Faith & Finance

660 episodes — Page 8 of 14

Ep 591Trusting God for Our Daily Bread

"Do not heap up empty phrases as the Gentiles do, for they think that they will be heard for their many words." – Matthew 6:7In Matthew 6, Jesus warns against meaningless repetition in prayer. Thankfully, He doesn’t leave us wondering how to pray. Instead, He gives us the Lord’s Prayer—an example of how we should approach God with our needs.But have you ever noticed how often we overlook a key part of this prayer? The request for provision:"Give us this day our daily bread." – Matthew 6:11This simple yet profound verse reminds us that God is our provider. He wants us to come before Him humbly, asking for what we need. And in a world where self-sufficiency is often celebrated, this truth is more important than ever.God Is Our ProviderJesus’ words in Matthew 6:11 serve as a powerful reminder that we depend on God for our most basic needs—starting with food. It’s easy to take this for granted, especially in a time and place where food shortages are rarely a daily concern.But do we truly recognize that all provision comes from God? Do we regularly thank Him for our meals and daily necessities? Or do we fall into the trap of thinking that our own efforts—our jobs, savings, and financial planning—are what sustain us?It’s only when we face scarcity—when food, money, or security seem uncertain—that we remember our true dependence on God. But Jesus calls us to recognize this truth every day, not just in times of crisis.The phrase “Give us this day our daily bread” has a deeper meaning than just food. It speaks to all our needs—physical, emotional, and spiritual. We hunger for more than just nourishment. We long for peace, love, purpose, and meaningful relationships.Jesus teaches us to bring these needs to God in prayer, acknowledging that only He can truly satisfy us. The Lord’s Prayer is not just about survival—it’s about trusting that God will provide everything we need, both physically and spiritually.The Danger of Self-SufficiencyFor those of us living in relative abundance, the idea of asking for daily bread might feel distant. Unlike Jesus’ original audience, who often faced food insecurity, we may not think about whether we’ll eat tomorrow. In fact, for many, the challenge is having too much rather than too little.Yet, even in prosperity, Jesus’ words remain critical. This prayer reminds us that we are not self-sufficient. It helps guard against the illusion that we control our own destiny.The danger of materialism is subtle. We may not consciously reject God’s provision, but when we place our trust in our bank accounts, investments, or careers, we begin to believe that we sustain ourselves. That mindset leads to pride—and ultimately distances us from God.Jesus knew our hearts would struggle with this. That’s why He later says:"Seek first the kingdom of God and His righteousness, and all these things will be added to you." – Matthew 6:33We don’t need to worry about our next meal, our financial security, or our future. What we truly need is God Himself. And prayer reminds us of that.Breaking the Grip of MaterialismOne way to keep our hearts aligned with this truth is through generosity. Giving is a tangible way to acknowledge that God—not our wealth—is our provider. When we give, we loosen the grip that money has on us and demonstrate our faith that God will continue to meet our needs.There will always be reasons to worry—economic downturns, market fluctuations, unexpected expenses. But these uncertainties should drive us to prayer, not fear.So, the next time you pray, “Give us this day our daily bread,” say it with sincerity. Recognize your dependence on God. Thank Him for His provision. And let that gratitude lead you to trust—and give—more freely.On Today’s Program, Rob Answers Listener Questions:I'm 68 and plan to retire at 72. I owe $95,000 on a condo with a 7.125% interest rate. I've been paying an extra $1,000 per month towards the principal, but I'd like to know if I should do something else with that money instead of paying down the mortgage. I want to be debt-free when I retire. What should I do?I have some stock savings I was planning to use for retirement. But I had to max out a credit card a couple of years ago when I lost income. The collection agency is offering to let me pay 75-80% of the debt in a lump sum. Should I take money from my stocks to pay this off or try to work out a monthly payment plan instead?I recently won a $570,000 home from the St. Jude Dream Home Giveaway. When I took ownership, I had to pay $205,000 in taxes. My CPA says I could pay an additional 20% capital gains tax when I sell. I've had the home for a few years, and its value hasn't changed much. Can you help me understand the capital gains tax and how I can minimize the tax burden?Resources Mentioned:Faithful Steward: FaithFi’s New Quarterly MagazineChristian Credit CounselorsLook At The Sparrows: A 21-Day Devotional on Financial Fear and AnxietyRich Toward God: A Study on the Parable of the Rich FoolFind a Certified Ki

Ep 590Aligning Your Giving with God's Heart with David Wills

You’re generous; you love to give. But how do you know that your giving is having a real impact?It’s great that you have a heart for giving. The next step is to make sure your giving really counts…and that’s by aligning it with God’s heart. David Wills is here today to help us do that.David Wills is President Emeritus of The National Christian Foundation (NCF). He is also the co-author of Investing in God’s Business (The “How To” of Smart Christian Giving) and numerous articles and lectures nationwide. The Three Big Questions of GenerosityWhen it comes to giving, most Christians wrestle with three fundamental questions:Why should I be generous?How do I give?Where should I give?The first two questions deal with the heart and the head—our motivations for generosity and the practical ways to implement it. But the third question—where should I give?—often receives less attention. Instead of starting with our passions, we should begin with God's priorities.God asks us to be generous on every occasion so that it brings Him glory and joy to our hearts. But instead of asking, “What am I passionate about?” We should ask, “What is God passionate about?”A Framework for Giving: The Three-by-Three GridTo help believers align their giving with God’s priorities, David introduced a three-by-three framework that incorporates both geography and biblical causes.1. The Geography of GivingA great biblical guide for the where of giving comes from Acts 1:8:“You will be my witnesses in Jerusalem, and in all Judea and Samaria, and to the ends of the earth.”This verse provides a three-tiered approach to geographic giving:Local (Jerusalem)—Giving within our immediate communities, such as supporting our local church and meeting local needs. National (Judea and Samaria)—Supporting broader efforts within our country, including church planting, evangelism, and charitable organizations. International (Ends of the Earth)—Expanding generosity to global missions, Bible translation, and aid to those who have never heard the Gospel.Most people focus on what’s right in front of them—their local church or nearby needs. However, a biblical giving strategy challenges us to think beyond our immediate surroundings.2. The Biblical Priorities of GivingScripture reveals three overarching themes that reflect God's heart for giving:The Great Commission (Matthew 28:19-20)—Supporting efforts that spread the Gospel, such as evangelism, church planting, missions, and discipleship. The Greatest Commandment (Matthew 22:37-38)—Giving to ministries that help people grow in their love for God, including churches, theological education, and discipleship initiatives. The Great Compassion (Matthew 22:39)—Caring for our neighbors by giving to those in need—orphans, widows, the poor, and the vulnerable.These three biblical priorities form the vertical axis of the giving framework, while geography forms the horizontal axis.By overlaying these two dimensions—geography and biblical priorities—believers can develop a well-rounded and God-centered giving plan. This framework helps us see the gaps in our giving. Many believers focus on what’s nearby, but God calls us to care for those who have never heard the Gospel or are in extreme need.Making Giving a Family PracticeOne of the most powerful aspects of this framework is its ability to teach children about generosity. Parents can use this model to discuss giving priorities as a family and even create a family giving plan that reflects God’s heart.We encourage families to:Sit down together and map out their giving on the three-by-three frameworkDiscuss where they are giving too much or too little.Involve children in researching and selecting ministries that align with biblical priorities.Regularly review and adjust their giving strategy as a family.For those who want to track their giving over time, organizations like the National Christian Foundation (NCF) provide tools to help families and individuals monitor their generosity.Aligning Your Giving with God's HeartUltimately, giving isn’t about following personal passions—it’s about reflecting God’s heart. By using a biblical framework for giving, we can be more intentional and experience greater joy in generosity.Take Action Today:Assess your current giving. Does it align with God’s heart?Use the three-by-three framework to create a more balanced, intentional plan.Involve your family in discussions about generosity.Consider using a giving platform like NCF to track and refine your generosity over time.To read David’s full article on this topic, explore Faithful Steward, FaithFi’s new quarterly magazine. You can access it by becoming a FaithFi Partner for $35 per month or $400 per year at FaithFi.com/give.On Today’s Program, Rob Answers Listener Questions:My daughter is turning 16 today, and I'd like to help her become more responsible with her money. Can you recommend any debit cards or apps that are good options for teens? I'm looking for something faith-oriented.I'm work

