The Paul Truesdell Podcast

566 episodes — Page 1 of 12

You Want To Kill Your AI Buddy? Here's Why

Antifa - Domestic Terrorism - Cleaning House - War Coming

Kaiser's Coffins to Killer Swarms - Why Cheap, Expendable Drones—Not Billion-Dollar Platforms—Will Decide the Next Century of American Power

The 2033 Deadline: What Every American Over 55 Needs to Know About Social Security and The Truth About Social Security's 2033 Problem

THE FUTURE OF DRONE TECH: NAVAL LAUNCH PLATFORMS, AI, AND MORE

Five Counts Down, the Rest of the Cabal to Go: The Morens Indictment Is Just the Start

May 22, 2026

May 21, 2026 - B

May 21, 2026 - A

Ocalawood

Either the President Owns the Wreckage or He Owns the Rescue. Pick One

The Middle-Class Millionaire Trap - Why Financial Comfort Doesn't Protect You From

The Movies Home With Sneaky China

Sleep

A New Dawn of Americanism: America Is Back at the Bargaining Table — and the World Knows It

When Britannia Ruled the Waves — and When She Stopped

AI Is Making People Average

Russia Cannot Deliver - Why Higher Oil Prices Are Not Saving Moscow — and What That Means for Your Portfolio

Why Higher Oil Prices Are Not Saving Moscow — and What That Means for Your PortfolioPaulTruesdell.com Picture a warehouse full of product the world suddenly wants to buy. The orders are coming in. The prices are the best they've been in years. The problem is the loading dock. Someone has been quietly, patiently, methodically disabling the loading dock — not once, not dramatically, but in waves, each one designed to make the next repair harder than the last. That is Russia's position in the global energy market today. And the people responsible for it have been working toward this outcome far longer than the recent headlines suggest.When the Iran conflict pushed global energy prices up 40 percent, most financial analysis treated it as an uncomfortable windfall for Moscow. The logic was clean on its face: Russia sells oil, prices rise, revenues follow. What the logic skipped was the operational question — the question of whether Russia retains the physical capacity to move its product to market. It does not. Not anymore. Not at anything close to the scale it needs.The first layer of the strategy targeting that capacity is Ukraine's sustained campaign against Russia's export terminal infrastructure. These are not sporadic strikes designed to make a point. They are a deliberate, repeated effort to keep port facilities offline long enough that Russian repair crews cannot restore function before the next wave arrives. The Black Sea ports at Novorossiysk — Russia's primary southern export corridor — have operated at sharply reduced throughput throughout the Iran conflict. Ukraine has now extended the same methodology into the Baltic, attacking the northern export corridor that serves Russia's European and Asian customers. The combined effect has reduced Moscow's total export capacity by approximately 40 percent. The number is moving upward, not stabilizing. The second layer arrives further down the chain and carries a different kind of significance. France and the United Kingdom have crossed a line that three years of sanctions rhetoric never crossed: they are physically stopping Russian shadow fleet tankers in their coastal waters. The shadow fleet — the collection of aging, often uninsured vessels that Russia assembled precisely to move oil outside the reach of Western financial pressure — depends on access to established shipping lanes. The English Channel is the natural exit route for tankers leaving the Baltic. When France and Britain plant themselves at that exit, shadow fleet tankers reroute north around Scotland. The detour adds 10 to 20 percent to transit time per voyage. At full fleet scale, the added operating cost runs to approximately one billion dollars annually. More consequential than the dollar figure is what the added time does to effective capacity: a fleet running 15 percent slower is a fleet that has been functionally reduced by 15 percent without a single additional legislative instrument. Britain's prime minister was traveling to a conference with other NATO members as this episode was being prepared — a conference specifically focused on what comes next for the shadow fleet. France and Britain putting their chips on the table first was not coincidence. It was positioning.Now here is what the official accounts leave out, and a serious audience deserves to hear it plainly. The coordination behind this three-layer strategy did not emerge organically from separate governments acting independently. There are agencies — the kind with three letters and no public comment policy — that have been working on Russia's energy revenue problem for years. The architecture of what we are watching unfold, the timing of the Baltic escalation, the sequencing of NATO interdiction, the precision with which Ukrainian drone campaigns have escalated from proof-of-concept to sustained operational pressure — none of that happens without planning that begins in rooms that do not appear on organizational charts. This is not conspiracy. This is how serious nations conduct economic warfare against a nuclear-armed adversary. You do not put it in a press release. You put it in motion and you let the results speak.There is also a larger strategic frame that most financial commentary is missing entirely. Donald Trump understands something that most diplomats spend careers trying not to say out loud: leverage works best when it is applied to multiple pressure points simultaneously. Russia and China are not operating in isolation from each other, and the people managing American strategic interests know that. A Russia whose energy revenues are collapsing is a Russia that becomes a more desperate and therefore more demanding partner for Beijing. A China managing that relationship while simultaneously navigating its own economic pressures and trade exposure to the United States is a China that has less room to maneuver than it appears. The art of the deal, applied at geopolitical scale, is not about one negotiation. It is about

The Wall Street Journal's Dirty Little Secret

The Wall Street Journal's Dirty Little SecretLet me be perfectly clear about something. I rarely read comment sections. Life is too short, and my time is too valuable.But this morning, I made an exception.The Wall Street Journal ran a piece about President Trump. He likes a particular brand of dress shoes. He buys them out of his own pocket and gives them to people. As gifts. Because he's generous and he found something he likes. I personally favor Stacy Adams — good fit, fine construction — and I own most of the brands mentioned in the article. So I read it. It was a pleasant, harmless little piece showing the human side of a man the media has spent nearly a decade trying to dehumanize.Now here is where it gets interesting.You need to understand something about how the Wall Street Journal manages its comment sections — because there is a pattern, and it is not subtle once you see it. Not every article at the Journal allows comments. Many do not. But the ones that *do* allow comments? Pay attention. The articles that tend to attract comment sections are the ones that *mock* President Trump, *criticize* President Trump, or otherwise provide red meat for the Trump Derangement Syndrome crowd. And that crowd shows up. Every time. Reliably. Like clockwork. Low-brow, mean-spirited, factually hollow commentary that adds absolutely nothing to what was once one of the most respected financial publications in the world.Here is what I have done in the past. I have called those people out. Not with insults. Not with profanity. With facts. With plain spoken, professional observations about the quality of their commentary and their contribution — or rather, their spectacular *lack* of contribution — to serious public discourse.And I have been throttled for it.My comments don't appear anymore. Not because they are derogatory. Not because they are mean. Because they are *factual*, *direct*, and *insufficiently hostile to the President of the United States*. That, apparently, is the standard the Wall Street Journal's comment editors have adopted.Today, a gentleman posted that the shoe article was cute enough, but it belonged in People magazine — not the Journal. That was an insightful observation. I agreed with him completely, and added that the article had nonetheless accomplished something useful: it brought the Trump Derangement Syndrome crowd out of the woodwork, which provides rich material for future commentary.Rejected. Banned. Gone.And then he reminded me — because he had noticed — that many of my past comments, few as they are, have met the same fate.So I went back and looked. The pattern is undeniable. Criticize the TDS crowd? Blocked. Agree with a reasonable reader that professional standards matter? Blocked. Post something calm, factual, and plain spoken that happens to be insufficiently contemptuous of Donald Trump? Blocked.But rant like a lunatic about shoes? *Published.*The Wall Street Journal's comment editors have Trump Derangement Syndrome. That is not an accusation. That is a fact pattern. And here is why it matters beyond my own mild irritation at being censored in a publication I pay for.This is *exactly* what happened to Twitter.A once-powerful platform, rotting from the inside. Editors and moderators — drunk on ideological certainty — systematically silencing one side of every conversation while amplifying the other. Professional, factual voices throttled. Unhinged, deranged voices amplified. The inmates running the asylum. And the audience, slowly but surely, noticing. Trust eroding. Credibility collapsing. Until finally the whole rotten structure was so compromised that one man with a checkbook and a commitment to free speech walked in, paid forty-four billion dollars, and blew the whole thing up.Elon Musk didn't buy Twitter because he had nothing better to do. He bought it because what was happening there was a scandal hiding in plain sight — and the people responsible were too arrogant and too ideologically captured to see it coming.The Wall Street Journal would do well to study that history. Carefully. Because the readers who once made this publication great are watching. And they are not confused about what they are seeing.I will keep my subscription. For now. There is still good financial reporting buried in these pages, and I am not the kind of man who walks away from a fight.But I will tell you this. I would not be even slightly surprised to open my email one morning and discover that my subscription has been cancelled. Not because I missed a payment. Because I had the nerve to say — plainly, professionally, and without apology — that the Emperor has no clothes.And now you know — *the rest of the story.*Tippecanoe and Tyler Too, I'm out of here.Truesdellwealth.com Paul Grant Truesdell, J.D., AIF, CLU, ChFC, RFC Founder of The Truesdell Companies Truesdell Wealth, Inc. A Registered Investment AdvisorThe Truesdell Professional Building 200 NW 52nd Avenue, Ocala, Florida 34481 352-612-1000 This

