SF Compute: Commoditizing Compute to solve the GPU Bubble forever

Latent Space: The AI Engineer Podcast

Audio is streamed directly from the publisher (api.substack.com) as published in their RSS feed. Play Podcasts does not host this file. Rights-holders can request removal through the copyright & takedown page.

Show Notes

We are calling for the world’s best AI Engineer talks for AI Architects, /r/localLlama, Model Context Protocol (MCP), GraphRAG, AI in Action, Evals, Agent Reliability, Reasoning and RL, Retrieval/Search/RecSys , Security, Infrastructure, Generative Media, AI Design & Novel AI UX, AI Product Management, Autonomy, Robotics, and Embodied Agents, Computer-Using Agents (CUA), SWE Agents, Vibe Coding, Voice, Sales/Support Agents at AIEWF 2025! Fill out the 2025 State of AI Eng survey for $250 in Amazon cards and see you from Jun 3-5 in SF!

Coreweave’s now-successful IPO has led to a lot of questions about the GPU Neocloud market, which Dylan Patel has written extensively about on SemiAnalysis. Understanding markets requires an interesting mix of technical and financial expertise, so this will be a different kind of episode than our usual LS domain.

When we first published $2 H100s: How the GPU Rental Bubble Burst, we got 2 kinds of reactions on Hacker News:

* “Ah, now the AI bubble is imploding!”

* “Duh, this is how it works in every GPU cycle, are you new here?”

We don’t think either reaction is quite right. Specifically, it is not normal for the prices of one of the world’s most important resources right now to swing from $1 to $8 per hour based on drastically inelastic demand AND supply curves - from 3 year lock-in contracts to stupendously competitive over-ordering dynamics for NVIDIA allocations — especially with increasing baseline compute needed for even the simplest academic ML research and for new AI startups getting off the ground.

We’re fortunate today to have Evan Conrad, CEO of SFCompute, one of the most exciting GPU marketplace startups, talk us through his theory of the economics of GPU markets, and why he thinks CoreWeave and Modal are well positioned, but Digital Ocean and Together are not.

However, more broadly, the entire point of SFC is creating liquidity between GPU owners and consumers and making it broadly tradable, even programmable:

As we explore, these are the primitives that you can then use to create your own, high quality, custom GPU availability for your time and money budget, similar to how Amazon Spot Instances automated the selective buying of unused compute.

The ultimate end state of where all this is going is GPU that trade like other perishable, staple commodities of the world - oil, soybeans, milk. Because the contracts and markets are so well established, the price swings also are not nearly as drastic, and people can also start hedging and managing the risk of one of the biggest costs of their business, just like we have risk-managed commodities risks of all other sorts for centuries. As a former derivatives trader, you can bet that swyx doubleclicked on that…

Show Notes

Full Video Pod

Timestamps

* [00:00:05] Introductions

* [00:00:12] Introduction of guest Evan Conrad from SF Compute

* [00:00:12] CoreWeave Business Model Discussion

* [00:05:37] CoreWeave as a Real Estate Business

* [00:08:59] Interest Rate Risk and GPU Market Strategy Framework

* [00:16:33] Why Together and DigitalOcean will lose money on their clusters

* [00:20:37] SF Compute's AI Lab Origins

* [00:25:49] Utilization Rates and Benefits of SF Compute Market Model

* [00:30:00] H100 GPU Glut, Supply Chain Issues, and Future Demand Forecast

* [00:34:00] P2P GPU networks

* [00:36:50] Customer stories

* [00:38:23] VC-Provided GPU Clusters and Credit Risk Arbitrage

* [00:41:58] Market Pricing Dynamics and Preemptible GPU Pricing Model

* [00:48:00] Future Plans for Financialization?

* [00:52:59] Cluster auditing and quality control

* [00:58:00] Futures Contracts for GPUs

* [01:01:20] Branding and Aesthetic Choices Behind SF Compute

* [01:06:30] Lessons from Previous Startups

* [01:09:07] Hiring at SF Compute

Transcript

Alessio [00:00:05]: Hey everyone, welcome to the Latent Space podcast. This is Alessio, partner and CTO at Decibel, and I'm joined by my co-host Swyx, founder of Smol AI.

Swyx [00:00:12]: Hey, and today we're so excited to be finally in the studio with Evan Conrad from SF Compute. Welcome. I've been fortunate enough to be your friend before you were famous, and also we've hung out at various social things. So it's really cool to see that SF Compute is coming into its own thing, and it's a significant presence, at least in the San Francisco community, which of course, it's in the name, so you couldn't help but be.

Evan: Indeed, indeed. I think we have a long way to go, but yeah, thanks.

Swyx: Of course, yeah. One way I was thinking about kicking on this conversation is we will likely release this right after CoreWeave IPO. And I was watching, I was looking, doing some research on you. You did a talk at The Curve. I think I may have been viewer number 70. It was a great talk. More people should go see it, Evan Conrad at The Curve. But we have like three orders of magnitude more people. And I just wanted to, to highlight, like, what is your analysis of what CoreWeave did that went so right for them?