Ep 589Navigating Tariffs and Economic Uncertainty with Bob Doll

"And my God will supply every need of yours according to His riches in glory in Christ Jesus." — Philippians 4:19This verse is a powerful reminder that God is our ultimate provider, no matter the economic uncertainties we face. Recently, we have seen that many have been concerned about trade tariffs and their potential impact on the economy. Today, Bob Doll joins us to explain what this means and what we can expect moving forward.Bob Doll is the CEO and CIO of Crossmark Global Investments. He regularly contributes to Faith and Finance and other media outlets like Bloomberg TV, Fox Business, and CNBC. What Are Tariffs and How Do They Affect Us?Tariffs are essentially taxes. If a 10% tariff is placed on imported goods, the price of those goods increases. That means consumers pay more for the products they need, which can slow down economic activity.However, tariffs are not just about taxation; they are often used as a bargaining tool in international trade negotiations. Sometimes, it depends on the day of the week because tariffs are on one day and then off the next. This back-and-forth can create uncertainty in the market and impact businesses, investors, and consumers alike.Why Do Markets React Negatively to Tariffs?The stock market tends to respond negatively whenever there's talk of tariffs. Why?Tariffs can slow economic growth. If companies and consumers have to pay more for goods, they either buy fewer products or cut back on spending in other areas. This dampens growth, and the market doesn’t like it.Could tariffs alone push the economy into a recession? If they are significant enough, last too long, and trigger retaliation from other countries, it could certainly lead to what economists call a trade war. A trade war is not healthy for economic growth, but cooler minds will likely prevent it from escalating too far.The Strategy Behind Tariffs: Negotiation or Necessity?So, is the push for tariffs simply a negotiation tactic, or is there a deeper economic issue at play?There’s no question that the U.S. has a trade imbalance with many countries. Addressing this imbalance is part of the reasoning behind tariffs. However, political leaders understand the risks and use tariffs more as a bargaining tool than a long-term strategy. They don’t want to sink the economy because these leaders have a vested interest in economic stability.Finding Peace in Economic UncertaintyDiscussions about tariffs, markets, and recessions can easily lead to fear. Economic uncertainty often leaves people feeling anxious about their financial future. But as believers, we have a greater source of security.Here are three key reminders:Leaders Care About Economic Stability—Regardless of their approach, political leaders generally want a strong economy. The Economy is Resilient—Whether we have tariffs or not, the economy is doing well, and its economic fundamentals are still strong. God is in Control—Most importantly, our hope is not in governments, markets, or policies but in God. God knows the end from the beginning, including tariffs. Psalm 91 reminds us that God is our refuge and fortress—we can rest securely in His protection.Focus on What You Can Control: Faithful StewardshipWhile we can’t control global trade policies, tax laws, or the stock market, we can control how we manage our own finances. We can control our own little economies—what passes through our hands. That means practicing faithful stewardship.We need to take care of everything God has given us—not just money, but all aspects of life: our minds, our bodies, our time. Being wise stewards of our finances means making thoughtful financial decisions, saving wisely, and giving generously. After all, it’s not ours; it’s all God’s.When we recognize that everything we have belongs to God, it transforms the way we handle money. Rather than holding onto it tightly, we can give joyfully and generously.Economic uncertainty will always exist, whether through tariffs, inflation, or market fluctuations. But believers are called to a higher perspective. Instead of being driven by fear, we can rest in the truth that God is sovereign over all things—even global trade policies.The key is to focus on what we can control: managing our finances wisely, practicing faithful stewardship, and embracing the joy of generosity. And through it all, we can trust that God is our refuge and provider, no matter what challenges come our way.On Today’s Program, Rob Answers Listener Questions:I recently received a sizable inheritance. I have some ideas about what to do with it, but I wanted to get your thoughts first.I would like to know where and how to invest. My husband and I are both retired. I have $200,000 left in my TSP and approximately $270,000 in IRA CDs, a small portion of which is Roth IRAs.Resources Mentioned:Faithful Steward: FaithFi’s New Quarterly MagazineCrossmark Global InvestmentsLook At The Sparrows: A 21-Day Devotional on Financial Fear and AnxietyRich Toward God: A Study on the Pa

Ep 588The Key to Long-Term Financial Success with Matt Bell

"Prepare your work outside; get everything ready for yourself in the field, and after that build your house." - Proverbs 24:27That verse underscores the need for planning and execution, key elements for long-term financial success. Matt Bell joins us today to discuss how to put planning and execution to work for you.Matt Bell is the Managing Editor at Sound Mind Investing, an underwriter of Faith & Finance. The Importance of a Financial PlanLife tends to happen to us while we’re making other plans. Unfortunately, for many people, life happens without any financial planning at all. Millions of individuals fail to establish a clear strategy for managing their money, and even those who attempt to plan often struggle to stay on track.Without a plan, it's easy to drift financially, reacting to circumstances rather than proactively building a stable financial future. The impact of financial planning—and, more importantly, execution—can be profound.A 2011 study analyzed data from over 1,200 individuals aged 50 and older, examining their approach to financial planning and its effect on their retirement net worth. The study categorized participants into four groups based on their level of planning and follow-through:Non-Planners: More than two-thirds of those studied had not done any financial planning despite being close to retirement. Many had not even researched what to expect from Social Security. Simple Planners: This group at least considered their future financial needs and made basic calculations about saving for retirement. However, only about half of them created a tangible financial plan. Serious Planners: These individuals sought financial information and even paid for professional planning advice. However, like the previous group, about half failed to implement their plans. Successful Planners: The final group—only about 20% of those studied—both created and consistently followed a financial plan over many years.Even Small Steps Can Make a Big DifferenceOne encouraging takeaway from this study is that every step toward better planning leads to improved financial outcomes. Even moving from the “non-planner” to the “simple planner” category doubled or tripled net worth at retirement. Advancing to the “serious planner” level added another 25% to 35% in wealth accumulation.This demonstrates that financial planning isn’t an all-or-nothing proposition. Even taking small steps—like estimating future financial needs or using basic retirement calculators—can lead to significant benefits.Proverbs 21:5 reminds us, “The plans of the diligent lead to profit.” This timeless wisdom underscores the necessity of both planning and execution.If you haven’t started the planning process yet, or if you have a plan but aren’t consistently following it, research shows there’s substantial value in getting back on track. Tools like Sound Mind Investing’s MoneyGuide, or even free online retirement calculators, can be a great way to start.Long-term financial success doesn’t happen by accident—it requires both a solid plan and the discipline to follow through. Every step forward matters, whether you’re just beginning your financial journey or looking to refine your existing plan.For more insights, you can read the full article, “Planning and Execution: The Keys to Long-Term Financial Success,” at SoundMindInvesting.org.On Today’s Program, Rob Answers Listener Questions:I have a 401(k) contributing 8%, but my company stopped matching and moved to a pension system. Should I roll over my 401(k) to a Roth or annuity? The balance is around $32,000.I know we need to be generous with our money, and I want to do the same with God's money. So, I was looking into donating to St. Jude's Hospital and my local church. Is it possible to do both, or should I double down and donate all of it to my local church?I have an HSA and had to start Medicare 7.5 years ago. I read I can retroactively take out the Medicare Part B premiums I've paid from my HSA over those 7.5 years. Is that correct?My wife is 62, and we wanted to know if she should start taking Social Security now. We don't need the money for income; we would just invest 100% of it. We're not sure what the drawbacks would be.I'm 64 years old and have significant money in IRA CDs. I considered slowly withdrawing the money every year to increase my liquid assets. I understand that the money goes toward my annual income, but I wanted to know if there is another way to lessen the taxes I have to pay.Resources Mentioned:Faithful Steward: FaithFi’s New Quarterly PublicationSound Mind Investing | MoneyGuidePlanning and Execution: The Keys to Long-Term Financial Success (Article from Sound Mind Investing)Look At The Sparrows: A 21-Day Devotional on Financial Fear and AnxietyRich Toward God: A Study on the Parable of the Rich FoolFind a Certified Kingdom Advisor (CKA) or Certified Christian Financial Counselor (CertCFC)FaithFi App Remember, you can call in to ask your questions every workday at (800)