The Bill Is Coming Due — And Nobody Wants to Hear It

The Bill Is Coming Due — And Nobody Wants to Hear ItGovernor DeSantis said it plainly this week in Kentucky: Interest payments on the national debt now eclipse defense spending. Our national debt is projected to reach a record $64 trillion by 2036 — triple the pre-COVID figure. Twenty-eight states have already passed resolutions supporting a federal balanced budget amendment. Every state except Vermont has a balanced budget requirement in its constitution. It's time Congress lived by the same rules the rest of us do.I've been watching this slow-motion train wreck for a long time.Back during the Obama years, I stood before a room of about 50 retired men and women — clients and prospective clients — and walked them through the numbers. The national deficit. The debt. Then the unfunded mandates at the federal and state level. Then municipalities — pensions especially — Chicago, Baltimore, Detroit. When I added it all up, my estimate of total unfunded obligations was somewhere around $34 trillion.The room went quiet. Not the good kind of quiet.It didn't go over well. Denial is a powerful thing, even among smart people.That was then. Today, the federal debt alone is approaching double that figure — and we haven't even started counting the unfunded mandates, state obligations, and municipal pension disasters still sitting off the books. My best estimate now? We are approaching — or will soon reach — **$100 trillion in total obligations** when you fold it all in.History is not kind to nations that reach a certain ratio of debt to gross domestic product. Revolutions happen. I don't want that. It's bad for business. It's bad for everything. But you can feel it in the tone and temperament of the country right now. People are not happy. And I'm watching more and more younger Americans channeling Howard Beale — the fictional television anchor at the center of the 1976 film *Network*, brought to life by the brilliant Peter Finch. In one of the most memorable scenes in American cinema, Beale throws away the script, leans into the camera, and tells his audience to open their windows and shout into the streets: *"I'm mad as hell, and I'm not going to take it anymore."*The performance was so powerful, so achingly human, that Peter Finch won the Academy Award for Best Actor. He never got to hold that Oscar. He died of a heart attack in January 1977 — just weeks before the ceremony. The Academy awarded him posthumously, the first time in history that had ever been done.That scene is fifty years old now. It feels like it was written yesterday.Here's what worries me most for my clients and their generation: as Boomers pass on and Millennials take their place, there are simply fewer of them. That younger generation is going to have serious voting power — and they may decide they're done paying for benefits they'll never receive. The cuts that follow could be substantial and swift.The solution has never been complicated. It's always the same three choices: **make more, spend less, or adjust your expectations.** Some combination of those three is the only path forward. It has never been more difficult than that.But something has to give.---*And with that said, as I always say, Tippecanoe and Tyler Too — I'm out of here.**— Paul Truesdell, Truesdell Wealth, Inc. | Fiduciary Advisor | Ocala, Florida*

All Men Are Created Equal?

Scheduling Prevented Paul From RecordingTHE GREATEST SENTENCE EVER WRITTENWalter Isaacson’s Timely Meditation on America’s Founding CreedA Discussion, Elaboration, and OutlineIntroduction: Thirty-Five Words That Built a NationThere is something audacious about writing a book on a single sentence. But when the sentence in question is the second line of the Declaration of Independence—the one that begins “We hold these truths to be self-evident”—the audacity seems proportionate to the subject. Walter Isaacson’s The Greatest Sentence Ever Written, published by Simon & Schuster in November 2025, is a slim volume—barely 67 pages of main text—that punches well above its weight. Timed to the approach of America’s 250th birthday in 2026, the book is part historical detective story, part philosophical meditation, and part civic sermon. It is also, unmistakably, a plea: in an era of corrosive polarization, Isaacson wants Americans to remember what they agreed upon before they started disagreeing about everything else.The premise is deceptively simple. Isaacson takes the 35-word sentence drafted by Thomas Jefferson, edited by Benjamin Franklin and John Adams, and examines it the way a jeweler examines a stone—word by word, facet by facet. In doing so, he illuminates the Enlightenment philosophy, the political pragmatism, and the personal contradictions embedded in the language. The result is a book that reads quickly but lingers long, precisely because it forces the reader to slow down and actually think about words most Americans can recite from memory but rarely pause to examine.The Drafting: A Masterclass in Collaborative EditingOne of the book’s great pleasures is its account of how the sentence came to be. Isaacson, who previously authored a definitive biography of Benjamin Franklin, is on familiar terrain here, and it shows. He walks the reader through four drafts of the sentence, reproducing Jefferson’s original text alongside the markups made by the drafting committee. The story of the editing process is itself a kind of parable about the value of collaboration, compromise, and the willingness to subordinate ego to purpose.The most celebrated edit belongs to Franklin. Jefferson’s original draft read, “We hold these truths to be sacred.” Franklin, with his characteristic blend of wit and philosophical precision, crossed out sacred and wrote in self-evident. It is a small change that carries enormous weight. As Isaacson argues, the substitution moved the entire justification for American independence from the realm of religious dogma into the realm of rational inquiry. The new nation would ground its legitimacy not in divine decree alone, but in the power of reason—in truths so obvious they required no priestly authority to validate them.And yet, the sentence does not abandon the divine altogether. John Adams contributed the phrase “endowed by their Creator,” replacing Jefferson’s more secular formulation that people simply “derive rights.” Isaacson reads this interplay as a deliberate balancing act—a synthesis of faith and reason, providence and philosophy, that would define the American experiment from its inception. The Founders were not choosing between God and Enlightenment. They were insisting on both, and daring the future to hold the tension.The Philosophy: Enlightenment Ideas in American SoilIsaacson is at his best when tracing the intellectual genealogy of the sentence’s key phrases. The concept of natural rights—rights that exist prior to and independent of government—runs through the work of John Locke, whose Second Treatise of Government directly influenced Jefferson’s thinking. But Isaacson extends the lineage further, noting Franklin’s month-long stay in David Hume’s home in the early 1770s, where the two men discussed natural rights and moral philosophy at length. The Scottish Enlightenment, with its emphasis on empiricism and common sense, left a deep imprint on the American founding—deeper, Isaacson suggests, than most standard histories acknowledge.The phrase “the pursuit of Happiness” receives particular attention. Isaacson argues that in the context of 18th-century moral philosophy, happiness did not mean mere personal pleasure or contentment. It carried connotations of civic virtue, public contribution, and the opportunity for each generation to improve upon the circumstances of the last. The pursuit of happiness, in this reading, is inseparable from the concept of the commons—the shared infrastructure of schools, libraries, fire brigades, and public institutions that Franklin himself helped pioneer in Philadelphia. It is not a license for atomistic individualism; it is a compact about what a society owes to each of its members and what each member owes in return.All Men Are Created Equal: The Nucleus of LifeThe Conventional ReadingNo serious treatment of the Declaration can sidestep the contradiction at its heart, and Isaacson does not attempt to. He notes bluntly that 41 of the 56 sig

Deliberation, Not Debate: A Casual Conversation on Writing Your Story with AI Reflections on Session One of a Four-Part Series