Evan: Sell locked-in long-term contracts and don't really do much short-term at all. I think like a lot of people had this assumption that GPUs would work a lot like CPUs and the like standard business model of any sort of CPU cloud is you buy commodity hardware, then you lay on services that are mostly software, and that gives you high margins and pretty much all your value comes from those services. Not really the underlying. Compute in any capacity and because it's commodity hardware and it's not actually that expensive, most of that can be sort of on-demand compute. And while you do want locked-in contracts for folks, it's mostly just a sort of de-risk situation. It helps you plan revenue because you don't know if people are going to scale up or down. But fundamentally, people are like buying hourly and that's how your business is structured and you make 50 percent margins or higher. This like doesn't really work in GPUs. And the reason why it doesn't work is because you end up with like super price sensitive customers. And that isn't because necessarily it's just way more expensive, though that's totally the case. So in a CPU cloud, you might have like, you know, let's say if you had a million dollars of hardware in GPUs, you have a billion dollars of hardware. And so your customers are buying at much higher volumes than you otherwise expect. And it's also smaller customers who are buying at higher amounts of volume. So relative to what they're spending in general. But in GPUs in particular, your customer cares about the scaling law. So if you take like Gusto, for example, or Rippling or an HR service like this, when they're buying from an AWS or a GCP, they're buying CPUs and they're running web servers, those web servers, they kind of buy up to the capacity that they need, they buy enough, like CPUs, and then they don't buy any more, like, they don't buy any more at all. Yeah, you have a chart that goes like this and then flat. Correct. And it's like a complete flat. It's not even like an incremental tiny amount. It's not like you could just like turn on some more nodes. Yeah. And then suddenly, you know, they would make an incremental amount of money more, like Gusto isn't going to make like, you know, 5% more money, they're gonna make zero, like literally zero money from every incremental GPU or CPU after a certain point. This is not the case for anyone who is training models. And it's not the case for anyone who's doing test time inference or like inference that has scales at test time. Because like you, your scaling laws mean that you may have some diminishing returns, but there's always returns. Adding GPUs always means your model does actually get. And that actually does translate into revenue for you. And then for test time inference, you actually can just like run the inference longer and get a better performance. Or maybe you can run more customers faster and then charge for that. It actually does translate into revenue. Every incremental GPU translates to revenue. And what that means from the customer's perspective is you've got like a flat budget and you're trying to max the amount of GPUs you have for that budget. And it's very distinctly different than like where Augusto or Rippling might think, where they think, oh, we need this amount of CPUs. How do we, you know, reduce that? How do we reduce our amount of money that we're spending on this to get the same amount of CPUs? What that translates to is customers who are spending in really high volume, but also customers who are super price sensitive, who don't give a s**t. Can I swear on this? Can I swear? Yeah. Who don't give a s**t at all about your software. Because a 10% difference in a billion dollars of hardware is like $100 million of value for you. So if you have a 10% margin increase because you have great software, on your billion, the customers are that price sensitive. They will immediately switch off if they can. Because why wouldn't you? You would just take that $100 million. You'd spend $50 million on hiring a software engineering team to replicate anything that you possibly did. So that means that the best way to make money in GPUs was to do basically exactly what CoreWeave did, which is go out and sign only long-term contracts, pretty much ignore the bottom end of the market completely, and then maximize your long-term contracts. With customers who don't have credit risk, who won't sue you, or are unlikely to sue you for frivolous reasons. And then because they don't have credit risk and they won't sue you for frivolous reasons, you can go back to your lender and you can say, look, this is a really low risk situation for us to do. You should give me prime, prime interest rate. You should give me the lowest cost of capital you possibly can. And when you do that, you just make tons of money. The problem that I think lots of people are going to talk about with CoreWeave is it doesn't really look like a cloud platform. It doesn't really look like a cloud provider financially. It also doesn't really look like a software company financially.

Swyx [00:05:37]: It's a bank.

Evan [00:05:38]: It's a bank. It's a real estate company. And it's very hard to not be that. The problem of that that people have tricked themselves into is thinking that CoreWeave is a bad business. I don't think CoreWeave is explicitly a bad business. There's a bunch of people, there's kind of like two versions of the CoreWeave take at the moment. There's, oh my God, CoreWeave, amazing. CoreWeave is this great new cloud provider competitive with the hyperscalers. And to some extent, this is true from a structural perspective. Like, they are indeed a real sort of thing against the cloud providers in this particular category. And the other take is, oh my gosh, CoreWeave is this horrible business and so on and blah, blah, blah. And I think it's just like a set of perception or perspective. If you think CoreWeave's business is supposed to look like the traditional cloud providers, you're going to be really upset to learn that GPUs don't look like that at all. And in fact, for the hyperscalers, it doesn't look like this either. My intuition is that the hyperscalers are probably going to lose a lot of money, and they know they're going to lose a lot of money on reselling NVIDIA GPUs, at least. Hyperscalers, but I want to, Microsoft, AWS, Google. Correct, yeah. The Microsoft, AWS, and Google. Does Google resell? I mean, Google has TPUs. Google has TPUs, but I think you can also get H100s and so on. But there are like two ways they can make money. One is by selling to small customers who aren't actually buying in any serious volume. They're testing around, they're playing around. And if they get big, they're immediately going to do one of two things. They're going to ask you for a discount. Because they're not going to pay your crazy sort of margin that you have locked into your business. Because for CPUs, you need that. They're going to pay your massive per hour price. And so they want you to sign a long-term contract. And so that's your other way that you can make money, is you can basically do exactly what CoreWeave does, which is have them pay as much as possible upfront and lock in the contract for a long time. Or you can have small customers. But the problem is that for a hyperscaler, the GPUs to... To sell on the low margins relative to what your other business, your CPUs are, is a worse business than what you are currently doing. Because you could have spent the same money on those GPUs. And you could have trained model and you could have made a model on top of it and then turn that into a product and had high margins from your product. Or you could have taken that same money and you could have competed with NVIDIA. And you could have cut into their margin instead. But just simply reselling NVIDIA GPUs doesn't work like your CPU business. Where you're able to capture high margins from big customers and so on. And then they never leave you because your customers aren't actually price sensitive. And so they won't switch off if your prices are a little higher. You actually had a really nice chart, again, on that talk of this two by two. Sure. Of like where you want to be. And you also had some hot takes on who's making money and who isn't.