Ep 587Finding Joy and Peace in Financial Uncertainty

If you’re worried about your financial future, struggling to figure out how to pay for college, or feeling the pinch at the grocery store, you’re not alone. Financial challenges can make joy seem out of reach, but as Christians, we are called to face difficulties with a heart at peace.When financial worries—or struggles of any kind—overwhelm us, God’s Word offers wisdom and reassurance. Here are three biblical principles to hold onto in difficult times:Hardships are opportunities to grow in your faith.Joy and peace are not dependent on your circumstances.Your struggles have a purpose.Hardships Can Strengthen Your FaithThe book of James opens with a powerful challenge:"Consider it pure joy…whenever you face trials of many kinds, because you know that the testing of your faith develops perseverance." – James 1:2-3At first glance, this perspective on financial struggles might seem counterintuitive. Why would we consider trials to be beneficial? James isn’t saying that we should enjoy hardship itself but that through trials, God is shaping us into the people He wants us to be.James was writing to believers far from home, discouraged, and facing persecution—challenges far greater than most of us experience. Yet he reassured them:“The testing of your faith develops perseverance, and perseverance must finish its work so you may be mature and complete, not lacking anything.” – James 1:3-4Like muscles that grow stronger through resistance and tearing down before being rebuilt, our faith is strengthened through trials. Financial difficulties can either weaken our faith or push us closer to God, deepening our trust in His provision.Joy and Peace Are Not Dependent on CircumstancesFinancial struggles are a part of life, but joy is an attitude that looks beyond the pain and frustration of the moment. Nehemiah 8:10 reminds us:"The joy of the Lord is our strength."This joy isn’t based on how much money is in our bank account or whether our financial future is secure. Instead, it comes from knowing that our true security is in Christ.Similarly, peace isn’t dependent on our financial situation. True peace is found in the assurance that nothing can separate us from God’s love:“Neither height nor depth, nor anything else in all creation, will be able to separate us from the love of God that is in Christ Jesus our Lord.” – Romans 8:39This is the kind of peace that Philippians 4:7 describes as “surpassing all understanding.” It doesn’t make sense from a worldly perspective, but it is real and available to us when we place our trust in God rather than our financial stability.Does God Want Me to Be Happy?A common question people ask during financial hardship is, “Doesn’t God want me to be happy?” The assumption is that if God is loving, He would protect us from circumstances that cause discomfort or pain. However, this is a misunderstanding of God's character.God is not a cosmic Santa Claus who gives us everything we want to make life easy. Instead, He offers us something far greater—Himself. He created us for a relationship with Him, and true fulfillment is found when He is our greatest treasure.“Now if we are children, then we are heirs—heirs of God and co-heirs with Christ, if indeed we share in his sufferings in order that we may also share in his glory.” – Romans 8:17Happiness is fleeting, tied to external circumstances like economic trends, financial stability, and shifting emotions. But joy in Christ is constant, anchored in God's unchanging character. We can navigate any financial challenge with peace because He is always good, just, and loving.Your Struggles Have a PurposeNo trial is without meaning. God may allow financial struggles for several reasons:To strengthen our faith and deepen our dependence on Him. To reveal His love and provision as we trust Him. To redirect us when we’ve drifted off course.Romans 8:28 gives us a powerful promise:“And we know that in all things God works for the good of those who love him, who have been called according to his purpose.”Even in financial hardships, God is at work. He is refining us, drawing us closer to Him, and shaping us into the people He created us to be.Understanding these biblical truths can transform the way we approach financial challenges. When we recognize that hardships grow our faith, that joy and peace come from God rather than our circumstances, and that our struggles have a purpose, we can face uncertain times with confidence.No matter what financial difficulty you are facing today, remember this: God is with you, working all things together for your good. Trust in Him, and He will lead you to true joy and peace.On Today’s Program, Rob Answers Listener Questions:I'm helping a friend with about $4,000 in payday loan debt. Can Christian Credit Counselors help him get out of this debt?I'm 70 and approaching retirement. A well-known investment firm, Fisher, has offered to manage my IRA. I've always self-managed it and am a bit conservative. They say they can nearly

Ep 586Unlocking the Secret to Better Communication in Marriage with Kathleen Edelman

“Let each one of you love his wife as himself, and let the wife see that she respects her husband.” - Ephesians 5:33Love and respect are often conveyed in the words that spouses choose to communicate. Those words can have a big impact on the marriage relationship. Kathleen Edelman joins us to discuss choosing the right words for your spouse.Kathleen Edelman is the author of “I Said This, You Heard That: How Your Wiring Colors Your Communication.” She is certified in biblical studies and Christian Counseling Psychology and has spent over thirty years coaching clients in communication.The Key to Healthy Communication in MarriageCommunication styles are the key to understanding one another. There's a big gray area between what we say and what our spouse hears. Each temperament speaks its own language, and we must apply it to become fluent in our spouse’s language.Many marital conflicts appear to be about money, parenting, or household responsibilities, but at their core, they stem from miscommunication. Recognizing that your spouse’s temperament affects how they express and receive information is the first step toward reducing misunderstandings.One of the biggest communication pitfalls is assumption—assuming that your spouse speaks and understands your language. That’s not true. We each speak our own language and must become fluent in our spouse’s language.Another common trap is operating out of our weaknesses rather than our strengths. Ask yourself: “What part did I play in this miscommunication?”“How can I choose differently to stay in my strengths?”Most miscommunication is not intentional, she emphasizes. Rather, it’s a result of speaking different emotional and verbal languages.The Power of Words: Choosing to Build Up, Not Tear DownEphesians 4:29 reminds us:"Do not let any unwholesome talk come out of your mouths, but only what is helpful for building others up according to their needs, that it may benefit those who listen."Our words hold incredible power. They can either build up or tear down our spouse. Learning to communicate in a way that blesses rather than wounds is a game changer in marriage.Listening is a critical skill in communication, and there are three key practices for improving it:The Power of the Pause—Before responding, take a moment to reflect. Instead of reacting to what was said, focus on why it was said. Listening to Understand—Rather than formulating your response while your spouse is talking, actively listen to grasp their perspective. Responding, Not Reacting—Choose words carefully, ensuring they are constructive rather than defensive.We should desire that every word that comes out of our mouths be a gift to the person we speak to.Of course, it’s also crucial to remember that communication is more than words—it includes body language, tone, and facial expressions. Our temperament even affects how we express ourselves nonverbally. Everything you do is motivated by the design God gave you. Understanding how our spouse interprets our nonverbal cues can help avoid unnecessary misunderstandings.Understanding Temperaments in MarriageA significant takeaway from Kathleen’s work is the importance of understanding temperaments—both our own and our spouse’s. Kathleen’s book includes an inventory to help couples identify their temperament, which can be a game changer in communication.Each temperament has specific needs that shape how they engage in communication:Yellows (Sanguine)—Need fun, people, and spontaneity. They may struggle with feeling restricted.Reds (Choleric)—Need goals, control, and results. They want to be part of decision-making.Blues (Melancholic)—Need security and order. They may be hesitant to spend money without planning.Greens (Phlegmatic)—Need balance and peace. They want to avoid conflict and seek compromise.When couples recognize these differences, it fosters empathy and prevents unnecessary frustration.Money is a significant source of marital conflict, but these disagreements often stem from temperament differences more than financial realities.Yellows love generosity but also crave financial security. They may struggle with balancing saving and spontaneous giving.Reds want financial goals and a clear plan for achieving them.Blues prioritize security and tend to be more cautious with money.Greens seek balance and prefer avoiding financial stress.Understanding why your spouse approaches money how they do can foster mutual respect and teamwork. Instead of seeing their perspective as frustrating, you can recognize it as their God-given design.Keeping Communication Strong Over the YearsAs years pass, spouses may drift apart if they stop investing in communication. That’s why couples are encouraged to stay in dating mode:Remember why you fell in love. Remember when you were dating—you put your best of yourself forward. Keep doing that. Look for the best in your spouse. Instead of focusing on their weaknesses, celebrate their strengths. Avoid complacency. Once you become cont