Deliberation, Not Debate: A Casual Conversation on Writing Your Story with AIReflections on Session One of a Four-Part SeriesBy Paul TruesdellThis piece is written for those who attended the first session of our four-part series on using artificial intelligence to write your own personal stories. It is also written for the lady who arrived a bit late and missed the handout, for those who could not attend but wish they had, and for anyone considering joining us for session two. Consider this your on-ramp. Consider this your invitation to keep going.— — —One of the things I enjoy most in life, beyond doing the talking myself, is listening. Really listening. Not the kind of listening where you are just waiting for the other person to stop so you can say your piece, but the kind where you are genuinely trying to understand the why behind what someone is telling you.In my world, the why is what we call the qualitative analysis. You have your quantitative side, of course, the facts and figures, the hard numbers. And those numbers tell a powerful story. But sometimes the numbers alone do not tell the full story. You can have a situation where one plus one plainly equals two, and yet the consensus among a great many people will insist the answer is three. No amount of arithmetic will change their minds. You see this all the time in life. Something is objectively, unequivocally wrong, and yet to another group of perfectly reasonable folks, it is just fine. They see it differently, and that is the end of the discussion.That gap between what the numbers say and what people believe is where I like to spend my time. When I teach, when I instruct, when I advise clients on their financial futures, I like to explain the why. I like to walk people through the deliberative process. How did I arrive at this answer? How did I come to this conclusion? What is the common sense path that got us here?— — —The Difference Between Debate and DeliberationOne of the things I see throughout the world, and increasingly so, is a tendency for men and women to engage in debate rather than discussion. This is the very reason I use the phrase a casual conversation when describing what we do. I will often pair it with the words cocktail and coffee, because the image I want you to hold in your mind is that of breaking bread together, having something to drink, and simply talking. People have been doing this for centuries. It is not a debate. It is a conversation.We have all met people, usually around the holidays, Thanksgiving, Christmas, birthday parties, who turn every gathering into a contest. The conversation becomes a debate. People get excited, then agitated, then angry. Somebody storms off. Somebody else sits quietly fuming into their mashed potatoes. And every sensible person in the room thinks the same thing: I do not want anything to do with that.A wonderful conversation between people, even people who do not agree on much of anything, is one that has moved from debate into deliberation. Debate is about owning another person. It is one-upmanship. It is about winning. I have known people you cannot even share a meal with because they will turn away from you, ignore you, and only engage when they see an opportunity to elevate themselves at your expense. Whether that comes from deep insecurity or simply a gap in their personal development, I do not know and frankly do not care. The result is the same. They are debaters, not deliberators.Deliberation is about getting somewhere. It is two or more people sitting down and honestly working through a question together. It is what I sometimes call sense-making, which is the practice of not just expressing an opinion, but explaining how you arrived at that opinion, the sequence of thought and experience that brought you to where you stand. When two different opinions are laid out this way, they can both be tested, challenged, and examined. And from that exchange, you can actually make sense of the issue. That is deliberation. That is how adults solve problems.I was fortunate recently to have that exact kind of experience when I presented the first session of a four-part series on using artificial intelligence to help people write their own personal stories.— — —The Overton Window and Why It Matters Here Before I get into the specifics of what we covered, I want to take a moment to explain a concept that is useful for understanding how people think about what is acceptable and what is not, whether in politics, in public discourse, or in something as personal as your own writing style. It is called the Overton Window.The concept was developed in the 1990s by Joseph Overton, a policy analyst at the Mackinac Center for Public Policy. Overton observed that at any given time, there exists a range of ideas and policies that the general public considers acceptable or at least worthy of serious discussion. Ideas inside that window are considered mainstream. Ideas outside it are considered radical or extr

Almost Nobody Writes. Here’s the Proof. And Why That’s About to Change for You.

Almost Nobody Writes. Here’s the Proof.And Why That’s About to Change for You.A Handout for Folks Who Like FactsBy Paul Truesdell, JD, AIF, CLU, ChFC, RFC——————————Let me tell you why you’re here, or at least why I hope you’re here. You’re not here to write the next great American novel. You’re not here to craft fiction or chase a publishing deal or see your name on a shelf at Barnes and Noble. You’re here because somewhere inside you, there are stories that matter. Real stories. Your stories. The ones your children and grandchildren deserve to hear, the ones that explain where they came from and what shaped the family they were born into. Memories that will be cherished long after you and I are gone.The problem is, almost nobody actually writes those stories down. And I can prove it.The Size of the CountryThe United States population sits at roughly 342 million people as of early 2026. That’s the official Census Bureau figure, not one of those inflated estimates floating around the internet. Of those 342 million, about 260 to 270 million are adults, eighteen and older. Remember that number.Books: The Numbers Are Smaller Than You ThinkAccording to Bowker, the official ISBN agency in this country, self-published titles with ISBNs hit over 2.6 million in 2023, up about seven percent from the year before. Traditionally published titles, books that went through an actual publishing house, came in around 563,000 that same year and actually declined slightly. Toss in titles that skip the ISBN process, like many Amazon Kindle Direct Publishing e-books, and you’re looking at roughly three million or more new titles per year.Three million sounds like a lot until you realize nobody tracks unique authors. Bowker counts titles, not people. On the traditional side, industry estimates put it at roughly 300,000 to 600,000 unique authors per year, accounting for writers who publish multiple books annually. On the self-publishing side, when you narrow it down to people who actually completed and released a real, full-length book, estimates land around 500,000 to a million.Combine both sides and a reasonable estimate for unique authors publishing at least one book in any given year is somewhere between 500,000 and 1.5 million. And that high end is generous, because a whole lot of those self-published titles are barely pamphlets.Even at one million unique authors, that’s three-tenths of one percent of the U.S. population. Zero point three percent. At the more realistic estimate of 500,000 to 800,000, you’re looking at fifteen-hundredths to a quarter of one percent.Almost nobody writes books.Short Stories: Even Fewer People BotherShort stories, the real kind, crafted fiction that appears in literary magazines, journals, and anthologies, not your nephew’s social media ramblings, are an even smaller world.The top outlets like The New Yorker, Paris Review, One Story, and Granta publish maybe ten to fifty stories a year each. Smaller publications run four to twelve. Add in anthologies like Best American Short Stories, the O. Henry Prize collections, and the Pushcart Prize, and you’re looking at maybe 5,000 to 15,000 unique short stories published in legitimate U.S. outlets per year. And many of those are written by the same people, established writers and MFA graduates cycling through the same magazines year after year.Unique short story authors in any given year? Probably a few thousand to maybe 10,000, and a good number of them are also publishing books, so there’s overlap.Almost nobody writes short stories either.Put It All TogetherCombine book publishing and legitimate short story publication, account for the overlap, and the total number of unique Americans producing real, publishable creative writing in any given year is probably under one million. More realistically, it sits between 300,000 and 800,000.As a percentage of the total population? Somewhere between one-tenth and a quarter of one percent. For adults only? Still under four-tenths of one percent.Well under half a percent.But Everybody Says They WriteHere’s where it gets interesting. The National Endowment for the Arts ran a Survey of Public Participation in the Arts in 2022, the most recent detailed data available. According to that survey, about seven to eight percent of American adults said they did some form of creative writing in the past year. Stories, poems, plays, that sort of thing.Seven to eight percent sounds significant until you understand what that number actually includes. It includes the person who scribbled a poem on a napkin at Applebee’s and never looked at it again. It includes the fellow who started chapter one of his memoir in January and abandoned it by Valentine’s Day. It includes everybody who told people at a cocktail party that they were “working on something.”The distance between “I did some creative writing” and “I actually finished something” is roughly the same distance as the one between telling people you jog and actually running a m