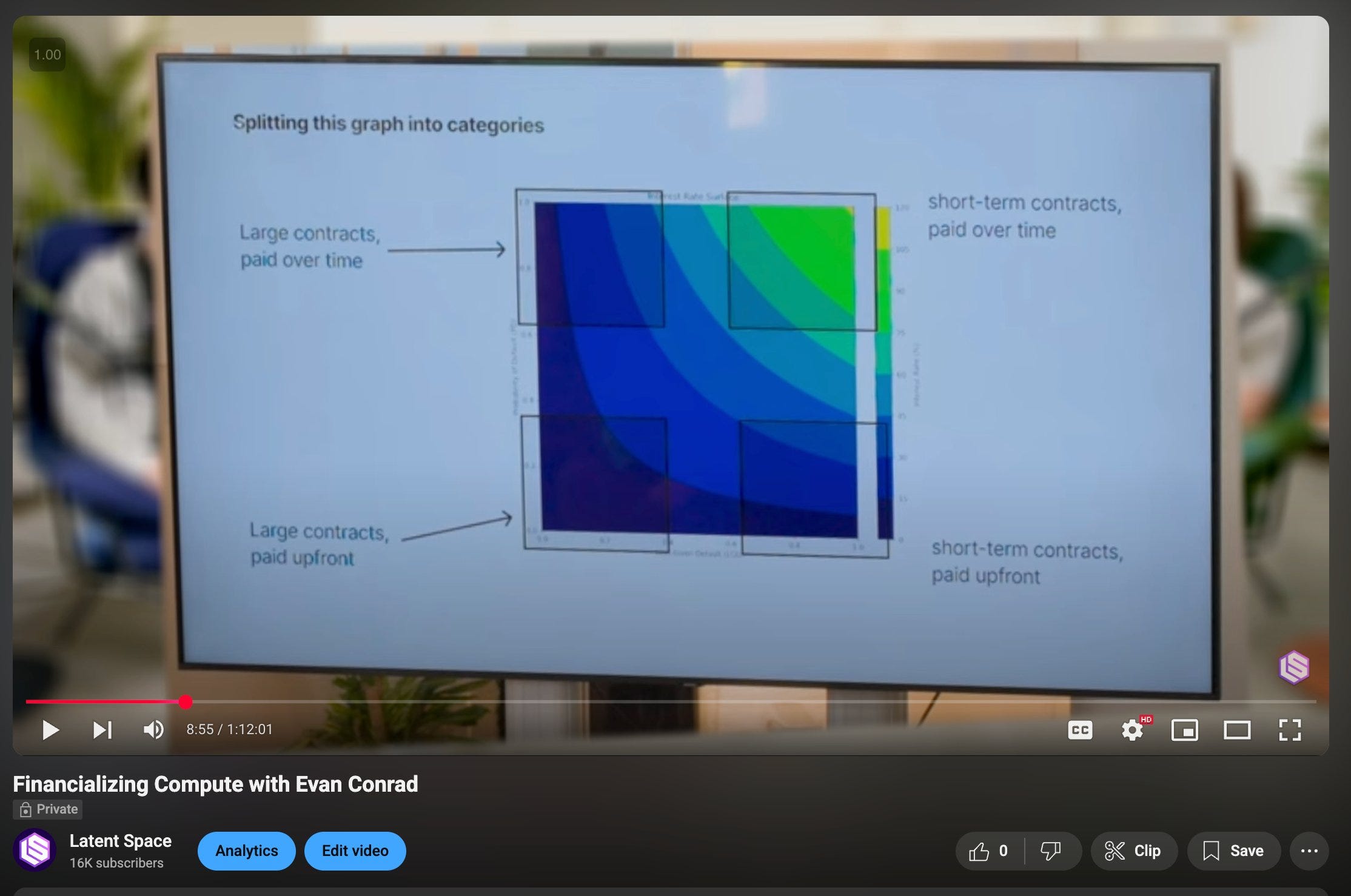

Swyx: So CoreUv locked up long-term contracts. Get that. Yes. Maybe share your mental framework. Just verbally describe it because we're trying to help the audio listeners as well. Sure. People can look up the chart if they want to.