Ep 585How to Keep Your Bank Accounts Safe from Fraud with Aaron Caid

With financial fraud on the rise, protecting your personal and banking information has never been more important. A recent JD Power study found that nearly 29% of bank account holders experienced fraud in some form over a 12-month period.To help us navigate the best security practices, Aaron Caid shares expert advice on how to safeguard your accounts from cybercriminals.Aaron Caid is the Chief Marketing Officer at Christian Community Credit Union, an underwriter of Faith & Finance. 1. Strengthen Your Password SecurityA strong, unique password is your first line of defense against fraud. Here’s how to create one that’s tough to crack:Use a mix of uppercase and lowercase letters, numbers, and special characters.Avoid using common words or easily guessed phrases (e.g., "password123" or your birthdate).Consider using a password manager to generate and securely store complex passwords.In addition to a strong password, enable two-factor authentication (2FA) for your financial apps. This extra layer of security requires a one-time passcode (usually sent via text or an authentication app) to verify your identity when logging in or completing transactions.Pro Tip: Turn off text message previews on your phone. If a scammer steals your phone, they could see your passcode on your lock screen and gain access to your accounts.2. Monitor Your Accounts & Stay Alert for FraudVigilance is key when it comes to detecting fraudulent activity early.Regularly check your bank accounts for unauthorized transactions.Review your credit reports through the three major bureaus—Equifax, Experian, and TransUnion—by visiting AnnualCreditReport.com.Sign up for transaction alerts from your bank or credit union to get notified of suspicious activity.Fraudsters also use phishing scams—fake emails, texts, or calls—to trick people into giving away personal information. These scams often create a sense of urgency to pressure you into acting quickly.Never share your:Username or passwordOne-time passcodesAccount or personal information over the phone, email, chat, or textHackers can spoof phone numbers and email addresses to make messages appear legitimate, even impersonating banks and credit unions. If you’re ever unsure, call your financial institution directly to verify any suspicious messages.3. Use Secure Wi-Fi & Protect Your Personal InformationWe all love a good coffee shop work session, but public Wi-Fi networks are a big security risk when accessing sensitive financial accounts. Hackers can intercept your data and steal your login credentials.Always use a secure, password-protected Wi-Fi network when banking online.Use a Virtual Private Network (VPN) for added encryption and security.Also, ensure you don’t let identity thieves find your personal information in the trash!Shred documents containing sensitive details like account numbers, social security numbers, or other financial information. Shredders cost as little as $35—a small price to pay for big security.Stay Secure & Bank with PurposeAs fraud prevention becomes increasingly important, many Christians are seeking banking solutions that align with their values. Christian Community Credit Union (CCCU) offers a Harvest Bundle—a unique checking and savings account designed to help members grow their savings while supporting missions worldwide.4% APY on the first $5,000 in Harvest Checking5% APY on the first $5,000 in Harvest Savings1.5% cash back on purchases with the Cash Rewards Visa CardA portion of proceeds supports missions, including gospel outreach, protecting vulnerable children, and fighting human trafficking. For those looking to align their banking with their faith, the Harvest Bundle from CCCU offers competitive rates and kingdom impact—a win-win for wise financial stewardship.If you're looking for a banking partner that reflects your faith and values, consider joining Christian Community Credit Union (CCCU).Ready to bank with purpose? Visit JoinChristianCommunity.com today!On Today’s Program, Rob Answers Listener Questions:Can you provide a list of the faith-based investments that I can invest in? I'm trying to invest differently with my 401(k) funds. I have an old work comp claim that was incorrectly billed, causing Medicare to deny payment. What happened, and how can I prevent this in the future? Also, if I submit a claim to the work comp company and they only pay a portion, am I responsible for the remaining balance? I own a free-and-clear home in Davenport. There is no mortgage anymore, and I would like to transfer 50% of ownership to a family member. Would I have to pay any taxes, or would my family members have to pay them because of this transfer? I'm retired, receiving $70,000 annually from disability and SSDI. I have $50,000 in a TSP account and $9,000 in debt that I'm paying off. I'm currently renting for $1,500 per month. Should I use my VA loan to purchase a home or just continue renting? I have a Roth IRA that I formed from a 403(b) annuity a couple of years ag

Ep 584Render Unto Caesar What Is Caesar’s

"So give back to Caesar what is Caesar’s, and to God what is God’s." - Matthew 22:21This statement from Jesus is one of the most profound and thought-provoking verses in the New Testament. While it is often quoted in discussions about paying taxes, it carries far deeper implications. What does this passage truly mean for us as Christ-followers today? Let’s explore its historical context and the spiritual truths that challenge us to live with a kingdom perspective.The Trap Set for JesusThe words of Jesus in Matthew 22:21 came during a tense confrontation between Him and the Pharisees. They sought to trap Him with a politically charged question:"Is it lawful to pay taxes to Caesar or not?"At that time, Israel was under Roman rule, and paying taxes to the emperor was a sore subject among the Jewish people. Saying “yes” would alienate Him from His Jewish followers, who resented Roman oppression. Saying “no” would paint Him as a revolutionary in the eyes of the Roman authorities.But instead of falling into their trap, Jesus turned the question back on them. He asked for a denarius—a Roman coin bearing Caesar’s image—and posed a question of His own:"Whose likeness and inscription is this?"When they answered, “Caesar’s,” Jesus delivered His famous response:"Give back to Caesar what is Caesar’s, and to God what is God’s."On a surface level, Jesus affirmed that people should fulfill their civic duties, including paying taxes. The coin bore Caesar’s image, signifying that it belonged to the government. By saying, “Render unto Caesar what is Caesar’s,” Jesus acknowledged the legitimacy of human authority.This teaching aligns with what the Apostle Paul later wrote in Romans 13:1-7, where he urged believers to submit to governing authorities, recognizing them as instruments of God’s order. Paying taxes, respecting laws, and contributing to society are responsibilities of every Christian.Yet, Jesus did not stop with Caesar—He introduced a deeper spiritual truth.What Belongs to God?Jesus followed His statement: "Render unto God what is God’s.” This raises an important question: What belongs to God?To answer this, we must look at Genesis 1:27, which tells us that humanity is made in the image of God (Imago Dei). Just as the denarius bore Caesar’s image and belonged to him, we bear God’s image—meaning our entire lives belong to Him.This truth calls us to complete surrender. While we owe taxes, respect, and obedience to earthly authorities, our ultimate allegiance is to God. He doesn’t just claim a portion of our income—He claims our hearts, minds, souls, and strength.Many people compartmentalize their lives, separating the "secular" from the "sacred." Work, finances, and citizenship belong to the earthly realm, while prayer, worship, and church belong to God. But Jesus’ teaching destroys this false divide.If everything belongs to God, then every aspect of our lives—including our work, relationships, finances, and civic responsibilities—should be offered to Him as an act of worship.By pointing to the coin’s image, Jesus subtly challenges us:Whose image do we bear? To whom do we belong? Where does our primary allegiance lie?This is not just a lesson about paying taxes—it’s about our identity and purpose in God’s kingdom.Jesus' words also highlight the temporary nature of earthly governments compared to God's eternal reign. Rome’s empire, like every human government, would eventually fall. But God’s kingdom is everlasting.This is why Scripture reminds us:"Our citizenship is in heaven, and we eagerly await a Savior from there, the Lord Jesus Christ." - Philippians 3:20"Do not store up for yourselves treasures on earth...but store up for yourselves treasures in heaven." - Matthew 6:19-20While we must live responsibly within earthly systems, we do so with the understanding that our true home is in God’s unshakable kingdom.Faithful Stewards in Both Realms"Render unto Caesar what is Caesar’s" is a call to faithful stewardship both in earthly and heavenly matters. As followers of Christ, we are called to:Honor our civic responsibilities (pay taxes, obey laws, engage in society). Live with eternity in mind (prioritizing God's kingdom above all else). Offer our whole lives to God (because we bear His image and belong to Him).As 1 Peter 2:9 reminds us, we are "a chosen people, a royal priesthood, a holy nation, God’s special possession." This identity should shape every decision we make, including how we manage our finances, serve others, and navigate our role in the world.Ultimately, Jesus' response was not just a clever answer to a political trap but a profound statement of divine truth.While we live in this world, we are not of it (John 17:16). Our ultimate purpose is not to accumulate wealth, power, or influence in earthly systems but to live in a way that reflects God's glory.So, as you navigate financial decisions, work responsibilities, and civic duties, ask yourself:Am I honoring God with everything I have? Am I living as a fai