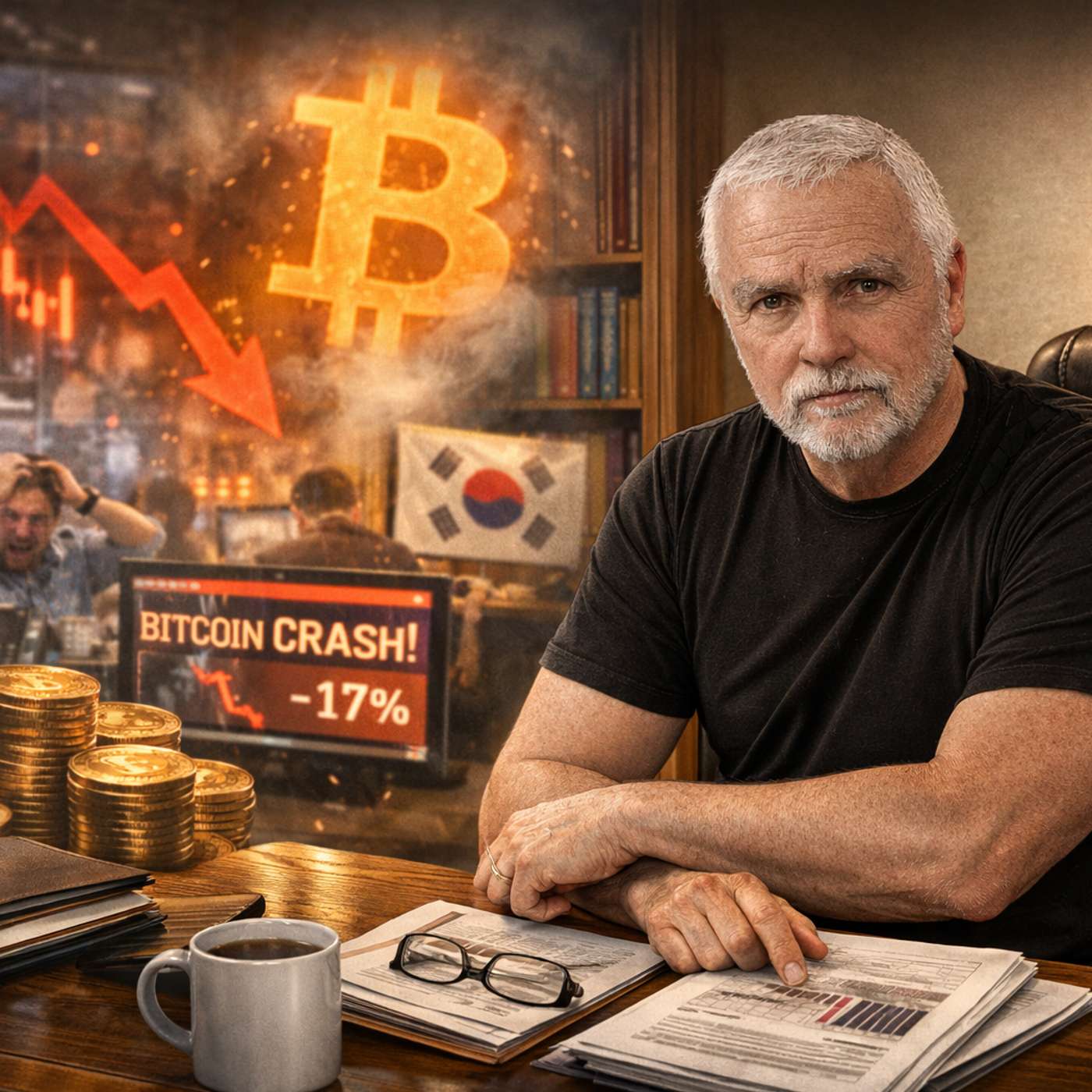

Gone in 30 Minutes

Oops. $40 Billion in Bitcoin—Gone in 30 Minutes.By Paul Truesdell, JD, AIF, CLU, ChFC, RFCIf you ever needed a reason to be skeptical about cryptocurrency, South Korea just handed you one wrapped in a bow. Bithumb, the country’s second-largest crypto exchange, accidentally gave away 620,000 bitcoins—valued at more than $40 billion—because a staffer made an input error during a rinky-dink promotional giveaway. The total prize pot was supposed to be about $425. Four hundred and twenty-five dollars. Instead, one lucky winner who was supposed to get enough for a cheap cup of coffee walked away—at least temporarily—with over $120 million in bitcoin. You can’t make this stuff up.Within minutes, enough recipients tried to cash out that bitcoin’s price dropped 17%. Bithumb scrambled to halt transactions after roughly 30 minutes, but not before investors—including people who had absolutely nothing to do with the giveaway—lost about $685,000. And here’s the real kicker: Bithumb only held around 50,000 bitcoins in its vault. So how exactly did they distribute 620,000? South Korean lawmakers are calling them “phantom coins,” which is a polite way of saying the emperor had no clothes. A law professor at Seoul National University called it a “catastrophic failure of internal controls.” That’s academic speak for “Nobody was watching the store.”Now imagine this scenario. You’re 65. Maybe 70. You recently retired, or you’ve been retired for a while, and you’re living on a fixed income. Someone at a seminar—a slick presenter with a nice PowerPoint—talked you into putting a chunk of your hard-earned savings into cryptocurrency. “It’s the future!” they said. “You’re going to miss out!” And then on some random Tuesday morning, you wake up to find your holdings have cratered 17% because an exchange on the other side of the world made a typo. You didn’t do anything wrong. You didn’t panic sell. You were just sitting there drinking your morning coffee, and your retirement money evaporated because some employee in Seoul confused Korean won with bitcoin.And what do you do about it? Nothing. You have no recourse. No FDIC insurance. No regulatory body stepping in to make you whole. No customer service number that actually connects you to a human being who can help. This isn’t a bank. It isn’t even a proper brokerage with compliance officers and auditors. It’s the digital Wild West, and you just got caught in the crossfire of someone else’s incompetence.I’ve had people come to me over the years, some nearly in tears, saying, “Paul, I need to build my money back. I lost so much.” And when we dig into it, the story is almost always the same: they weren’t investing. They were gambling. Chasing the hot tip, the next big thing, the promise of easy money from somebody who had no fiduciary obligation to act in their best interest. That’s not what we do at Truesdell Wealth. That’s not what any reputable fiduciary-based advisor does. We don’t chase. We don’t gamble. We plan.Now, before anyone accuses me of being a crypto dinosaur, let me be clear: I understand cryptocurrency. My eldest son was a bitcoin miner back when it was brand new—back when the people who made real money were early adopters who understood the technology and, more importantly, knew when to get out. It was a gamble with money that meant nothing to us: a computer, some electricity, a little time, and the curiosity to see what would happen. Those days are long, long gone. Today’s crypto market is a speculative circus masquerading as a legitimate asset class, and incidents like this Bithumb disaster are Exhibit A for the prosecution.What we practice at Truesdell Wealth is fiduciary-based investment and wealth management. We take the family office approach and facilitate running an individual’s or family’s household like a business—with discipline, accountability, transparency, and a plan. A plan that doesn’t include crossing your fingers and hoping some exchange in Asia doesn’t accidentally give away $40 billion before breakfast. If gambling is your business, that’s your business. It’s not ours.Tippecanoe and Tyler Too, I’m out of here.

The Deadly Poison of Nullification

The Deadly Poison of NullificationHow the Selective Application of Justice Is Destroying the Republic and Why the Reckoning Will Be SevereBy Paul Grant Truesdell, JD, AIF1What We Are Witnessing Is Nullification and It Will Not End Well: A Warning From HistoryThere is a principle in American jurisprudence that most citizens never learn about in school, and for good reason. It is called jury nullification, and it occurs when jurors refuse to convict a defendant not because the evidence is insufficient, but because they disagree with the law itself or believe the prosecution is unjust. It is not written into statute. It is not encouraged by judges. But it exists, and it has been used throughout American history for purposes both noble and shameful.What we are witnessing in Minneapolis, in Portland, in Los Angeles, and in courtrooms across this nation is something adjacent to this principle but far more corrosive. We are seeing the selective application of justice based on political alignment. We are seeing prosecutors who decline to charge rioters while throwing the book at protesters on the other side. We are seeing juries that appear to render verdicts based not on evidence but on tribal loyalty. And we are seeing a significant portion of the American public cheering this on, apparently unaware that they are sawing off the branch they are sitting on.Let me be direct about something. I am generally aligned with conservative principles. I supported President Trump. I believe in law and order, border security, limited government, and the rights enumerated in our Constitution. But what I am about to say is not partisan cheerleading. It is a warning, and it applies to everyone regardless of which cable news channel they prefer.When you normalize the weaponization of the justice system against your political opponents, you are not winning. You are establishing a precedent. And precedents, once established, do not care about your intentions. They simply exist, waiting to be used by whoever holds power next.2The Great Triumvirate and the Death of Serious Political DiscourseBefore we examine the constitutional issues at stake, we need to understand something about the quality of political discourse in America and how far we have fallen from what we once were.In the early nineteenth century, the United States Senate was home to three men whose debates on the floor of that chamber are still studied today as examples of the highest form of political argument. They were called the Great Triumvirate, sometimes the Immortal Trio: Daniel Webster of Massachusetts, Henry Clay of Kentucky, and John C. Calhoun of South Carolina. These men disagreed on almost everything. They were political rivals. They represented fundamentally different visions of what America should become. And yet they engaged each other with a level of intellectual rigor, rhetorical skill, and mutual respect that would be unrecognizable in today's political environment.Daniel Webster was the great defender of the Union and the Constitution. His reply to Robert Hayne in 1830, in which he declared "Liberty and Union, now and forever, one and inseparable," is considered one of the greatest speeches in American history. Henry Clay was the Great Compromiser, the man who brokered the Missouri Compromise of 1820 and the Compromise of 1850, repeatedly stepping into the breach when sectional tensions threatened to tear the nation apart. John C. Calhoun was the brilliant theorist of states' rights and the most articulate defender of Southern interests, a man whose intellectual contributions to American political thought continue to be studied even as his defense of slavery is rightly condemned.These were serious men having serious debates about serious issues. They read deeply. They argued carefully. They understood that their words would be scrutinized by posterity. They believed that ideas mattered and that the outcome of their debates would shape the future of the Republic.Compare that to what passes for political discourse today. We have replaced the Lincoln-Douglas debates with Twitter feuds. We have replaced careful constitutional argument with sound bites and gotcha moments. We have politicians who cannot articulate the basic principles of their own positions, let alone engage thoughtfully with the positions of their opponents. We have a political class that treats governance as performance art rather than the serious business of managing a republic.This matters because the issues we face today are no less consequential than the issues faced by the Great Triumvirate. The questions of federal power, states' rights, the limits of government authority, and the protection of minority interests are as urgent now as they were in 1830. But we are trying to answer those questions with a political class that would have been laughed out of any nineteenth century debating society.3John C. Calhoun: The Democrat Who Created Modern NullificationTo understand the danger of w

