:27:00] head, plus 100 yen per member later. 100 yen per month per person.

Barely enough for, for survival. So just to be clear, again, your money doesn’t work anymore. All the cash you have is, is broken. Only the stuff you have in banks is still valid with now a different kind of yen. But you, you, you’re only allowed to withdraw. Yeah. A tiny amount, barely enough to survive. Okay.

A