Ep 583Is 2025 the Right Time to Buy or Sell A House? with Dale Vermillion

The real estate market may be in its winter slump, but spring is just around the corner—only five weeks away!Higher interest rates have kept many home buyers and sellers off the sidelines in recent years. But could a change be on the horizon? Today, mortgage expert Dale Vermillion joins us with a market forecast and some practical advice on how to move forward.Dale Vermillion is the author of Navigating the Mortgage Maze: The Simple Truth About Financing Your Home. This book covers everything you need to know about securing a mortgage—all from a biblical perspective.Is the Housing Market About to Shift?For the past few years, many homeowners have stayed put due to high interest rates, a phenomenon known as the lock-in effect. However, recent data suggests a shift might be on the horizon.Existing home sales rose by 6.1% in November 2024, signaling a potential increase in market activity. While December and January are traditionally slow, spring is expected to bring renewed momentum as buyers become more eager to move. Consumer confidence is growing, and as patience wears thin, many are deciding to buy now and refinance later.Should Buyers Accept Current Interest Rates?Many potential buyers have been waiting for rates to drop before making a move. But sometimes, waiting is no longer an option. Life goes on, and people need to relocate for jobs, family, or other personal reasons.That said, budgeting wisely is key. Before purchasing a home, we recommend:Assessing what you can truly afford Creating a solid budget to plan for mortgage payments Considering the long-term potential to refinance in a few yearsWhile mortgage rates remain higher than the record lows of a few years ago, waiting indefinitely for the “perfect” rate may mean missing out on opportunities.What to Expect From Interest Rates in 2025Many homebuyers have been banking on rate cuts to ease affordability, but will they actually happen?Only one or two rate cuts are expected in 2025, and even those are not guaranteed. The biggest factor influencing mortgage rates is inflation, which is tied to federal deficit control. Unlike previous periods of low mortgage rates, the government is unlikely to buy trillions in mortgage-backed securities to artificially lower rates.Bottom line: Mortgage rates are likely to stay between 6% and 7% for most of 2025, with a slight possibility of dipping into the high 5% range.Navigating the 2025 Housing MarketWhether you’re looking to buy or sell, market conditions are changing, and understanding them is crucial.For Sellers:Home values are flattening or declining in some areas. In Q3 of 2024, annual real estate appreciation dropped to 2.5% (an average of $5,700 per home), starkly contrasting with Q2’s 8% growth ($25,000 per home). If you’re considering selling, now may be the best time to maximize your home’s value before the market shifts further.For Buyers:Affordability should be your top priority. Home price appreciation may slow down in 2025, making it a good time to enter the market without facing rapid price hikes. While interest rates remain elevated, they will eventually decline, giving buyers a future opportunity to refinance. Homeownership still offers significant tax benefits, making it a worthwhile long-term investment.Mortgage Trends: What’s Changed?If it’s been a while since you’ve looked into getting a mortgage, you may be surprised by the range of options now available.New mortgage products cater to diverse financial situations. Credit challenges? There are more flexible loan options than before. Need down payment assistance? Programs exist to help qualified buyers.The housing market is shifting, and while interest rates may not drop dramatically, buyers and sellers alike have opportunities in 2025. For those needing to move, careful planning and budgeting will be essential. And for sellers, this could be a good time to capitalize on home values before potential declines.No matter your situation, making an informed, strategic decision is key, and consulting professionals can confidently help you navigate the mortgage landscape.For more expert insights on financing your home, check out The Mortgage Maze: The Simple Truth About Financing Your Home by Dale Vermillion.On Today’s Program, Rob Answers Listener Questions:I'm 37, with a family of five. I've been building a home on the property I bought three years ago, using cash so far. I have the funds for the roof this year, but I need to take out a loan or wait three more years to pay cash for the rest. Should I take out a loan to finish it sooner or wait and pay cash?I'm 56 and about to take early retirement with a $1,400 monthly pension. Then, I'll return to work in the private sector, making more. I have a 6% mortgage and a 7% HELOC. Should I invest or use the pension money to pay down my debts?I'm 76 years old and just finished a messy divorce. I have about $200,000 to invest, but I don't have a house, car payments, or significant debt. What should I do wi

Ep 582What Ecclesiastes Teaches Us About Life and Money

One book of the Bible reminds us that life is short and we should make the most of every moment.If you guessed Ecclesiastes, you’re right. This book emphasizes that our time here is fleeting, but what lies beyond is eternal. In this post, we’ll explore this profound truth and introduce a new FaithFi study on the book of Ecclesiastes—Wisdom Over Wealth: 12 Lessons from Ecclesiastes on Money.The Shortness of LifeImagine standing on the summit of Mount Everest, over 29,000 feet above sea level. At that moment, you are higher than every other person on the planet. But as breathtaking as the view may be, you can’t stay there long.At 26,000 feet, climbers enter the “death zone,” where oxygen is too thin to sustain human life. Even the most well-trained mountaineers must rely on oxygen tanks just to survive the final push to the peak. And when they reach the top, they have just five minutes—300 precious seconds—before they must begin their descent or risk never making it back.How do you think a climber should spend those five minutes? Complaining about an aching ankle? Wishing they hadn’t endured the brutal climb? Or should they take in the view, praise God for the beauty of creation, and appreciate the rare opportunity they’ve been given?Five Minutes On The SummitEcclesiastes teaches us that life is like having five minutes on the summit.We’re here for a short time. Many have come before us, and many will come after. Some moments in life are filled with sunshine and calm, while others bring fierce storms. But regardless of our circumstances, we have one brief chance to live and no do-overs.The book of Ecclesiastes repeatedly urges us to embrace this reality. Solomon, the author, reminds us that all earthly pursuits—wealth, pleasure, status—are ultimately fleeting. But rather than making us despair, this truth should inspire us to live with gratitude and purpose.Facing the Reality of Death to Find Joy in LifeEcclesiastes does not shy away from the topic of death. In fact, it is mentioned in 11 out of its 12 chapters. Solomon writes:"Remember also your Creator in the days of your youth, before the evil days come and the years draw near of which you will say, ‘I have no pleasure in them’… before the silver cord is snapped, or the golden bowl is broken, or the pitcher is shattered at the fountain, or the wheel broken at the cistern, and the dust returns to the earth as it was, and the spirit returns to God who gave it. Vanity of vanities, says the Preacher; all is vanity.” (Ecclesiastes 12:1, 6-8)Why does Solomon want us to think about death? Not to depress us—but to help us truly live. When we remember that our time is short, we learn to treasure each moment. If I know I have to leave the summit soon, I’ll savor every second. If I know death is coming, I’ll be thankful to be alive.The closing chapters of Ecclesiastes paint a vivid picture of aging and decline. Our eyesight dims, our strength fades, and our bodies slow down. But instead of fearing this reality, we’re encouraged to embrace it—to use the time we have wisely and to find joy in the life God has given us.Live With Eternity In MindOur new FaithFi study, Wisdom Over Wealth: 12 Lessons from Ecclesiastes on Money, explores how these lessons apply to financial decisions. Solomon warns us that wealth, like life itself, is temporary. Money cannot ultimately satisfy, and hoarding riches without purpose is meaningless.Instead, Ecclesiastes teaches us to steward our finances with eternity in mind. That means:Trusting God over material wealthUsing money to bless othersEnjoying the good gifts God provides without making them our ultimate pursuitAs Moses wrote in Psalm 90:12: “So teach us to number our days that we may get a heart of wisdom.”You are standing on the summit of life. You have five minutes.How will you spend them?Will you focus on fleeting troubles, or will you fix your eyes on the One who holds eternity in His hands?Ecclesiastes calls us to live with purpose—to love God, love others, and make the most of every moment. When the expedition leader, God, taps us on the shoulder and says, “It’s time to go,” may we be found faithful.We've only begun to explore the depth of this powerful new study, Wisdom Over Wealth: 12 Lessons from Ecclesiastes on Money, coming next month. Once it's available, you can find it at FaithFi.com/Shop.On Today’s Program, Rob Answers Listener Questions:I'm 73 and self-employed. Five years ago, I left my house for my daughter, who had thyroid cancer. The house could rent for $3,000/month, but I'm not getting any of that. Is there a way I can get a tax deduction or deferment for this situation?My credit score has gradually decreased from around 780 to 720, even though I always pay my bills on time. I'm unsure why this is happening since I have a mortgage, and my housing payments are half my income. What could be causing my credit score to go down?I'm 58 on disability and only get $1,300 a month. If something happened to my husband, I