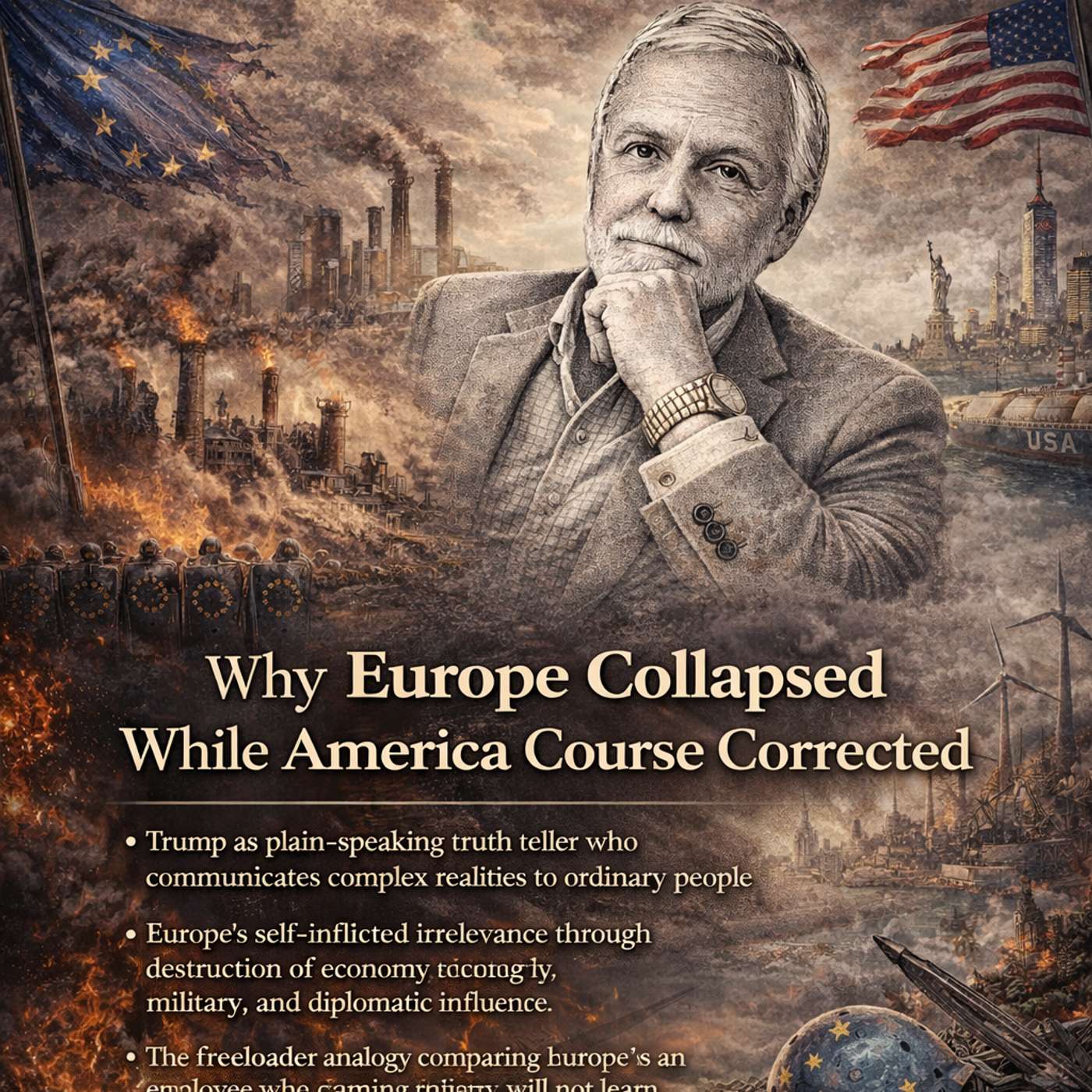

Freeloaders And Fantasies

Freeloaders And FantasiesWhy Europe Collapsed While America Course CorrectedTrump as plain-speaking truth teller who communicates complex realities to ordinary peopleEurope's self-inflicted irrelevance through destruction of economy, industry, military, and diplomatic influenceThe freeloader analogy comparing Europe to an employee who cannot perform, will not learn, but expects full compensationStatistical reality of Europe consuming sixty percent of world welfare spending while representing twelve percent of populationTrump's warning to Germany about Russian gas dependency and their dismissive laughter followed by the five thousand helmets debacleNet Zero as industrial suicide illustrated by Britain unable to produce virgin steelThe North Sea hypocrisy of Britain shutting down domestic gas production while importing gas from Norway drilled in the same watersGreen energy paradox where petroleum required to manufacture and maintain wind and solar often exceeds fossil fuels replacedNet Zero producing net zero growth over twenty years while energy prices climb and industry fleesDEI and Net Zero as potential Russian and Chinese strategy to degrade Western civilizationAmerica's divergence from Europe by never fully implementing destructive energy policies or making electricity unaffordableUniparty governance in Europe where both major parties delivered identical policies leaving voters no real choiceFundamental difference between European conservatism based on tradition versus American conservatism based on valuesEuropean inability to defend against cultural attacks on their history versus American pushback through electionsIraq and Afghanistan as failures of the Western intervention model but survivable errors if strength had been maintainedRules-based international order exposed as fiction and smokescreen by its own proponentsPath forward through abundant cheap domestic energy productionTax policy reform to encourage business and entrepreneurshipWelfare reform starting with no benefits for foreign nationalsCultural renewal and rejection of civilizational self-hatredRealignment as opportunity rather than crisis with conversation finally startedI’ve been watching the world wake up to something I’ve been saying for years, and frankly, it’s about time. President Trump has done what great communicators do. He’s taken complicated realities and distilled them into plain language that ordinary people understand. That’s his superpower. He speaks to the man and woman who actually pays the bills, raises the kids, and wonders why everything keeps getting more expensive while the people in charge keep telling them everything is fine.What we’re witnessing isn’t really about Trump at all. What we’re witnessing is the exposure of a fraud that’s been running for decades. Europe has made itself irrelevant. They’ve destroyed their own economies, gutted their industrial capacity, hollowed out their militaries, and squandered whatever diplomatic influence they once had. And now someone has finally said it out loud in a way that can’t be ignored.Think about it. Europe represents about twelve percent of the world’s population. They generate roughly a quarter of the world’s economic output. And they consume sixty percent of the world’s welfare spending. That’s not a civilization preparing for the future. That’s a civilization in hospice care, arguing about what color to paint the walls.The Americans, behind closed doors, call Europeans freeloaders. Are they wrong? I don’t think so. When you hire someone to do a job, and they can’t do it, won’t learn how to do it, but still expect the paycheck and the benefits, you fire them. In business, that’s called deadweight. In life, those are the neighbors who contribute nothing but always show up when there’s something to take. Eventually, you stop answering the door. That’s what Europe has become to the United States, and Trump is simply acknowledging reality.Now, there are exceptions. Poland, for instance. They’re less infected with the woke virus because they live next door to Russia. When your neighbor has a history of rolling tanks across your border, you tend to stay focused on things that actually matter. But overall, the European project is collapsing under the weight of its own delusions.Remember when Trump warned German leaders that their energy policies were making them dependent on Russian gas? They laughed in his face. Literally laughed at him. Then Russia invaded Ukraine, and suddenly Germany’s big contribution to the defense of a free nation was five thousand helmets. Not tanks. Not ammunition. Helmets. That tells you everything you need to know about what decades of fantasy-based policy produces when reality comes knocking.The whole Net Zero agenda deserves special attention because it perfectly illustrates the self-destructive madness that’s consumed the Western world. Britain can no longer produce virgin steel because of policies designed to save the planet. Meanwhile, they i

Greenland Is Not About Ice. It Is About America.