Evan: Sure. Okay. So this is a graph of interest rates. And on the y-axis, it's a probability you're able to sell your GPUs from zero to one. And on the x-axis, it's how much they'll depreciate in cost from zero to one. And then you had ISO cost curves or ISO interest rate curves. Yeah. So they kind of shape in a sort of concave fashion. Yeah. The lowest interest rates enable the most aggressive. form of this cost curve. And the higher interest rates go, the more you have to push out to the top right. Yeah. And then you had some analysis of where every player sits in this, including CoreUv, but also Together and Modal and all these other guys. I thought that was super insightful. So I just wanted to elaborate. Basically, it's like a graph of risk and the genres of places where you can be and what the risk is associated with that. The optimal thing for you to do, if you can, is to lock in long-term contracts that are paid all up front or in with a situation in which you trust the other party to pay you over time. So if you're, you know, selling to Microsoft or something or OpenAI. Which are together 77% of the revenue of CoreUv. Yeah. So if you're doing that, that's a great business to be in because your interest rate that you can pitch for is really low because no one thinks Microsoft is going to default. And like maybe OpenAI will default, but the backing by Microsoft kind of doesn't. And I think there's enough, like, generally, it looks like OpenAI is winning that you can make it's just a much better case than if you're selling to the pre-seed startup that just raised $30 million or something pre-revenue. It's like way easier to make the case that the OpenAI is not going to default than the pre-seed startup. And so the optimal place to be is selling to the maximally low risk customer for as long as possible. And then you never have to worry about depreciation and you make lots of money. The less. Good. Good place to be is you could sell long-term contracts to people who might default on you. And then if you're not bringing it to the present, so you're not like saying, hey, you have to pay us all up front, then you're in this like more risky territory. So is it top left of the chart? If I have the chart right, maybe. Large contracts paid over time. Yeah. Large contracts paid over time is like top left. So it's more risky, but you could still probably get away with it. And then the other opportunity is that you could sell short-term contracts for really high prices. And so lots of people tried that too, because this is actually closer to the original business model that people thought would work in cloud providers for CPUs. It works for CPUs, but it doesn't really work for GPUs. And I don't think people were trying this because they were thinking about the risk associated with it. I think a lot of people are just come from a software background, have not really thought about like cogs or margins or inventory risk or things that you have to worry about in the physical world. And I think they were just like copy pasting the same business model onto CPUs. And also, I remember fundraising like a few years ago. And I know based on. Like what we knew other people were saying who were in a very similar business to us versus what we were saying. And we know that our pitch was way worse at the time, because in the beginning of SF Compute, we looked very similar to pretty much every other GPU cloud, not on purpose, but sort of accidentally. And I know that the correct pitch to give to an investor was we will look like a traditional CPU cloud with high margins and we'll sell to everyone. And that is a bad business model because your customers are price sensitive. And so what happens is if you. Sell at high prices, which is the price that you would need to sell it in order to de-risk your loss on the depreciation curve, and specifically what I mean by that is like, let's say you're selling it like $5 an hour and you're paying $1.50 an hour for the GPU under the hood. It's a little bit different than that, but you know, nice numbers, $5 an hour, $1.50 an hour. Great. Excellent. Well, you're charging a really high price per GPU hour because over time the price will go down and you'll get competed out. And what you need is to make sure that you never go under, or if you do go under your underlying cost. You've made so much money in the first part of it that the later end of it, like doesn't matter because from the whole structure of the deal, you've made money. The problem is that just, you think that you're going to be able to retain your customers with software. And actually what happens is your customers are super price sensitive and push you down and push you down and push you down and push you down, um, that they don't care about your software at all. And then the other problem that you have is you have, um, really big players like the hyperscalers who are looking to win the market and they have way more money than you, and they can push down on margin. Much better than you can. And so if they have to, and they don't, they don't necessarily all the time, um, I think they actually keep pride of higher margin, but if they needed to, they could totally just like wreck your margin at any point, um, and push you down, which meant that that quadrant over there where you're charging a high price, um, and just to make up for the risk completely got destroyed, like did not work at all for many places because of the price sensitivity, because people could just shove you down instead that pushed everybody up to the top right-hand corner of that, which is selling short-term. Contracts for low prices paid over time, which is the worst place to be in, um, the worst financial place to be in because it has the highest interest rate, um, which means that your, um, your costs go up at the same time, your, uh, your incoming cash goes down and squeezes your margins and squeezes your margins. The nice thing for like a core weave is that most of their business is over on the, on the other sides of those quadrants that the ones that survive. The only remaining question I have with core weave, and I promise I get to ask if I can compute, and I promise this is relevant to SOF Compute in general, because the framework is important, right? Sure. To understand the company. So why didn't NVIDIA or Microsoft, both of which have more money than core weave, do core weave, right? Why didn't they do core weave? Why have this middleman when either NVIDIA or Microsoft have more money than God, and they could have done an internal core weave, which is effectively like a self-funding vehicle, like a financial instrument. Why does there have to be a third party? Your question is like... Why didn't Microsoft, or why didn't NVIDIA just do core weave? Why didn't they just set up their own cloud provider? I think, and I don't know, and so correct me if I'm wrong, and lots of people will have different opinions here, or I mean, not opinions, they'll have actual facts that differ from my facts. Those aren't opinions. Those are actually indeed differences of reality, is that NVIDIA doesn't want to compete with their customers. They make a large amount of money by selling to existing clouds. If they launched their own core weave, then it would be a lot more money. It'd make it much harder for them to sell to the hyperscalers, and so they have a complex relationship with there. So not great for them. Second is that, at least for a while, I think they were dealing with antitrust concerns or fears that if they're going through, if they own too much layers of the stack, I could imagine that could be a problem for them. I don't know if that's actually true, but that's where my mind would go, I guess. Mostly, I think it's the first one. It's that they would be competing directly with their primary customers. Then Microsoft could have done it, right? That's the other question. Yeah, so Microsoft didn't do it. And my guess is that... NVIDIA doesn't want Microsoft to do it, and so they would limit the capacity because from NVIDIA's perspective, both they don't want to necessarily launch their own cloud provider because it's competing with their customers, but also they don't want only one customer or only a few customers. It's really bad for NVIDIA if you have customer concentration, and Microsoft and Google and Amazon, like Oracle, to buy up your entire supply, and then you have four or five customers or so who pretty much get to set prices. Monopsony. Yeah, monopsony. And so the optimal thing for you is a diverse set of customers who all are willing to pay at whatever price, because if you don't, somebody else will. And so it's really optimal for NVIDIA to have lots of other customers who are all competing against each other. Great. Just wanted to establish that. It's unintuitive for people who have never thought about it, and you think about it all day long. Yeah.