Ep 581Aligning Your Financial Goals with God’s Purpose with Rachel McDonough

“The purpose in a man's heart is like deep water, but a man of understanding will draw it out.” - Proverbs 20:5Man’s ultimate purpose is to glorify God, but deciding how to do that can be challenging. Sometimes, we need help from a trusted advisor. I’ll discuss that today with Rachel McDonough. Rachel McDonough is a Certified Financial Planner (CFP®), a Certified Kingdom Advisor (CKA®), and a regular Faith & Finance contributor.The Cultural Challenge: Are We Asking the Right Financial Questions?Money is more than just a tool—it’s a reflection of our values, priorities, and ultimately, our faith. But how do we ensure that our financial decisions align with God’s purpose for our lives?As believers, we all want to honor God with the resources He has entrusted to us. However, navigating financial decisions can be overwhelming—especially when culture pushes us in the opposite direction.Traditional financial planning often starts with one simple question: “What are your financial goals?”At first glance, that sounds logical. But the problem? It starts with us—our dreams, our desires—rather than seeking God’s plan first.Many people feel pressure to already have their financial goals figured out. If they don’t, they may experience anxiety, uncertainty, or even guilt. Instead of feeling liberated, they feel like they’re failing.So, how do we shift from “What do I want?” to “What does God want for me?”The Heart of Financial Planning: Start with Your ValuesTake a step back before setting financial goals. Instead of ready, aim, fire—we should first seek to understand:Our values – What matters most in this season of life? Our priorities – How should we allocate resources to reflect these values? God’s purpose – What is He calling us to pursue financially?As Paul David Tripp once said:“The thing that is your treasure will control your heart, and what controls your heart will control your words, your behaviors, your choices, and your decisions.”If we start with financial goals before examining our hearts, we risk aiming at the wrong target.A Real-Life Example: Aligning Values with Financial DecisionsRachel shared a story about a couple who initially sought financial advice because they wanted to:Build a cabin on a parcel of land they owned. Renovate part of their house to improve their living space.Sounds reasonable, right? But as they went through a values discovery exercise, something surprising happened.The wife valued respect and security, yet she was deeply stressed in her job, to the point of tears during their financial planning session. The husband valued loyalty and family, which made watching his wife suffer painful for him.After reflecting on their true priorities, they realized now was not the right season for a cabin. Instead, they needed a financial plan that allowed the wife to:Move into a less stressful job (even if it meant earning less) Find financial stability while navigating a large inheritance Postpone the cabin to a future season once their immediate needs were metThe outcome? A plan that prioritized peace, purpose, and financial security—without regret.The Role of a Certified Kingdom Advisor (CKA®)Many financial advisors focus solely on wealth accumulation and goal-setting. But a Certified Kingdom Advisor (CKA®) brings a biblical perspective, asking questions like:“What do you think God is calling you to pursue in this season?” “Do you need more income or more impact?” “What does surrender look like in your financial life?”This kind of financial planning frees people from guilt and regret. Instead of chasing worldly success, they begin pursuing God’s best for their lives.Aligning values with financial goals isn’t just a nice idea—it requires practical steps. In the case of Rachel’s story from earlier, their financial strategy included:The wife transitioning to a lower-stress, lower-income job. The husband re-entering the workforce to ease financial pressure. Using their inheritance wisely to cover healthcare costs before Medicare kicks in. Delaying the cabin goal until it was a better fit for their priorities.Their financial decisions became intentional—not just reactionary.The Fruit of Biblical Financial PlanningWhen people approach financial decisions with a heart of surrender, the results are transformational. The fruit we see in people who adopt this mindset is:Freedom from regret Peace and joy in their financial journey Stronger relationships as they align finances with God’s planYou're not alone if you’ve ever felt uncertain about your financial goals. Instead of feeling pressured to have it all figured out, take a step back and ask:What are my core values? What is God’s purpose for my finances? Am I making financial decisions out of trust or fear?And most importantly:How can my money reflect what’s most important to me as a Christ-follower?If you’re looking for a biblical approach to financial planning, consider working with a Certified Kingdom Advisor (CKA®)—a professional trained to help yo

Ep 578How to Choose a Trustworthy Tax Preparer This Tax Season

The holidays are behind us; you know what that means—it’s tax season! But before you start gathering your W-2s and receipts, there’s an important question: Do you know who will prepare your taxes this year?With a nationwide shortage of Certified Public Accountants (CPAs) and tax professionals, waiting too long to find a preparer could leave you scrambling—and vulnerable to scams. Here’s how to protect yourself and find a trusted tax preparer.Who Can Prepare Your Taxes?When hiring a tax professional, your preparer will likely fall into one of three categories:Certified Public Accountant (CPA): These professionals undergo rigorous education, exams, and licensing requirements. Many specialize in tax preparation and can also provide broader financial guidance. Enrolled Agent (EA): Licensed by the IRS, EAs are tax experts who can prepare and file returns, represent clients before the IRS, and provide tax planning services. Tax Attorney: These legal professionals specialize in tax law and are particularly useful for complex tax situations, audits, or disputes.Each of these professionals is highly qualified—but the problem is there aren’t enough of them.There is a growing shortage of CPAs and tax professionals, mainly because fewer young people are entering the field. Some firms are even hiring high school interns at $22 an hour to recruit future CPAs.What does this mean for you?Longer wait times to book a tax preparerHigher fees due to increased demandGreater risk of falling into the hands of fraudulent preparersWhen people are desperate to file their returns, they can become easy targets for scammers who fake credentials or engage in tax fraud.How to Avoid Tax Scams and Find a Qualified PreparerTo protect yourself, follow these IRS-recommended steps when choosing a tax preparer:1. Choose a Year-Round Tax PreparerA reputable preparer should be available beyond tax season. You don’t want your tax preparer to disappear if you get audited.2. Verify Their IRS CredentialsAsk for the IRS Preparer Tax Identification Number (PTIN). All paid tax return preparers must register with the IRS and enter their PTIN on every return they file.Check their status using the IRS Directory of Federal Tax Return Preparers at IRS.gov.3. Look for Professional CredentialsAsk if the preparer holds a credential such as:CPA (Check with the State Board of Accountancy)Enrolled Agent (Verify at IRS.gov under "Verify Enrolled Agent Status")Tax Attorney (Confirm with their State Bar Association)Additionally, inquire about continuing education—since tax laws change frequently, professionals should stay current.4. Be Cautious About FeesBeware of tax preparers who:Charge fees based on a percentage of your refundClaim they can get you a larger refund than competitorsA legitimate preparer should charge a flat or hourly rate based on the complexity of your return.5. Verify IRS E-File CapabilityMost tax preparers handling more than 10 clients must file electronically. If your preparer refuses to e-file, that’s a red flag.6. Ensure Proper DocumentationA trustworthy tax preparer will ask for the following:Your W-2 and 1099 forms (not just a pay stub)Records of deductions and creditsIf a preparer doesn’t ask for supporting documents, walk away. The IRS requires proper documentation to verify your return.7. Understand Representation RulesOnly CPAs, Enrolled Agents, and tax attorneys can represent you before the IRS if you're audited.Non-credentialed tax preparers—including your math-savvy cousin Bill—cannot represent you in an audit.8. Never Sign a Blank or Incomplete Tax ReturnPlease review your return carefully before signing. Ensure all information is accurate, and ask questions if anything appears incorrect.9. Your Refund Should Go to You—Not the PreparerCheck the routing and account number on your tax return to ensure your refund is deposited into your own account, not your preparer’s.Looking for a Faith-Based Financial Professional?If you want to work with a tax professional who aligns with biblical financial principles, consider finding a CPA, Enrolled Agent, or tax attorney with the Certified Kingdom Advisor (CKA®) designation.To find a trusted, faith-based financial professional, visit FaithFi.com and click “Find a Professional.”With tax season here, choosing a reputable, qualified tax preparer is more important than ever. Don’t wait until the last minute—start your search today to avoid scams and ensure your taxes are filed accurately and ethically.On Today’s Program, Rob Answers Listener Questions:As I turn 70 and a half, is it advantageous for me to start doing my charitable giving from my IRA? Or should I wait until 73, when I have to do the required minimal distribution (RMD)?I have $10,000 in a savings account with my local bank, but I only earn about 10 cents in monthly interest. Since I've never invested before, I'm interested in investing that money elsewhere to create some extra available money. What would you suggest?I ran a landscaping