Greenland Is Not About Ice. It Is About America.Let me tell you something that most people do not want to hear. Greenland is not some frozen wasteland at the top of the world that we should ignore. Greenland is the key to North American security in the twenty-first century, and anyone who cannot see that is either not paying attention or does not want you to understand what is really happening on the global stage.The world got small. It happened faster than most people realize. When intercontinental ballistic missiles can reach any city on earth in thirty minutes, when satellites can photograph your backyard from space, when hypersonic weapons are being tested by our adversaries, the old rules about geography went out the window. Except they did not. Geography matters more than ever. It just matters differently now.Greenland is the largest island on the planet. Over eight hundred thirty thousand square miles. More than three times the size of Texas. And fewer people live there than in Kalamazoo, Michigan. In fact, the City of Ocala has approximately 20,000 more residents than Greenland. About fifty-seven thousand souls spread across a handful of coastal settlements, most of them Inuit descendants who have lived there for centuries because they are genetically and culturally adapted to conditions that would kill the rest of us in a week.Why so empty? The obvious answer is that eighty percent of the island is covered in ice up to two miles thick. The growing season is measured in weeks, not months. The soil, where it exists at all, is ancient bedrock scraped clean by glaciers. Farming is essentially impossible except for a few sheep operations at the southern tip. There are no roads connecting towns. No rail. You get around by boat in summer, by snowmobile and dog sled in winter, and by helicopter or small plane year-round if you can afford it and the weather cooperates. Which it often does not.The Vikings tried to settle Greenland a thousand years ago during a warm period when the southern coast actually looked somewhat green. Erik the Red named it Greenland as a marketing pitch to convince Icelanders to join him. They showed up, tried to farm, watched the climate turn brutal, and disappeared within a few centuries. And by the way, the Greenland climate switcheroo, was not due to Erik the Red or anything related to the endeavors of Vikings, not matter what Al Gore has to say. And so, the Inuits, the indigenous Arctic and Subarctic residents stayed because they knew how to hunt seals through breathing holes in the ice, how to build kayaks to navigate between ice floes, how to make clothing from caribou hide that actually kept the cold out. And so, the Norse, well they were farmers in a land where farming does not work. They lost.But here is what matters now. Greenland sits between North America and Europe at the top of the North Atlantic. It is positioned directly in the path of the shortest flight routes between the continental United States and Russia. During the Cold War, we understood this perfectly. We built Thule Air Base in northwest Greenland in 1951. Today it is called Pituffik Space Base, (pronounced bee-doo-FEEK) and understanding what happens there tells you everything you need to know about why Greenland matters.Pituffik Space Base is not some relic from the Cold War collecting dust. It is one of the most strategically critical military installations in the entire northern hemisphere. The base hosts the northernmost deep-water port in the United States military system. It operates sophisticated ballistic missile early warning radar systems that would detect any intercontinental ballistic missile launch from Russia or anywhere else coming over the polar route toward North America. That radar gives us precious minutes of warning time. In a nuclear exchange, minutes are the difference between a coordinated response and chaos.And before we continue, always remember and never forget, Putin, the dictator of Russia, has regularly threatened to use nuclear weapons against Ukraine and the United States. Now, back to Pituffik, which does more than watch for missiles. It is a critical node in our space surveillance network, tracking satellites and debris in orbit, monitoring what our adversaries are doing in space, and supporting military space operations that most Americans never hear, read, or think about. The base also serves as a staging point for Arctic operations, scientific research, and search and rescue missions across the High North. When we talk about controlling the Arctic approaches to North America, Pituffik is where that control lives.The name change from Thule to Pituffik happened in 2023, reflecting the local Greenlandic name for the area. But do not let the rebranding fool you. The mission has only grown more important as great power competition has intensified. Russia has been rebuilding Soviet-era Arctic bases and expanding its military footprint across the northern latitudes. China, des

Follow the Money

Follow the MoneyWhere Campaign Cash Really Comes From, Who Benefits from Climate Policy, and Why Christians Stay Silent About ChinaBy Paul TruesdellBefore I begin…Why I Do Long-Form: A Four-Minute ExplanationYou know what’s funny? Every marketing guru out there tells me I’m doing it all wrong. “Paul, you need to be on TikTok. You need fifteen-second clips. You need memes. You need to hook ‘em in three seconds or they’re gone.”And I say: Good. Let ’em go.Here’s the thing about those short-form videos—the TikToks, the Reels, the quick-hit content. They’re designed for instant gratification. Quick dopamine hits. Scroll, laugh, scroll, react, scroll. The average user burns through two hundred videos in thirty minutes. Half of viewers bail within three seconds if they’re not immediately entertained.That’s not a bug in the system. That’s the feature.And it works beautifully—for a certain kind of audience. The “entertain me” crowd. The “what have you done for me lately” folks. The meme-based, short-attention-span consumer who wants answers without questions and solutions without understanding.That’s not my type of prospect or client.Let me tell you who I’m looking for. I work with people who are fifty-five and older, often within five years of retirement or already there. These are folks who’ve spent decades building something—careers, families, wealth, wisdom. They didn’t get there by scrolling through thirty-second clips. They got there by thinking things through. By asking hard questions. By sitting with complexity.Long-form podcasting is my filter.When I do a two-hour episode, I’m not trying to compete with TikTok. I’m doing the opposite. I’m saying: If you’ve got the patience to listen to this, if you’re intellectually curious enough to follow a conversation that unfolds over time, if you actually enjoy thinking deeply about money, about retirement, about how to spend the next chapter of your life—then you might be my kind of person.The research backs this up. Long-form podcast listeners are different. They score high on what psychologists call “openness to experience”—intellectual curiosity, comfort with complex ideas, appreciation for nuance. They have what’s called a “high need for cognition”—they genuinely enjoy thinking. They’re not stressed out by three-hour conversations; they’re energized by them.These are the people who say, “I really want to dig into this and understand it fully.” Not “just give me the bullet points.”And here’s the beautiful irony: the completion rates on long-form podcasts are extraordinary. Seventy to ninety percent of listeners finish episodes. Even those marathon three-hour shows? Dedicated listeners stick around because the content rewards their attention.Compare that to short-form, where you lose half your audience in three seconds.Now, some would call that a failure. I call it efficiency.When someone finds The Paul Truesdell Podcast and actually listens—really listens—to an episode or two, they’re self-selecting. They’re telling me something about who they are. They’re patient. They’re thoughtful. They want depth over speed. They’re not looking for entertainment; they’re looking for insight.That’s exactly the kind of person I want to work with in my practice. Because when we sit down to talk about retirement planning, about protecting what they’ve built, about making decisions that will affect the rest of their lives—I need someone who can handle a real conversation. Not a soundbite.The “entertain me” client? They’ll fire you the moment the market dips. The “what have you done for me lately” client? They’re always chasing the next shiny thing. But the intellectually engaged client—the one who found you through a long-form podcast and thought, “This guy thinks like I do”—that’s a relationship built on substance.So no, I’m not going to dance on TikTok. I’m not going to compress forty years of experience into fifteen seconds. I’m going to keep doing what I do: long conversations, deep dives, real thinking.And the right people will find their way here.That’s the nature of the beast.Now, the rest of the story. Let me tell you something I learned a long time ago, back when I was carrying a badge and working cases that most folks never hear about. If you want to understand why something that makes no sense keeps happening, you have to follow the money. It is that simple. The money trail never lies, even when everybody around it does.Now, when you start looking at where the big institutional money managers are putting their clients' assets, you discover something interesting. All that patriotic advertising, all those commercials with American flags waving and military families featured prominently, well, it starts to look a lot like window dressing. Marketing. Because when you dig into the actual portfolios, you find massive investments flowing into companies that operate primarily in countries that are not exactly our friends. American patriotism, for a lot of these outfits, is noth

Think About It How China Bullies Its Rivals and What That Should Teach Us About Recognizing the Same Behavior Here