Swyx: The last thing I'll call out from the talk, which is kind of cool, and then I promise we'll get to SF Compute, is why will DigitalOcean and Together lose money on their clusters? Why will DigitalOcean and Together lose money on their clusters?

Evan [00:16:33]: I'm going to start by clarifying that all of these businesses are excellent and fantastic. That Together and DigitalOcean and Lambda, I think, are wonderful businesses who build excellent products. But my general intuition is that if you try to couple the software and the hardware together, you're going to lose money. That if you go out and you buy a long-term contract from someone and then you layer on services, or you buy the hardware yourself and you spin it up and you get a bunch of debt, you're going to run into the same problem that everybody else did, the same problem we did, same problem the hyperscalers did. And that's exactly what the hyperscalers are doing, which is you cannot add software and make high margins like a cloud provider can. You can pitch that into investors and it will totally make sense, and it's like the correct play in CPUs, but there isn't software you could make to make this occur. If you're spending a billion dollars on hardware, you need to make a billion dollars of software. There isn't a billion dollars of software that you can realistically make, and if you do, you're going to look like SAP. And that's not a knock on SAP. SAP makes a f**k ton of money, right? Right. Right. Right. Right. There aren't that many pieces of software that you could make, that you can realistically sell, like a billion dollars of software, and you're probably not going to do it to price-sensitive customers who are spending their entire budget already on compute. They don't have any more money to give you. It's a very hard proposition to do. And so many parties have been trying to do this, like, buy their own compute, because that's what a traditional cloud does. It doesn't really work for them. You know that meme where there's, like, the Grim Reaper? And he's, like, knocking on the door, and then he keeps knocking on the next door? We have just seen door after door after door of the Grim Reeker comes by, and the economic realities of the compute market come knocking. And so the thing we encourage folks to do is if you are thinking about buying a big GPU cluster and you are going to layer on software on top, don't. There are so many dead bodies in the wake there. We would recommend not doing that. And we, as SF Compute, our entire business is structured to help you not do that. It's helped disintegrate these. The GPU clouds are fantastic real estate businesses. If you treat them like real estate businesses, you will make a lot of money. The cloud services you can make on that, all the software you want to make on that, you can do that fantastically. If you don't own the underlying hardware, if you mix these businesses together, you get shot in the head. But if you combine, if you split them, and that's what the market does, it helps you split them, it allows you to buy, like, layer on services, but just buy from the market, you can make lots of money. So companies like Modal, who don't own the underlying compute, like they don't own it, lots of money, fantastic product. And then companies like Corbeave, who are functionally like really, really good real estate businesses, lots of money, fantastic product. But if you combine them, you die. That's the economic reality of compute. I think it also splits into trading versus inference, which are different kinds of workloads. Yeah. And then, yeah, one comment about the price sensitivity thing before we leave this. This topic, I want to credit Martin Casado for coining or naming this thing, which is like, you know, you said, you said this thing about like, you don't have room for a 10% margin on GPUs for software. Yep. And Martin actually played it out further. It's his first one I ever saw doing this at large enough runs. So let's say GPT-4 and O1 both had a total trading cost of like a $500 billion is the rough estimate. When you get the $5 billion runs, when you get the $50 billion runs, it is actually makes sense to build your own. You're going to have to get into chips, like for OpenEI to get into chip design, which is so funny. I would make an ASIC for this run. Yeah, maybe. I think a caveat of that that is not super well thought about is that only works if you're really confident. It only works if you really know which chip you're going to do. If you don't, then it's a little harder. So it makes in my head, it makes more sense for inference where you've already established it. But for training there's so much like experimentation. Any generality, yeah. Yeah. The generality is much more useful. Yeah. In some sense, you know, Google's like six generations into the CPUs. Yeah. Yeah. Okay, cool. Maybe we should go into SF Compute now. Sure. Yeah.