Ep 580Transforming the Lives of the Poor with Kelly Miller

“Whoever has a bountiful eye will be blessed, for he shares his bread with the poor.” - Proverbs 22:9Do you have a generous heart—one that seeks out opportunities to bless others, especially those in need? Today, Kelly Miller joins us to share a powerful way you can not only support the poor around the world but also help bring lasting transformation to their lives.Kelly Miller is the CEO and President of Cross International, an underwriter of Faith & Finance. The Global Crisis: Hunger, Clean Water, and PovertyPoverty remains a critical issue around the world, affecting millions of families who struggle to access basic necessities like food, clean water, and education.The numbers are staggering:Over 800 million people go hungry every day.More than 50% of child deaths are linked to hunger-related issues.Nearly 700 million people lack access to safe and clean water.Cross International is a faith-based humanitarian organization dedicated to transforming the lives of impoverished individuals and families worldwide. It is on the front lines, working in over a dozen low-income countries to meet these urgent needs while also addressing the deeper spiritual transformation that brings lasting hope.The Mission of Cross InternationalFounded in 2001, Cross International partners with local Christian ministries to provide essential resources to struggling communities. Their mission is to provide food, water, and shelter and transform lives through the love of Christ.The organization primarily serves Latin America and regions of Eastern and Southern Africa, where the need is particularly dire. Through local partnerships, they empower communities by offering:Nutritious meals for childrenClean drinking waterEducational opportunitiesDiscipleship and spiritual developmentBeyond Humanitarian Aid: Transforming Lives Through ChristCross International goes beyond simply meeting physical needs—they focus on long-term transformation. One example of this is their Thriving Kids Initiative, which ensures children not only receive food and education but also grow in faith and purpose.Take Kenny, a young man from rural Malawi. He grew up in extreme poverty, with little access to food or education. Through Cross International’s partnership with local ministries, Kenny was able to attend school and receive his only meal of the day—a nutritious meal provided through the program.Over the years, Kenny has thrived academically, and today, he is a university student in Malawi. He dreams of returning to his village, starting a business, and helping lift others out of poverty. His story is just one of many transformed lives through the work of Cross International.How You Can Help: Become a Thriving Kids AmbassadorThe impact of your generosity can be life-changing. For just $62, you can provide:Life-saving food and waterEducational opportunitiesSpiritual nourishment through the GospelYour gift can make an eternal difference in a child's life. Consider becoming a Thriving Kids Ambassador by giving today.Every gift of $62 helps a child not only survive but thrive through the love of Christ. To join this mission, visit crossinternational.org/faith. On Today’s Program, Rob Answers Listener Questions:My problem isn't necessarily with the credit cards. This year, I have financed three reasonably large items, including a used RV that I financed for $17,000 at 10.99% interest over 15 years. If I wait to pay it off for the entire 15 years of the loan, the total cost will triple or even more. How can I pay off this RV more quickly with the resources I have left?I'm in a tough financial spot with debt and no money, and I'm not sure if I should file for bankruptcy or keep trying to pay it off. I want to honor God with my finances, but I'm really struggling.I'm interested in the advantages and disadvantages of creating a trust with money we have after the passing of a loved one, as opposed to investing the money in mutual funds. Since I'm unsure of our intentions for the money, I'm trying to determine whether a trust is the better option or whether I should invest it in mutual funds.I have a $400,000 rental property with $60,000 left on my home mortgage. The rental brings in $1,800 per month. Should I sell the property, use the proceeds to pay off my debts, and invest the remaining $340,000, or should I continue renting the property until I'm 65?Resources Mentioned:Faithful Steward: FaithFi’s New Quarterly PublicationCross InternationalLook At The Sparrows: A 21-Day Devotional on Financial Fear and AnxietyRich Toward God: A Study on the Parable of the Rich FoolFind a Certified Kingdom Advisor (CKA) or Certified Christian Financial Counselor (CertCFC)FaithFi App Remember, you can call in to ask your questions every workday at (800) 525-7000. Faith & Finance is also available on Moody Radio Network and American Family Radio. You can also visit FaithFi.com to connect with our online community and partner with us as we help more people live as faithful stewa