Rough Draft / Script When the power was cut to the Stone Creek Republican Club Christmas party in 2025, think about it. When power was cut to the George Bush presidential campaign visit to the Villages in 2004 by a disgruntled Democratic Party operative working for Sumter Electric, think about it. When Covid lockdowns took place and you were told to trust the science without being allowed to question it, think about it. When political leaders at the national or local level behave like children and tell you to shut up and go away, think about it. When school textbooks reflect revisionist history designed to support DEI principles and present fiction as fact, think about it. When form over substance continues to rule the roost, think about it. When people who claim to be Republicans play games of continual posturing that would be better suited to the Democratic Party where that kind of nonsense is tolerated, think about it. And when major defense contractors reap ridiculous profits and pay outrageous salaries to chief executive officers who are nothing more than employees gaming the system at the cost of the American taxpayer and our national defense, think about it. The tactics are not that different. The playbook looks familiar. Connect the dots.RingerUnderstanding China’s Pressure Campaign and Why It Matters to Your Family’s FutureLet me tell you something that needs saying plainly, because the evening news is not going to spell it out for you. We are in a Cold War with China. Not the kind where everybody acknowledges it and acts accordingly, but the kind where one side pretends it is not happening while the other side presses every advantage. And if you think this is somebody else’s problem because you are seventy-two years old and planning your next cruise, I need you to think again. Think about your grandchildren. Think about the world they are going to inherit if we keep sleepwalking through this.What happened recently between China and Japan is not an isolated diplomatic spat. It is a textbook demonstration of how Beijing operates when any nation dares to speak truthfully about Chinese aggression. Japanese Prime Minister Sanae Takaichi made a simple observation in November. She said Japan could get drawn into conflict if China tried to seize Taiwan by force. That is not an inflammatory statement. That is a geographical and military reality. Japan sits right there. But Beijing treats honesty the way a bully treats a smaller kid who finally speaks up. They came after her with everything they had.And when I say everything, I mean information warfare, economic coercion, legal manipulation, cultural punishment, and military intimidation. These are not new tactics. They have been refined over years of squeezing Taiwan. Now they are being deployed against a major ally of the United States. If you think they will not eventually be aimed at us directly, you have not been paying attention.CommercialLet us talk about the information warfare piece first because it reveals something important about how Beijing thinks. They used artificial intelligence to generate fake content attacking Takaichi. Fake text messages. Fake photos showing jewelry she supposedly received as bribes from Taiwan. Character assassination on an industrial scale. They did the same thing to Taiwan’s leaders before the 2024 election. Deep fakes. Fake opinion polls. Anything to undermine public confidence in elected officials who refuse to bow to Beijing.Now here is where the sarcasm becomes unavoidable. When confronted with evidence of these campaigns, China’s Foreign Ministry said with a straight face that China is a victim of disinformation. That takes a particular kind of audacity. It is like the schoolyard bully punching you in the nose and then telling the teacher he is being picked on. And some folks in Washington seem perfectly happy to believe him.The economic coercion is equally instructive. China is now the world’s second largest economy, and they use trade like a weapon. They banned Norwegian salmon after a Chinese dissident won the Nobel Peace Prize. They banned Lithuanian goods after Lithuania allowed Taiwan to open a representative office. And within days of Takaichi’s honest comment, they halted Japanese seafood imports and restricted rare earth exports to Japan. They also warned Chinese tourists not to visit Japan, citing earthquake threats. The earthquake that poses the real threat is the one Beijing creates when any nation tells the truth about their intentions.Remember when they banned Taiwanese pineapples in 2021? Same playbook. Different target. The message is clear. Cross us and we will hurt you economically. And the message to everyone else is equally clear. Keep quiet or you are next.Then there is what Beijing calls lawfare. Using legal claims and treaties as weapons. They cite World War Two declarations to justify their claim to Taiwan. They use a 1971 UN resolution to argue that the international community already rec

The Pop Bomb Bust

Rough NotesPaul Truesdell dot ComWhen a nation loses its people, it loses everything else shortly thereafter. This is not philosophy or political commentary. This is arithmetic. An economy requires workers to produce, consumers to purchase, and taxpayers to fund the infrastructure that makes commerce possible. Remove the people, and the entire system unravels like a cheap sweater.History offers no shortage of examples, and they are worth examining because the patterns repeat with uncomfortable regularity.Start with the American West. The ghost towns scattered across Nevada, California, Colorado, and Arizona tell the same story over and over again. Rhyolite, Nevada, exploded into existence in 1904 when gold was discovered nearby. Within three years, the population swelled to somewhere between five and ten thousand people. They built a train station, a stock exchange, an opera house, and a three-story bank made of concrete. By 1920, the population was fourteen. The gold played out, the miners left, and everything they built became a monument to impermanence. Bodie, California, followed a similar arc. At its peak in 1879, nearly ten thousand people lived there, making it one of the largest towns in California. Today it sits frozen in time, a state historic park where tourists wander through buildings that housed saloons, churches, and general stores. The people vanished because the economic engine that brought them there sputtered and died. Centralia, Pennsylvania, offers a more recent and peculiar example. A coal mine fire started in 1962 and never stopped burning. The underground fire made the town uninhabitable, and the government relocated nearly everyone. A town that once had over a thousand residents now has fewer than ten. The economic foundation literally went up in smoke, and so did the community.Florida has its own collection of forgotten places. Marion County saw several small commercial centers rise and fall before modern development patterns took hold. Ocklawaha was once a busy steamboat landing on the Ocklawaha River, a genuine hub of commerce when waterways were the highways of their day. When the railroads came and the steamboats became obsolete, Ocklawaha faded into obscurity. Fort King, the original reason Ocala exists at all, was a military outpost that sparked settlement in the region. When the Seminole Wars ended, the fort closed, and the original settlement patterns shifted. Dunnellon provides an interesting case study in survival. The town boomed when phosphate was discovered in the 1880s, and for a brief moment it was one of the wealthiest small towns in America per capita. When the phosphate played out, Dunnellon could have become another ghost town. Instead, it stabilized at a modest size and maintained its city character. Today they celebrate Boomtown Days as a nod to that history. The town sits near the Withlacoochee and Rainbow Rivers, and while the surrounding area has grown considerably, Dunnellon itself never recaptured that original boom. It found equilibrium at a smaller scale, which is more than most boom towns manage.The ancient world offers examples on a grander scale. The Aztec Empire collapsed not primarily because of Spanish military superiority but because European diseases decimated a population with no immunity. Smallpox, measles, and typhus killed millions. Some estimates suggest that ninety percent of the indigenous population of Mexico died within a century of contact. You cannot maintain an empire, collect taxes, field armies, or sustain an economy when ninety percent of your people are dead. The Spanish did not so much conquer the Aztecs as inherit the ruins of a civilization that disease had already destroyed.The Roman Empire took centuries to decline, but population loss played a significant role. The Antonine Plague in the second century killed millions. The Plague of Cyprian in the third century killed millions more. Armies could not be recruited, farms could not be worked, and tax revenues collapsed. Rome did not fall in a single dramatic moment. It bled out slowly as its population dwindled and its economic capacity declined in parallel.The Black Death that swept through Europe in the fourteenth century killed somewhere between thirty and sixty percent of the entire population. The economic consequences were staggering. Labor became so scarce that the feudal system began to collapse. Peasants who survived could demand higher wages because there simply were not enough workers to go around. Entire villages disappeared. Trade routes that had functioned for centuries were disrupted. The economic map of Europe was redrawn by a bacterium.The United States experienced its own population shock with the influenza pandemic of 1918, which arrived on the heels of World War One. Estimates suggest somewhere between fifty and one hundred million people died worldwide, with about 675,000 deaths in America. The pandemic killed disproportionately among young, working-age adu

Casual Cocktail Conversations and Client Coffee Quarterly

Casual Cocktail Conversations and Client Coffee Quarterly at The Truesdell CompaniesWednesday, December 31, 2025 – Episode 526 Somewhere along the way, the financial services industry decided that the best way to talk to people about their money was to put them in a conference room with stale coffee, a PowerPoint presentation, and a sales pitch dressed up as education. You sit there for an hour, maybe two, nodding along while someone reads bullet points off a screen and wonders why you are not more excited about their proprietary mutual fund.Well, that is not how we do things at Truesdell Wealth.Starting in the first quarter of 2026, we are hosting a series of Casual Cocktail Conversations at the Stonewater Club in Stone Creek. These are not seminars. They are not sales presentations. TheyCasual Cocktail Conversations and Client Coffee Quarterly are exactly what the name suggests, conversations. You show up, grab a drink, sit down with people who are in the same chapter of life you are, and we talk about the things that actually matter when you are fifty-five or older and thinking seriously about retirement.The format is simple. I pick a topic that deserves more than a thirty-second explanation, and we dig into it. Not with jargon. Not with complicated charts designed to make you feel stupid so you will hand over your money. Just plain talk about real issues.On January 11th, we start with Buckets of Income with Clarity. This is the straightforward approach to retirement income that separates your fixed money from your flexible money. You will know exactly what is safe, what is moderate, what is growing, and what you can actually spend. No guessing. No hoping. No waking up at two in the morning wondering if the market just ate your grocery budget.January 25th is Hidden Investment Costs, Fees, and Expenses in Plain View. Here is a number for you: ninety-five percent of investors have no idea what they are actually paying. The financial industry has gotten remarkably good at burying costs inside layers of fees, expense ratios, and trading costs that never show up on your statement. They do not hide these fees because they are proud of them. We are going to pull back the curtain and show you where the money goes. Awareness is not optional when your retirement depends on it.February 8th covers Essential Florida Estate Documents and Much More. If you moved to Florida thinking a will from Ohio was good enough, you need to be in this room. We are talking about the must-have documents, the second marriage complications, the blended family landmines, and the probate surprises that catch retirees off guard every single day. This is not the glamorous side of planning, but it is the side that keeps your family out of court and your wishes intact.February 22nd is The IRA Tax Bomb, Social Security Cliff, and Cost of War. That IRA you have been contributing to for thirty years? It is not your money. It is a delayed tax bill with your name on it. Social Security is under strain, and unless you have been living under a rock, you have noticed that global conflict tends to change economic assumptions in ways nobody predicts. We are going to talk about what all of this means for your income planning right now, not in some theoretical future.March 8th brings The Truesdell Retirement Meltdown Calculator. I built this tool thirty-five years ago and have been updating it ever since. It shows your income, your spending, your risk, and your longevity under real-world conditions. Not best-case fantasy scenarios. Real conditions. I will demonstrate it live, and every client gets unlimited access to use it themselves.Then on March 22nd, we wrap up the quarter with The Big Five Truesdell Investment Portfolios and More. This is how we build durable, disciplined portfolios, how allocations work, and how we manage risk in a world that seems determined to surprise us. We will cover blended equal weight indexing with fractional shares, and if that sounds confusing, that is precisely why you need to attend.Now, for our existing clients and their invited guests, we have something different. On Wednesday, March 11th, we are holding the Client Quarterly, a private briefing over coffee where I walk through major economic, business, and investment developments. This is not a pep rally. This is a serious look at what is happening, using both quantitative and qualitative analysis and a few intelligence sources that do not show up in the morning headlines. I will explain why forecasting is disciplined mathematics while prediction is just guesswork with confidence, and how we incorporate the Rumsfeld framework of knowns, known unknowns, and unknown unknowns into how we think about risks, realities, and opportunities.If you are a client, you are invited. If you have friends or family who ought to hear this, bring them along.These conversations are for people who want straight answers, not sales pitches. If that sounds like you, we will see you at Stonew