Alessio [00:20:37]: Yeah. So you kind of talked about the different providers. Why did you decide to go with this approach and maybe talk a bit about how the market dynamics have evolved since you started a company?

Evan [00:20:47]: So originally we were not doing this at all. We were definitely like forced into this to some extent. And SF Compute started because we wanted to go train models for music and audio in general. We were going to do a sort of generic audio model at some points, and then we were going to do a music model at some points. It was an early company. We didn't really spec down on a particular thing. But yeah, we were going to do a music model and audio model. First thing that you do when you start any AI lab is you go out and you buy a big cluster. The thing we had seen everybody else do was they went out and they raised a really big round and then they would get stuck. Because if you raise the amount of money that you need to train a model initially, like, you know, the $50 million pre-seed, pre-revenue, your valuation is so high or you get diluted so much that you can't raise the next round. And that's a very big ask to make. And also, I don't know, I felt like we just felt like we couldn't do it. We probably could have in retrospect, but I think one, we didn't really feel like we could do it. Two, it felt like if we did, we would have been stuck later on. We didn't want to raise the big round. And so instead, we thought, surely by now, we would be able to just go out. To any provider and buy like a traditional CPU cloud would sell offer you and just buy like on demand or buy like a month or so on. And this worked for like small incremental things. And I think this is where we were basing it off. We just like assumed we could go to like Lambda or something and like buy thousands of at the time A100s. And this just like was not at all the case. So we started doing all the sales calls with people and we said, OK, well, can we just get like month to month? Can we get like one month of compute or so on? Everyone told us at the time, no. You need to have a year long contract or longer or you're out of luck. Sorry. And at the time, we were just like pissed off. Like, why won't nobody sell us a month at a time? Nowadays, we totally understand why, because it's the same economic reason. Because if you if they had sold us the month to month or so on and we canceled or so on, they would have massive risk on that. And so the optimal thing to do was to only to just completely abandon the section of the market. We didn't like that. So our plan was we were going to buy a year long contract anyway. We would use a month. And then we would. At least the other 11 months. And we were locked in for a year, but we only had to pay on every individual month. And so we did this. But then immediately we said, oh, s**t, now we have a cloud provider, not a like training models company, not an AI lab, because every 30 days we owed about five hundred thousand dollars or so and we had about five hundred thousand dollars in the bank. So that meant that every single month, if we did not sell out our cluster, we would just go bankrupt. So that's what we did for the first year of the company. And when you're in that position. You try to think how in the world you get out of that position, what that transition to is, OK, well, we tend to be pretty good at like selling this cluster every month because we haven't died yet. And so what we should do is we should go basically be like this broker for other people and we will be more like a GPU real estate or like a GPU realtor. And so we started doing that for a while where we would go to other people who had who was trying to sell like a year long contract with somebody and we'd go to another person who like maybe this person wanted six months and somebody else on six months or something and we'd like combine all these people. Together to make the deal happen and we'd organize these like one off bespoke deals that looked like basically it ended up with us taking a bunch of customers, us signing with a vendor, taking some cut and then us operating the cluster for people typically with bare metal. And so we were doing this, but this was definitely like a oh, s**t, oh, s**t, oh, s**t. How do we get out of our current situation and less of a like a strategic plan of any sort? But while we were doing this, since like the beginning of the company, we had been thinking about how to buy GPU clusters, how to sell them effectively, because we'd seen every part of it. And what we ended up with was like a book of everybody who's trying to buy and everyone is trying to sell because we were these like GPU brokers. And so that turned into what is today SF Compute, which is a compute market, which we think we are the functionally the most liquid GPU market of any capacity. Honestly, I think we're the only thing that actually is like a real market that there's like bids and asks and there's like a like a trading engine that combines everything. And so. I think we're the only place where you can do things that a market should be able to do. Like you can go on SF Compute today and you get thousands of H100s for an hour if you want. And that's because there is a price for thousands of GPUs for an hour. That is like not a thing you can reasonably do on kind of any other cloud provider because nobody should realistically sell you thousands of GPUs for an hour. They should sell it to you for a year or so on. But one of the nice things about a market is that you can buy the year on SF Compute. But then if you need to sell. Back, you can sell back as well. And that opens up all these little pockets of liquidity where somebody who's just trying to buy for a little bit of time, some burst capacity. So people don't normally buy for an hour. That's not like actually a realistic thing, but it's like the range somebody who wants, who is like us, who needed to buy for a month can actually buy for a month. They can like place the order and there is actually a price for that. And it typically comes from somebody else who's selling back. Somebody who bought a longer term contract and is like they bought for some period of time, their code doesn't work, and now they need to like sell off a little bit.