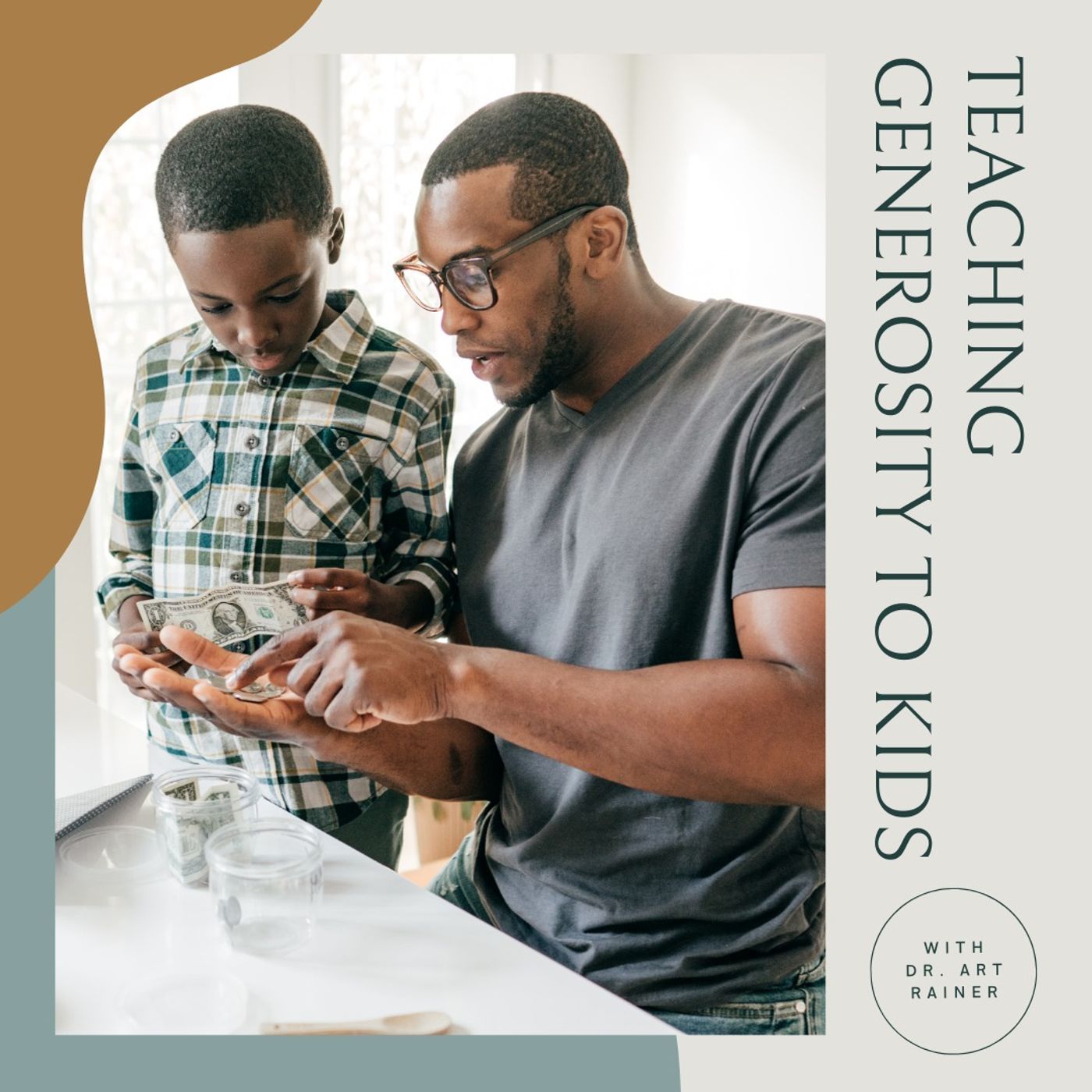

Ep 579Teaching Generosity to Kids with Dr. Art Rainer

“I have no greater joy than to hear that my children are walking in the truth.” - 3 John 1:4In that verse, the Apostle John praises his friend Gaius and other believers for their generosity toward missionaries. As parents, we want our children to be generous toward God’s Kingdom. Dr. Art Rainer joins us today with some steps we can take to grow our kids in generosity.Dr. Art Rainer is the founder of the Institute for Christian Financial Health and Christian Money Solutions. He is also the author of The Money Challenge: 30 Days of Discovering God's Design for You and Your Money and the Secret Slide Money Club, a book series designed to teach young readers about God’s way of being wise with money. Why Teaching Generosity MattersParenting is a high calling. Everything we say and do influences our children’s lives, shaping their worldview and their relationship with God. Generosity is part of God’s plan for His people, so we must intentionally guide our kids away from selfishness and toward selflessness.But how do we teach children to be generous when human nature tends to favor holding on rather than giving away? It starts with a few key principles.1. Model GratefulnessBefore kids can learn to give, they must first recognize the blessings they’ve received. A heart of gratitude fosters a heart of generosity.Regularly express thankfulness for the resources God has given your family. Teach your children that everything belongs to God—we are simply stewards of His gifts. Share stories of how generosity has impacted your own life and how giving frees us from the grip of money.Gratefulness leads to an open-handed posture toward money and possessions.2. Talk About GenerosityChildren won’t naturally connect giving to their faith unless we explain it to them. Conversations about generosity help shape their understanding of why we give.Explain that we give because God first gave to us (John 3:16). Share personal testimonies of times when generosity blessed others—or when you were blessed by someone else’s generosity. Connect giving to the gospel: Just as God gave us His Son, we reflect His love when we give to others.3. Model Generosity in Everyday LifeKids have a strong radar for hypocrisy. If we talk about generosity but don’t practice it, they’ll notice. That’s why we must demonstrate generosity in tangible ways.Let them see you giving—to your church, to charities, or to people in need. Discuss the needs of others. Ask them, “Have you ever needed help? How did it feel when someone helped you?” Involve them in acts of giving, such as donating food, helping a neighbor, or supporting a ministry.When children witness generosity in action, they begin to understand its value.4. Let Them Earn and GiveFor kids to truly grasp generosity, they need to experience both the sacrifice and joy of giving. One way to do this is by allowing them to earn their own money.Provide opportunities for them to do small jobs or earn an allowance. Encourage them to set aside a portion for giving, just as they do for saving and spending. Let them choose where to give—whether it’s to the church, a missionary, or a local charity.Handling their own money makes giving more meaningful and personal.5. Prioritize Giving to the Local ChurchOne of the best ways to instill a habit of generosity is by encouraging children to give to their church.Introduce them to pastors and missionaries so they can see how their giving impacts the Kingdom. Show them how to give—let them physically place money in the offering plate rather than only giving online. Reinforce that their giving contributes to something much bigger than themselves.6. Encourage Giving with Joy, Not GuiltGiving should be joyful, not forced. Pressuring kids to give out of obligation can lead to resentment rather than a cheerful heart. Instead, celebrate their generosity and show them the blessings that come from giving freely.As 2 Corinthians 9:7 reminds us, “God loves a cheerful giver.”Raising generous children requires intentionality. By modeling gratefulness, discussing generosity, and providing opportunities for them to give, we can help shape their hearts to reflect God’s generosity.Want to dive deeper into this topic? You can read more in Faithful Steward, FaithFi’s brand-new quarterly publication that equips families to align their faith and finances for God’s glory.To start receiving Faithful Steward every quarter, become a FaithFi Partner by giving $35 or more per month or $400 annually. Visit FaithFi.com/give to partner with us and receive this inspiring publication delivered right to your mailbox.On Today’s Program, Rob Answers Listener Questions:I have a 401(k) with about $128,000 in it, and I'd like to invest $60,000 into an annuity. The person I talked to said I would get an 8,600-dollar bonus immediately if I invested the $60,000. He also said I could take out 20% of the annuity after two years. What do you think about this annuity option?I am 51 years old. I retire at the end of ne

Ep 577Navigating Giving with an Unbelieving Spouse with Ron Blue

You want to give generously to your church, but your non-believing spouse objects. What do you do?We occasionally get that question, and it’s a situation that must be handled with care. If you or someone you know is in that position, don’t miss today’s program, as Ron Blue is here with some sage advice.Ron Blue is the co-founder of Kingdom Advisors and the author of many books on biblical finance, most notably “Master Your Money: A Step-by-Step Plan for Experiencing Financial Contentment.”Biblical Principles for Giving in MarriageThere are two key biblical principles to consider when navigating giving disagreements in marriage:Marriage is more important than money. While generosity is an important biblical value, unity in marriage takes precedence. Submission and honor in marriage matter. Ephesians 5:21 reminds us to “submit to one another out of reverence for Christ,” emphasizing mutual respect in financial decisions. Likewise, Matthew 19:6 affirms that a husband and wife “are no longer two, but one flesh. What therefore God has joined together, let not man separate.”Ultimately, financial decisions—including giving—should be made together, with mutual understanding and agreement.Ron’s Personal Story: When His Wife Wanted to TitheRon has firsthand experience with this issue. When his wife, Judy, became a Christian, she wanted to tithe. But at the time, Ron was not a believer and giving was the last thing on his mind.Instead of forcing the issue, Judy decided to remain silent about it for two years. However, she lived a transformed life, which was compelling to Ron. Her quiet witness ultimately softened his heart and led him to faith in Christ.This aligns with the biblical wisdom of 1 Peter 3:1-2, which encourages wives to live in such a way that they may win their husbands to Christ “without a word, by the conduct of their wives, when they see your respectful and pure conduct.”Judy’s patient, godly approach allowed Ron to come to faith in his own time, and ultimately, they found joy in giving together.Building Unity in Giving as a CoupleOnce Ron became a Christian, he and Judy intentionally set aside time to align their financial goals—including giving. Twice a year, they would take a weekend away to pray, discuss their finances, and determine their giving goals.Ron’s perspective on giving is clear:The tithe is a starting point. Giving should go beyond the tithe, as generosity is a way to break the grip of money on our hearts. Giving should be joyful and unified. When spouses give together in agreement, it becomes a source of great joy.As Ron says, “The only way you can break the power of money is to give.”Practical Steps for Couples Navigating Giving DisagreementsIf you and your spouse are struggling to agree on giving, consider these steps:Prioritize your marriage. Remember, God values unity in your relationship more than any specific financial contribution. Listen openly. Take time to truly hear your spouse’s concerns and seek to understand their perspective. Share why giving is important to you. Explain what generosity means to you personally and spiritually. Find a giving framework you both can support. This might mean starting small, gradually increasing giving over time, or designating funds for causes you both agree on.At the end of the day, God doesn’t need our money—He wants our hearts. And He wants our marriages to reflect His love and unity. If you and your spouse are wrestling with this issue, focus first on fostering understanding and alignment. When you give together with a joyful heart, the blessing is even greater.If you’d like to read more on this topic, Ron Blue’s full article on this subject is featured in our new quarterly publication, Faithful Steward. To receive it in your mailbox every quarter, become a FaithFi Partner at $35 a month or $400 annually at FaithFi.com/give.On Today’s Program, Rob Answers Listener Questions:My husband's business distributing for a bread company has fallen apart. He was forced to resign, and they slandered his name. We only have $300 left and had a small business loan. What should we do?I received a letter in the mail stating that my student loans were put on some kind of permanent disability that I had never applied for. The letter mentioned being affiliated with a teacher, but I'm not a teacher. I don't know if this is a scam or if it's legitimate. What should I do?I'm calling to learn how to help my 20-year-old granddaughter start building credit. She needs to get a credit card and establish a credit history to buy a car in the fall. She works full-time but doesn't have any credit history yet. What's the best way for her to start building credit?I'm 55 years old and plan to retire in about 10 years. I recently filed an insurance claim for roof damage from a hurricane, but the claim was denied. Should I use the money in a money market account to replace the roof, or should I get an equity loan from the bank to pay for it?Resources Mentioned:Faithful Ste

Ep 576How Asking For Help Glorifies God