Military Procurement - Navy - 11 of 17

The Variable Annuity Money Pit

The Variable Annuity Money PitTuesday, December 30, 2025 - Episode 525Now let's talk about variable annuities, which might be the most cleverly disguised fee machine the financial services industry ever invented. And I say that with the kind of admiration you'd give a con artist who manages to pick your pocket while shaking your hand.Here's how they work, and pay attention because the industry counts on you not understanding this. When you buy a variable annuity, your money goes into what they call separate accounts. Not mutual funds. Separate accounts. Why the fancy terminology? Because the law requires it. Insurance products can't technically hold mutual funds directly, so they create these separate accounts that are, for all practical purposes, mirror images of mutual funds. Same stocks. Same bonds. Same management. Same everything. Except the price tag. Think of it this way: you're buying a name-brand product repackaged in a fancier box, and someone's charging you a premium for the privilege of the new label.The separate accounts inside your variable annuity hold the exact same investments you could buy in a regular mutual fund, but now you're paying extra layers of fees that would make a toll road operator blush.Let's walk through the damage. First, there's the mortality and expense charge, which sounds like something from an undertaker's invoice. This typically runs about 1.4 percent annually. That's the insurance company's cut for providing the annuity wrapper and taking on some actuarial risk. Fair enough, you might think. Except we're just getting started.Next come the riders. Income riders guarantee you a certain payout down the road. Death benefit riders promise your heirs won't lose money if you die while the market is down. These sound wonderful in the sales presentation, and they're not free. Each rider might cost you another half percent to one percent per year. Sometimes more. Stack a couple of these on top of your mortality charge, and suddenly you're looking at total annual expenses of three and a half to four percent.Let me put that in plain English. If your variable annuity earns seven percent in a given year, and you're paying four percent in fees, you keep three percent. The insurance company keeps four. You did all the investing. You took all the risk. They took more than half the return. If that arrangement sounds fair to you, I've got a bridge in Brooklyn I'd like to discuss.But wait, as they say in those late-night commercials, there's more. Many variable annuities require you to keep a certain percentage of your money in bond funds. The sales pitch calls this risk management or asset allocation. Here's what it really means: when interest rates are low and bond returns are anemic, you're stuck in investments returning maybe four or five percent while paying three and a half percent in fees. Your net return might be one percent. In a good year. Meanwhile, inflation is eating your purchasing power for breakfast, and the insurance company is still collecting their cut like clockwork.Consider this example. You put two hundred thousand dollars into a variable annuity. Over twenty years, assuming average market returns of eight percent but total fees of three and a half percent, you'd net about four and a half percent annually. Your account might grow to roughly four hundred eighty thousand dollars. Sounds decent until you realize that the same two hundred thousand in a low-cost index fund charging a quarter of one percent would have grown to approximately six hundred eighty thousand dollars. That's two hundred thousand dollars that evaporated into fee structures and rider charges. Two hundred thousand dollars you'll never see because someone convinced you that complexity equals sophistication.Here's another way to look at it. If you're sixty years old and you live to ninety, those annual fees compound into a small fortune you're handing to the insurance company instead of your grandchildren. Over thirty years of retirement, a four percent annual fee drag on a five hundred thousand dollar portfolio amounts to hundreds of thousands of dollars in lost wealth. Not lost to bad investments. Lost to fees.Variable annuities aren't inherently evil. For a small slice of the population with very specific needs, they might make sense. But for most folks, they're an expensive solution to a problem that could be solved more simply and cheaply. The question you should always ask is this: who benefits most from this complexity? If the answer isn't you, maybe it's time for a different approach.

Military Procurement - Navy - 10 of 17

Military Procurement - Navy - 09 of 17

Military Procurement - Navy - 08 of 17

Military Procurement - Navy - 07 of 17

Military Procurement - Navy - 06 of 17

Military Procurement - Navy - 05 of 17

Military Procurement - Navy - 04 of 17

Military Procurement - Navy - 03 of 17

Military Procurement - Navy - 02 of 17

Military Procurement - Navy - 01 of 17

The Cost Blindness Problem

The Cost Blindness ProblemLet me tell you something that might sting a little, but sometimes the truth does that. After thousands of conversations over the years, I can tell you with near certainty that about half the people I sit down with simply do not want to know what they are paying. Not cannot know. Will not know. There is a difference, and it matters.I call it willful cost blindness, and it is one of the most expensive conditions you will never find in a medical textbook. These folks have spent decades building wealth, making sharp decisions, negotiating deals, and running households or businesses with precision. But when it comes to the fees their financial advisor or firm charges, they suddenly develop a remarkable ability to look the other way.Here is the uncomfortable part. When you work with someone for years, you build a relationship. You know their kids' names. You have been to their office Christmas party. They sent flowers when your mother passed. And that is exactly how the game is designed to work. Because once you like someone, once you trust them, it becomes almost impossible to look them in the eye and say, "I appreciate the relationship, but I am not paying these kinds of fees anymore."But there comes a point, and I have seen it happen again and again, when people just snap. Like that fellow in the movie Network who threw open the window and shouted that he was mad as hell and was not going to take it anymore. Something clicks. The loyalty finally costs more than the comfort is worth.Let me give you three examples from real folks I have worked with. Names changed, of course, but the stories are true enough.First, a married couple in their early sixties. Retired teachers, both of them. Good pensions, modest lifestyle, about four hundred thousand saved. They had been with the same broker for eighteen years. Nice guy. Sent birthday cards. The problem was they were paying one and a quarter percent annually on assets under management plus the hidden fees inside the mutual funds he recommended. When we sat down and ran the numbers, they discovered they had paid over seventy thousand dollars in fees over the past decade. For what? A portfolio that underperformed a basic index fund. The wife actually cried. Not from sadness, but from frustration. She kept saying, "We trusted him." They did. And that trust cost them a small car every year.Second, a widow in her mid-seventies. Her husband handled everything before he passed. She inherited a relationship with an advisor she barely knew and a portfolio stuffed with products that paid the advisor handsomely whether the market went up or down. When I asked her what she was paying, she had no idea. None. When we pulled the statements apart, we found she was losing nearly fourteen thousand dollars a year in fees on a seven hundred thousand dollar account. She had been a widow for six years. Do the math. She looked at me and said, "My husband would have fired this man years ago." She was right. He would have.Third, a retired business owner, seventy-one years old, sold his company for just under two million dollars. Sharp as a tack. Built something from nothing. But when it came to his investments, he handed the reins to a big-name firm and assumed the brand meant quality. It did not. He was paying advisory fees, platform fees, trading fees, and expense ratios that together added up to nearly two percent annually. On two million dollars, that is forty thousand dollars a year walking out the door. When I showed him, he got quiet. Then he said something I will never forget. "I would have fired any employee who wasted money like that."The point is simple. Loyalty is a fine quality. But blind loyalty to someone who is bleeding your retirement dry is not loyalty at all. It is denial dressed up in good manners. At some point, you have to look at the numbers, set aside the relationship, and ask yourself a hard question: Am I paying for service, or am I paying for comfort?

The Bundled Financial Product Problem and How to Solve It