Alessio [00:25:49]: What are the utilization rates at which a market? What are the utilization rates at which a market? Like this works, what do you see the usual GPU utilization rate and like at what point does the market get saturated?

Evan [00:26:00]: Assuming there are not like hardware problems or software problems, the utilization rate is like near 100 percent because the price dips until the utilization is 100 percent. So the price actually has to dip quite a lot in order for the utilization not to be. That's not always the case because you just have logistical problems like you get a cluster and parts of the InfiniBand fabric are broken. And there's like some issue with some switch somewhere and so you have to take some portion of the cluster offline or, you know, stuff like this, like there's just underlying physical realities of the clusters, but nominally we have better utilization than basically anybody because, but that's on utilization of the cluster, like that doesn't necessarily translate into, I mean, I actually do think we have much better overall money made for our underlying vendors than kind of anybody else. We work with the other GPU clouds and the basic pitch to the other GPU clouds is one. So we can sell your broker so we can we can find you the long term contracts that are at the prices that you want, but meanwhile, your cluster is idle and for that we can increase your utilization and get you more money because we can sell that idle cluster for you and then the moment we find the longer, the bigger customer and they come on, you can kick off those people and then go to the other ones. You get kind of the mix of like sell your cluster at whatever price you can get on the market and then sell your cluster at the big price that you want to do for long term contract, which is your ideal business model. And then the benefit of the whole thing being on the market. Is you can pitch your customer that they can cancel their long term contract, which is not a thing that you can reasonably do if you are just the GPU cloud, if you're just the GPU cloud, you can never cancel your contract, because that introduces so much risk that you would otherwise, like not get your cheap cost of capital or whatever. But if you're selling it through the market, or you're selling it with us, then you can say, hey, look, you can cancel for a fee. And that fee is the difference between the price of the market and then the price that they paid at, which means that they canceled and you have the ability to offer that flexibility. But you don't. You don't have to take the risk of it. The money's already there and like you got paid, but it's just being sold to somebody else. One of our top pieces from last year was talking about the H100 glut from all the long term contracts that were not being fully utilized and being put under the market. You have on here dollar a dollar per hour contracts as well as it goes up to two. Actually, I think you were involved. You were obliquely quoted in that article. I think you remember. I remember because this was hidden. Well, we hid your name, but then you were like, yeah, it's us. Yeah. Could you talk about the supply and demand of H100s? Was that just a normal cycle? Was that like a super cycle because of all the VC funding that went in in 2003? What was that like? GPU prices have come down. Yeah, GPU prices have come down. And there's some part that has normal depreciation cycle. Some part of that is just there were a lot of startups that bought GPUs and never used them. And now they're lending it out and therefore you exist. There's a lot of like various theories as to why. This happened. I dislike all of them because they're all kind of like they're often said with really high confidence. And I think just the market's much more complicated than that. Of course. And so everything I'm going to say is like very hedged. But there was a series of like places where a bunch of the orders were placed and people were pitching to their customers and their investors and just the broader market that they would arrive on time. And that is not how the world works. And because there was such a really quick build out of things, you would end up with bottlenecks in the supply chain somewhere that has nothing to do with necessarily the chip. It's like the InfiniBand cables or the NICs or like whatever. Or you need a bunch of like generators or you don't have data center space or like there's always some bottleneck somewhere else. And so a lot of the clusters didn't come online within the period of time. But then all the bottlenecks got sorted out and then they all came online all at the same time. So I think you saw a short. There was a shortage because supply chain hard. And then you saw a increase or like a glut because supply chain eventually figure itself out. And specifically people overordered in order to get the allocation that they wanted. Then they got the allocations and then they went under. Yeah, whatever. Right. There was just a lot of shenanigans. A caveat of this is every time you see somebody like overordered, there is this assumption that the problem was like the demand went down. I don't think that's the case at all. And so I want to clarify that. It definitely seems like a shortage. Like there's more demand for GPUs than there ever was. It's just that there was also more supply. So at the moment, I think there is still functionally a glut. But the difference that I think is happening is mostly the test time inference stuff that you just need way more chips for that than you did before. And so whenever you make a statement about the current market, people sort of take your words and then they assume that you're making a statement about the future market. And so if you say there's a glut now, people will continue to think there's a glut. But I think what is happening at the moment. My general prediction is that like by the winter, we will be back towards shortage. But then also, this very much depends on the rollout of future chips. And that comes with its own. I think I'm trying to give you like a good here's Evan's forecast. Okay. But I don't know if my forecast is right. You don't have to. Nobody is going to hold you to it. But like I think people want to know what's true and what's not. And there's a lot of vague speculations from people who are not that close to the market actually. And you are. I think I'm a closer. Close to the market, but also a vague speculator. Like I think there are a lot of really highly confident speculators and I am indeed a vague speculator. I think I have more information than a lot of other people. And this makes me more vague of a spectator because I feel less certain or less confident than I think a lot of other people do. The thing I do feel reasonably confident about saying is that the test time inference is probably going to quite significantly expand the amount of compute that was used for inference. So a caveat. This is like pretty much all the inference demand is in a few companies. A good example is like lots of bio and pharma was using H100s training sort of the bio models of sorts. And they would come along and they would buy, you know, thousands of H100s for training and then just like not a lot of stuff for inference. Not in any, not relative to like an opening iron anthropic or something because they like don't have a consumer product. Their inference event, if they can do it right. There's really like only one inference event that matters. And obviously I think they're going to run into it. And Batch and they're not going to literally just run one inference event. But like the one that produces the drug is the important one. Right. And I'm dumb and I don't know anything about biology, so I could be completely wrong here. But my understanding is that's kind of the gist. I can check that for you. You can check that for me. Check that for me. But my understanding is like the one that produces the sequence that is the drug that, you know, cures cancer or whatever. That's the important deal. But like a lot of models look like this where they're sort of more enterprising use cases or they're so prior to something that looks like test time inference. You got lots and lots of demand for training and then pretty much entirely fell off for inference. And I think like we looked at like Open Router, for example, the entirety of Open Router that was not anthropic or like Gemini or OpenAI or something. It was like 10 H100 nodes or something like that. It's just like not that much. It's like not that many GPUs actually to service that entire demand. But that's like a really sizable portion of the sort of open source market. But the actual amount of compute needed for it was not that much. But if you imagine like what an OpenAI needs for like GPT-4, it's like tremendously big. But that's because it's a consumer product that has almost all the inference demand. Yeah, that's a message we've had. Roughly open source AI compared to closed AI is like 5%. Yeah, it's like super small. Super small. It's super small. Super small. But test time inference changes that quite significantly. So I will... I will expect that to increase our overall demand. But my question on whether or not that actually affects your compute price is entirely based on how quickly do we roll out the next chips. The way that you burst is different for test time.

Alessio [00:34:01]: Any thoughts on the third part of the market, which is the more peer-to-peer distributed, some are like crypto-enabled, like Hyperbolic, Prime Intellect, and all of that. Where do those fit? Like, do you see a lot of people will want to participate in a peer-to-peer market? Or just because of the capital requirements at the end of the day, it doesn't really matter?

Evan [00:34:20]: I'm like wildly skeptical of these, to be frankly. The dream is like steady at home, right? I got this $15.90. Nobody has $15.90. $14.90 sitting at home. I can rent it out. Yeah. Like, I just don't really think this is going to ever be more efficient than a fully interconnected cluster with InfiniBand or, you know, whatever the sort of next spec might be. Like, I could be completely wrong. But speaking of... I mean, like, SpeedoLite is really hard to beat. And regardless of whatever you're using, you just like can't get around that physical limitation. And so you could like imagine a decentralized market that still has a lot of places where there's like co-location. But then you would get something that looks like SF Compute. And so that's what we do. That's why we take our general take is like on SF Compute, you're not buying from like random people. You're buying from the other GPU clouds, functionally. You're buying from data centers that are the same genre of people that you would work with already. And you can specify, oh, I want all these nodes to be co-located. And I don't think you're really going to get around that. And I think I buy crypto for the purposes of like transferring money. Like the financial system is like quite painful and so on. I can understand the uses of it to sort of incentivize an initial market or try to get around the cold start problem. We've been able to get around the cold start problem just fine. So it didn't actually need that at all. What I do think is totally possible is you could launch a token and then you could like subsidize the crypto. You could compute prices for a bit, but like maybe that will help you. I think that's what Nuus is doing. Yeah, I think there's lots of people who are trying to do things like this, but at some point that runs out. So I would, I think generally agree. I think the only thread in that model is very fine grained mixture of experts that can be like algorithms can shift to adapt to hardware realities. And the hardware reality is like, okay, it's annoying to do large co-located clusters. Then we'll just redesign attention or whatever in our architecture to distribute it more. There was a little bit buzz of block attention last year that Strong Compute made a big push on. But I think like, you know, in a world where we have 200 experts in MOE model, it starts to be a little bit better. Like, I don't disagree with this. I can imagine the world in which you have like, in which you've redesigned it to be more parallelizable, like across space.

Evan [00:36:43]: But assuming without that, your hardware limitation is your speed of light limitation. And that's a very hard one to get around.

Alessio [00:36:50]: Any customers or like stories that you want to shout out of like maybe things that wouldn't have been economically viable like others? I know there's some sensitivity on that.

Evan [00:37:00]: My favorites are grad students, are folks who are trying to do things that would normally otherwise require the scale of a big lab. And the grad students are like the worst pilots. They're like the worst possible customer for the traditional GPU clouds because they will immediately turn if you sell them a thing because they're going to graduate and they're not going to go anywhere. They're not going to like, that project isn't continuing to spend lots of money. Like sometimes it does, but not if you're like working with the university or you're working with the lab of some sort. But a lot of times it's just like the ability for us to offer like big burst capacity, I think is lovely and wonderful. And it's like one of my favorite things to do because all those folks look like we did. And I have a special place in my heart for that. I have a special place in my heart for young hackers and young grad students and researchers who are trying to do the same genre of thing that we are doing. For the same reason, I have a special place in my heart for like the startups, the people who are just activel